Se encuentra usted aquí

Agregador de canales de noticias

The 2020 Olympics will be memorable, but not in the way Japan hoped

Even if disaster is averted, a sense of national renewal will remain elusive

Categorías: 3 Noticias economicas ingles

Japan is struggling to keep covid-19 at bay at the Olympics

It has banned spectators and fraternising among athletes, among other things

Categorías: 3 Noticias economicas ingles

Estructura de hierro

Hola a tod@s !! Tenía una duda... Tengo una estructura de hierro forjado para un acuario de 212 litros y mi duda era si al no llegar a cubrir toda la base, podría aguantar el peso del acuario según está en la foto? Muchas gracias

Categorías: Metalurgia, forja y fundicion

1985-2021: XAU Velocity Indicator

Below is the Velocity Indicator for the Philadelphia Gold and Silver Stock Index (XAU).

Categorías: Blogs y opiniones de economia en ingles

1985-2021: XAU Velocity Indicator

Below is the Velocity Indicator for the Philadelphia Gold and Silver Stock Index (XAU).

Categorías: Blogs y opiniones de economia en ingles

Market X-Ray: Want to Invest in Infrastructure? Consider These Stocks

Categorías: Blogs y opiniones de economia en ingles

1982-2021: BSE Sensex Velocity Indicator

Below is the Velocity Indicator for the BSE Sensex Index. For the dates that are listed on the Velocity Indicator, we have outlined the price levels on the BSE Sensex Index: 1988-2004 2003-2021 Observations In general, the dates provided at … Continue reading →

Categorías: Blogs y opiniones de economia en ingles

1982-2021: BSE Sensex Velocity Indicator

Below is the Velocity Indicator for the BSE Sensex Index. For the dates that are listed on the Velocity Indicator, we have outlined the price levels on the BSE Sensex Index: 1988-2004 2003-2021 Observations In general, the dates provided at … Continue reading →

Categorías: Blogs y opiniones de economia en ingles

What We're Reading

“Just think about it,” the luminary told me. “It’s nearly impossible to spend a billion dollars.” I laughed at the ridiculousness of this statement, but he went on, doing the math in front of me to make his point. “The most expensive Gulfstream jet in the world is $65 million; a couple of very fancy houses will cost you $20 million, $30 million total; many of the highest-end cars are only a few hundred thousand dollars each. You’ve done all that and you’ve still got around $900 million or so left to spend.” I responded, “Well, you could just give it away to people and organizations in need.” “Ahh, but you can’t,” the man said to me. “Are you just going to hand it to someone and hope they do the right thing with it? You have to build entire infrastructures to give the money away.” He went on to explain that you need to hire legions of people, often hundreds, including teams of lawyers and tax lawyers, finance experts, project managers, communications staffers, and so on, to manage the distribution of the money. “Just look atWarren Buffett.Rather than figure out how to give his money away, he just gave it to the Gates Foundation to do it for him.” Then, the man explained, there is the “problem” that your billions will only grow, often quicker than you can give them away, with interest and rising investments. “Being a billionaire is a lot harder than it looks,” the man said.

Fees:

[Realtory] Commission revenue – the cut that brokers collect for helping buy and sell homes – is on track to surge 16% in 2021, surpassing $100 billion for the first time.

They say the “days go slow but the years fly,” and as I sit here stewing in my worries, I can’t help but reflect on just how fast my life is going.

My 20s were a blur. I met my wife and we got married. As we entered our 30s, we knew we wanted to start a family. After that period of time, it seems like someone pushed fast forward.

If I could map my life from the moment my son was born to its end and compress it into one 24-hour period, it would probably look like this.

At 18, Mr. Daemen will be the youngest person ever to go to space. At 82, Ms. Funk, who goes by Wally, will be the oldest.

Have a good weekend.

Categorías: Blogs y opiniones de economia en ingles

Revolution in the Air

Welcome to another issue of Net Interest, my newsletter on financial sector themes. If you’re reading this but haven’t yet signed up, join 21,000 others and get Net Interest delivered to your inbox every Friday by subscribing here 👇

Revolution in the AirAs a finance newsletter, we touch on fintech here a lot. We’ve looked in detail at a host of new entrants into financial services – Wise, Tinkoff, Paytm, Robinhood – all of them attempting to disrupt the traditional way of doing finance. This week, we turn our attention to one I’m particularly close to: Revolut.

I first came across Revolut in 2016 when an early investor showed me around its app and the backend dashboard he had access to. I used to travel a lot and the opportunity to access cheap foreign exchange via a payment card was very appealing. I signed up as a customer and – as the app informs me today – went on to spend £6,438 on my travels through the remainder of the year.

I knew that if I found the app useful, others would too; I was keen to invest. A short while later the company was out raising its series A and I got the opportunity to participate.

This week, Revolut became the UK’s most valuable private tech company of all time. It announced a series E fundraising, valuing it at $33 billion. That puts it roughly on a par with NatWest Group, the bank where I had my first account as a kid.

The massive growth of Revolut is clearly very exciting for me as an investor. But it also raises questions. Last year, NatWest did £11 billion of revenue; Revolut did £261 million. NatWest is on track to make £2.5 billion of profit; Revolut may or may not make a profit. Revolut has a few more customers than NatWest – 16 million versus 12.5 million – but what are those customers worth?

It’s time to sharpen my pencil and update my analysis of Revolut.

Personal Money CloudRevolut was founded at the end of 2013 by CEO, Nikolay Storonsky and his co-founder Vlad Yatsenko. Like the founders at Transferwise, discussed here a few weeks ago, the pair were fed up with the charges banks levied on foreign currency transfers. While Transferwise initially focused on making it cheaper to send money back home, Revolut focused on making it cheaper to spend money abroad. Storonsky recalls how he suffered around $2,000 of hidden foreign exchange transaction fees on a trip to the US from his home in the UK.

However you cut it, both markets are large. Revolut estimates that combined, the markets are worth £190 billion in the UK and Europe and ten times that globally. In the world before Covid, people used to travel abroad a lot and they spent money when they went. Revolut estimated that in its initial target market of the UK, more than three quarters of the population went away in the twelve months prior to launch, spending an average £220 per trip. The company’s proposition was that it could save these people from having to pay bank fees on their holiday spend.

The focus on spend meant that Revolut needed to launch with a payment card. In July 2015, it came to market with a prepaid Mastercard issued by Paysafe. The card allowed customers to hold funds in GBP, Euro and USD, and to spend online and in-store with a globally accepted multi-currency MasterCard linked to their Revolut account. A virtual card was available for online purchases as soon as the account was set up and a physical card was dispatched shortly afterwards. Customer funds would be ring-fenced in accounts at Barclays.

At that stage, Revolut was just an app – the infrastructure was provided by others like Paysafe, Mastercard and Barclays. But as an app, it offered an effortless and well-designed solution to multiple consumer pain points: transferring money across currencies, spending money abroad and tracking transactions.

The revenue model was to exploit the spend side of the business to capture a share of the merchant interchange fees earned when customers use their cards. Initially, the company offered currency exchange and money transfers up to £500 for free. Later, it extended the terms of free currency exchange. However, the economics didn’t really add up. In Europe, debit interchange fees are capped at around 0.20% of the value of the transaction – not enough to cover the cost of free foreign exchange. So Revolut was on the hunt for new revenue streams.

The original model had the hunt fulfilled by subscription fees. Revolut’s seed pitch deck projected £5.7 million of revenue three years after launch, of which over £5 million would come from subscriptions – enough for it to make a profit. It estimated that around 30% of customers would pay around £165 a year in subscriptions. Sure enough, it did launch a subscription product right about then. However, by this time, the strategy had shifted; the important thing wasn’t to hunt for revenue streams, it was to hunt for more customers.

Global Money AppIn its seed deck, Revolut projected 140,000 customers three years out. It got there in nine months. Through viral referral campaigns, Revolut was able to pick up customers very quickly. Media helped: the company featured in the press and on TV. It also moved into new markets early, with 10% of its customers coming from France very soon after it launched there.

Today, the company is in 35 countries and has 16 million customers. It’s a big number, but many of its accounts are likely to be dormant. Third party data (Apptopia) suggests that in June, the app had 3.4 million monthly users and 1.3 million daily users globally.

Revolut’s biggest market remains the UK (19% of monthly average users) where in 2020 it booked 88% of its revenue. Other big markets include Ireland (12% of monthly average users) where 1 in 2 adults is a customer; Romania (10% of monthly average users); and France (7.5%).

Revolut launched in the US in March 2020, and had seen 200,000 customers sign up by year end; total downloads are now running at more than twice that, but monthly average users lag at around 135,000 as of June. Its target market in the US is the 40-45 million people who aren’t originally from the US, who may have greater demand for a multi-currency account and are more likely to want to send money abroad.

a.image2.image-link.image2-478-733 { padding-bottom: 65.21145975443383%; padding-bottom: min(65.21145975443383%, 478px); width: 100%; height: 0; } a.image2.image-link.image2-478-733 img { max-width: 733px; max-height: 478px; }The rapid growth in customer numbers has led to some growing pains at Revolut. Customers complain about funds getting frozen and accounts being closed as anti-money laundering systems pick up too many false positives while customer service is insufficiently resourced to pick up the pieces. In the first nine months of 2020, Resolver, an online complaints service, received almost 4,000 complaints about Revolut, after getting nearly 2,500 for the whole year before.

In addition, in 2019, Wired painted a picture of a toxic work culture where staff turnover was rife. That issue was tackled with a governance overhaul that led to the arrival of several new non-executive directors. The customer issue still rankles with many.

Nevertheless, with customers come revenues, albeit still of the capped interchange variety and not sufficient to support the business. By the time of the series A round in 2016, the 2017 revenue projection had been upgraded from £5.7 million to £10.0 million. The actual outturn was £12.8 million. But yet again, profits were pushed out. The series A deck pushed breakeven back a year to 2018; three years on, the company has yet to report a profit over a sustained twelve month period.

It claims to be getting close, though. In 4Q2020, Revolut reported an adjusted operating loss of £6 million, underpinned by profits in November and December. Subscriptions provide a ballast. In the UK, the company offers three tiers of subscription: plus (£30 per year), premium (£72 per year) and metal (£120 per year). They offer varying limits on no-fee ATM withdrawals, no fee currency exchange (the lower tier is limited to £1,000 per month), and the number of free international payments. Last year, subscriptions contributed £75 million to total revenue, with 14% of new customers taking a paid subscription.

The biggest revenue upside is from new products. Revolut has been a machine at rolling out new products. In 2020 alone, it launched 15 new products and innovations for retail customers. These include interest-bearing savings vaults, open banking, gold and silver trading, junior accounts, cash gifting, rewards, bill sharing, subscription management tools, salary advance and new crypto tokens.

According to the CEO, shipping products fast is important:

“It’s our secret weapon, right, it’s how we compete with other companies. Because ultimately all… businesses, what they do, they give products to people and then the faster you can ship products, the faster you can iterate on products, so the more chances that you will win. As a result, [in the] last 5-6 years, we just perfected the speed – and we pay so much attention to speed and quality of the product – because ultimately, product wins.”

In its rush to deliver product, the company is not embarrassed to mimic others. Its salary advance product is based on a product offered by companies such as Salary Finance, Wagestream and Level Financial Technology [disclosure: I am an investor in Level]. It is in the process of rolling out social trading similar to what is offered by eToro (discussed here). In the future, it has ambitions to pull together its retail ecosystem with its business ecosystem (500,000 customers) to allow businesses and consumers to transact without intermediaries. Sounds a bit like Square.

a.image2.image-link.image2-825-1456 { padding-bottom: 56.66208791208791%; padding-bottom: min(56.66208791208791%, 825px); width: 100%; height: 0; } a.image2.image-link.image2-825-1456 img { max-width: 1456px; max-height: 825px; } Source: White Sight via Aika’s [very good] NewsletterThe machine-like product rollout was just as well because the decline in travel during the pandemic was devastating for Revolut’s legacy business. International payment volumes declined by two-thirds compared with pre-Covid levels, leading to a 12% decline in overall revenues between the first and second quarters. Fortunately, stock and later crypto trading picked up the slack. For the full year, card and interchange revenues were up 28% to £95 million, but fees from foreign exchange and wealth were up 150% to £80 million.

Revenue per customer reached around £36 on an annualised basis in the first quarter of this year, up from around £21 for the full year 2020. Similar to Robinhood, which we discussed last week, the numbers are small. In US Dollar terms, the first quarter revenue run rate is equivalent to $50 per customer. This compares with around $90 per customer at US challenger bank Chime (2020) and $137 at Robinhood (1Q21). At incumbent banks, the numbers are larger. NatWest generates around $420 of revenue per customer and in the US, Bank of America and Chase generate over $500 per customer.

The difference is of course that challengers can in principle scale at low cost. Revolut is still growing its customer base rapidly through referral, although it’s unclear what the return on a customer acquisition is when the referral incentive is £50 (even if the new customer does have to make three transactions to qualify). In 2020, the gross margin of the business improved from 29% in the first quarter to 61% in the fourth. Underneath gross profit, there’s £226 million of administrative expenses; right now that expense base is growing more quickly than revenues as the company invests in expansion, but at some point that will slow. Indeed, the company already employs more compliance personnel per head than major UK banks, so it may not need to invest as much there. Based on LinkedIn data, 16% of its headcount is employed in compliance compared with 8-9% at larger UK banks.

Global Financial SuperappLike other consumer fintech companies, Revolut has converged on the super app strategy. “One app for all things money,” is the lede on the company website. “We are building the world’s first truly global financial superapp.” Unlike others, though, it doesn’t have a core profitable business. Chime has unregulated debit interchange – it doesn’t suffer the cap that Revolut does in Europe. Robinhood has payment for order flow. Tinkoff in Russia has credit card lending.

Revolut has two things going for it: it wants to be global and, unlike some of the others, it wants to be a bank.

“Our vision is we want to build a global bank… sooner or later, someone will do it, and we want it to be us.” [Source]

Revolut is entering new markets at a rate of 5-10 a year. It typically spends up to two years on the ground before launch and invests between $10 million and $20 million in the process. Revolut reckons it can outgrow local competitors in the majority of countries it enters once it turns on its marketing campaigns.

It’s a tough challenge, though. There’s no real precedent for a global consumer bank. Citi and HSBC both tried, but retrenched from their global ambitions in waves. HSBC recently gave away its French business, but years earlier had given up on its slogan ‘the world’s local bank’. Citi is close to selling its retail banking operations in South Korea as part of its strategy to exit consumer banking in 13 markets across Asia and Europe.

At a recent investor event, the CEO of Tinkoff took a sideswipe at Revolut: “Our model that we’re thinking about at the moment is not a light model, where you skim off a few hundred thousand customers in 20 different markets. That’s not what we’re thinking about.”

Revolut also wants to be a bank. Right now it is regulated as an e-money issuer in the UK, although it has a banking license in Lithuania. It sits on £4.5 billion of customer funds (£310 per customer) which it needs to hold in cash at accounts at authorised financial institutions as a safeguarding mechanism. A banking license would bring three benefits. It would allow Revolut to invest customer funds more broadly, for example by offering loans. It would also provide customers with deposit insurance on their funds (although it’s not clear how much of an obstacle this is to gathering funds; Wise sits on customer funds averaging £2,300 per account without insurance). Finally, a banking license would give Revolut access to central bank facilities. As chairman Martin Gilbert said recently:

“The banking license would be pretty advantageous for us … at the moment, one of the big disadvantages we have is we might have £3bn or £4bn on overnight every night on negative interest rates, so you can see the drag on earnings that that has, because we have to safeguard clients money obviously because we’re not a bank.”

In the US, SoFi is seeking a banking license and has indicated that it could add $200 million to $300 million per year to its baseline EBITDA projections over the next few years. Its business model focuses much more on the lending side than Revolut’s but it reflects the appeal of a banking license.

The downside is of course the cost. Revolut currently has to operate with only £63 million of capital. A banking license would ramp that capital requirement, which is one of the reasons it has just raised $800 million in its series E.

There’s another downside, which is valuation. In the same interview, chairman Martin Gilbert said, “We don’t want to be perceived as a bank because banks are rated at a far lower rating than a fintech business, so we really do need to keep that advantage of being seen as fast moving and fee based rather than interest based business.”

That’s not something Revolut has to worry about for a while. It just raised capital at a valuation of 74x last twelve months’ revenue; that compares with NatWest at 2.3x. The question now is whether it can extract sufficient profitability from its customers to grow into that valuation.

Wise came to the market in the UK last week with an unbundled approach to financial services – isolate a product and provide it cheaper than the competition, with no cross-subsidisation. Revolut’s bundled model is different. Its newest shareholders, Softbank and Tiger Global, know that the revenues are out there; they are betting that by spraying products across markets, Revolut can capture some of them.

More Net InterestBuy Now Pay LaterThe Buy Now Pay Later market is hotting up with Apple entering the market in partnership with Goldman Sachs. (I have said before that the most formidable competitor in fintech could be Apple + Goldman Sachs.) Increasingly it looks like Buy Now Pay Later could be a feature rather than a business of its own.

John Street Capital @JohnStCapital$AAPL & $GS are launching a BNPL service known as "Apple Pay Later" enabling Apple Pay users to pay across 4 payments every two weeks or across several months. $V & $GPN annc a similar product in Canada today. This + $PYPL & eventually $SQ make BNPL a feature & not a companyJuly 13th 2021

36 Retweets224 LikesA good representation of this is in India, where MobiKwik recently filed to go public. The company started out as a mobile wallet in 2009. It now has 101.37 million registered users. In May 2019, it launched a Buy Now Pay Later product (MobiKwik Zip) that enables users to activate a Rs500 to Rs30,000 credit limit in their wallet which they can draw down, interest-free, in 15-day cycles. At the end of the cycle, the user is required to pay what’s due within five days, failing which late fees are applied (the user also pays a one-time activation fee).

As at the end of March, MobiKwik had pre-approved 22.25 million users for the product, out of which 741,000 had activated. MobiKwik retains some of the risk (5-15%) but passes most of it on to financial institutions. Its advantage is that merchants are already signed up, via its wallet, and it has good data on its consumers via their purchase history.

In the year to March 2021, the Buy Now Pay Later product contributed 21% to total revenue. A part of the investment case behind the IPO is that this will grow; it’s likely a feature other wallet providers will replicate.

Loan GrowthA major issue overhanging US banks since the beginning of the pandemic has been the absence of loan growth. JPMorgan’s consumer and business loans were down 3% year-on-year in the second quarter as customer cash balances remain elevated leading to higher prepayments in mortgage and lower card outstandings. But the company is optimistic loan growth will resume. On his earnings call, the CFO said, “we are quite optimistic that the current spend trends will convert into resumption of loan growth through the end of this year and into next.” Bank of America provided a useful chart that backs up the assertion. It shows daily loan balances, with the trough having passed in March. Lending companies will be hopeful of a strong rebound in loan growth in the second half.

a.image2.image-link.image2-308-500 { padding-bottom: 61.6%; padding-bottom: min(61.6%, 308px); width: 100%; height: 0; } a.image2.image-link.image2-308-500 img { max-width: 500px; max-height: 308px; } Source: Bank of AmericaAIG/BlackstoneBack in 1998, AIG took a 7% stake in Blackstone. Ten years later, AIG was in financial trouble and had to be bailed out by the US Government. Blackstone’s price was severely affected by the crisis, so the stake couldn’t be used to raise cash, but a few years later AIG was able to exit for a considerable gain.

This week, the two announced a reverse transaction. Blackstone will take a 10% stake in AIG’s life-insurance and retirement-services unit ahead of its IPO. Blackstone will also manage $50 billion of AIG assets, rising to $100 billion over six years. The move is the latest in the convergence of insurance and private equity as insurance companies seek to improve investment returns in their portfolios. It’s a theme we discussed in Other People’s Money – the latest application of a model Warren Buffett developed back in 1967.

Categorías: Blogs y foros de trabajar madera en ingles

A new starting position with a 2% yield

I just initiated a new position in Philips NV. It yields 2% and in this post I'm explaining you my thoughts about why I bought some shares in them.

The post A new starting position with a 2% yield appeared first on European Dividend Growth Investor.

Categorías: Blogs y opiniones de economia en ingles

Las industrias que crecen pese a la crisis económica en Latinoamérica

Si sumamos a esto al problema de salubridad ocasionado por la pandemia del coronavirus, entonces estamos frente a un escenario lamentable; que por desgracia se repite en otros países de la región.

Pero, no todo es negativo. También, se ha podido observar que es cierto eso de que en las crisis es donde afloran las mejores ideas. Hoy en día a pesar de todos estos acontecimientos, no sólo en Colombia, sino en toda Latinoamérica existen industrias que han mantenido su estabilidad e incluso han crecido paulatinamente en medio de la crisis.

El juego online y su crecimiento en ColombiaSeguramente, estarás dudando de que en un escenario como el antes descrito puedan existir empresas e industrias que han seguido su tendencia al crecimiento. Pero la verdad es esa, en Colombia tenemos hoy varios ejemplos que lo corroboran.

La industria del entretenimiento online es quizás el ejemplo más claro. Empresas dedicadas a las apuestas deportivas y juegos de casino como Colbet Colombia, son una muestra de que en estos tiempos de crisis existen alternativas para el sano esparcimiento, y al mismo tiempo para el desarrollo económico del país.

Hoy en día son cada vez más los colombianos que se suman a la comunidad de amantes de los juegos de casino. Gracias a los sitios de apuestas online de la comodidad del hogar estas pueden disfrutar de juegos populares como la Ruleta, Blackjack, Poker, Tragamonedas y otros.

Proyecciones de crecimiento para este 2021La aparición de la pandemia gracias al coronavirus tomó por sorpresa a muchos países de la región. Sin embargo, gracias a las políticas que algunos de estos venían aplicando en materia económica y social, se puede observar que a algunos les ha afectado más que a otros.

Para finales del año 2021 se manejan proyecciones que establecen a Brasil, Argentina y Perú como los países latinoamericanos con mayor caída en su actividad económica. Por otro lado, los que tendrán caídas menos profundas se estima que sean Uruguay, Paraguay y Guatemala.

El único país de la región que no entra en ninguna de las proyecciones es Venezuela, debido a la gran recesión que sufre esta nación durante varios años. De hecho, se establece que Venezuela caerá para este año un 26%.

Según las estimaciones realizadas por la CEPAL, en 2022 América Latina y el Caribe crecerá 2,9% en promedio, lo que implica una desaceleración respecto del rebote de 2021 y una caída en su producto interno bruto en -9.1% este año, el peor registro en los últimos 100 años.

Categorías: 1 Noticias economicas en español

Starlink and the REAL Space Race

The “BDE” of billionaires is next level.

Jeff Bezos made an announcement that he’s going to space via Blue Origin.

Whether he didn’t want to be outdone or wanted to steal all the spotlight (clever), Richard Branson announced he was doing the same via Virgin Galactic.

Only earlier.

But the billionaire race to space is just a sideshow to the real race to space.

Bezos and Amazon might control a significant portion of e-commerce and even tech infrastructure (through Amazon Web Servers). However…

- There is an even bigger play here: Control over the internet itself.

And it all begins right before the Dot Com boom…

The Battle for Global SignalsIn November 1998, a new company called Iridium launched a brand-new satellite communications service.

And just ten months later, the company filed for Chapter 11 bankruptcy.

They’d failed to take into account one pretty simple fact: it requires billions of dollars to launch satellites into space.

Twenty years later, Elon Musk is barging into the exact same space.

Only he’s doing it Musk-style, using his now-typical (and ultra-successful) gameplan.

First, he’s turned the really expensive thing into a commodity, just like he did with electric cars and rocket ships.

His company, Starlink, is on the verge of creating satellites on an assembly line.

Second, he’s his own customer.

SpaceX needs a continually full calendar of payloads to take to space, and Starlink always needs to get satellites up to build out its network. It’s a win-win.

Third, he’s leveraging the U.S. government (okay, your taxpayer dollars) to fund the entire thing.

Starlink has been picking up lucrative FCC contracts to provide satellite-based internet to areas all across the United States.

And fourth, the company is making a ton of money before it has even fully launched, and using that to fund future growth.

- Starlink already has $500 million worth of subscribers and reservations.

Even the founder of Iridium knows the eventual outcome:

“I wish Mr. Musk well,” he said. “I expect him to succeed.”

Iridium was just building a satellite phone service, but Starlink is taking that a few major leaps further.

Starlink wants to be the internet service provider for the world…And when it’s fully built out, it will upend the world order in much the same way the internet did in the late ‘90s and early ‘00s.

The Starlink concept is really simple. With a small, pizza-box-sized satellite dish, a user can access the internet from anywhere in the world.

Anywhere.

A barge in the Suez Canal… The top of Mt. Everest…

The Sahara Desert…

The service is currently being tested in a few countries. In true Musk fashion, they’re calling it the “Better Than Nothing Beta Test.”

Already, it’s pretty great. Testers are getting better than 100 Mbps speeds. And by the end of the year, that’s expected to reach 300 Mbps.

(For context, the average U.S. internet speed is <200 Mbps.)

And it’s just going to keep getting better…

- Starlink’s original stated goal was 1 Gbps internet—four times the fastest country in the world, Singapore.

And they’ve promised the FCC they will provide the internet with zero contracts, early cancellation fees, and no data caps.

All for the whopping price of $99. But that’s expected to come down.

As Musk tweeted:

- “Starlink is a staggeringly difficult technical & economic endeavor. However, if we don’t fail, the cost to end-users will improve every year.”

Once Starlink is fully operational, a majority of internet users won’t even consider anything else.

Which begs the question…

When and how will all of this unfold?As of early 2019, less than 5,000 satellites total had ever been launched.

Starlink projects that 12,000 satellites will be necessary to provide reliable global internet coverage at ultra-fast speeds.

Seems impossible, right?

The first small batch of Starlink satellites was sent into space via SpaceX in May 2019.

Right now, there are now nearly 1,500 Starlink satellites in orbit.

Courtesy of https://satellitemap.space/More importantly, the frequency of launches is accelerating—from six months between the first two is now down to just nine days between launches. Expect that to become hourly.

Yes, hourly.

Further, Musk is preparing a new Starship, which will be able to haul four times as many satellites per trip.

In other words…

- Starlink is going to get bigger than expected, much faster than expected, all paid for by U.S. customers through the FCC.

It gets better. The satellites will be de-orbited after three or four years.

So just like Teslas, SpaceX will be able to upgrade them on a rolling basis.

In an early 2021 presentation, Starlink revealed they plan to reach speeds of 10 Gbps—in part by using lasers to communicate between satellites.

This isn’t about faster Netflix and porn speeds.

- This is going to revolutionize where, when, and how business is done.

And it’s going to have massive ramifications for global politics and the world order.

OK, I’m going to channel President Reagan for this next title:

“Mr. Musk, Tear Down This Firewall”Once the satellites are in space—remember, more than twice as many have ever been launched—there will not be room for a second internet service provider.

China and Russia fear this in a big way.

The Space Race was in my book, The Rise of America, if you want to know more.

But if Musk is successful: The game will be over.

And the second-order effects of a single, global internet service provider will be unlike anything you’ve seen before.

For example, right now, Jeff Bezos (Amazon), Mark Zuckerberg (Facebook), Sundar Pichai (Google), and Tim Cook (Apple) wield incredible power.

As you’ve seen, a flip of the Twitter or Facebook PNG switch can instantly mute someone from the world stage.

- Elon Musk is positioning himself to be the person with power over the people who have power.

Once he controls the world’s internet, he can dictate what is and is not transmitted worldwide.

You can bet that major world powers and governments are watching this closely.

And you’re probably aware of the so-called “Great Firewall of China,” which the government uses to determine what users can access.

Russia, India, Iran, Syria, and Vietnam also have or are implementing similar programs.

With Starlink, users will be able to circumvent that filter. It’s a little difficult to block all of the space.

I’m even willing to speculate that Starlink will open-source the patents for the receiver dishes, just like Tesla did. Same guy in control.

But all of that is nothing compared to the real competition unfolding.

Because the world’s biggest country and the world’s biggest entrepreneur both have the same grand ambition:

- Get to Mars. First.

SpaceX knows the entire space launch industry is only worth about $5 billion in revenue a year.

Global internet access? That’s a $1 trillion+ market…

Or the size of China’s entire GDP in 1999.

With that kind of revenue, SpaceX—and Elon—have a shot at winning this thing.

Over the course of the next year, we’re going to watch a no-holds-barred fight, with Earth as the arena.

Like the founder of Iridium, my money’s on Elon.

And to all those who bash Elon, I ask—what have you done to make society better?

Until next time, stay safe.

Regards,

Marin

The post Starlink and the REAL Space Race appeared first on Katusa Research.

Categorías: Blogs y foros de trabajar madera en ingles

Intel negocia la compra de GlobalFoundries por unos 30.000 millones de dólares

La compañía tecnológica estaría en conversaciones para adquirir GlobalFoundries, uno de los mayores fabricantes de superconductores del mundo. Leer

Categorías: 1 Noticias economicas en español

Devastating floods in Germany warn Europe of the dangers of warming

Whether or not climate change caused these floods, it made them more likely

Categorías: 3 Noticias economicas ingles

Level "11" Market Risk

History will say that at peak Baby Boomer retirement there was not enough buying power to fund their market exodus so the geniuses of the day turned to money printing to get them over the cliff. The ONLY inflation these serial morons don't fear is stratospheric asset valuations...

This week, Fed Chief Powell gave gamblers the green light to party like it's 1929. The concepts of moral hazard and conflict of interest are now entirely foreign to this latent Idiocracy.

As against all of today's Ponzi schemers, the only ones who don't believe in Ponzi reflation happens to be the entire Treasury bond market. Copious morons bidding up their own assets versus the most liquid market on the planet. Who to believe? Given the asinine size of the deficit, it indeed seems axiomatic that inflation should be the dominant concern right now, however the fact that it isn't causing sustainable inflation should be of even greater concern.

It points to the fact that the fiscal multiplier has collapsed.

My hypothesis is that with each successive recession and attendant mass layoff over these past decades, the Federal government has become a far greater share of the overall economy. Which means that what would formerly be considered "stimulus" at any other time in U.S. history is merely backfilled GDP. In other words, absent this massive deficit, the U.S. would be in depression right now. To that point, the U.S. debt will grow at a 13% rate (vis-a-vis GDP) this year while GDP itself will grow 2% annualized vis-a-vis 2019 levels. A staggering gap that can only be rationalized in the context of 100% Japanification.

All of which means that "inflation" now depends far more on what is happening globally versus what is happening solely in the U.S. If the dollar soars, then deflation will be the end result as everything in Walmart will be much cheaper. And we all know these zombies love lower prices, EXCEPT when it comes to asset prices. When it comes to asset prices, they love hyper inflation. Why? Because they STILL can't remember how this movie always ends.

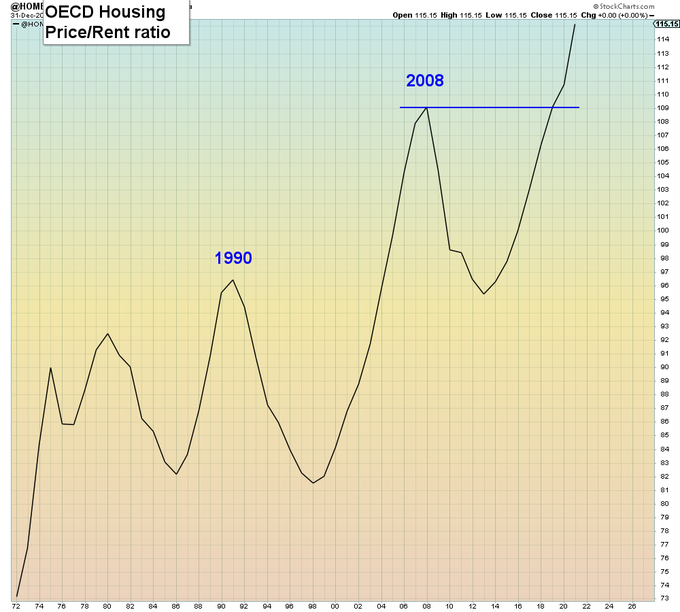

Picture a global housing bubble now BIGGER than 2008:

A Tech bubble that now exceeds Y2K:

“The problem with this setup is that tech sector profitability and earnings are vulnerable,” wrote Lisa Shalett, chief investment officer of Morgan Stanley Wealth Management. She sees “unprecedented headwinds” for the group"

A reflation bubble the likes of which has taken valuations to unprecedented levels by any measurement: Earnings, sales, market cap/GDP etc.

Dow Autos and Parts are just one example of the post-pandemic rally that was predicated upon ONE TIME earnings effects as compared to last year's lockdown depression. In other words, the same extrapolation that has abided the extreme "inflation" hysteria is now embedded in stock multiples.

"Sustained inflation"

And of course we must not forget the crypto Ponzi bubble and all of the other speculative pump and dump schemes that adorn this era. All coalescing during the tenuous re-opening phase of a global pandemic in which global mass unemployment has sky-rocketed. A minor detail in the overall "reflation" calculation, so we are told.

And now the fiscal stimulus is unwinding as well. Which is a far greater factor for true economic reflation than monetary policy and the beloved asset hyper bubble. Gamblers are SOLELY fixated on Fed policy and ignoring the fast receding fiscal impulse which is driving the underlying economy.

In summary, this was a one time post-pandemic re-opening party. And sadly, the Fed can't bail out everyone who believes any different.

They are collateral damage, and despite watching the same movie over and over again, they haven't learned anything in the past twenty years:

{kind=link}

This week, Fed Chief Powell gave gamblers the green light to party like it's 1929. The concepts of moral hazard and conflict of interest are now entirely foreign to this latent Idiocracy.

As against all of today's Ponzi schemers, the only ones who don't believe in Ponzi reflation happens to be the entire Treasury bond market. Copious morons bidding up their own assets versus the most liquid market on the planet. Who to believe? Given the asinine size of the deficit, it indeed seems axiomatic that inflation should be the dominant concern right now, however the fact that it isn't causing sustainable inflation should be of even greater concern.

It points to the fact that the fiscal multiplier has collapsed.

My hypothesis is that with each successive recession and attendant mass layoff over these past decades, the Federal government has become a far greater share of the overall economy. Which means that what would formerly be considered "stimulus" at any other time in U.S. history is merely backfilled GDP. In other words, absent this massive deficit, the U.S. would be in depression right now. To that point, the U.S. debt will grow at a 13% rate (vis-a-vis GDP) this year while GDP itself will grow 2% annualized vis-a-vis 2019 levels. A staggering gap that can only be rationalized in the context of 100% Japanification.

{kind=link}

All of which means that "inflation" now depends far more on what is happening globally versus what is happening solely in the U.S. If the dollar soars, then deflation will be the end result as everything in Walmart will be much cheaper. And we all know these zombies love lower prices, EXCEPT when it comes to asset prices. When it comes to asset prices, they love hyper inflation. Why? Because they STILL can't remember how this movie always ends.

Picture a global housing bubble now BIGGER than 2008:

{kind=link}

A Tech bubble that now exceeds Y2K:

“The problem with this setup is that tech sector profitability and earnings are vulnerable,” wrote Lisa Shalett, chief investment officer of Morgan Stanley Wealth Management. She sees “unprecedented headwinds” for the group"

{kind=link}

A reflation bubble the likes of which has taken valuations to unprecedented levels by any measurement: Earnings, sales, market cap/GDP etc.

Dow Autos and Parts are just one example of the post-pandemic rally that was predicated upon ONE TIME earnings effects as compared to last year's lockdown depression. In other words, the same extrapolation that has abided the extreme "inflation" hysteria is now embedded in stock multiples.

"Sustained inflation"

{kind=link}

And of course we must not forget the crypto Ponzi bubble and all of the other speculative pump and dump schemes that adorn this era. All coalescing during the tenuous re-opening phase of a global pandemic in which global mass unemployment has sky-rocketed. A minor detail in the overall "reflation" calculation, so we are told.

And now the fiscal stimulus is unwinding as well. Which is a far greater factor for true economic reflation than monetary policy and the beloved asset hyper bubble. Gamblers are SOLELY fixated on Fed policy and ignoring the fast receding fiscal impulse which is driving the underlying economy.

In summary, this was a one time post-pandemic re-opening party. And sadly, the Fed can't bail out everyone who believes any different.

They are collateral damage, and despite watching the same movie over and over again, they haven't learned anything in the past twenty years:

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Páginas

Custom Search