Se encuentra usted aquí

Agregador de canales de noticias

Biden Administration Moving Forward With Trump-Era Proposal For US Uranium Reserve

Biden Administration Moving Forward With Trump-Era Proposal For US Uranium Reserve

The Biden administration is taking steps to establish a US uranium reserve, a proposal put forward by the Trump administration which could boost mining of the mineral as well as the potential to expand nuclear energy in the United States.

"Yellowcake" uranium coming off a conveyor line{kind=link}

In Tuesday testimony before the Senate Energy and Natural Resources Committee, Energy Secretary Jennifer Granholm said that her department is laying the groundwork for such a move.

"We’re about to issue a request for information [RFI] regarding establishing a reserve," she said, adding "We are, I think this month, issuing an RFI on that."

Jennifer Granholm{kind=link}

In a major funding bill passed late last year, Congress set aside funds to establish the strategic reserve, which would buy US-mined uranium from domestic producers, which we assume is separate from the US reserves bought by Russia during Hillary Clinton's Uranium One scandal.

When asked why the Biden administration's budget request for 2022 didn't include funding for the reserve, Granholm cited the existing funding for the project.

"It had been appropriated for last year so it’s carrying over," she said.

A 2020 Trump administration report endorsed spending millions on the reserve, which would aim to boost domestic mining.

The concept is similar to that of the already existing strategic petroleum reserve, where the government can hold up to 714 million barrels of that fuel in case of an emergency. -The Hill

Zero Hedge readers will recall our coverage on the uranium sector, which we said in April was set to benefit from several factors - including upcoming infrastructure spending, the reddit short squeeze crowd, an extremely bullish case laid out by a BofA analyst, and a passionate tweetstorm by former hedge fund manager Hugh Hendry, who said "A lot of you are invested in uranium. I commend you. I wish I was. Uranium is the rockstar of commodities. It doesn't mess around - bull and bear markets are of epic proportions."

Furthermore, Michael "big short" Burry advocated for converting US to nuclear power as a way for Democrats to create jobs in a 'green' industry.

Related stocks moved higher on the news.

{kind=link}

And to review what we said in April:

The first reason is a mix of regulatory and market developments.

As we reported earlier today, the spot price for U3O8 moved above $30 per pound for the first time this year as uranium producers and mine developers hoovered up above-ground inventories and reactor construction continues apace. Two new research notes from BMO Capital Markets and Morgan Stanley say today’s price marks a floor and predict a rally in prices over the next few years to the ~$50 level by 2024, which - all else equal - would translate into soaring stock prices for names such as CCJ, UEC, URA and URNM.

Indeed, as Mining.com said, the stars seem to be aligning for a new phase of nuclear energy investment with the US, China and Europe bolstering the bull case for the fuel this month.

And while nuclear energy was not (yet) mentioned explicitly in the $2 trillion Biden infrastructure proposal released today, its federally mandated “energy efficiency and clean electricity standard” is hardly achievable without it.

Curiously, the big regulatory move may be coming out of Europe, where - as we expected - Uranium is now officially part of the cool ESG crowd as over the weekend leaked documents showed a panel of experts advising the EU is set to designate nuclear as a sustainable source of electricity which opens the door for new investment under the continent’s ambitious green energy program.

{kind=link}

Then there is China - as Mining.com notes, China’s 14th five-year plan released a fortnight ago also buoyed the uranium market with Beijing planning to up the country’s nuclear energy capacity by 46% – from 48GW in 2020 to 70GW by 2025. There are several factors working in uranium’s favor, not least the fact that annual uranium demand is now above the level that existed before the 2011 Fukushima disaster when Japan shut off all its reactors:

-

Uranium miners, developers and investment funds like Yellow Cake (13m lbs inventory build up so far) are buying material on the spot market bringing to more normal levels government and utility inventories built up over the last decade

-

Major mines are idled including Cameco’s Cigar Lake (due to covid-19) which accounts for 18m lbs or 13% of annual mine supply. The world’s largest uranium operation McArthur River was suspended in July 2018 taking 25m lbs off the market

-

Permanent closures so far this year include Rio Tinto’s Ranger operation in Australia (3m lbs) and Niger’s Cominak mine (2.6m lbs) which had been in operation since 1978. Rio is exiting the market entirely following the sale of Rössing Uranium in Namibia

-

Like Cameco, top producer Kazatomprom, which mined 15% less material last year due to covid restrictions has committed to below capacity production (–20% for the state-owned Kazakh miner) for the foreseeable future

-

Price reporting agency and research company UxC estimates that utilities’ uncovered requirements would balloon to some 500m lbs by 2026 and 1.4 billion lbs by 2035

-

Roughly 390m lbs are already locked up in the long term market while 815m lbs have been consumed in reactors over the last five years, according to UxC

-

There are 444 nuclear reactors in operation worldwide and another 50 under construction – 2 new connections to the grid and one construction start so far in 2021

-

Much cheaper and safer, small modular nuclear power reactors which can readily slot into brownfield sites like decommissioned coal-fired plants (or even underground or underwater) are expected to become a significant source of additional demand.

The last bullet brings us to reason number 2: the coming "small modular reactor" frenzy:

As Nikkei Asia reports today, one of Japan's top industrial engineering companies will join a US-led project to build a new type of nuclear power plant designed with added precautions against meltdowns. These plants will be built in the US, where they will propel the uranium sector to level it hasn't seen in decades (indicatively CCJ traded roughly double where it is today as just before the 2008 financial crisis).

According to the Nikkei, Japan's JGC Holdings will help build a plant in the state of Idaho designed by NuScale Power, an American company whose proposal for a small modular reactor (SMR) involves immersing the containment units in a pool of water.

Small nuclear reactors have been hailed as an option for replacing fossil fuel power plants as nations commit to cutting carbon dioxide emissions in the coming decade

And here, we get one step closer to Uranium becoming part of ESG: when Joe Biden meets Japanese Prime Minister Yoshihide Suga for a summit in the U.S. later this month, fighting climate change will be on the agenda and "small nuclear" - and uranium - will be high on the agenda.

JGC has invested $40 million for a roughly 3% stake in NuScale, one player in the emerging field of SMRs. The Japanese group will work with NuScale's parent, U.S.-based engineering company Fluor, on construction management and other aspects of the Idaho project.

One thing is clear: as the SMR strategy takes off, much more uranium will be needed, as the partners eventually could set their sights on similar projects in the Middle East - where JGC boasts a long track record in oil and petrochemical infrastructure - and Southeast Asia. In fact, the entire world could soon be covered in small, safe nukes which will lead to an unprecedented renaissance for the uranium sector.

Why the scramble for SMR?

The first reason is simple: price. Nuclear plants on the scale of 1,000 megawatts cost around $10 billion to build using established reactor designs. NuScale's SMR design - which completed a technical review by the U.S. Nuclear Regulatory Commission in August 2020, ahead of rival proposals - reportedly costs around $3 billion for more than 900 MW. The Idaho plant will have a capacity between 600 MW and more than 700 MW, according to announced plans. NuScale also has a strategic partnership with South Korea's Doosan Heavy Industries and Construction, which will supply components for the plant.

The second, and far more important reason, is safety. Japan's Fukushima nuclear disaster a decade ago shows what happens when reactor cooling systems break down. The loss of emergency power after a devastating 2011 tsunami led to reactor meltdowns at the Fukushima Daiichi plant operated by Tokyo Electric Power Co. Holdings. Well, NuScale's SMR design seeks to remove this risk, as the water in the pool takes a month to evaporate and helps keep the reactor's temperature down.

The U.S. government supports research and development in small-scale reactors. A Green Growth Strategy announced by Japan last year calls for "providing active support" to Japanese companies participating in experimental overseas projects in this field. Many existing nuclear plants in Japan, the U.S. and other advanced economies have been in operation for decades and require upgrades or decommissioning.

In short, between recent bullish market dynamics, and a sector that is on the cusp of becoming the next ESG craze, the promise of new SMR technologies could ensure uranium demand is stable for decades, leading to a new golden age for uranium stocks.

Tyler Durden Tue, 06/15/2021 - 14:15

Categorías: Blogs y opiniones de economia en ingles

Watch: Roger Waters Tells "Little Pr**k" Zuckerberg To "F**k Off" Following Request To Use Iconic Pink Floyd Song For Ad

Watch: Roger Waters Tells "Little Pr**k" Zuckerberg To "F**k Off" Following Request To Use Iconic Pink Floyd Song For Ad

Authored by Steve Watson via Summit News,

Pink Floyd song writer Roger Waters slammed Mark Zuckerberg during a press conference recently, announcing that the Facebook owner had offered a “huge, huge amount of money” to use the iconic song Another Brick In The Wall Part II in an advert for Instagram.

{kind=link}

Speaking at an event to raise awareness about imprisoned WikiLeaks founder Julian Assange, Waters noted the deep deep irony of Facebook wanting to buy and use a song that rails against ‘thought control’ and mindless conformity.

Waters described the development as part of Zuckerberg’s “insidious movement… to take over absolutely everything.”

Waters read out Facebook’s request, which noted “We want to thank you for considering this project. We feel that the core sentiment of this song is still so prevalent and so necessary today, which speaks to how timeless the work is.”

“And yet, they want to use it to make Facebook and Instagram more powerful than it already is,” Waters urged, adding “so that it can continue to censor all of us in this room and prevent this story about Julian Assange getting out into the general public so the general public can go, ‘What? No. No More.’”

“So it’s a missive from Mark Zuckerberg to me… with an offer of a huge, huge amount of money and the answer is, ‘f**k you! No f**king way!’,” Waters boomed to rapturous applause.

“I will not be a party to this bullsh-t, Zuckerberg,” Waters added.

He then asked “How did this little pr**k, who started off going, ‘She’s pretty, we’ll give her a four out of five. She’s ugly, we’ll give her a one’… How the f**k did he get any power in anything?”

“And yet here he is, one of the most powerful idiots in the world,” Waters emphasised.

Watch:

“¡Vete a la chingada!”: @rogerwaters a Mark Zuckerberg. El músico contó que le ofrecieron “una gran cantidad de dinero” por permitir el uso de Another brick in the wall II para promover Instagram. Lo narró en un acto por la libertad de Julian Assange (@Wikileaks)#VideosLaJornada pic.twitter.com/gEVqaor8Eo

— La Jornada (@lajornadaonline) June 12, 2021Following media attention, Waters requested trolls to pile on and call him a hypocrite for posting the video on “Zuckerberg’s crappy censored platform”:

.@petercronau, thank you for paying attention brother. Calling all trolls, come on you pricks, call me a hypocrite for posting this on Zuckerberg’s crappy censored platform @Facebook now. https://t.co/3NYrW7Pw2i

— Roger Waters (@rogerwaters) June 12, 2021You would know for sure that we had descended into dystopian hell if this song was ever approved for promoting shiny Instagram graphics, urging kids to sign up to liquify their brains and act like every other insta-zombie uploading 4 million selfies every second:

* * *

Brand new merch now available! Get it at https://www.pjwshop.com/

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. We need you to sign up for our free newsletter here. Support our sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Also, we urgently need your financial support here.

Tyler Durden Tue, 06/15/2021 - 14:00

Categorías: Blogs y opiniones de economia en ingles

Arizona Senator: State Lawmakers Prepared To Act On Findings From Election Audit

Arizona Senator: State Lawmakers Prepared To Act On Findings From Election Audit

Authored by Zachary Stieber via The Epoch Times,

The Arizona legislature is ready to take action if the election audit taking place in the state’s largest county uncovers irregularities, a state senator said.

“It’ll be our duty to act in whatever way is appropriate,” Arizona Sen. Wendy Rogers, a Republican who has been closely tracking the audit in Maricopa County, told The Epoch Times.

Auditors, led by Florida-based Cyber Ninjas, started reviewing ballots from the 2020 election at Veterans Memorial Coliseum in Phoenix last month, along with machines used in the contest and other election materials. Auditors expect to finish their work by the end of this month. They will then produce a report outlining what they found.

{kind=link}

Contractors working for Cyber Ninjas, who was hired by the Arizona State Senate, work during a 2020 election audit at Veterans Memorial Coliseum in Phoenix, Ariz. on May 1, 2021. (Courtney Pedroza/Getty Images)

Arizona Senate President Karen Fann, a Republican who authorized the audit, said last month that she thinks some irregularities will be uncovered.

“I hope we don’t find anything serious. I think we’ll find irregularities that is going to say, you know what, there’s this many dead people voted, or this many who may have voted that don’t live here anymore. We’re going to find those,” she said.

Alexander Kolodin, who formerly represented Cyber Ninjas and remains a lawyer for the Arizona GOP, said in a recent interview that the audit “is going to show that something went wrong, because something goes wrong in every election.”

“I think even Maricopa County would probably admit that the question is, to what degree did it go wrong? Okay, that’s question one. But even that doesn’t tell you so much. It went wrong, and someone caused it to go wrong. The next question is, does the audit tell you who caused it to go wrong?” he said on NTD’s “Wide Angle.”

“If the audit illuminates that there’s [sic] vulnerabilities in X, Y, and Z parts of our election system, state legislatures can target those with a laser beam and fix X, Y, and Z parts of our election system,” he added.

{kind=link}

Maricopa County ballots cast in the 2020 general election are examined and recounted by contractors working for Florida-based company, Cyber Ninjas, at Veterans Memorial Coliseum in Phoenix, Ariz., on May 6, 2021. (Matt York/AP Photo/Pool)

If the audit reveals fraud, then there would be a referral to law enforcement authorities, according to Fann. The Arizona Senate would focus on closing any loopholes in the election system.

Speaking just hours after spokespersons for the audit shot down rumors that hundreds of thousands of ballots were found missing, Rogers said she’s not sure what auditors will uncover.

“As of now we do not know what the results will be,” she said.

The first-term state senator, a retired U.S. Air Force pilot, has been keeping close tabs on the audit. She has been a regular presence at the coliseum, consulting with Cyber Ninjas CEO Doug Logan and helping lead tours for legislators from other states who want to see what’s happening.

Delegations from over a dozen states, including Georgia, Pennsylvania, and Virginia, have visited the audit in recent weeks.

“They want to come in to see what a gold standard forensic audit is and this is a real deep dive into not only counting the ballots, but looking at the machines and interestingly, examining very closely, microscopically if you will, the ballots themselves,” she said. “They have been blown away.”

Pennsylvania Sen. Doug Mastriano, a Republican who toured the coliseum, told The Epoch Times last week that he was impressed by what he saw. He recommended lawmakers from battleground states go to Arizona to tour the facility. Pennsylvania Republicans are pushing for a similar audit in their state, but leadership has not yet decided on whether to order one.

Rogers wanted people to know that Arizonans “are resolute” and “will never quit” on election integrity efforts.

“We will get to the bottom of the truth, not only for truth’s sake, but also to restore election integrity for 2022,” she said.

Tyler Durden Tue, 06/15/2021 - 13:54

Categorías: Blogs y opiniones de economia en ingles

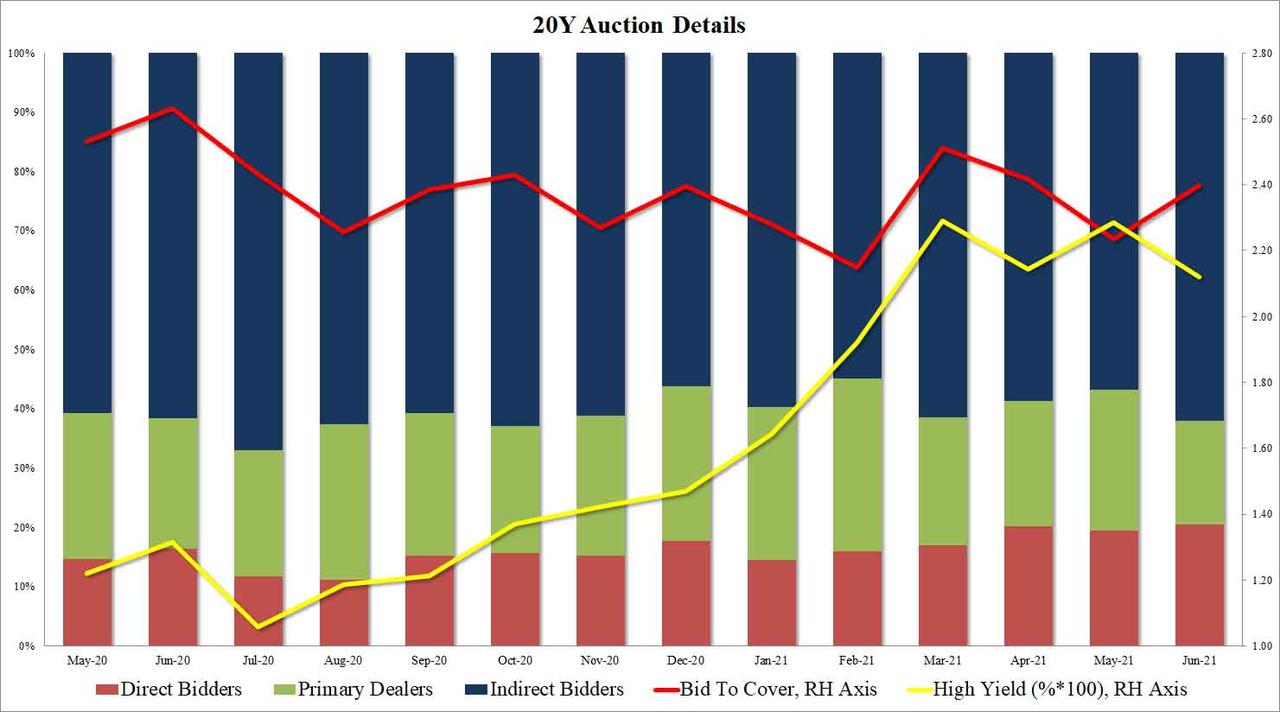

Record High Directs, Record Low Dealers In Blockbuster 20Y Auction

Record High Directs, Record Low Dealers In Blockbuster 20Y Auction

Coming several days after the trifecta of benchmark auctions when both the 10Y and 30Y auctions demonstrated solid demand despite a blistering hot CPI print, moments ago the Treasury sold another $24BN in 20Y paper in the form of a 19Y-11M reopening of Cusip SY5 which, too, was greeted with stellar demand.

The high yield of 2.12% was not only far below last month's 2.286% but was also the lowest since February's sub-2% auction; it also stopped 1.7bps through the When Issued, the biggest stop through since March's 2.0bps.

The bid to cover of 2.40 was also a solid improvement to the 2.24 in May and the 2.33 6-auction average, while the internals were perhaps the most impressive, with Indirects taking down 62.1%, the highest since October and far above the 58.0% recent average, and with Directs taking down 20.4%, or the most since the 20Y auction restarted in May, Dealers were left with just 17.5%, the lowest Dealers takedown on record.

{kind=link}

Overall, a stellar 20Y auction which despite the lack of concession saw tremendous buyside demand. Yet despite the blockbuster result there was barely a move in the curve, with the 10Y trading virtually unchanged from before the 1PM deadline.

Tyler Durden Tue, 06/15/2021 - 13:41

Categorías: Blogs y opiniones de economia en ingles

Pfizer, Moderna Jabs Cause Heart Inflammation In Some Young Men, CDC Finds

Pfizer, Moderna Jabs Cause Heart Inflammation In Some Young Men, CDC Finds

As American public health officials and political leaders struggle to entice more young adults to accept the COVID-19 vaccine, researchers have just discovered a disturbing side effect of the Pfizer and Moderna jabs, which rely on new mRNA technology to program the body to fight the virus. While the adenovirus-vector jabs like the AstraZeneca shot have been tied to dozens of fatal cerebral blood clots, the mRNA vaccines have now been found to cause heart inflammation in some patients.

We first caught wind of this late last week when the CDC announced it would hold an "emergency meeting" about the rising number of heart inflammation cases in the US VAERs database.

YOU STUPID, STUPID STUPIDS.

This was so predictable. pic.twitter.com/oHKFgR9vF4

According to Reuters, the CDC started investigating after Israel's Health Ministry reported that it had discovered a likely link to the condition in young men who received the Pfizer jab. Although some patients were hospitalized, most recovered on their own and (most importantly) nobody died.

{kind=link}

The CDC told Reuters that it's still assessing the risk from the condition and has not yet concluded that there was a causal relationship between the vaccines and cases of myocarditis or pericarditis. Still, there are some lingering signs that the potential side effects from the vaccines is higher for young people. More than 50% of the cases reported to the US Vaccine Adverse Event Reporting System - better known as VAERS - after people had received their second dose of the jab were in people between the ages of 12 and 24, the CDC said. Those age groups accounted for under 9% of doses administered.

"We clearly have an imbalance there," said Dr. Tom Shimabukuro, deputy director of the CDC's Immunization Safety Office, during a presentation to an advisory committee to the agency on Thursday. The bulk of these cases have emerged within a week of vaccination. Shimabukuro added that doctors saw a "preponderance" of young white men. This contrasts with the AstraZeneca brain clots, which overwhelmingly afflicted women. Just under 80% of all of these cases were found in men.

Scientists knew something was wrong because, according to VAERS, there were 283 observed cases of heart inflammation after the second vaccine dose in patients aged 16 to 24. That's compared with an expectations of 10-to-102 cases tally for that age group based on demographic data.

Another database, the Vaccine Safety Datalink, also showed a jump in incidents of heart inflammation in younger men after their second shot when compared to the rate seen after jab 1.

Meanwhile, Pfizer said it supports the CDC's assessment of the heart inflammation cases, noting that "the number of reports is small given the number of doses administered." Already 130MM Americans have already received both of the Pfizer, or both of the Moderna, jabs. Moderna spokespeople cautioned that consumers shouldn't jump to conclusions before scientists have had time to further study this issue. At this point, health authorities officially consider both vaccines to be "safe" for public use. Moderna also claimed that researchers hadn't established a "causal" relationship between the jabs and the heart complications.

OF course, it's just the latest reminder of the drawbacks when authorities take short cuts to approve vaccines.

Tyler Durden Tue, 06/15/2021 - 13:39

Categorías: Blogs y opiniones de economia en ingles

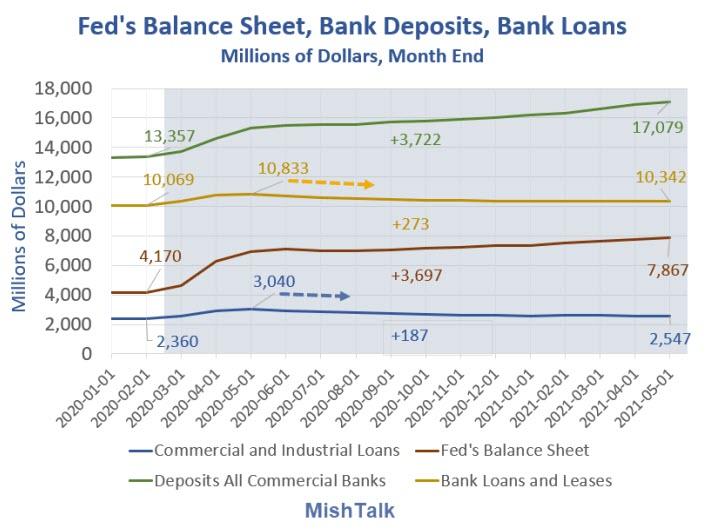

Charts That Should Scare The Pants Off The Fed (And Probably Do)

Charts That Should Scare The Pants Off The Fed (And Probably Do)

Authored by Mike Shedlock via MishTalk.com,

Let's investigate the relationship between the Fed's QE program, bank lending, and alleged stockpiling of cash...

{kind=link}

In an effort to stimulate bank lending and thus the economy, the Fed launched a massive QE program that lowered interest rates and crammed money into banks.

Let's take a look at some numbers.

January 1973 Numbers-

Commercial and Industrial Loans: $135 Million

-

Fed's Balance Sheet: $0

-

Bank Deposits: $599 Million

-

Bank Loans and Leases: $405 Million

-

Commercial and Industrial Loans: $2.547 Trillion

-

Fed's Balance Sheet: $7.867 Trillion

-

Bank Deposits: $17.079 Trillion

-

Bank Loans and Leases: $10.342 Trillion

{kind=link}

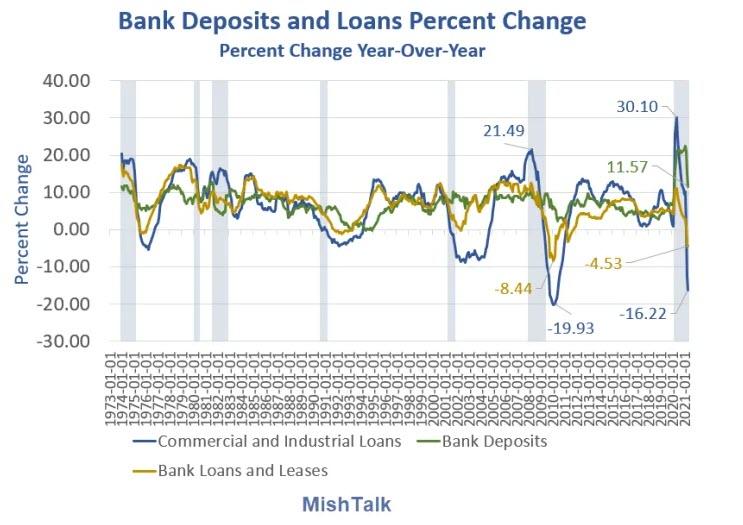

Year-over-year commercial and industrial loans are down 16.22%, loans and leases are down 4.53%, and deposits are up 11.57%.

The last time year-over-year commercial loans and loans and leases were negative for two consecutive months (as they are now) was August 2010.

However, these are distorted figures.

Notice the big 30% year-over-year spike in commercial and industrial loans in May of 2020. Year-over-year loans and leases also surged 11.12%. Those surges were artificial and related to government programs and guarantees.

The best way of looking at things is a month-by-month take since the beginning of the recession.

Loans, Bank Deposits, and the Fed's Balance Sheet Details{kind=link}

Since May of 2020, bank loans and leases, and commercial loans have shrunk in a continuous fashion. Both are barely above where they were pre-Covid-19.

Pre-Covid-19 to May of 2021-

Bank Deposits: +3.7 Trillion

-

Fed's Balance Sheet: +3.7 trillion

-

Bank Loans and Leases: +0.3 Trillion

-

Commercial and Industrial Loans: +0.2 Trillion

Is this all we get out of expansion of the Fed's balance sheet by $3.7 trillion, from $13.4 trillion to $17.1 trillion coupled with trillions of dollars of stimulus from Congress?

I am afraid so. And it means businesses just do not want to expand.

Corporations are borrowing, but from the corporate bond market, not banks, and just to have money, not to expand.

Small to mid-sized businesses that depend on banks are not borrowing at all.

What About Jamie Dimon?Good question. Please recall Jamie Dimon Stockpiles Cash, Thinks Inflation is Here to Stay, Fears PayPal

“If you look at our balance sheet, we have $500 billion in cash, we’ve actually been effectively stockpiling more and more cash waiting for opportunities to invest at higher rates,” Dimon said. “I do expect to see higher rates and more inflation, and we’re prepared for that.”

I commented:

Even if Dimon believes the inflation setup, I do not buy his story as he presents. He could have and should have mentioned the QE aspect as to why banks are sitting on cash.

Stockpiling Cash?Dimon is not really stockpiling cash. Rather, Banks are So Stuffed With Cash They Tell Companies: No More Deposits

Since March of 2020, the Fed's balance sheet is up by $3.7 Trillion and bank deposits are also up by $3.7 trillion.

This we call "stockpiling cash" or (Dimon talking trash), take your pick.

Amazingly,

-

The Fed crams trillions of dollars down banks' throats.

-

Banks tell corporations no more deposits because they are losing money on them. Alternatively banks have to raise capital.

-

So corporations turn to money market funds.

-

The money market funds do not know what to do with the cash either.

-

So the Fed is forced to take a half trillion dollars back.

-

The Fed said this was expected and is working exactly as designed.

Thank You Fed!

Tyler Durden Tue, 06/15/2021 - 13:17

Categorías: Blogs y opiniones de economia en ingles

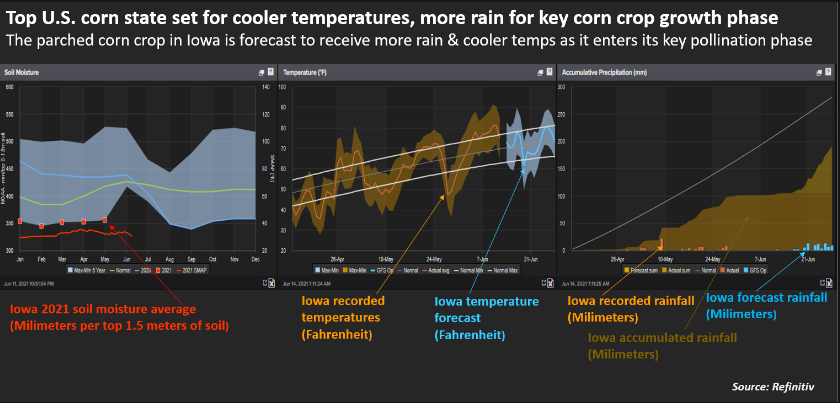

Corn, Soy Futures Slump As Weather Models "Flipped Cooler"

Corn, Soy Futures Slump As Weather Models "Flipped Cooler"

Corn and soybean futures started the week off on the wrong foot after weather forecasts improved crop conditions in the Midwest, including cooler temperatures and the possibility for rain later this week, according to Refinitiv's commodity desk.

On Monday, it was a slaughterhouse for corn and soybean futures, Chicago Board of Trade (CBOT) July corn futures settled down 3.7% at $6.59-1/4 per bushel, and CBOT July soybeans were down 2.4%, at $14.72-1/4 a bushel. By Tuesday morning, corn futures are lower by half a percent, and soybeans are up by half a percent.

Source: Refinitiv{kind=link}

"The ags sold off with gusto overnight after weekend weather models flipped cooler and wetter for many key crop production areas of the United States," Arlan Suderman, StoneX chief commodities economist, wrote in a note.

Source: Refinitiv{kind=link}

Cooler weather models signify relief after we showed weather forecasts that suggested dryness and heat across the corn belt. Still, threats of a megadrought linger for the western half of the country as surface soil moisture for early June is the worst in two decades.

{kind=link}

Last week, the USDA progress report rated 68% of the corn crops as good to excellent, down four percentage points from the prior week, and 62% of the soy crop was good to excellent, down five percentage points. The downward rating has to do with the dryness of surface soil moisture.

"Early planted crops are starting to show moisture stress," Iowa Secretary of Agriculture Mike Naig said in a statement. Iowa is the top producing state for corn production and number two in soybeans.

In a completely separate fundamental driver, corn and soybeans prices slumped the last week after the Biden administration may consider scaling down biofuel blending in fossil fuels and provide assistance to oil refiners.

S&P GSCI Agriculture Index is down more than 13% in 23 trading sessions from its all-time-high in early May of $474.

{kind=link}

Peak ag prices?

Tyler Durden Tue, 06/15/2021 - 13:00

Categorías: Blogs y opiniones de economia en ingles

Supply-Chain Chaos: Container Rates Skyrocket Even Higher... And There’s No End In Sight

Supply-Chain Chaos: Container Rates Skyrocket Even Higher... And There’s No End In Sight

By Greg Miller of FreightWaves,

Another week, another record for container shipping spot rates. And alarmingly for shippers, upward rate momentum is accelerating.

Container ships unloading in Oakland (Photo: Shutterstock/Sheila Fitzgerald){kind=link}

Different indexes come up with different numbers, and the premium charges on top of spot rates are now so high that index rates no longer capture the true cost of ocean shipping. However, when various indices all move in the same direction, it does reflect changes in the supply-demand balance. That balance is tipping more to the detriment of cargo shippers with each passing week.

“We haven’t seen the worst of it — $20,000 [per FEU] all-in rates to the East Coast are coming,” predicted Steve Ferreira, CEO and founder of Ocean Audit.

Peak season is just around the corner and supply chain disruptions remain widespread. COVID-disrupted ports in China and Malaysia are the latest hot spots. “It clearly appears that supply chain problems are worsening and not improving,” warned Lars Jensen, CEO of Vespucci Maritime.

Asia-East Coast rates jumpThe Freightos Baltic Daily Index for Asia-East Coast surged by around 20% in just the past few days. As of Thursday, the Freightos rate reached $9,317 per FEU, its highest point ever and up 224% year on year (y/y).

The Drewry weekly assessment for the Shanghai-New York route was $8,251 per FEU, up 9% week on week (w/w) and 203% y/y.

Rates in dollars per FEU. Green line = Drewry weekly Shanghai-New York. Blue line = Freightos daily Asia-East Coast. Chart: FreightWaves SONAR (To learn more about FreightWaves SONAR, click here.){kind=link}

S&P Global Platts provides daily assessments of Freight All Kinds (FAK) rates. Its North Asia-East Coast FAK assessment, as of Thursday, was $6,800 per FEU, up 152% y/y.

Asia-West Coast rates also jumpThere have recently been big moves up for rates to West Coast ports, as well.

Freightos put Thursday’s Asia-West Coast spot rate at a record-high $6,341 per FEU, up 194% y/y. Drewry’s weekly Shanghai-Los Angeles index is at $6,313 per FEU, up 6% w/w and 199% y/y.

Rates in dollars per FEU. Green line = Drewry weekly Shanghai-Los Angeles. Blue line = Freightos daily Asia-West Coast.{kind=link}

S&P Global Platts’ North Asia-West Coast North America FAK rate was $4,200 per FEU on Thursday, almost triple the FAK rate a year ago.

Panama spread keeps wideningAsia-East Coast rates have been rising faster than Asia-West Coast rates, according to Freightos’ data.

As a result, Freightos’ East Coast-West Coast spread — the premium importers pay to take the long route via the Panama Canal — hit $2,976 per FEU on Thursday, a record high. It has spiked in recent days.

Rates in dollars per FEU. Blue line = Premium of Freightos daily Asia-East Coast over Freightos daily Asia-West Coast. Trans-Atlantic westbound rates keep rising{kind=link}

At first, the trans-Atlantic westbound route from Europe to the East Coast averted the massive rate inflation seen on other lanes. That reprieve ended in April. Freightos’ Europe-East Coast assessment for Thursday was $5,193 per FEU, a new record and up 164% y/y.

Underscoring how different indexes come up with different figures, Drewry’s number is much lower than Freightos’. Drewry put Rotterdam-New York rates at $3,988 per FEU, up 66% y/y.

Rates in dollars per FEU. Green line = Drewry weekly Rotterdam-New York. Blue line = Freightos daily Europe-East Coast.{kind=link}

During an interview last month, Nerijus Poskus, Flexport’s vice president of global ocean, told American Shipper, “The most interesting to me is the trans-Atlantic, where prices have hit over $5,000 [per FEU, westbound]. It is quite balanced between imports and exports and while eastbound pays less than westbound, it still pays well. So, in my opinion, the trans-Atlantic is the best money-maker for shipping lines these days.”

Trans-Pacific exports: Full and emptyRates for U.S. exports out of the West Coast to Asia have also jumped, albeit off a far lower base. Freightos assessed rates on this route at $1,208 per FEU on Thursday, up 154% y/y. Drewry’s weekly rate is lower: $808 per FEU, up 61% y/y.

Rates in dollars per FEU. Green line = Drewry weekly Los Angeles-Shanghai. Blue line = Freightos daily West Coast-Asia.{kind=link}

The trans-Pacific has always been much less balanced than the trans-Atlantic — and is now even more so. There is a scramble to get empty containers to West Coast ports so they can be returned to Asia and used for U.S. imports. This is leading to never-before-seen patterns in rail data.

FreightWaves SONAR has proprietary data on a portion of movements of loaded and unloaded international containers by rail, including 20- and 40-foot units.

Usually, loaded inbound international containers to Los Angeles/Long Beach carrying export cargoes are around double the volume of empty containers arriving at the ports.

The spread between the two narrowed at the beginning of the year, and since April, international rail empties covered by the dataset arriving in Southern California have exceeded loaded inbound boxes. The gap is widening. On Thursday, the volume of inbound empties arriving in Los Angeles/Long Beach was 46% higher than the loaded rail volume.

Blue line = loaded international containers inbound to Los Angeles by rail included in dataset. Green line = empty international containers.{kind=link}

Another highly unusual pattern has emerged in Chicago, yet another indicator of the rush to get empties back to Asia.

Last year, the number of loaded international containers included in the proprietary dataset leaving Chicago by rail was around double the outbound empty units. But this month, outbound empties surpassed outbound loaded international boxes.

Blue line = loaded full international containers outbound from Chicago by rail included in dataset. Orange line = empty international containers{kind=link}

On a relative basis, the shift is even clearer. The number of loaded full containers covered by the dataset that were leaving Chicago on Thursday was down 4% y/y, while empties were up 62% y/y.

Blue line = change in full international containers outbound from Chicago by rail included in dataset versus June 11, 2020. Green line = change in empty international containers{kind=link}

According to FreightWaves Maritime Expert Henry Byers, “The situation with international containers in Chicago is yet another major indicator of how severe the supply side problems are.”

Tyler Durden Tue, 06/15/2021 - 12:40

Categorías: Blogs y opiniones de economia en ingles

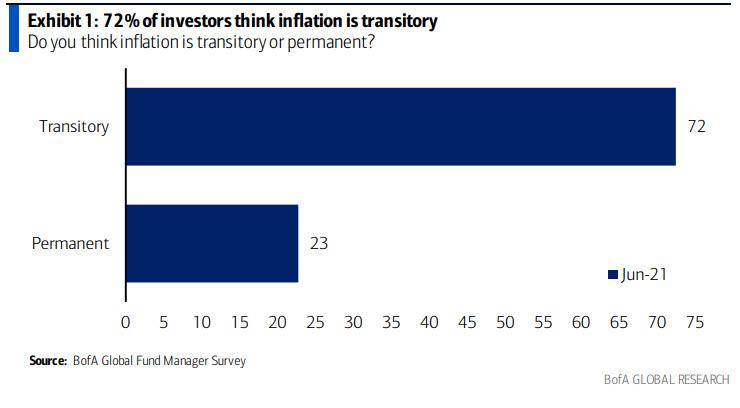

Wall Street Goes Full Fed Groupthink: 72% Think Inflation Is "Transitory"

Wall Street Goes Full Fed Groupthink: 72% Think Inflation Is "Transitory"

We have previously slammed the Bank of America Fund Manager Survey which over the past two years lost all "signal" and mutated into a noisy exercise of virtue signaling and meaningless posturing, where the respondents say not what they actually think or do, but merely regurgitate trite convention goalseeking what they think the "right answer" should be so they aren't ostracized by their peers. Worse than that, the survey now simply reflects whatever prevailing prices telegraph, and instead of seeking to predict or discount the future, Wall Street best (paid) and brightest have become a herd of mindless cattle, swaying in the wind from one liquuidity injection to the next, without every formulating an opinion (one can't really blame them for this though, if anyone is to blame, it's the Fed for destroying what little market efficiency remained).

The release of today's latest FMS (in which BofA CIO Michael Hartnett polled 224 panelists managing $667BN between June 4 and 10th), was a case in point: the punchline of the report that the vast majority of Wall Street pros now siding with the Fed (and taking the other side of the trade to such luminaries as Paul Tudor Jones and Kyle Bass), as 72% said inflation is "transitory", while less than a quarter, or 23% view inflation as permanent.

{kind=link}

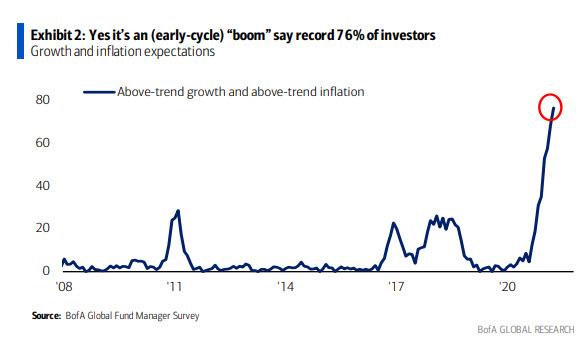

And just to cement their laughable view, a record 76% says that the US economy - with its $24 trillion in debt - is currently "early cycle", i.e. a boom.

{kind=link}

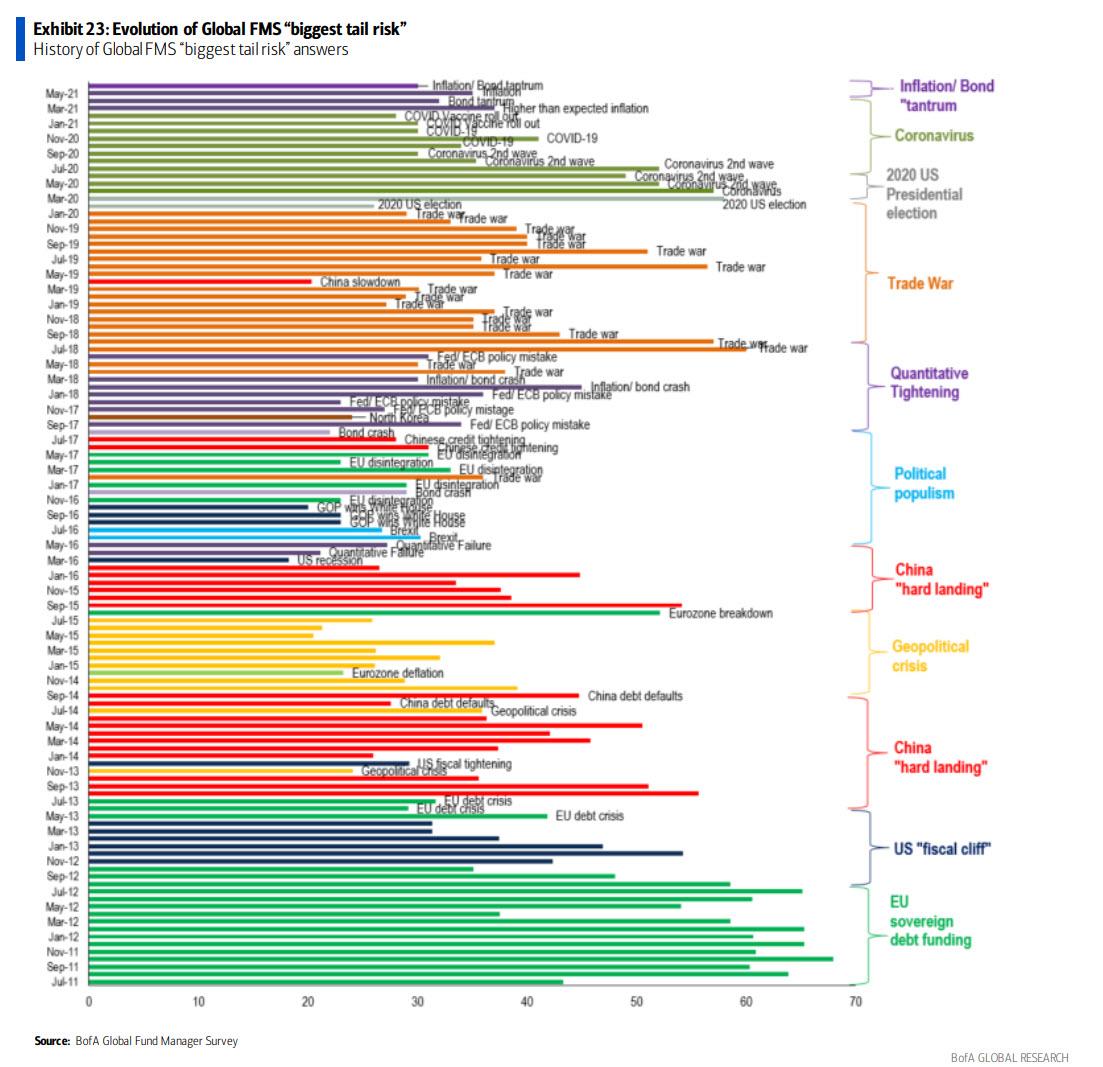

Hilariously, and a testament to just how little said "fund managers" believe their own BS, the biggest tail risk according to the same sample of respondents was... inflation.

{kind=link}

But why, if it' transitory? Actually, ignore that: such rhetorical questions that seek to maintain some intellectual consistency within the Fund Manager Survey - which just last month saw bitcoin as the "most crowded trade" even though virtually none of the respondents are actually allowed to trade it - are a total waste of time, as is trying to divine some predictive signal out of the survey which is impossible as it has devolved into a worthless snapshot of goupthink, and if anyone wants to get the right trade, our advice is just to do what the majority on Wall Street pretends to do or believe.... especially when said fake conviction is on the same side as the Fed.

So with that in mind, and with the clear understanding that the only way to use any of this data is to take the other side of the trade, here are some other findings from the latest FMS (which really should rename itself FBS):

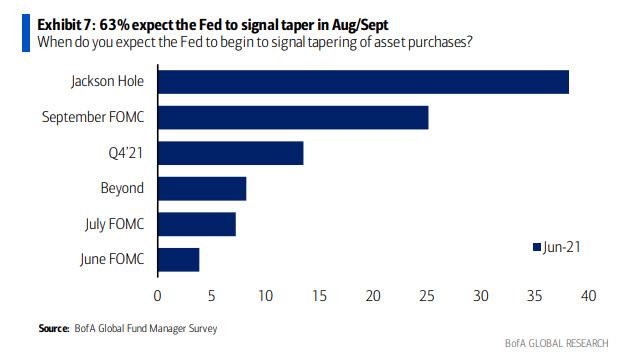

63% expect Fed to signal taper Aug/Sept, with virtually nobody expecting the Fed to even so much as hint at tapering tomorrow or July. Translation: it will be a very boring summer.

{kind=link}

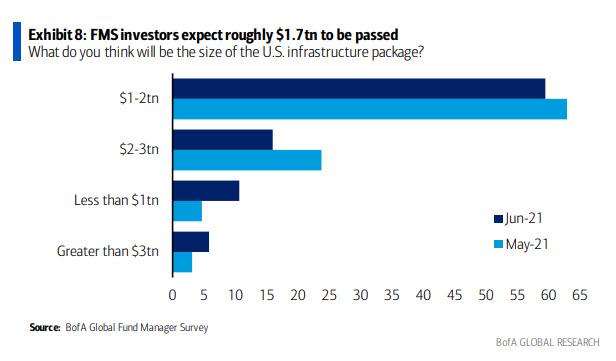

One reason for the pullback in inflationary expectations is the pessimism that Biden can get any more stimmies done, and as the next chart shows, US infrastructure hopes dip to $1.7tn from $1.9tn...

{kind=link}

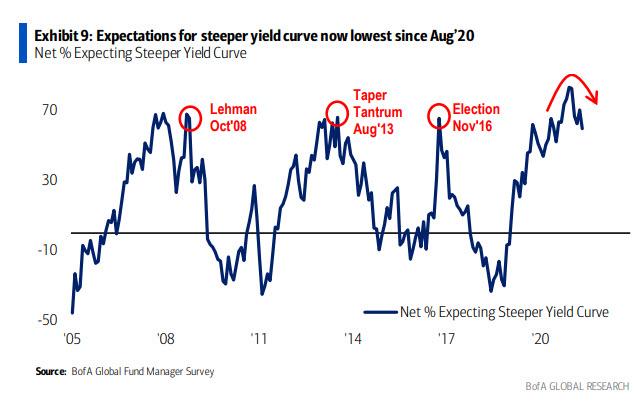

... which has also pushed expectations for a steeper yield curve to the lowest since Aug’20 (i.e. the flattening is about to come back).

{kind=link}

Meanwhile, the red-line in 10Y yields that will spark a stock selloff keeps rising: as BofA notes, ";Nobody believed that rates at 1.5% would cause an equity correction. But the move from 1.5% to 2% is critical as a large majority of investors now think rates >2% would be detrimental for stocks. "

{kind=link}

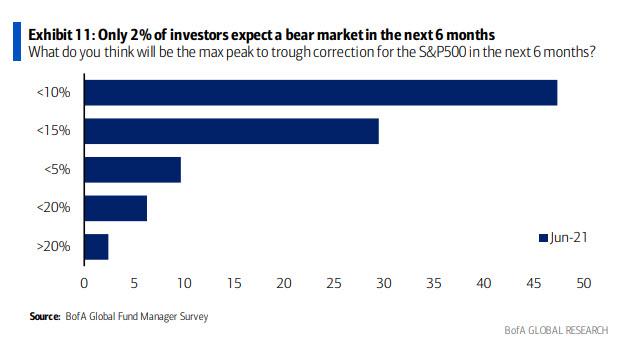

In addition to enjoying the safety of the herd and lack of original groupthink, the surveyed wall street pros also tend to be quite optimistic, and while few expect any economic turmoil any time soon, only 2% expect a bear market in the next 6 months: "Asked how big an equity correction will be likely in the next 6 months, FMS investors say <5% (10%), <10% (47%), <15% (29%), <20% (6%), bear market (2%)."

{kind=link}

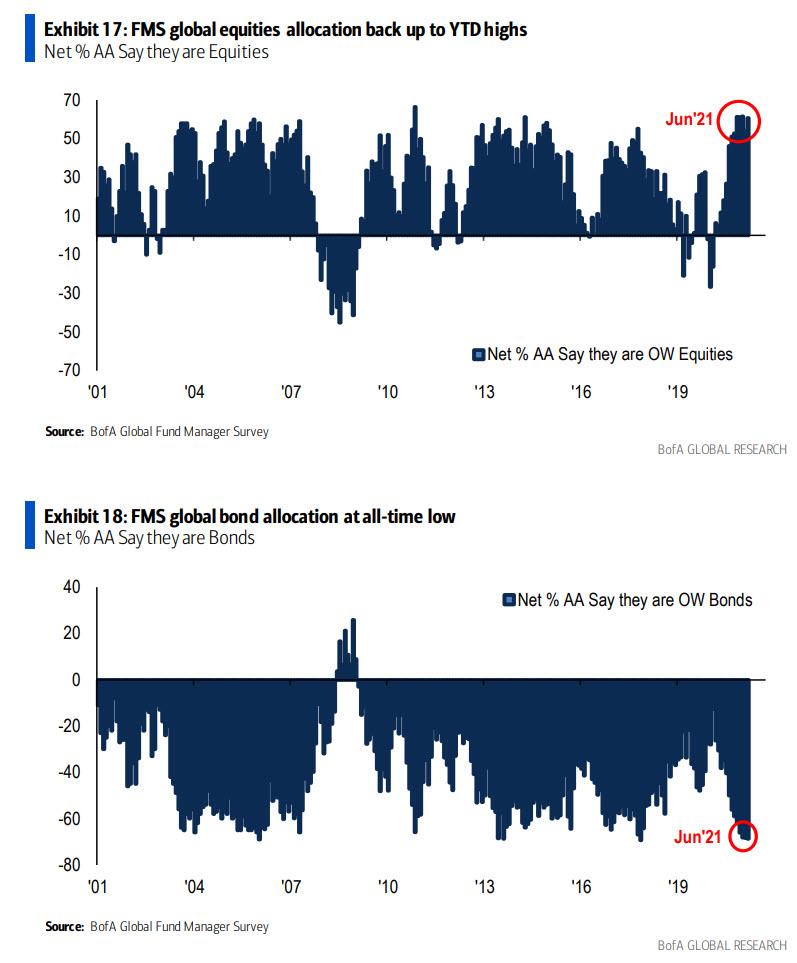

Some other observations: the survey found that cash levels are down to 3.9% from 4.1% last month...

{kind=link}

... while allocation to bonds fell to 3-year low at net -69%, and stocks allocation back up to YTD highs at 61%. This means that we are going to see another major bond short squeeze in the comings days.

{kind=link}

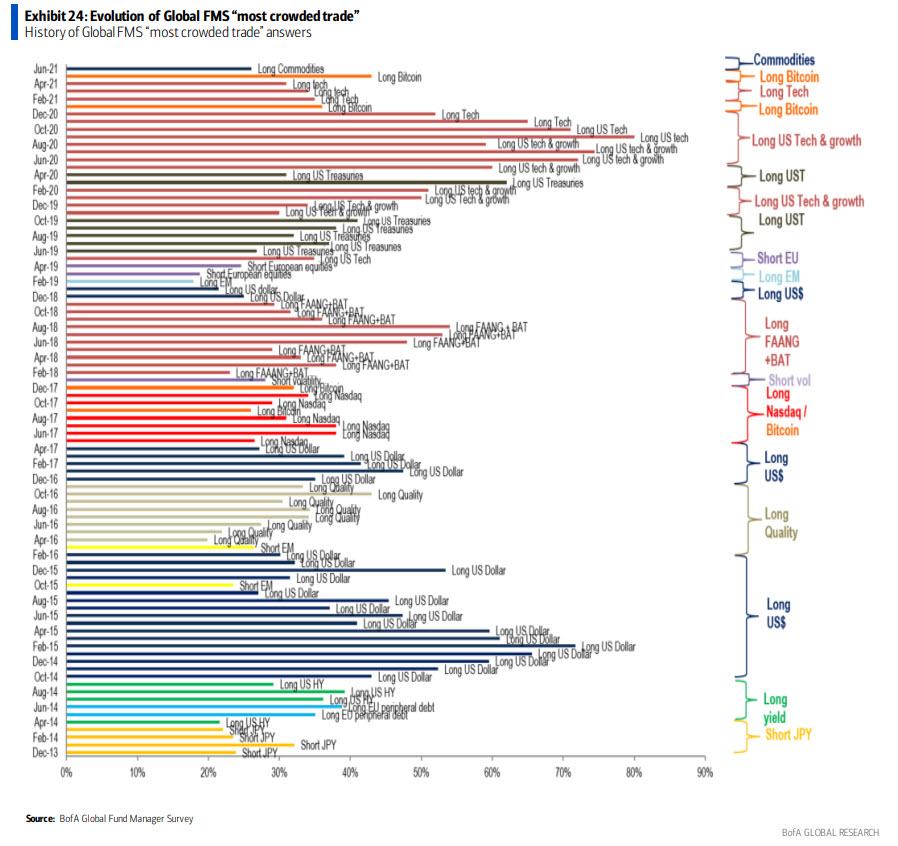

And speaking of projecting, for the first time in BofA survey history, commodities is now the top most crowded trade, as it overtakes "long Bitcoin" as most “crowded trade.”

{kind=link}

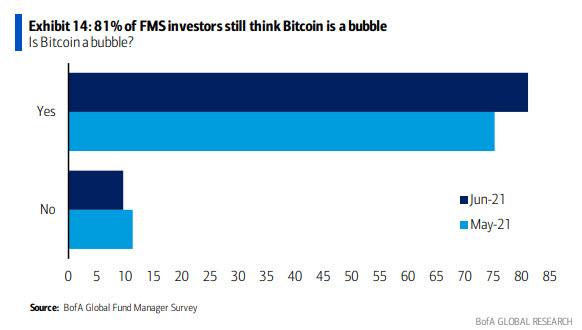

Meanwhile, since nobody can trade it and everyone has missed the move higher, 81% of jealous jaded investors still think Bitcoin is a bubble despite the price pullback. Well, good luck getting rich daytrading AMC.

{kind=link}

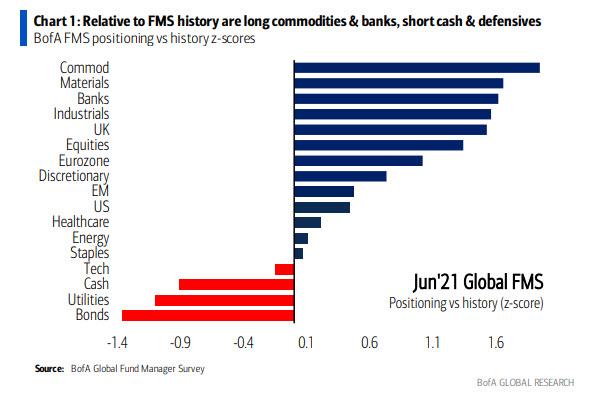

Finally, some views on positioning: Hartnett says that based on survey responses, banks are now the biggest sector overweight at 30%, while “chunky” cyclical positioning persists on materials at 23%, industrials, U.K., euro area. Allocation to euro area stocks increased 6ppt MoM to net 41% overweight, highest since January 2018, while allocation to U.K. equities increased 2ppt to 4% overweight, highest since March 2014.

{kind=link}

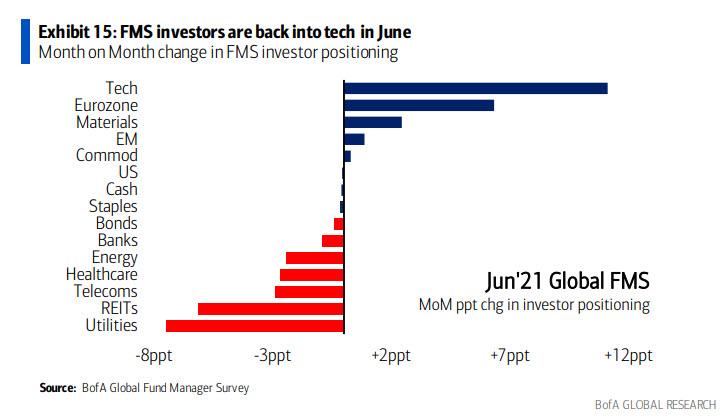

And while tech saw largest jump in exposure from 11% to 22% (after being massively shorted several weeks earlier), defensives exposure was cut again, with underweight in utilities largest since February 2017.

Tyler Durden Tue, 06/15/2021 - 12:20{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Buchanan: All Is Hype For The Biden-Putin Summit

Buchanan: All Is Hype For The Biden-Putin Summit

History repeats itself, first as tragedy, then as farce.

Karl Marx’s comment came to mind as President Joe Biden and Prime Minister Boris Johnson sought to equate their tete-a-tete at the G7 confab in Cornwall, England, to the Atlantic Charter conference of 80 years ago.

Those were historic days, to which these days cannot compare.

In August 1941, Prime Minister Winston Churchill and President Franklin D. Roosevelt met secretly on warships off Newfoundland to confer and commit to a set of principles that were to govern the world after the defeat of a then-triumphant Nazism.

Aboard HMS Prince of Wales, the battleship that brought Churchill across the Atlantic, Americans and British sang together, defiantly and movingly, an old and venerable hymn.

“Onward, Christian Soldiers!

Marching as to War,

With the Cross of Jesus,

Going on Before.”

Four months later, hours after the attack on Pearl Harbor, Prince of Wales would be sunk by Japanese fighter-bombers along with its sister ship, the battlecruiser Repulse, in the South China Sea.

When Churchill arrived in Placentia Bay off the Canadian coast, the Battle of Britain had been won, Adolf Hitler had turned on his former ally Joseph Stalin, and German armies were advancing from victory to victory in the USSR.

The danger then was that the Nazis might win the war.

And what did Biden, landing at Royal Air Force Base Mildenhall, identify for the U.S. troops there as the “existential threat” facing today’s world?

Said Biden: “When I first was elected vice president with President Obama, the military sat us down to let us know what the greatest threats facing America were — the greatest physical threats. … You know what the Joint Chiefs told us the greatest threat facing America was? Global warming.”

“This is not a joke,” Biden assured the troops.

Chairman of the Joint Chiefs Army Gen. Mark Milley told Congress the following day that, over at the Pentagon, they had a somewhat different ranking of threat assessments.

Said Milley: “Climate change does impact, but the president is looking at a much broader angle than I am … from a strictly military standpoint, I’m putting China, Russia up there.”

Kicking off the first day’s discussion of the seven leaders from the U.S., U.K., Canada, France, Germany, Italy and Japan, Johnson laid out his vision for the post-COVID-19 world.

Building on Biden’s theme to “build back better,” Johnson said that we should ensure that “we’re building back better together. And building back greener. And building back fairer. And building back more equal … perhaps in a more feminine way.”

Johnson knows his media audience.

In the 12,400-word closing communique, the G7 accused Russia of threatening Ukraine while China was guilty of human rights abuses in Xinjiang and Hong Kong. The anti-China commentary was said to have been inserted at the request of President Biden.

But no concrete action was agreed upon in the communique that would unduly upset either Chinese President Xi Jinping or Russian President Vladimir Putin.

Indeed, the Chinese embassy in London dismissed the whole G7 exercise, with Reuters quoting a spokesman as saying, “The days when global decisions were dictated by a small group of countries are long gone.”

That Chinese diplomat came as close to describing the reality at the Cornwall confab as anyone present.

For the G7 meeting — of the heads of government of seven of the world’s 10 largest economies — and the gatherings this week of NATO and the European Union in Brussels appear designed more to send messages than to portend action.

What are those messages?

“America is back!” The prodigal son has come home. The bad old days of The Donald are over. We are united again and agreed we must stand together and raise our differences behind closed doors, not raucously in open forums.

And the struggle for the future lies in competition, not conflict, between autocrats and democrats, to determine which system works better for its people.

To show solidarity, the G7 agreed to contribute 1 billion COVID-19 vaccine shots to poor and needy nations by the end of 2022. Half will come from the USA.

And what are the geopolitical realities largely left unaddressed?

Russia continues to hold Alexei Navalny in prison, to stand behind the dictator Alexi Lukashenko in Belarus and to support the pro-Russian rebel resistance in the Donbas.

China is not surrendering any of the reefs it claims in the South China Sea. Beijing continues to squeeze the political life out of Hong Kong, and its persecution persists in Xinjiang. And the Chinese military exercises in the Taiwanese waters and air space will continue and grow more aggressive.

Wednesday’s meeting between Biden and Putin is the event toward which these preliminary meetings — the G7, NATO and EU gatherings — have been pointing.

And from the signals Putin has been sending, he intends to disagree firmly and frankly with Biden, who has called him a “killer.”

{kind=link}

Following the Putin summit, Biden will hold his own separate press conference, by himself. What, one wonders, are the Americans afraid of?

Tyler Durden Tue, 06/15/2021 - 11:59

Categorías: Blogs y opiniones de economia en ingles

Hunter Biden Invested Millions In Chinese Nuclear Plant Operator That Vented Dangerous Buildup Of Gasses

Hunter Biden Invested Millions In Chinese Nuclear Plant Operator That Vented Dangerous Buildup Of Gasses

Hunter Biden's private equity firm invested millions of dollars in a Chinese state-owned nuclear power plant operator whose French partner warned the White House that the Taishan Nuclear Power Plant in Guangdong province was in danger of an "imminent radiological threat" due to a build-up of noble gasses in the cooling system of one of the facility's two reactors, according to the National Pulse.

{kind=link}

The incident has been downplayed by the Biden administration, which told CNN that the facility is not yet at a "crisis level," and does not pose a severe safety threat to workers at the plant or Chinese public. But is there more to it?

As the National Pulse's Natalie Winters reported on Monday:

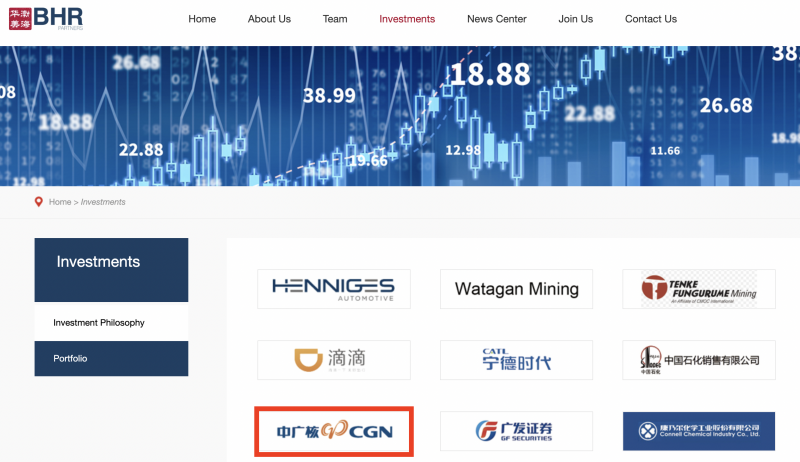

The Biden team’s lack of concern comes as the primary operator of the China-based plant – China General Nuclear Power Corporation (CGN) – counts millions in investment from Hunter Biden.

BHR Partners – the private equity firm where Hunter Biden served as a director since 2013 – was a $10 million cornerstone investor in CGN’s initial public offering. Occurring in 2014, the IPO was the second largest of the entire year, valued at over $3 billion.

The company, which Hunter Biden reportedly retains a sizable stake in, still lists GCN as part of its portfolio on its website.

BHR PORTFOLIO (via National Pulse){kind=link}

What's more, in 2017 a CGN consultant was sentenced to two years in prison by the DOJ for approaching and enlisting "U.S. based nuclear experts to provide integral assistance in developing and producing special nuclear material in China," and "did so without registering with the Department of Justice as an agent of a foreign nation or authorization from the U.S. Department of Energy."

"Theft of our nuclear technology by foreign adversaries is of paramount concern to the FBI. Along with our local, state and federal partners, we will aggressively investigate those who seek to steal our technology for the benefit of foreign governments," said FBI Special Agent Renae McDermott at the time.

As we noted on Monday, the US government is analyzing a reported leak at a China's Taishan Nuclear Power Plant, after a French company that co-owns and helps operate it warned of an "imminent radiological threat," according to CNN, citing US officials and documents reviewed by the outlet.

According to AFP, "EDF reported earlier a build-up of noble gases in one of the two reactors' primary circuits, which is part of the cooling system," adding "Noble gases are elements which have low chemical reactivity -- in this case it was xenon and krypton."

#UPDATE A Chinese nuclear company has deliberately released gas from a power plant into the atmosphere within authorised limits, as it seeks to fix an issue at the facility, its French partner EDF said Monday https://t.co/hFaZCnjXaO #Taishan pic.twitter.com/2H8wXvmzt3

— AFP News Agency (@AFP) June 14, 2021"The gas was released after the coating on some fuel rods had deteriorated, said the spokesman, who asked not to be named."

According to Bloomberg, the French firm has called for an "extraordinary board meeting with majority owner China General Nuclear Power Corp., to discuss the increased concentration of inert gases at the Unit 1 reactor in Guangdong."

Tyler Durden Tue, 06/15/2021 - 11:42

Categorías: Blogs y opiniones de economia en ingles

Georgia To Investigate After Fulton County Official Says Election Forms Are 'Missing'

Georgia To Investigate After Fulton County Official Says Election Forms Are 'Missing'

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

Georgia’s secretary of state said Monday that his office will probe Fulton County after an election official there said forms verifying the chain of custody for some mail-in ballots went missing.

“New revelations that Fulton County is unable to produce all ballot drop box transfer documents will be investigated thoroughly, as we have with other counties that failed to follow Georgia rules and regulations regarding drop boxes. This cannot continue,” Georgia Secretary of State Brad Raffensperger, a Republican, said in a statement.

An election worker processes absentee ballots at State Farm Arena in Atlanta, Ga., on Nov. 2, 2020. (Megan Varner/Getty Images){kind=link}

Raffensperger previously announced similar probes in Coffee, Grady, and Taylor counties. In doing so, he alleged that the state’s other 120 counties had properly completed absentee ballot transfer forms.

Earlier Monday, Mariska Bodison with the county’s Board of Registration and Elections told the Georgia Star News that “a few forms are missing” when asked for documentation on approximately 19,000 absentee ballots that were said to have been placed in drop boxes.

The forms that are not available at this time would detail the chain of custody for the ballots. They are required by law.

A Fulton County spokeswoman told The Epoch Times in an email that the county “followed procedures for the collection of absentee ballots from Fulton County drop boxes.”

“We maintain a large quantity of documents and researching our files from last year to produce the ballot transfer forms. We have been in communication with the Secretary of State’s office to update them of our progress on this matter,” she said.

Democrat Joe Biden won Georgia by under 12,000 votes. Biden typically received more mail-in ballots in each state, and Georgia was no exception. While former President Donald Trump received over 254,000 more Election Day votes than Biden, Biden received over 848,000 absentee ballots compared to Trump’s 450,522.

Election workers count Fulton County ballots at State Farm Arena in Atlanta, Ga., on Nov. 4, 2020. (Jessica McGowan/Getty Images){kind=link}

Trump has said the 2020 election was rife with fraud, particularly in the swing states like Georgia.

“Whether it be voting machines, underaged people, dead people, illegal aliens, ballot drops, ballot cheating, absentee ballots, post office delivery (or lack thereof!), lock boxes, people being paid to vote, or other things, the 2020 Presidential Election is, in my mind, the Crime of the Century,” he claimed in a June 12 statement.

A group of Georgia voters that alleged in a petition last year that they witnessed an “abnormal” increase in Biden’s vote count in Fulton County while performing election observation was slated to obtain images of the county’s absentee ballots late last month.

But the judge overseeing the case decided to delay the visit to the county’s ballot storage warehouse, where the images were to be taken by county workers while petitioners or their representatives watched, until he rules on motions to dismiss filed by the county’s Board of Registrations and Elections and two other county agencies.

Garland Favorito, head of the Voter GA election integrity group, and a petitioner, told The Epoch Times that the new admission of missing forms could be used in the ongoing case at some point, but he would have to discuss that matter with his attorney.

Favorito believes the missing forms “could explain why we saw counterfeit ballots.”

Those ballots “could have originated from these drop boxes that don’t have chain of custody forms,” he added. “So I think there is a connection there.”

Susan Voyles, a poll manager who worked on a recount in November 2020, has said she handled ballots she believes were fraudulent or fabricated. Her affidavit was cited in the Fulton County petition, as were affidavits from others who participated in the recount and said they saw ballots they believe were fake. Voyles was later terminated by the county.

Follow Zachary on Twitter: @zackstieber Follow Zachary on Parler: @zackstieber Tyler Durden Tue, 06/15/2021 - 11:30

Categorías: Blogs y opiniones de economia en ingles

Michael "Big Short" Burry: This Is The Greatest Bubble Of All Time In All Things "By Two Orders Of Magnitude"

Michael "Big Short" Burry: This Is The Greatest Bubble Of All Time In All Things "By Two Orders Of Magnitude"

Earlier this year, none other than Michael 'Big Short' Burry confirmed BofA's greatest fears, as he picked up on the theme of Weimar Germany and specifically its hyperinflation, as the blueprint for what comes next in a lengthy tweetstorm cribbing generously from Parsson's seminal work, warning that:

"The US government is inviting inflation with its MMT-tinged policies. Brisk Debt/GDP, M2 increases while retail sales, PMI stage V recovery. Trillions more stimulus & re-opening to boost demand as employee and supply chain costs skyrocket."

"The life of the inflation in its ripening stage was a paradox which had its own unmistakable characteristics. One was the great wealth, at least of those favored by the boom..Many great fortunes sprang up overnight...The cities, had an aimless and wanton youth"

"Prices in Germany were steady, and both business and the stock market were booming. The exchange rate of the mark against the dollar and other currencies actually rose for a time, and the mark was momentarily the strongest currency in the world" on inflation's eve.

"Side by side with the wealth were the pockets of poverty. Greater numbers of people remained on the outside of the easy money, looking in but not able to enter. The crime rate soared."

"Accounts of the time tell of a progressive demoralization which crept over the common people, compounded of their weariness with the breakneck pace, to no visible purpose, and their fears from watching their own precarious positions slip while others grew so conspicuously rich."

"Almost any kind of business could make money. Business failures and bankruptcies became few. The boom suspended the normal processes of natural selection by which the nonessential and ineffective otherwise would have been culled out."

"Speculation alone, while adding nothing to Germany's wealth, became one of its largest activities. The fever to join in turning a quick mark infected nearly all classes..Everyone from the elevator operator up was playing the market."

"The volumes of turnover in securities on the Berlin Bourse became so high that the financial industry could not keep up with the paperwork...and the Bourse was obliged to close several days a week to work off the backlog" #robinhooddown

"all the marks that existed in the world in the summer of 1922 were not worth enough, by November of 1923, to buy a single newspaper or a tram ticket. That was the spectacular part of the collapse, but most of the real loss in money wealth had been suffered much earlier."

"Throughout these years the structure was quietly building itself up for the blow. Germany's #inflationcycle ran not for a year but for nine years, representing eight years of gestation and only one year of #collapse."

His punchline: the above was "written in 1974 re: 1914-1923" and then makes the ominous extrapolation that "2010-2021: Gestation" adding that "when dollars might as well be falling from the sky...management teams get creative and ultimately take more risk.. paying out debt-financed dividends to investors or investing in risky growth opportunities has beaten a frugal mentality hands down."

{kind=link}

And, as if reading from the same playbook, Paul Tudor Jones warned yesterday that things are "bat shit crazy" and if Jay Powell

“The idea that inflation is transitory, to me ... that one just doesn’t work the way I see the world."

All of which led to Burry's latest tweet warning this morning...

"People always ask me what is going on in the markets. It is simple. Greatest Speculative Bubble of All Time in All Things. By two orders of magnitude. #FlyingPigs360"

People always ask me what is going on in the markets. It is simple. Greatest Speculative Bubble of All Time in All Things. By two orders of magnitude. #FlyingPigs360

— Cassandra (@michaeljburry) June 15, 2021In other words: "Brace!"

So what are you going to do about it?

Tudor Jones had some simple advice: "buy commodities, buy crypto, buy gold."

Tyler Durden Tue, 06/15/2021 - 11:10

Categorías: Blogs y opiniones de economia en ingles

Que agradecido es el cuero.

Buén finde amigos, he aceptado la sugerencia de @Txerra_2 de realizar una funda para mi Weidmannsheil.

Como ultimamente he notado cierto interés por parte de vosotros por las labores "cueriles", he pensado en entreteneros con un "paso a paso". Así que cargué la batería de mi vieja Sanyo y "p'alante".

Hice un molde para conseguir unas "orejas" bién planchadas.

Recorte las formas basicas.

Marqué costuras y perforé.

Rebajé el asiento de los herrajes para que queden embutidos.

Tintado de base marrón claro.

Sombreado marrón oscuro con aerógrafo.

Un ligero toque de pátina antigua y pre-sellado.

Remachado de clip.

Un protector interno (aunque esté el remache embutido)

Para el pegado es conveniente alinear con agujas (que desastre si se te tuerce).

Cosido y listo para lijar cantos.

Tintado de cantos y bruñir.

Encerado generoso aplicando calor para licuar la cera y facilitar su penetración.

Esta funda solo se ajusta a esta navaja especificamente por sus poco habituales proporciones.

El resultado en la siguiente tanda de imágenes.

Esta hebilla la realicé en aluminio.

2009... como pasa el tiempo.

Espero que os haya gustado el post, animaros a meter mano al cuero, es bastante grato.

Un gran saludo a toda la peña.

PACO.

Categorías: Metalurgia, forja y fundicion

Macleod: The End Of The LBMA Is Nigh

Macleod: The End Of The LBMA Is Nigh

Authored by Alasdair Macleod via GoldMoney.com,

Basel 3 is on course to regulate the LBMA out of existence. And with it will go all the associated arbitrage business and position-taking on Comex, because most bullion bank trading desks will cease to exist. The only supply to buy-side speculators of gold and silver contracts will be producer hedging.

In recent months there has been some limited commentary concerning the introduction of Basel 3 regulations and the implications for precious metals trading. These new regulations are scheduled to be introduced for European banks at the end of June — only seven weeks’ time — and in the UK from 1 January next, affecting all LBMA member banks.

This article explains the new regulations and concludes that the recent joint LBMA/WGC consultation paper addressed to the British regulator is unlikely to save London’s unallocated gold trading market. And because Basel 3 regulations are scheduled to be introduced into the UK at the year-end all banks in the London gold market can be expected to wind down their exposure well ahead of the deadline.

The unallocated forward settlement market will effectively be shut down.

Hedging into Comex futures from this source will also cease.

As it is unwound, the withdrawal of synthetic supply has enormous implications for future precious metals prices by transferring pricing power to physical markets, now dominated by China.

{kind=link}

Abbreviations in this article

-

PRA Prudential Regulation Authority, the UK financial sector and banking regulator.

-

EBA European Banking Authority, the EU banking regulator.

-

LBMA London Bullion Market Association, the trade body for forward dealings in unregulated, unallocated precious metals in London.

-

WGC The World Gold Council, a trade body based in London which researches and quantifies global gold supply and demand.

-

CME Chicago Metal Exchange, the US-based regulated futures market used by bullion banks around the world.

-

BIS Bank for International Settlements, a sub-committee of which devises the Basel series of rule-based banking regulations. In the wake of the financial crisis of 2007—2009, Basel 3 is being implemented to ensure that banks are adequately capitalised globally to undertake their various lines of business without imparting systemic risk to other banks.

-

RSF Required stable funding, introduced by Basel 3 and is applied to banking assets.

-

ASF Available stable funding, introduced by Basel 3 and is applied to banking liabilities.

-

NSFR Net stable funding ratio, the ratio between ASF and RSF, introduced by Basel 3 and never to fall below 100%.

On 4 May, the London Bullion Market Association in conjunction with the World Gold Council submitted a paper to the Prudential Regulation Authority making the case for unallocated gold to be spared a required stable funding factor (RSF) of 85% under new Basel 3 regulations. The new regulations are due to be implemented in Europe by the European Banking Authority at the end of June, to be followed in the UK on 1 January 2022. The paper claims that if the proposed RSF of 85% is imposed on gold and other precious metals it would undermine clearing and settlement, drain liquidity, dramatically increase financing costs and curtail central bank operations.

These are very serious statements to the effect that unless the London bullion market gets a waiver on the net stable funding ratio calculation (NSFR), it may as well shut up shop. And with the LBMA severely curtailed, the CME’s gold and silver futures contracts would lose out badly on both volumes and liquidity as well, with the number of active bullion bank trading desks (the Swaps) reduced to very few at the least.

At first sight it seems crazy that the impact of Basel 3 regulations will be permitted to radically undermine forwards and futures markets, which have been so instrumental to deflecting hoarding demand from physical bullion. It is through paper derivatives that the gold price in particular has been kept suppressed in conjunction with central bank leasing, and therefore prevented from challenging the US dollar’s credibility, following gold’s replacement as the world’s reserve currency fifty years ago.

The disruption to forwards and futures markets from Basel 3 will be a major shock, yet wider markets appear to be blithely ignoring the problem. When it goes ahead, Basel 3 will mean that banks will be forced to wind down their positions in unallocated precious metals, almost certainly causing massive disruption to physical bullion markets as well. If the expansion of paper markets has suppressed the prices of gold and silver for the last fifty years, then a severe contraction of paper equivalents at a time of escalating fiat money inflation could send prices to the moon.

In order to understand the proposed regulations, we need to look at them while taking into account the standard accounting practice of double entry bookkeeping as it is applied to bank balance sheets. There are three new Basel 3 definitions that matter in this regard:

-

The Available Stable Funding factor (ASF) is applied to the sources of a bank’s funding on the liability side of its balance sheet. Depending on the liability (shareholders’ equity, customer deposits, interbank loans etc.) they are multiplied by a factor, from 100% for the most stable forms of funding, such as Tier 1 bank equity, to 0% for the least stable. Being on their balance sheets, unallocated gold owed to a bank’s depositing customers is to be given a Basel III ASF of 0%, which means it will not be permitted to be a source of funding for any balance sheet assets, which must therefore be funded from other liabilities.

-

The Required stable funding (RSF) is to be applied to a bank’s assets. Unallocated gold positions are to be valued at 85% of their market value. Note that allocated gold, being held in custody, is not on bank balance sheets (except where the bank actually owns physical gold in its own right) and is therefore not involved in the calculation.

-

The Net stable funding requirement (NSFR) is the ASF divided by the RSF and must be at least 100% at all times.

The LBMA’s problem with Basel III becomes obvious. Unallocated gold liabilities cannot be used for funding the bank’s assets, and unallocated gold assets take a valuation haircut of 15% of market value as well. In future, the former cannot be simply offset against the latter, but bullion banks in London naturally run unallocated positions on both sides of their balance sheets. Whether the bank owns vaulted allocated gold to offset some of the price risk is immaterial. If this Basel 3 proposal goes through without modification, it will effectively be the end of the LBMA’s forward settlement business, and the end of arbitrage and hedging between LBMA members and the CME’s Comex futures contracts. And the Swaps on Comex, which are the bullion bank trading desks, could be regulated out of existence.

We cannot be sure yet that this will definitely happen, because it was put out for consultation in the UK by the PRA until 3 May. The end-June deadline after which Basel III applies in Europe might be extended again — which seems increasingly unlikely. In a patched-up compromise, unallocated gold could be rescheduled for a higher ASF and/or RSF, though again, that seems unlikely. Furthermore, the LBMA’s plea to the PRA, if successful, would only apply to UK regulated banks, not those in other jurisdictions, unless they set up full-blown London subsidiaries. And even that is unlikely to be acceptable to European and other regulators regulating their parents, because it is normal practice for regulators to look through such arrangements.

The LBMA paper suggests a compromise, that London could follow Switzerland which intends to rely on a clause in the European Banking Authority’s rule book allowing banks to make returns to the regulator instead, and for the regulator to decide stable funding matters. For this to work, the PRA would have to obtain agreement on a common approach with banking regulators in Europe and elsewhere. If that is to be the case, time is running out rapidly.

But the Swiss option only works on the basis that unallocated positions on both sides of the balance sheet are classified as interdependent. Any mismatch between unallocated gold liabilities and assets would not be covered. One assumes that hedging through Comex futures could resolve this issue partially, but that is only an assumption. And even if this get-out is adopted, liquidity will still dry up, because bullion bank trading desks will be given minimal trading discretion, limited to maintaining even books across the markets because of the NSFR issue.

The Swaps category on Comex (the bullion bank trading desks) is currently net short of about $24bn in the GC gold futures contract and $1.6bn in silver futures. Pressure to pare back ownership of these positions to a few genuine market makers and American bank trading desks is bound to increase, because the short positions held by European bullion banks would have to be covered in the next six weeks. And in London, all LBMA banking members will similarly reduce their unallocated activities because unbalanced books would be heavily penalised by the rule changes when they come in for the UK as well. That would make Comex gold and silver contracts entirely dependent on producer hedging.

The Bank of England will almost certainly express a view to the PRA as well as has the LBMA/WGC, not least because through swaps and leases for earmarked central bank gold in its custody it has been instrumental over the years in arranging for physical liquidity to be provided to the market in London. But it behoves the PRA to look more closely at the whole question of trading in unallocated gold, and specifically at the risks to the UK and European banking systems of a daily settlement average of 20 million ounces, or 620 unallocated equivalent tonnes between LBMA members. This does not appear to include additional unallocated tonnages between members and non-members, nor does it include intraday turnover.

The London shell gameIn the interests of understanding the London bullion market, it will be helpful to start with definitions of unallocated and allocated gold accounts. According to the LBMA’s own website,

Unallocated accounts

Most bullion in London is traded and settled on an unallocated account basis, where the customer does not own specific bars but has a general entitlement to an amount of metal. It is the most convenient, cheapest and most commonly used method of holding metal. It works very much like a bank currency account.

Note that instead of owning gold, the customer only has a general entitlement. Note also that it works like a normal bank currency account. And bear in mind that not only does a customer with an unallocated account not own gold but is just a creditor of the bank. All unallocated gold obligations appear on the bank’s balance sheet.

Allocated accounts

Allocated accounts are opened when a customer requires title or ownership of specific bars, with the dealer holding them on the client’s behalf. Clients’ holdings are identified in a weight list of bars, showing the unique bar number, gross weight, the assay or fineness of each bar and its fine weight. Credits or debits to the holding are linked to the physical movements of bars to or from the client’s physical holding. In this respect, it is like a safe deposit box with the account operator acting simply as custodian.

This is a completely different type of account, where the bank is a custodian, and holdings do not appear on the bank’s balance sheet. Allocated gold is not at the disposal of the bank and cannot be used for its trading. In practice, banks discourage customers from holding allocated gold through high charges for storage and account maintenance fees. By way of contrast, a customer who maintains an unallocated account is often freed from bank charges entirely. Consequently, the large majority of customer accounts are unallocated.

The LBMA/WGC letter leads its readers to assume the only difference between allocated and unallocated gold is the convenience unallocated gold provides for an efficient market. Nowhere is there any mention of the lack of physical gold backing unallocated accounts. And by ignoring the process of bank credit creation, it panders to the naïve assumption that banks are simply pass-through intermediaries with depositors on one side and loans on the other.

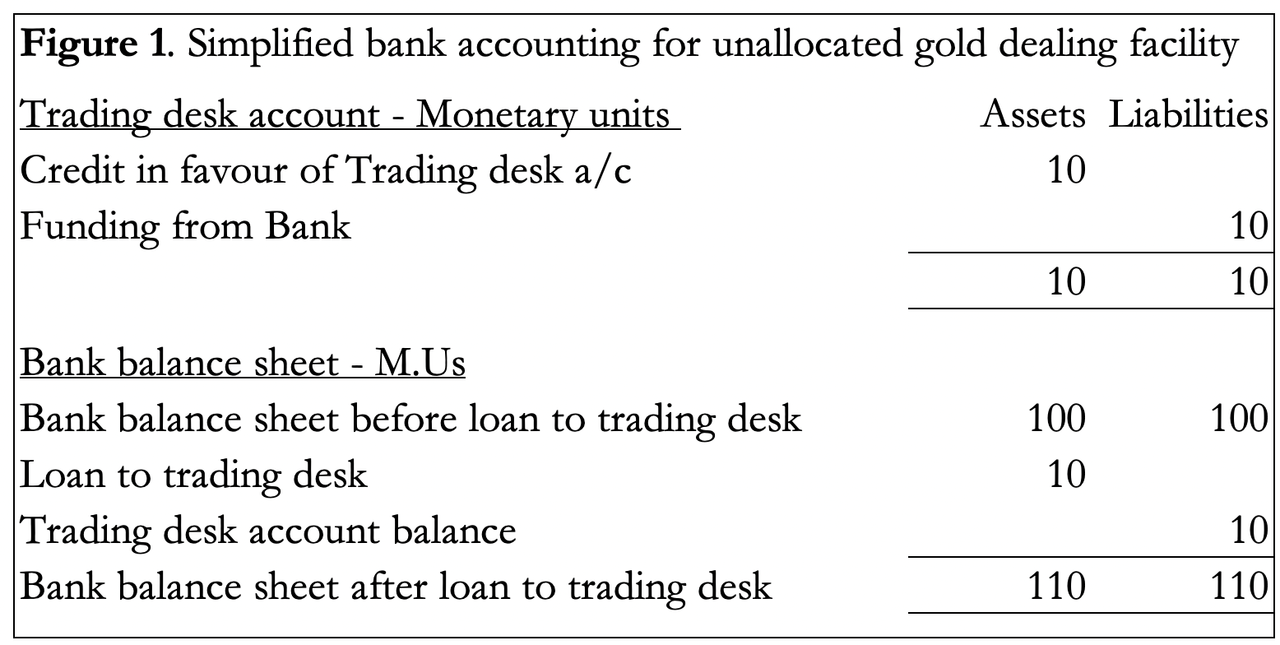

In common with banking regulators, the LBMA and WBC apparently fail to understand that unallocated accounts on bank balance sheets are only created by the process of bank credit expansion and have nothing to do with physical gold. The origin of all unallocated accounts is not the depositing of gold, but credit creation. Figure 1 shows how unallocated gold accounts are created in this way.

{kind=link}

Let us say the trading desk has a facility granted to it by the bank to trade unallocated gold, and its account is credited with this facility by its bank to the extent of 10 monetary units. On its books, the bank records an asset in Monetary Units (normally dollars, or sterling, euros etc. depending on the bank’s accounting currency), reflecting the loan created in favour of its trading desk. At the same time, the bank records an equal liability matching the credit to its trading desk to allow the latter to fund its dealing book. It can now deal with other banks in unallocated gold, all of which will have created the facility to deal in unallocated gold by the same process of credit expansion ever since facilities to trade in unallocated gold evolved into existence.

What’s happened is that the dealing desk’s facility has been funded by the expansion of bank credit out of thin air, in the same way that bank credit is expanded by any bank in any other line of banking business. This is standard accounting practice long established by banking law. From it, we derive two important points: the funding of unallocated positions in London is simply through the expansion of credit denominated not in gold, but currency; and with all banks using the same methods no gold is involved at all.

Customers of the bank can, of course, request physical delivery, or delivery into an allocated account at the bank, in which case the trading desk acts as a broker, sourcing physical metal. But this function must not be confused with unallocated dealing by banks acting as principals, or on behalf of their customers with unallocated accounts.

The LBMA/WGC submission claims that gold is vital collateral for central counterparties, which rely on the LBMA system to manage both it “and the physical delivery of precious metals derivative contracts” (page 3). The wording is misleading, because the delivery of a derivate contract is not the same as delivering the precious metal. The only other reference to collateral is in Annex 1, where the WGC trots out the usual stuff about gold having no counterparty risk and is widely accepted as collateral. That is true of physical gold, but is not relevant to unallocated gold, where counterparty risk is the only consideration and is the exclusive business between LBMA member banks.

Unallocated gold is no more than book entries tied to the price of gold, and its origin and continued existence is entirely funded by the creation of bank credit. It is this that Basel 3 recognises.

By introducing the net stable funding ratio, Basle III effectively makes standard banking practice unworkable in the case of unallocated precious metals by not permitting a trading book to net off its long and short positions. The regulators at the Basel Committee will not have jumped down on unallocated gold trading unless, in their opinion, they viewed it as a risk to the global banking system which must be offset by proper funding. Plainly, they understand the unallocated shell game for what it is, and that a failure in this market would be a threat to the entire banking system. Almost certainly, Basel III’s banking experts will have examined the risks in considerable detail before making their decision about the rates of both the ASF and RSF to be applied. And when it comes to cooperation from the European Banking Authority, there is also the additional risk that the UK’s PRA could find itself mired in post-Brexit non-cooperation.

The impact on physical precious metalsAsked to estimate the chances that the LBMA will succeed in stopping the imposition of the NSFR in Europe in six weeks’ time, the answer is it will be as likely as a cat in hell’s chance. While the Swiss proposal would provide some easement, it would effectively shut down their trading desks because of the penalties on uneven books. European and Swiss bank memberships of the LBMA are ten out of a total of forty-three, and most of those are UK incorporated subsidiaries. But it is unlikely that the EBA will accept that by sheltering the banking risks in a wholly owned UK subsidiary they can be simply ignored.