Se encuentra usted aquí

Agregador de canales de noticias

Archegos? Argh, Chaos More Like

Archegos? Argh, Chaos More Like

By Michael Every of Rabobank

I noted yesterday that the expected market turbulence caused by the Archegos sell-off was not representative of the underlying structural issues that will guide markets going forwards. I stick by that claim, but even so what a messy day it was. Some individual stocks got hit hard, and US bond yields were up, presumably due to the need to sell anything to get liquidity, while the USD see-sawed. Archegos? ‘Argh, chaos’ more like.

This overshadowed the good news that the Suez Canal is now open again. However, there is a link between the two: both stories reveal how stupid the key infrastructure of the global economy and financial system still is. ‘Too big to sail and too big to fail’, as some dub the two halves of this dyad: and Joe Public can again see our system encourages entities to get so large and complex that when a simple incident happens, everything gets stuck. Something surely needs to change, unless we are going to assume there can’t be any more ‘Argh, chaos’ “because markets”, or any more stuck giant ships in the Suez Canal “because boats”.

So, change? Fed Governor Waller spoke to the Peterson Institute for International Economics yesterday, where he rejected any suggestions the Fed was close to embracing the MMT: he wanted to “definitively put that narrative to rest. It is simply wrong”. Borrowing costs are not being kept low to help finance the government, apparently. (It’s all inflation; and unemployment; and social justice; and the climate?) Clearly there won’t be any need for an Operation Twist and Shout or for Yield Curve Control then…but can we get that in writing?

At the same time, the press reports the Biden administration is planning a further Covid relief bill separate from a key infrastructure bill to be launched Wednesday; and the latter is now rumored to be for as much as USD4 trillion, or close to 20% of GDP, funded by USD3 trillion of tax hikes on businesses and the rich, the largest hike in a generation, as opposed to the original idea of USD3 trillion in spending funded by USD1 trillion of taxes.

If the larger stimulus package is the one put forward, it means there is no sign of MMT in the White House either, because the net spend of USD1 trillion (over a decade) is hardly in the money-printing category. Instead, there is a redistributive fiscal package that presumes USD3 trillion the rich have can be spent more productively on bridges, roads, and ports, etc., than on $100m condos filled with gold-dusted caviar or stock buybacks. Cue a shift of political debate from ‘MMT’ vs. ‘no MMT’ to ‘The government doesn’t know what it’s doing!’ vs. ‘The rich do know what they are doing – turning the US into an oligarchic kleptocracy’. And may the best lobbyists win.

As a linked aside, yesterday I saw 1963 US plans for an alternative to the Suez Canal, because at the time Egypt was a Soviet client state. This was to use *530* nukes to blow a 160-mile long, 1,500 foot deep channel through Israel from its Mediterranean coast to the Red Sea, which would “probably contribute greatly to the economic development of the surrounding area”(!) That underlines the idiocy of central planning and of Cold War thinking. Which is doubly worrying given any new Cold War is again very likely going to see key global infrastructure in the hands of states not aligned with US geostrategic interests, and the US is already talking about its own Belt and Road rival (as China seems to slowly back away from the economic drain of its own). Beware Americans bearing nukes.

Yet the economic national-security Hamiltonian model, the ideas of Henry George, and the fact Eisenhower built the US inter-state highway network partially to prevent Soviet invasion from either coast, still all hold as much water as the glow-in-the-dark 160-mile long monstrosity through Israel would have.

Meanwhile, as the US and nukes and the Middle East make headlines for different reasons today, but still leaving much of Israel feeling antsy, BOJ Governor Kuroda just stated he will continue to buy ETFs within a JPY12 trillion cap “with a close eye on markets” even after Covid is over; he won’t sell the BOJ’s stock of ETFs; and the inflation target stays at 2% (ROFL!). He also thinks that it is “natural for the government to deploy fiscal stimulus flexibly, though Japan must also maintain market trust over its medium- and long-term fiscal health.” (Will the people in the market who associate Japan with long-term fiscal health please stand up?) The BOJ will also “support various entities’ efforts towards reform as Japan faces challenges in the post-Covid world”: does he mean the local Olympic Games Committee? In short, more of the same is on offer from the BOJ – which has worked so magnificently for it so far.

That’s another lesson for the US. Structural reform needs to be structural, not just cementing over river beds – or blowing up the Negev desert.

On which note, the FTSE Bond Index just announced that it is about to include Chinese government bonds (CGBs) in its world index, allowing global investors to buy both sides of the Cold War bet and all related public expenditures. But there is a sting in the tail: the FTSE CGB weighting will be just 5.25%, not the 6.5% expected, starting October 29, and this will be tapered in over 36 months, not 12 months as originally believed.

A few months ago, when China was seeing too much capital flow in for its liking, that slower pace might have been welcome. Indeed, and ironically, much of the capital that went in to Chinese markets from foreign funds is believed to have been encouraged to flow straight back out again via different channels to prevent excess appreciation pressure on the currency (and note that China’s FX reserves have hardly soared). Yet CNY and CNH are starting to move markedly lower again; and genuine capital outflows are being experienced as US yields rise, even despite bumper Covid-related trade surpluses (which will fade with the virus does). Moreover, with the geopolitical backdrop this Cold, how could this most political of all FX crosses not eventually respond in kind?

One wonders what the Fed (and ECB and BOJ) would make of any sustained move lower in CNY, given what it will mean for inflation; and the White House, given what it means for jobs.

Tyler Durden Tue, 03/30/2021 - 10:15

Categorías: Blogs y opiniones de economia en ingles

US Consumer Confidence Explodes Higher In March

US Consumer Confidence Explodes Higher In March

After a mixed picture in February (expectations down, current conditions up), analysts expected a big jump in Conference Board Consumer Confidence in March... and they got it.

March Consumer Confidence exploded from 90.4 (revised lower) in Feb to 109.7 in March - the highest since March 2020.

The underlying components also smashed expectations:

-

Present situation confidence rose to 110.0 vs. 89.6 last month.

-

Consumer confidence expectations rose to 109.6 vs. 90.9 last month - highest since July 2019

{kind=link}

Source: Bloomberg

Still, putting these levels in context, they are still dramatically below the pre-COVID levels of confidence...

{kind=link}

Source: Bloomberg

Maybe with just a few more trillion dollars of helicopter cash, that Main Street confidence will catch up?

Tyler Durden Tue, 03/30/2021 - 10:04

Categorías: Blogs y opiniones de economia en ingles

Regulators Grill Banks About Archegos Blowup As Market Ponders Broader Risks

Regulators Grill Banks About Archegos Blowup As Market Ponders Broader Risks

Traders across Wall Street and on the buy side are anxiously waiting to see if any more big block trades in names like VIAC, GXU, TME and the other constituents of Archegos founder Bill Hwang's busted portfolio will wander across the tape. As journalists, regulators and academics question how Hwang was ever allowed to take on so much leverage (a question that has yet to be thoroughly answered), Bloomberg reports that regulators have already started asking prime brokers tough questions about how this was allowed to happen.

Bloomberg reported that the prime brokers spent Monday briefing US regulators as Washington starts to dig in into a historic fund blowup that could have broader implications for market stability. According to the report, the SEC hastily summoned banks for meetings on what triggered the forced sale, while Finra, the industry self-regulator, asked brokerages about the impact to their operations and credit risks, people familiar said.

"We have been monitoring the situation and communicating with market participants since last week," an SEC spokesperson said in emailed statement. A Finra spokesman declined to comment.

But that's not all the Achegos news we're seeing Tuesday morning. Mitsubishi Financial Group has just become the latest major bank to warn about losses tied to the Archegos blowup, reporting that $300MM might be at risk. Of course, that's a paltry sum compared to the potential $2 billion claim reported by Nomura, Bloomberg.

MUFG’s securities arm said in a statement on Tuesday that it is evaluating the extent of the loss at its European subsidiary, which may change depending on market prices and the unwinding of transactions.

Mitsubishi UFJ Securities Holdings Co. said any loss won’t have a material impact on the firm’s business capability or financial soundness. A representative for the firm declined to comment beyond what it said in the statement.

Mitsubishi wasn't among the prime brokers who met last week to try and manage the unwind of Archegos's positions in a way that wouldn't saddle them all with huge losses - though Goldman and MS's decisions to break ranks with a series of block trades helped trigger the fire sale. And it's possible that more banks could come forward with losses.

{kind=link}

Bill Hwang

As more details about the blow-up have emerged over the past 24 hours, academics like Boston University finance lecturer Mark Williams have been quoted in the press criticizing apparent shortcomings in banks' risk-management. "In this environment, where information flows quickly and you have to move quickly, this demonstrates a significant weakness on the part of Nomura’s risk management," Williams said. "Did they not understand the risks they entered into, or did they ignore them because they wanted to grow?"

Put another way: Did Archegos mislead its prime brokers about its total leverage and exposure? Or did the intense competition among PB desks incentivize them to simply ignore these risks (perhaps figuring that, if Hwang's positions went tits up, competitors would be incentivize to cooperate and work out out a solution)?

What's more, Larry Peruzzi, director of international trading at Mischler Financial says the Archegos Capital block-trade incident could lead to calls for new regulations such as limiting the size of blocks or prohibiting off-board discounted prints on the open and close, or during the first or last 30 minutes of trading. It “will be tough, though, as exchanges and investors like liquidity,” Peruzzi said in a statement reportedly emailed to Bloomberg. “These types of swings seem to be another factor in pushing more trading into passive strategies”.

At any rate, Fed Chairman Jerome Powell has repeatedly touted the resilience of post-GFC banking regs. "We actually monitor financial conditions very, very broadly and carefully. And we didn’t do that before the global financial crisis 12 years ago. Now we do," Powell said during the post-FOMC Q&A on March 17. Unfortunately for him, the biggest hedge fund blowup since LCTM has revived talk about the risks of "leverage gone wrong," as Bloomberg pointed out in a piece published last night,

Sameer Samana, Wells Fargo Investment Institute’s senior global market strategist, added that "[w]hat it does make me think of is how much leverage in aggregate has now built up in the system” in brokerage accounts, options and credit, Samana said. “If a broader stock market pullback were to take shape, especially in the more widely owned areas of technology and technology-related stocks, a much bigger unwind would have to take place."

But as Bloomberg's Brian Chappatta pointed out (and as we have mentioned several times), Archegos' use of CFDs, an opaque derivative reserved for institutional clients, allowed his firm to crank up its exposure to ViacomCBS and the other companies without needing to file ownership disclosures. The shares themselves remained securely with the banks. This arrangement, Chappatta continued, could represent "a blind spot" for regulators, and raising the prospect that the market could see more hedge fund or "family office" blowups in the near future, should equities face further broad-based selling pressure.

"The world has already been battling a once-in-a-century pandemic," Chappatta wrote. "The last thing it needs is big banks heaping on risk in search of profits, leaving someone else to hold the bag." That's well put.

While AOC and her fellow progressive Democrats haven't publicly called for a hearing, at least not yet, we imagine the big banks will swiftly turn on their client, placing the blame for what happened squarely with Achegos. Though JPM managed to escape the drama, one twitter wit captured this point with a meme.

When that Archegos Capital hearing starts on Capitol Hill... pic.twitter.com/r8gkn8B0rG

— Thornton McEnery (@ThorntonMcEnery) March 29, 2021 Tyler Durden Tue, 03/30/2021 - 09:50

Categorías: Blogs y opiniones de economia en ingles

Canada's Supreme Court Upholds Trudeau Climate Tax That Biden Wants To Mimic

Canada's Supreme Court Upholds Trudeau Climate Tax That Biden Wants To Mimic

Canadian Prime Minister Justin Trudeau, who has long been criticized by progressives (who hold the political scion in contempt as a poser and "faux-feminist") for his quiet support for Canadian Big Oil, can clearly see where the political winds in increasingly liberal Canada are blowing. And as the youthful prime minister (who is rumored to have inherited his famous good looks from Cuban revolutionary Fidel Castro) tries to foster a reputation as one of the western world's foremost climate warriors, Canadian courts have handed him a major victory.

As the world waits for a ruling on a major climate change case from the US Supreme Court, and President Biden prepares to unveil his sweeping infrastructure/climate program, the Supreme Court of Canada ruled on Thursday that Prime Minister Justin Trudeau’s national carbon price, the cornerstone of his climate policy, is entirely constitutional.

{kind=link}

The API, an influential organization representing energy firms, announced Tuesday that it supports a carbon-pricing scheme, the first time the US energy industry has nominally supported a carbon tax. However, the organization specified that the tax should be used to encourage green energy use, not pad government coffers.

Trudeau declared that a carbon tax would be a key policy goal back in 2016, but it wasn't until 2019, after he was reelected, that the Canadian federal government set a minimum price on carbon emissions in provinces which don’t have an equivalent provincial price. The controversial program applies a price to fuel purchases by individuals and businesses with lower emissions, and on part of the actual emissions produced by companies that are responsible for large emissions, such as pipelines, manufacturing plants and coal-fired power plants.

The law was quickly challenged by the oil-rich province of Alberta as well as conservative governments in Saskatchewan and Ontario. In his ruling, the federal judge who decided the case said companies should pay a price for pollution, the AP reports.

Chief Justice Richard Wagner said in the written ruling that climate change is a real and existential threat to Canada and the entire world, and evidence shows a price on pollution is a critical element to addressing it.

"The undisputed existence of a threat to the future of humanity cannot be ignored," he wrote.

Wagner also said the Canadian provinces can’t set minimum national prices on their own and if even one province fails to reduce their emissions it could have an inordinate impact on the rest of the country. It is a split decision with six judges entirely in favor, one partial dissent and two entirely in disagreement with the majority.

Almost immediately after the ruling was handed down, Federal Environment Minister Jonathan Wilkinson issued a statement lauding the decision as "a win for the millions of Canadians who believe we must build a prosperous economy that fights climate change."

Bloomberg pointed out that the ruling is key to Canada’s goal of reaching net-zero emissions by 2050. It’s also a victory for Trudeau, who came to power in 2015 pledging to tackle climate change, but has faced strong opposition from the fossil-fuel sector and oil-rich western provinces like Alberta. Canada produces more greenhouse gas per capita than almost all the world’s top emitters.

Now, considering the timing of this decision, will we hear Joe Biden point to Canada as an example for the US to follow during his briefing Thursday afternoon?

Tyler Durden Thu, 03/25/2021 - 12:57

Categorías: Blogs y opiniones de economia en ingles

India Halts COVID Vaccine Exports As Novovax Delays Deal With EU

India Halts COVID Vaccine Exports As Novovax Delays Deal With EU

Update (1200ET): Despite AstraZeneca releasing its revised trial data earlier, Denmark has decided to extend its pause on the AstraZeneca jab.

On March 11, Denmark joined Norway, Austria, Italy and Iceland to suspend the use of the vaccine after reports of blood blots.

Originally the rollout of the coronavirus jab was paused for 14 days as a precautionary measure but Danish officials said on March 25 that this has been extended by three weeks as they conducted their own investigations.

Most European countries resumed the shots after the EU's medicines watchdog deemed it safe and effective.

In more bad news for the EU, Reuters reports that Novovax is delaying a deal to supply jabs to the Continent once its vaccine regulator decides to approve the jabs.

Following the release of the updates trial data earlier today, the FT reported that AstraZeneca is working on creating a vaccine nasal spray. According to the FT, Oxford, AstraZeneca's partner in developing the vaccine, has started advertising for participants for a trial of the nasal spray vaccine. The phase 1 trial will involve about 30 healthy adults aged up to 40 and will study the safety of the formulation, according to a recruitment sheet seen by the paper. It could begin as early as next week. Participants will receive at least one intranasal dose of the vaccine; and half will randomly receive a booster dose. The study will take about four months to finish.

Finally, in other vaccination news, Pfizer's revealed just minutes ago that it would soon start trialing the COVID vaccine on children younger than 12. This comes after a trial on children aged 12 to 15 went well. The trial’s first participants, a pair of 9-year-old twin girls, were immunized at Duke University in North Carolina on Wednesday. Results from the trial are expected in the second half of the year, and the company hopes to vaccinate younger children early next year, according to the New York Times.

But by far the biggest news comes out of India, which on Thursday imposed a de facto ban on vaccine exports. That's a huge problem for dozens of developing nations, as well as the WHO's Covax program. The Serum Institute of India, the largest manufacturer of vaccines in the world and Covax's biggest supplier, has reportedly been told to halt exports and that the measures could last as long as two to three months, according to two people familiar with the situation. Gavi, the UN-backed international vaccine alliance, immediately warned that the controls would have a direct impact on the Covax scheme

The European Commission is holding talks Thursday about whether to impose similar restrictions, although Brussels seemed yesterday to be on the cusp of a deal with the UK to ensure "reciprocity" in vaccine supplies, per the FT.

The Serum Institute is contracted to manufacture 550MM AstraZeneca jabs and 550MM Novavax jabs solely for Covax in 2021 and 2022. That accounts for 80% of the facility’s currently signed contracts according to data from earlier this month.

* * *

Update (1000ET): More holdouts have decided to allow AstraZeneca jabs to be used on patients once again Thursday morning, with Sweden ending its safety probe. Vaccinations will move forward, including for people aged 65+.

- SWEDEN TO RESUME ASTRAZENECA COVID-19 VACCINATIONS - HEALTH AGENCY

- RECOMMEND ASTRAZENECA COVID-19 VACCINE FOR PEOPLE AGED 65 AND ABOVE

- RECOMMENDS EXTENDING PAUSE ON VACCINATIONS FOR YOUNGER PEOPLE

* * *

Earlier this week, AstraZeneca managed to destroy the last remaining shreds of its credibility by prematurely releasing an analysis of its COVID vaccine Phase 3 trial data, drawing an uncomfortably public rebuke from an American oversight board tasked with regulating the trials. In response, the company acknowledged that the data it had just released was based on an interim analysis, and promised to re-release its final results later in the week.

The company made good on its promise early Thursday morning, when it re-published the trial data with one notable tweak: the jab, which was initially touted as 79% effective, is now 76% effective. Although the company's claim that the jab is "100% effective" against serious disease was unaltered (scientists counted eight severe cases during the trial, all among trial participants who received the placebo). The data included 190 confirmed cases of COVID among the trial participants - 49 new cases that weren't included in the data released Monday. On top of this, the company said there are 14 "possible or probable cases to be adjudicated so the total number of cases and the point estimate may fluctuate slightly."

{kind=link}

The 76% number results from including newer infections among the 30K+ trial participants (trials were conducted in the US, as well as Chile and Peru). AZ also said the vaccine was 85% effective in preventing sickness among adults aged 65+, which is 5 percentage points higher than the 80% number it reported Monday.

While the revision is the latest reminder that the efficacy numbers touted by vaccine-makers are effectively meaningless, Reuters reported that the restatement of the AZ trial results will "go a long way to putting the vaccine back on track for gaining U.S. emergency use authorization."

"The vaccine efficacy against severe disease, including death, puts the AZ vaccine in the same ballpark as the other vaccines," said William Schaffner, an infectious disease expert from the Vanderbilt University School of Medicine, adding that he expects the shot to gain US approval.

AstraZeneca said the latest data has been presented to the independent trial oversight committee, the Data Safety Monitoring Board, and it plans to submit the analysis for peer-reviewed publication in the coming weeks.

"The primary analysis is consistent with our previously released interim analysis, and confirms that our COVID-19 vaccine is highly effective in adults," Mene Pangalos, executive vice president of BioPharmaceuticals R&D at AstraZeneca, said in a quote included with the press release.

One top AZ executive said during an appearance on CNBC earlier this week that the company intends to apply for approval in the US during the first half of April. Europe, meanwhile, the nation of Denmark extended its suspension of the AstraZeneca jabs as local public health officials take a closer look at rare blood clots that appeared in a small handful of patients. The clots led to notable illnesses and a death among a trio of Norwegian health-care workers, and cases have also been reported in Austria, Italy, the Netherlands and elsewhere. Canada's health department on Wednesday became the latest western government to reiterate that it believes the vaccine is "safe" - though it also updated its label to warn about the risk of potentially deadly blood clots in patients with low blood-platelet counts.

Tyler Durden Thu, 03/25/2021 - 12:44

Categorías: Blogs y opiniones de economia en ingles

Previewing Today's Closely Watched 7Y Auction

Previewing Today's Closely Watched 7Y Auction

Today the Treasury will auction $62BN in 7-year notes at 1pm. It will be a closely watched auction because one month ago the same 7Y February auction was "catastrophic" and sparked a rout in bonds which then quickly morphed into a marketwide dump hitting tech, momentum and growth stocks the hardest.

As a reminder, last month's 7Y tailed 4.4bps, the largest tail on record with dismal end-user demand declining to 60.2%, 20.2%-pts below the previous auction and the lowest level since September 2014, while the bid-to-cover ratio declined to 2.04, the lowest since the Treasury reintroduced the 7-year in early 2009

{kind=link}

At the investor class level, the investment manager share declined 14.3%-pts to 49.1%, the lowest level since May 2020, and the foreign share of demand declined to 8.1%, the lowest level on record.

To be sure, it wasn't just fear of inflation that was the culprit last month: technicals played a prominent role in last month's weak results, as intermediate yields rose as much as 25bp on the day of the auction, and Treasury market depth declined significantly to levels not seen since the early spring of 2020

In fact, the deterioration in depth was particularly severe around the auction as volumes surged and the most rapid sequence of the sell-off took place.

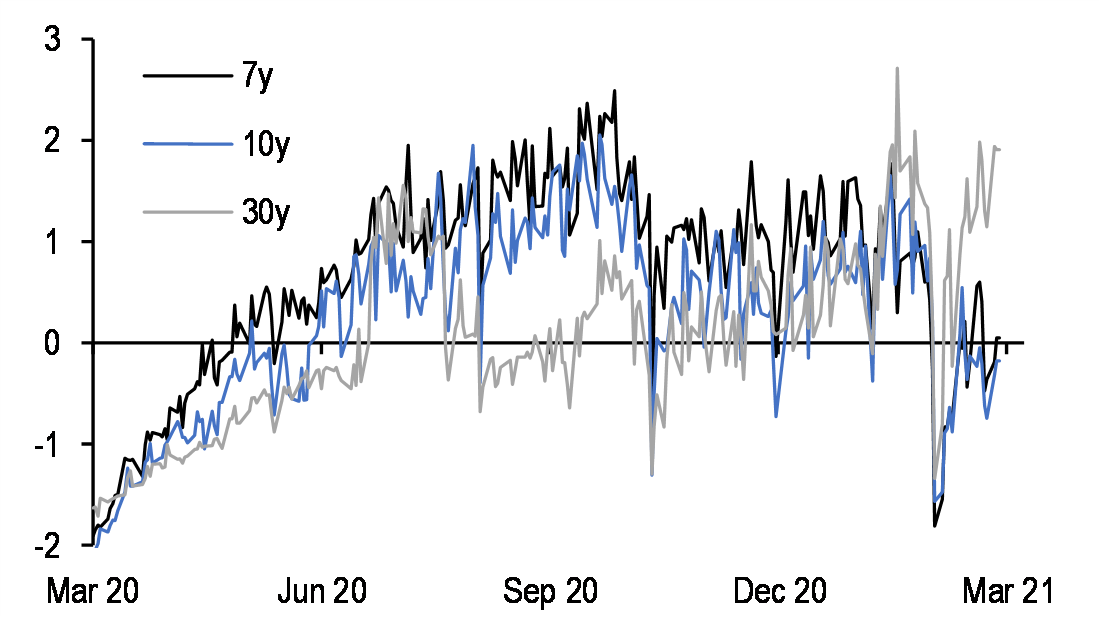

Market depth declined significantly around the last 7-year auction, but has since mostly recovered{kind=link}

Some more thoughts from JPM:

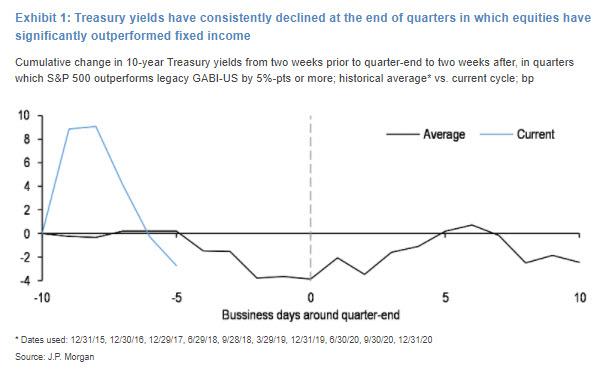

Looking ahead, though intermediate and long-end yields have declined 5-15bp from their recent highs last week, once we get through the 7-year auction, we think portfolio rebalancing could also drive yields lower. Equities have once again significantly outperformed fixed income: the S&P 500 has risen 3.5% QTD while the GABI-US (our aggregate fixed income index) has declined 3.4%. This sort of performance differential has typically led to rebalancing around quarter-end, and our colleagues estimate this could total $200bn rebalancing out of equities. Empirically, we have observed these sort of rebalancing flows have been supportive of lower Treasury yields: Exhibit 1 shows the cumulative change in 10-year yields around quarter-ends in which equities have outperformed the GABI-US by more than 5%-pts. Ten-year yields tend to decline by an average of 4bp in the weeks leading up to quarter-end and then reverse higher as the calendar turns to the new quarter, and this has occurred in 7 of 10 instances. Thus, cyclicals indicate risks are skewed toward a decline in yields in the coming days.

{kind=link}

Market depth has recovered in the intermediate sectors, retracing back in line with average levels over the past year, but remains lower than prior to the 7-year auction, and depth remains relatively depressed in intermediates compared to the long end. Additionally, even though seven-year yields are 7bp higher since the last auction, yields have declined 10bp this week alone. The 7-year sector appears modestly cheap versus the wings after adjusting for the level of rates and the shape of the curve. The WI 7-year roll opened at +1.75bp, in line with our fair value estimate, and is still trading, underperforming the erosion of carry. Lastly, though end-user demand at intermediate auctions have generally remained above historical averages—last month’s auction notwithstanding, dealers have had to absorb significantly more duration supply, which has likely driven more variable auction results recently. That said, the quarter-end rebalancing flows mentioned above could be supportive on the margin.

Overall, despite relatively cheap valuations, given the recent decline in yields, and technicals that have not yet fully recovered, JPM thinks today's auction will require above-average end-user demand to be digested smoothly, which following the two most recent auctions this week where we saw a solid 2Y and 5Y auction, this shouldn't prove to be too difficult.

Tyler Durden Thu, 03/25/2021 - 12:40

Categorías: Blogs y opiniones de economia en ingles

#62 Invirtiendo en TECNOLOGÍA con Andromeda Value Capital

Categorías: Blogs y opiniones de economia en español

¿Se puede vivir de los dividendos?

(adsbygoogle = window.adsbygoogle || []).push({});

Si te has preguntado alguna vez si es posible vivir de la bolsa gracias al reparto de dividendos, la respuesta es que sí, aunque necesitarás mucho dinero dependiendo del nivel de gasto que quieras llevar.

Explico cómo funcionan los dividendos y cómo poder llegar a vivir de las rentas en este artículo.

¿Qué son los dividendos?Los dividendos son una parte de los beneficios presentes o pasados de una empresa, que ésta distribuye a sus accionistas.

Para la empresa significa una salida de dinero real en sus cuentas, pues dejará de contar con esos recursos y no podrá destinarlos a realizar nuevas inversiones o eliminar deuda.

Los accionistas cobran los dividendos como un ingreso en su cuenta bancaria. A este ingreso en la mayoría de los casos se le practica una retención por parte de Hacienda del 19%, por lo que si una empresa nos paga 100 € de dividendos, nosotros veremos en cuenta un ingreso neto de 81 €.

Además, los dividendos tributan en el IRPF como capital mobiliario.

En el caso de acciones de empresas extranjeras dependiendo del país puede existir la posibilidad de que existan convenios de doble retención, para ahorrarnos parte de tributar en el país de origen de la empresa y en el nuestro.

Por poner un ejemplo en el cobro de dividendos. Imaginemos una empresa «A» que gana 2.000.000 €. Después de reinvertir en su propio negocio adquiriendo nueva maquinaria y contratando más personal, decide repartir un dividendo de 1.000.000 €, lo que equivale al 50% del beneficio anterior.

En el mundo financiero a este ratio se le conoce como «Pay-out», que no es más que el porcentaje sobre beneficio que la empresa destina a dividendos.

Sabemos que la empresa «A» tiene 50.000.000 de acciones en circulación, por lo que cada título tiene un dividendo de 0,02 € por acción. Si nosotros somos accionistas con 10.000 títulos, nos corresponden 200 € de dividendos, que una vez practicada la retención del 19%, se transforma en un ingreso en nuestra cuenta corriente de 162 €.

(adsbygoogle = window.adsbygoogle || []).push({}); ¿Cómo se calcula la rentabilidad por dividendo?La rentabilidad por dividendo es un ratio que nos indica cuánto dinero recibiremos por una determinada inversión en concepto de dividendos.

Por ejemplo, si una empresa paga 1 € de dividendo por acción y el precio de su cotización es de 100 €, tendremos un 1% de dividendo por acción.

Por lo tanto, este ratio se calcula de la siguiente manera:

- Rentabilidad por dividendo = Dividendo por acción / Cotización.

El único requisito para recibir dividendos en bolsa es ser accionista antes de la fecha «ex-dividend», que no es más que la fecha que determina quién tiene derecho a cobrar y quién no.

Todos los accionistas de una compañía tienen diferentes derechos, como por ejemplo el de acudir a la junta de accionistas y votar, derecho de información o derecho de participar en los beneficios de esa empresa, entre otros.

Si la empresa de la que somos accionistas decide repartir dividendos y nos corresponde por tener los títulos antes de la fecha «ex-dividend», la compañía está obligada a incluirnos en el reparto del beneficio.

¿Dónde ver y cuándo pagan dividendos las empresas?Esto depende de la política de cada compañía, pues las hay que reparten cada tres meses, cada seis meses, de forma anual o incluso cada mes. Otras compañías aún teniendo grandes beneficios prefieren no repartir dividendos y seguir invirtiendo en sus propios negocios.

Normalmente las empresas se comprometen con el reparto de los dividendos, de forma que suelen tener cierta periodicidad en sus pagos, aunque no estén obligadas a hacerlo.

Puede ver los dividendos de las empresas y cuándo pagan en páginas de información financiera como Investing.

(adsbygoogle = window.adsbygoogle || []).push({}); ¿Pueden las empresas cancelar los dividendos?Sí, de hecho empresas como Telefónica han cancelado alguna vez el reparto de beneficios entre sus accionistas por su mala situación financiera.

Si observamos que una empresa tiene mucha rentabilidad por dividendo debemos tener especial cuidado, y analizar si este dividendo es sostenible o corre el riesgo de ser reducido o incluso cancelado.

¿Es posible vivir de los dividendos?Los dividendos son un ingreso totalmente pasivo, pues simplemente nos irán ingresando dinero en nuestra cuenta corriente de forma periódica por nuestras inversiones.

Para vivir de los dividendos hace falta invertir dinero, y dependiendo de nuestro nivel de vida será necesaria una cantidad u otra que veremo en el siguiente punto.

¿Cuánto dinero necesito para vivir de los dividendos?Veamos cómo podemos calcular cuánto dinero necesitamos para vivir de las rentas con los dividendos.

Por ejemplo si nuestro objetivo es tener un sueldo de 20.000 € al año con una cartera de inversión de dividendos que nos genere una rentabilidad neta del 4%, necesitaremos tener invertido 500.000 €. (20.000 € dividido entre 0,04).

Si somos capaces de encontrar acciones con una rentabilidad del 5% que creamos que no van a cancelar el dividendo, esos mismos 20.000 € podríamos conseguirlos con una inversión de 400.000 €.

Si lo piensas esto no difiere a comprar un piso para alquilarlo o cualquier otro tipo de inversión, donde recibiremos un porcentaje por el servicio con una determinada rentabilidad.

La ventaja de las acciones es que son líquidas (podemos comprar y vender durante el día) y no requieren una actividad, por lo que tendremos rentas que se le pueden considerar pasivas.

En el caso de un piso probablemente no podremos comprarlo y venderlo durante un día y necesitaremos buscar inquilinos. (Vea mi artículo sobre la inversión en inmuebles aquí).

También puede profundizar más sobre este tema en mi artículo sobre cuánto dinero se necesita para vivir de las rentas y alcanzar la libertad financiera.

Cuando las empresas pagan dividendo, este valor se descuenta de su cotización el día de pago.

Imaginemos que la empresa «A» cotiza en bolsa a 10 € a cierre del 1 de febrero y paga un dividendo el 2 de febrero de 1 € por acción. Pues bien, este valor empezaría a cotizar a 9 € el día dos porque el pago del dividendo se descuenta de la cotización.

Es decir, el simple hecho de pagar dividendos no está creando valor, simplemente lo está distribuyendo.

¿Cuáles son las mejores acciones para invertir?Existen multitud de acciones, y es tarea de cada inversor identificar aquellas que más se ajustan a su filosofía. Por ejemplo, algunas inversiones que se pueden encontrar en bolsa son:

- Acciones que no reparten dividendos y reinvierten en sus propios negocios: Personalmente, mirando caso por caso, son las que más me gustan, pues aunque no generan una renta, si son empresas de calidad sí que suelen beneficiar al accionista, no mediante ingresos en cuenta, sino por revalorización bursátil.

Cada inversor es diferente con su visión y objetivos, por lo que considero que es bueno para mi igual no lo es para el resto.

Puede leer sobre mi preferencia en este tipo de acciones que pagan pocos o ningún dividendo aquí.

- Acciones con dividendos crecientes: Son mis segundo tipo de acciones favoritas, siempre que sigamos hablando de empresas de calidad. En estas compañías los dividendos suelen crecer todos los años, por lo que las rentas recibidas cada año van aumentando sin necesidad de hacer nada.

Puedes leer más sobre ellas y los aristócratas el dividendo pulsando en el enlace.

- Acciones con altos dividendos pero pay-out demasiado alto. En estas empresas corremos el riesgo de que hagan un recorte de dividendos o incluso lo cancelen, por lo que al igual que en toda inversión, es necesario mirar bien la contabilidad y las perspectivas de los negocios por si realmente nos encontramos ante una oportunidad o una trampa de valoración.

En definitiva, más que el objetivo final, lo importante es el camino a elegir y nuestra estrategia, sea de inversión en dividendos para generar rentas o no.

Ahorrar e invertir en bolsa es una de las mejores formas de enfrentarse a la inflación y si lo hacemos bien, aumentar nuestro patrimonio.

Por lo tanto, es tarea tuya hacer tus cálculos y determinar si merece la pena comprarte el último Iphone, o simplemente comprar acciones, ya sean de dividendos o no.

Si te ha gustado este artículo, no dudes en dejarme un comentario, compartirlo por redes sociales o suscribirte para recibir más contenido.

(adsbygoogle = window.adsbygoogle || []).push({});La entrada ¿Se puede vivir de los dividendos? se publicó primero en Pinigu.

Categorías: Blogs y opiniones de economia en español

El riesgo de invertir con los tipos de interés intervenidos

(adsbygoogle = window.adsbygoogle || []).push({});

Antes de la crisis financiera de 2008, en las universidades se estudiaba como una verdad indudable que cuando una entidad prestaba dinero a alguien, el primero recibía unos intereses a cambio de asumir un riesgo de contrapartida, sin que los tipos de interés pudieran ser negativos.

También, si un alumno hubiera hecho una simulación con precios del petróleo negativos, este habría recibido burlas y seguramente un suspenso por parte del profesor.

Pues bien, estos hechos han ocurrido en la última década, con la mayoría de los bonos de renta fija en terreno negativo y las bolsas en máximos. Además, todo esto en unos años, 2020 y 2021, en el que tenemos una pandemia mundial (COVID-19) asolando todas las economías.

¿Qué está ocurriendo entonces? ¿No deberían bajar las bolsas si la economía está en recesión? ¿Existe una burbuja financiera? ¿Es buen momento para invertir en bolsa?

La entrada El riesgo de invertir con los tipos de interés intervenidos se publicó primero en Pinigu.

Categorías: Blogs y opiniones de economia en español

#60. Inversión de crecimiento con Luis Miguel Ortíz

Categorías: Blogs y opiniones de economia en español

Los MODELOS MENTALES para tomar mejores decisiones

Categorías: Blogs y opiniones de economia en español

Cómo aprender a invertir en bolsa como los mejores

Desde que empecé a interesarme por la inversión en bolsa he estado pendiente de lo que hacían los mejores inversores. Recuerdo leer las cartas a los accionistas de Warren Buffett, ver los vídeos de las conferencias del antiguo equipo de Bestinver o leer con avidez El inversor Inteligente. Aunque con el tiempo he desarrollado mi propio estilo y personalidad invirtiendo, fueron sus enseñanzas las que me han convertido en el inversor que soy hoy.

La entrada Cómo aprender a invertir en bolsa como los mejores se publicó primero en Pinigu.

Categorías: Blogs y opiniones de economia en español

¿Cómo valorar empresas en bolsa?

(adsbygoogle = window.adsbygoogle || []).push({});

Cuando invertimos en bolsa a largo plazo, estamos poniendo nuestro dinero en compañías que realizan una actividad económica, y tienen un beneficio que nos pertenece en parte por ser accionistas.

La valoración de empresas es fundamental si queremos invertir con éxito sin depender de la suerte, pues nos dará la opción de analizar si estamos realizando una buena o mala adquisición teniendo en cuenta los riesgos que asumimos.

En este artículo se tratará el tema de cómo valorar empresas para invertir en bolsa, de la forma más simple y amena posible.

La entrada ¿Cómo valorar empresas en bolsa? se publicó primero en Pinigu.

Categorías: Blogs y opiniones de economia en español

Rentabilidad histórica y evolución del S&P 500, la bolsa de Estados Unidos.

(adsbygoogle = window.adsbygoogle || []).push({});

- El S&P 500 ha tenido una rentabilidad anualizada del 8,26% desde 1927 hasta 2020.

- Las FAANG cada vez pesan más en el principal índice de bolsa de Estados Unidos, haciendo del S&P 500 un índice cada vez menos diversificado.

- Solo el 0,1% de las veces no fue rentable mantener 20 años las acciones de este índice y ocurrió en el crack de 1929. El 99,9% restante siempre se ganó dinero.

- El mercado alcista más largo de la historia terminó en 2018 con una rentabilidad del 401% y una duración de 131 meses. El segundo finalizó en 2007 con un 417% de rentabilidad.

- -86% fue el resultado del mercado bajista más fuerte de la historia del índice, en la crisis de 1929.

Invertir en el S&P 500 históricamente ha sido hacerlo en uno de los índices más diversificados y seguros del mundo.

Esta diversificación se da porque el índice engloba las 500 mayores empresas de la bolsa de Estados Unidos, y está lejos de otras plazas como la española con el IBEX 35. Este último históricamente siempre ha sido muy dependiente de la banca en su ponderación. Además solo cuenta con 35 compañías , muchas de ellas por debajo de los 1.000 millones de capitalización.

En este artículo veremos y analizaremos el principal índice bursátil estadounidense, así como analizaremos su rentabilidad histórica a lo largo del tiempo y que se puede esperar de él en el futuro.

La entrada Rentabilidad histórica y evolución del S&P 500, la bolsa de Estados Unidos. se publicó primero en Pinigu.

Categorías: Blogs y opiniones de economia en español

¿Es Facebook una buena inversión?

(adsbygoogle = window.adsbygoogle || []).push({});

Facebook forma parte del selecto grupo de las FAANG (Facebook, Apple, Alphabet, Netflix y Google), que han sido historias de éxito. En el caso de la red social fundada por Mark Zuckerberg, los inversores que compraron en 2012 y mantuvieron su posición hasta hoy han conseguido multiplicar su inversión por 11,6 veces en 8 años, lo que nos da más de un 35% de rentabilidad anualizada.

En los últimos años las rentabilidades han disminuido, aunque siguen siendo excelentes, con crecimientos de doble dígito. Han sido las siguientes:

- 167,42% en los últimos 5 años, que es un 21,7% de rentabilidad anual.

- 54,6% de rentabilidad en los últimos 3 años, o un 15,6% anualizado.

- 19,7% de rentabilidad en el último año.

Este es el gráfico que ha dibujado la acción:

{kind=link}

¿Cuán ha sido el secreto de las acciones de Facebook para conseguir estos retornos? ¿Qué riesgos presenta la acción? Vamos a analizarlo:

La entrada ¿Es Facebook una buena inversión? se publicó primero en Pinigu.

Categorías: Blogs y opiniones de economia en español

Páginas

Custom Search