Se encuentra usted aquí

Agregador de canales de noticias

El Ibex 35 repunta un 1,46% y consolida los 8.700 enteros pero no salva la semana

Noticias bolsa España -

Apoyado en las compañías acereras y en el sector bancario, el Ibex 35 cierra con alzas del 1,46% hasta los 8.776,6 puntos, en línea con el resto de índices europeos, entre los que destaca el Cac francés. Pese al rebote, el selectivo pierde un 1,47% semanal.

Categorías: Blogs y opiniones de economia en español

The 50 Best Growth Stocks to Buy as the Inflation Trade Dies

I cannot emphasize this enough: The growth stock breakout has arrived

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Warren Buffett Series in PDF

Get the entire 10-part series on Warren Buffett in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

Short and fast, it was good while it lasted. That’s what the tombstone for the so-called “inflation trade” should read because, folks, it is dead. Once again, it’s time to look at strong growth stocks to buy, before they ride a wave of bullish macro sentiment higher.

You heard that right. The great “value rotation” that mainstream media and even some money managers have been pumping for months now thanks to what many saw as roaring inflation, is completely and utterly dead – shot by the cold reality that today’s vigorous economic recovery will not last.

You see… everyone’s been saying that this great, big economic reopening was going to spark runaway economic growth and huge inflation, the likes of which would spark a rise in Treasury yields, a huge run-up in cyclical stocks, and a big crash in growth stocks.

That is, everyone was saying that, except for me!

I’ve been saying this whole time that this great, big economic reopening is unsustainable. I’ve said it will taper off, economic activity will slow, inflation will subside, yields will fall, cyclical stocks will crash, and growth stocks will rebound.

Guess who has been right?

Not to brag, but yes, I’ve been proven right by the numbers.

The Case for Growth StocksThe U.S. Markit Services PMI for June came in yesterday, and it was not great. The reading came in at 64.6, below expectations for a 65.2 reading and lower than last month’s 64.8 reading.

Also yesterday, the U.S. ISM Services Index for June clocked in at 60.1, below expectations for a 63.3 reading and sharply lower than the May reading of 64.0.

This data is not isolated – it follows a multi-month trend of consecutive economic data misses and slowing economic activity.

The Citigroup Economic Surprise Index – a measure of how well economic data is coming in relative to expectations – has collapsed over the past few months, while the New York Fed’s Weekly Economic Index – a high-frequency indicator of economic activity – peaked in late April at 12.01%, and has since retreated basically every week since then. That’s basically nine consecutive weeks of economic activity compression.

All the while, the 10-year Treasury yield has collapsed. That yield was testing 1.8% not too long ago. Lots of folks were saying it was going to make a run toward 2%. Now, it’s languishing around 1.35%.

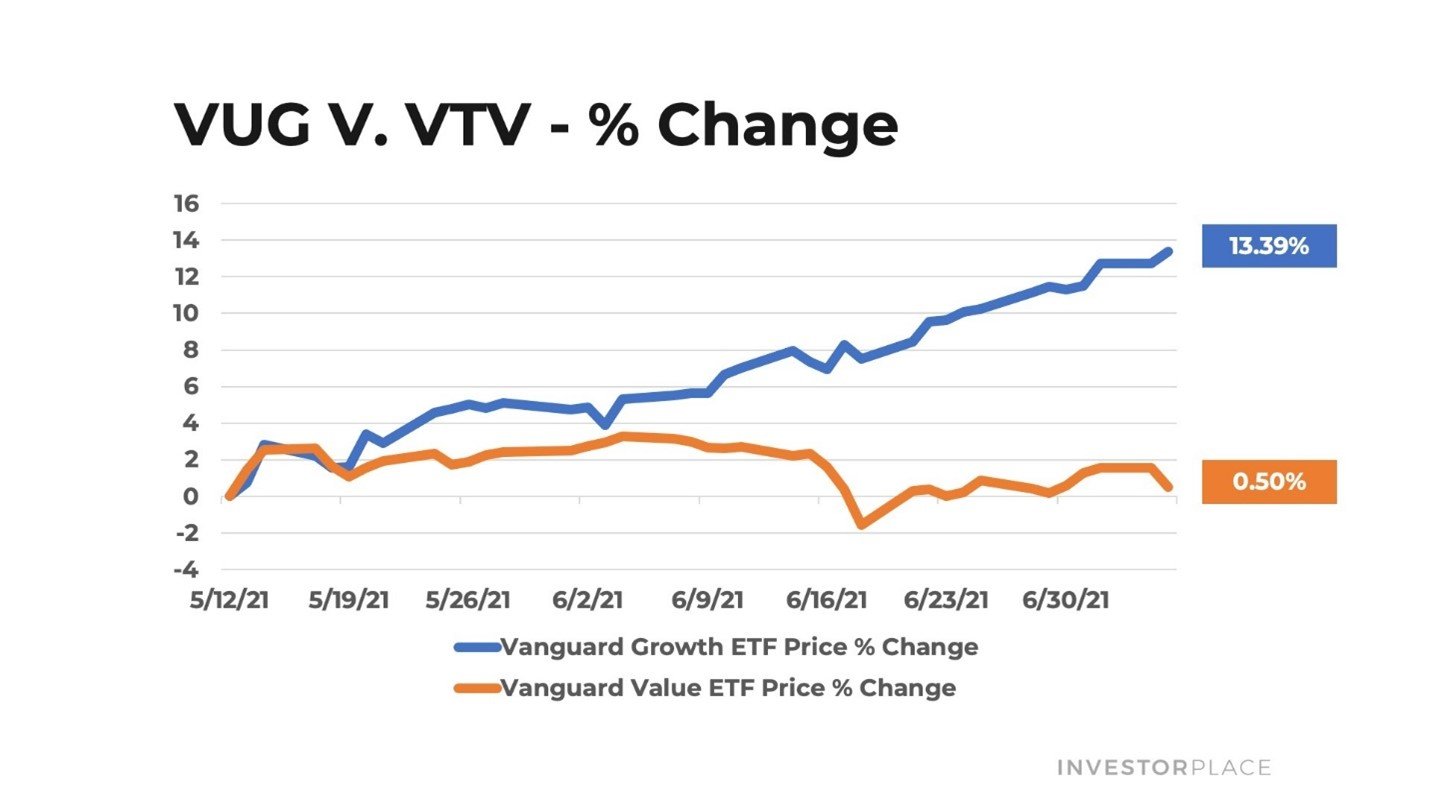

And, amid this slowdown in economic activity and crash in yields, growth stocks have surged higher. Since mid-May, the Vanguard Growth ETF (NYSEARCA:VUG) is up more than 13%, versus a mere 0.5% gain for the Vanguard Value ETF (NYSEARCA:VTV).

{kind=link}

The verdict is in, folks. The stock market has spoken. The bond market has spoken. The economic data has spoken. And they’re all saying the same thing: The U.S. economic recovery is quickly losing steam, inflation is subsiding, and growth stocks are ready to roar.

This trend is here to stay.

That is, over the next 6 months, the U.S. economy is going to keep slowing, yields are going to keep falling, and growth stocks are going to keep rallying.

How China Is Leading the MarketWhat makes me say that?

One word: China.

China was the first country to lock down because of the Covid-19 pandemic. It was also the first country to fully reopen. To that extent, it can be seen as somewhat of a “leading indicator” for how this unusual global economic reopening will play out in other countries.

Well, over in China, things are slowing quite dramatically. The Caixin China General Services Business Activity Index fell to 50.3 in June, from 55.1 the previous month and the lowest reading in 14 months. Of note: A number above 50 indicates economic expansion, so China’s services sector barely grew in June.

If we take China as a leading indicator for how the rest of the global economic reopening will play out – which, so far, it’s been a good leading indicator – then we can conclude that, indeed, economic activity throughout the world will continue to slow in the coming months. That will lead to a continued downtrend in bond yields, and a continued uptrend in growth stocks.

Folks… I cannot emphasize this enough… the growth stock breakout has arrived.

We had this weird bump in the road in early 2021 amid a once-in-a-lifetime, never-going-to-happen-again economic reopening that caused a multi-decade trend of growth stocks crushing the market to reverse course – and now, that unusual period is over. The reopening has come and gone. Things are getting back to normal on Main Street. And they’re getting back to normal on Wall Street, too, which means growth stocks crushing all other stocks.

That’s why I’m 100% genuine in saying there has never, ever been a better time to subscribe to my exclusive (and free) e-letter, Hypergrowth Investing.

In Hypergrowth Investing, we discuss many of the megatrends and leading stocks within our premium newsletters, which we feel represent the most exciting technology companies on the planet.

A lot of those stocks have been beaten and bruised over the past few months. Yet their businesses remain as strong as ever and their long-term growth outlooks remain as favorable as ever. Now, they’re rebounding. All of our “New Buys” are up more than 20% over the past month alone.

Still, from current levels, we think many of our stocks have enormous 10X-plus upside potential.

This is a once-in-a-lifetime opportunity. And it costs you absolutely nothing to join.

In fact, I’ll give you my latest research report, 11 Electric Vehicle Stocks for 2021, just for signing up.

Don’t let this opportunity pass you up. Capitalize on it by clicking here.

On the date of publication, Luke Lango did not have (either directly or indirectly) any positions in the securities mentioned in this article.

About the Author

By uncovering early investments in hypergrowth industries, Luke Lango puts you on the ground-floor of world-changing megatrends.

Article By Luke Lango, InvestorPlace

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});The post The 50 Best Growth Stocks to Buy as the Inflation Trade Dies appeared first on ValueWalk.

Categorías: Blogs y opiniones de economia en ingles

What is Robinhood?

Welcome to another issue of Net Interest, where I distill 25 years of experience investing in the financial sector into a weekly email. If you’re reading this but haven’t yet signed up, join over 20,000 others and get Net Interest delivered to your inbox each Friday by subscribing here:

What is Robinhood?Last June, I wrote a piece in Net Interest called The Stock Market as Entertainment. It explored the explosion in retail trading activity happening at the time and suggested that one cause for renewed interest in the stock market was the cancellation of sport:

… a pivot from sports is a compelling explanation. The demographic of Robinhood’s customer base is similar to that of a sports bettor. Men aged 25-34 are the segment most likely to bet on sports on a regular basis. According to Deloitte 43% of North American men aged 25-34 who watch sports also bet on sports at least once per week, and that’s the same group that has flocked to Robinhood. The median age of a Robinhood customer has drifted up from 27 in 2017 to 31 now, and 80% of them are men.1

Indeed, Robinhood’s interface makes the transition between sports betting and trading seamless. The app has been compared to a mobile game (“Charles Schwab, meet Candy Crush,” according to an NBC News report) which users check ten times a day or more.

Robinhood customers also appear to be attracted to stocks for the same reasons they are attracted to sports events. In its S-1 prospectus DraftKings, a sports betting company, says that it delivers “betting experiences designed for the ‘skin-in-the-game’ sports fan – the fan who seeks a deeper connection to the sporting events that he or she already loves.” A look inside Robinhood portfolios reveals the sorts of companies that customers no doubt have deep connections to.2

One year on, it is clear that this explanation doesn’t suffice. Sport came back, but retail trading continued with enhanced vigour. Indeed, activity accelerated earlier this year, as Robinhood data attests.

a.image2.image-link.image2-338-594 { padding-bottom: 56.9023569023569%; padding-bottom: min(56.9023569023569%, 338px); width: 100%; height: 0; } a.image2.image-link.image2-338-594 img { max-width: 594px; max-height: 338px; } Source: Robinhood S-1An alternative explanation is one promoted by Balaji Srinivasan: “Everyone is an investor now.” He argues that everyone being an investor is the natural endgame of the financialization of the economy, just as the shift from farming to manufacturing was the endgame of its industrialisation. “If in the 20th century, the 99% are labor and the 1% are capital, the flip happens this century where the 99% are capital and the 1% are labor.”

balajis.com @balajisFarming was the 1800s. Manufacturing was the 1900s. Counterintuitively, could investing become the most common "job" of the 2000s? Reason: crypto and fintech are turning everyone into an investor, just like the internet turned everyone into publishers. How far does that go?September 22nd 2020

388 Retweets1,769 LikesThe idea is reflected in large white-on-green font towards the front of Robinhood’s S-1: “We are all investors.” Data from the Federal Reserve Survey of Consumer Finances shows US household direct ownership of stocks rising from the trough of 2013 and Robinhood reckons that will continue: “We believe democratizing finance for all is a one-way door, and these forces of change are more likely to accelerate than reverse.”

A Tavern on the GreenIf there’s a synthesis between the two explanations, it lies in the conflation of gambling and investing. The two activities fall on the same spectrum and converge in the fuzzy area of financial speculation that sits between them. A few years ago, a group of researchers published a paper in the Journal of Behavioral Addictions looking at the relationship between gambling, investing, and speculation. Here’s how they frame the similarities and differences:

a.image2.image-link.image2-578-1456 { padding-bottom: 39.6978021978022%; padding-bottom: min(39.6978021978022%, 578px); width: 100%; height: 0; } a.image2.image-link.image2-578-1456 img { max-width: 1456px; max-height: 578px; } Conceptual similarities and differences between gambling, speculation and investment.Ask any bystander of the industry what the fundamental difference between gambling and investing is and the response might be the role of skill versus luck in the outcome. But that wouldn’t be right. Many gamblers (for example Matthew Benham or Tony Bloom) show profound skill, and the role of luck in investing is well known. Rather, the key difference is that investing typically involves the creation or purchase of an asset with the expectation of long-term capital appreciation, which does not occur with gambling. In addition, in investing, the asset is never explicitly staked, whereas this always occurs with gambling – the best definition of gambling is staking money on an event having an uncertain outcome in the hope of winning additional money.3

Speculation captures the crossover of the two activities. Like investing, it takes place in a financial markets environment but it tends to be shorter term, higher risk and focused on generating gains from price movement with less regard for the fundamental value assets.

There’s a class of financial instruments that lend themselves very well to speculation and they are financial options. Their fixed expiration dates make them more short term than owning their underlying assets, the leverage they carry heightens their risk and the premium you pay upfront is equivalent to a gambling stake.

Which brings us back to Robinhood.

While Robinhood employs the investor narrative in its marketing efforts and claims “evidence that most of our customers are primarily buy-and-hold investors,” it makes the largest slice of its revenue from options. In 1Q21, it made $198 million of revenue from options, compared with $133 million from straight equities. Perhaps its options customers are subsidising its equity customers, allowing them to buy-and-hold at cheaper rates than otherwise would be the case. But given how much money Robinhood makes from options, its incentives are less around promoting stock ownership and more around promoting options trading. In 1Q21, it made $2.9 revenue per options trade, which compares with $0.4 on an equities trade (and $1.0 on a crypto transaction). Customers had only 2% of their funds invested in options, yet options contributed 14% to total trades and 47% to transaction revenues.4

a.image2.image-link.image2-388-596 { padding-bottom: 65.1006711409396%; padding-bottom: min(65.1006711409396%, 388px); width: 100%; height: 0; } a.image2.image-link.image2-388-596 img { max-width: 596px; max-height: 388px; } Source: Robinhood S-1This set-up brings Robinhood closer to the contracts-for-difference (CFD) model popular in Europe. We discussed the model here in Net Interest back in March when we compared ETrade to eToro, just after eToro announced its intention to go public. CFDs are derivative instruments that allow traders to bet on the direction of an asset, either up or down. Unlike stocks, they don’t grant economic rights to the underlying asset. In some markets they bear tax advantages (for example in the UK, traders don’t have to pay stamp duty which they would be liable for on a stock purchase). As derivative instruments, they also embed leverage.

CFDs are a lot closer to gambling than to investing (hence the different tax treatment). Customers can lose all their money. eToro’s general risk disclosure states: “CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 67% of retail investor accounts lose money when trading CFDs with this provider.” At Plus500, a competitor, the number is 72% – regulators insist on the disclosure.

So CFD platforms are in a constant hustle to acquire new customers to replace the churn. In 1Q21, Plus500 lost 16.2% of its customers over the quarter. They make up for it with high ARPU (average revenue per customer). In Plus500’s case, revenue was $838 per customer in the first quarter ($3,351 annualised).5

What about Robinhood?

Riding Through The GlenCompared with Plus500, Robinhood’s churn rate is a lot lower. It is a more diversified business, and although it makes the biggest slice of its revenues from options, we don’t know what proportion of customers trade them. In 1Q21, it lost 4.8% of its customers, which is not as high as the CFD platforms but it is higher than Charles Schwab, where churn was 3.0% in the same period. Its ARPU is also a lot lower than Plus500’s, at $34 in the quarter ($137 annualised).

In really simple terms, those churn and ARPU numbers mean that Robinhood can expect to extract around $714 of revenue per customer over their lifetime, which compares with Plus500 at $5,200. Fortunately for Robinhood, its customer acquisition costs are commensurately low, at $15 in 1Q21, and all the free publicity Robinhood got in the first quarter actually pushed them down (from $20 in 2020).6

The analysis really is very simple though, because it assumes customers who stick around generate the same revenue contribution year-in, year-out. Robinhood expects that revenues from those customers may actually increase, and presents some impressive looking cohort charts to prove it. It’s true that as their assets appreciate, these customers will trade in bigger size, leading to higher revenues for Robinhood. The company estimates that as of the end of March 2021, its customers had seen appreciation of their assets of approximately $25 billion. Assuming this doesn’t include churned customers and only those currently active, it implies a 45% return on $56 billion of invested funds (given customers are currently sitting on $81 billion worth of assets).

a.image2.image-link.image2-340-599 { padding-bottom: 56.761268781302164%; padding-bottom: min(56.761268781302164%, 340px); width: 100%; height: 0; } a.image2.image-link.image2-340-599 img { max-width: 599px; max-height: 340px; } Source: Robinhood S-1The problem with this approach is that markets don’t always go up. As Robinhood’s UK risk warning declares, “Past performance is not a useful guide to future returns, which are not guaranteed. Your investments may go down in value.” And more importantly for Robinhood, transaction turnover may not always go up whatever markets do. In fact, Robinhood is IPOing off an extremely high turnover base. In 1Q21, its customers did an average of 30 trades each or 122 on an annualised basis, up from 84 last year and 54 the year before. That’s not as many as eToro, but it’s roughly twice the rate at Schwab.

Sustaining that level of turnover will be quite a feat, which is why cohort economics make more sense for a steady subscription based business than they do for a cyclical transaction based one.

a.image2.image-link.image2-639-1247 { padding-bottom: 51.242983159583%; padding-bottom: min(51.242983159583%, 639px); width: 100%; height: 0; } a.image2.image-link.image2-639-1247 img { max-width: 1247px; max-height: 639px; } Source: Robinhood S-1 and company reportsTo frame just how unusual this current period is, take a look at the chart below which shows the average number of trades per quarter executed by customers of Charles Schwab going back twenty years.

a.image2.image-link.image2-388-596 { padding-bottom: 65.1006711409396%; padding-bottom: min(65.1006711409396%, 388px); width: 100%; height: 0; } a.image2.image-link.image2-388-596 img { max-width: 596px; max-height: 388px; } Source: company reportsAnd with Schwab data, we can even zoom right in to the present day by looking at weekly trends. Brokerage activity peaked around the time of the Gamestop episode at the end of January and has been on the decline since.

a.image2.image-link.image2-388-596 { padding-bottom: 65.1006711409396%; padding-bottom: min(65.1006711409396%, 388px); width: 100%; height: 0; } a.image2.image-link.image2-388-596 img { max-width: 596px; max-height: 388px; } Source: company reportsFinally, it’s worth looking back twenty years to see what happened after the last frenzy in retail trading activity in 2000. The chart below shows ETrade’s average daily trading volumes during the period (this one is not shown per customer, it’s across the entire ETrade customer base). After the peak in 1Q00, activity rates halved over the next eight quarters. It took a while to realise it, of course. On a conference call in March 2001, Charles Schwab, the man, talking about the performance of Charles Schwab, the company, admitted, “We’ve come through a highly speculative technology bubble. Maybe I should have been more emphatic about understanding that this was a temporary phenomenon.”

a.image2.image-link.image2-388-596 { padding-bottom: 65.1006711409396%; padding-bottom: min(65.1006711409396%, 388px); width: 100%; height: 0; } a.image2.image-link.image2-388-596 img { max-width: 596px; max-height: 388px; }Perhaps we are all investors now – or speculators at any rate, doing 120 trades a year and checking our app ten days a day – but let’s not forget, “it’s a bull market, you know.” Robinhood customers are sitting on $25 billion of gains ($1,400 per account) and that ‘house money’ may sustain activity for some time. But when it’s gone, trading may lose its allure and Robinhood’s growth will have peaked.

Thanks to @FIGfluencer for great insights with this.

More Net InterestBuy Now Pay LaterThe Buy Now Pay Later (BNPL) market is getting increasingly competitive. As well as the pure play participants like Affirm, Klarna and Afterpay, there’s competition from PayPal (Pay in 4, which doesn’t charge merchants incremental fees) and legacy banks. Competition is particularly intense in lower ticket categories, where the credit decisioning process is simpler.

One response is to consolidate. The Australian Financial Review this week reported that Klarna (featured in Net Interest here) could be building up a stake in Australian company Zip Co which operates QuadPay, another player in the BNPL market. Given how much capital it has raised recently ($640 million at a $45 billion valuation) it makes some sense and explains why Klarna may have raised private capital so soon after a prior round, rather than going public. When it eventually does come to the market, it will be challenging enough to address regulatory risks; if it can show more stable competitive dynamics, it will be a much more compelling story.

M&AThe quarter that ended last week turned out to be the strongest quarter for announced M&A ever. Deal volume of $1.56 trillion was announced, with $400 billion of that coming in June alone, pushing the quarter’s volumes 5% above the prior record. From a sectoral perspective, the strength was broad based, although technology, energy and healthcare saw particularly high volumes. A lot of the strength was domestic US rather than cross-border, and was centred among large cap companies rather than small or mid-sized ones.

There’s a trend across many industries for the big to get bigger and M&A feeds that. There are many implications of that but for M&A advisory firms it’s a very profitable backdrop.

WeatherWe’ve covered some quite bizarre academic finance papers in More Net Interest over the months, all of them answering questions you never thought you had. For example, how earnings estimates can be influenced if analysts share the same first name as the CEO of a company they cover (spoiler: they’re more accurate, but don’t ask me about Salesforce.com). And how the accuracy of estimates correlates with how physically attractive the analyst is (spoiler: any benefit of an analyst being attractive diminished after Reg FD).

A recent paper looks at the impact of weather. It examines how pre-announcement weather conditions near a company’s major institutional investors affect stock market reactions to its earnings announcements. The conclusion: that unpleasant weather leads to more delayed market responses to subsequent earnings news. Investors in California should learn to take advantage.

1In its S-1, Robinhood provides an update of these demographics. The median age of customers is still 31, but “we continue to welcome an increasing proportion of women to our platform, having tripled the number of women on our platform at the end of 2020 as compared to 2019.” This would put the proportion of women in the customer base at around 23%.

2As of August 2020, Robinhood shut down the API that was used by Robintrack to collect data of stocks held in Robinhood portfolios.

3Another notable difference lies in the variability of returns. Commercial gambling has a precise and mathematically determined negative return, whereas the magnitude and direction of monthly or quarterly changes in financial markets are much more variable and uncertain.

4I’ve assumed 61 trading days in 1Q21 to calculate these numbers, which is right for options and equities, but crypto trades 24/7 in which case the revenue per transaction there is closer to $0.7.

5Plus500 disclosure puts ARPU at $753 for the quarter, but that is based on end of period accounts; I’ve used average accounts over the period.

6The calculation here is ARPU divided by churn. It gives the perpetual value of a fixed revenue stream assuming a given level of churn.

Categorías: Blogs y foros de trabajar madera en ingles

Repsol destinará 657 millones a la ampliación de su complejo industrial en Portugal

La compañía prevé crear 75 empleos directos y 300 indirectos cuando las instalaciones estén operativas en 2025. Leer

Categorías: 1 Noticias economicas en español

Super Idiocracy. Super Crash

In this society, asset hyper inflation is widely embraced, however if wages rise a tiny amount, it's the end of the world. It's what any terminal old age home in hardcore self-destruct mode would believe...

{kind=link}

The COVID pandemic achieved the full virtualization of the economy. Working from home and shopping from home achieved mainstream adoption. Cloud Tech stocks skyrocketed. We now have a virtual economy consisting of delivery couriers drop shipping made in China junk to yuppy doorsteps. Fully bypassing the real economy. However when Biden got elected and the vaccine was distributed, the entire script changed. Now we have the greatest recovery in history and all of the deflationary factors that were accelerated by the pandemic have been long forgotten. From greatest virtual economy to greatest real economy in one year.

Of all of the various pump and dump schemes from this era, cyclical reflation is by far the largest and most widely believed delusion. It's the post-pandemic super economy. This society is in mass denial over Japanification and the fact that there are now extreme levels of excess capital and excess capacity, both of which are deflationary. However, it's this excess capital that keeps propagating these lies and myths as it rotates from one global pump and dump scheme to the next in search of zero sum gains.

Fittingly, when the GOP governors all decided to rescind unemployment benefits, all of the inflation trades began imploding. Once again, these idiots are learning the hard way that asset inflation is ALWAYS transitory.

{kind=link}

Even at this late stage their primary concern is STILL inflation. Why? Because per the rules of Japanification an aging society has a strong preference for return on capital at the expense of return on labour:

"Inflation’s silver lining: your retirement funds will be worth nothing, but you will be paid more after being forced to go back to work"

According to these assholes rising wages are the greatest risk we face. Notice there is absolutely zero concern for asset hyper-inflation. Which happens to be by far the biggest risk that retirement funds now face. But you can't tell that to an Idiocracy, because they know everything. Although I notice that it's dawning on them, that they got screwed again by their trusted psychopaths.

{kind=link}

Today's pundits are telling the sheeple that this selloff is a buying opportunity. The question on the table is given the magnitude of recent inflation hysteria, how many more fools are left to buy?

{kind=link}

This week, the market imploded twice overnight but the dip got bought with both hands in the U.S. As usual, there is absolutely no concern for what is happening in the rest of the world.

{kind=link}

{kind=link}

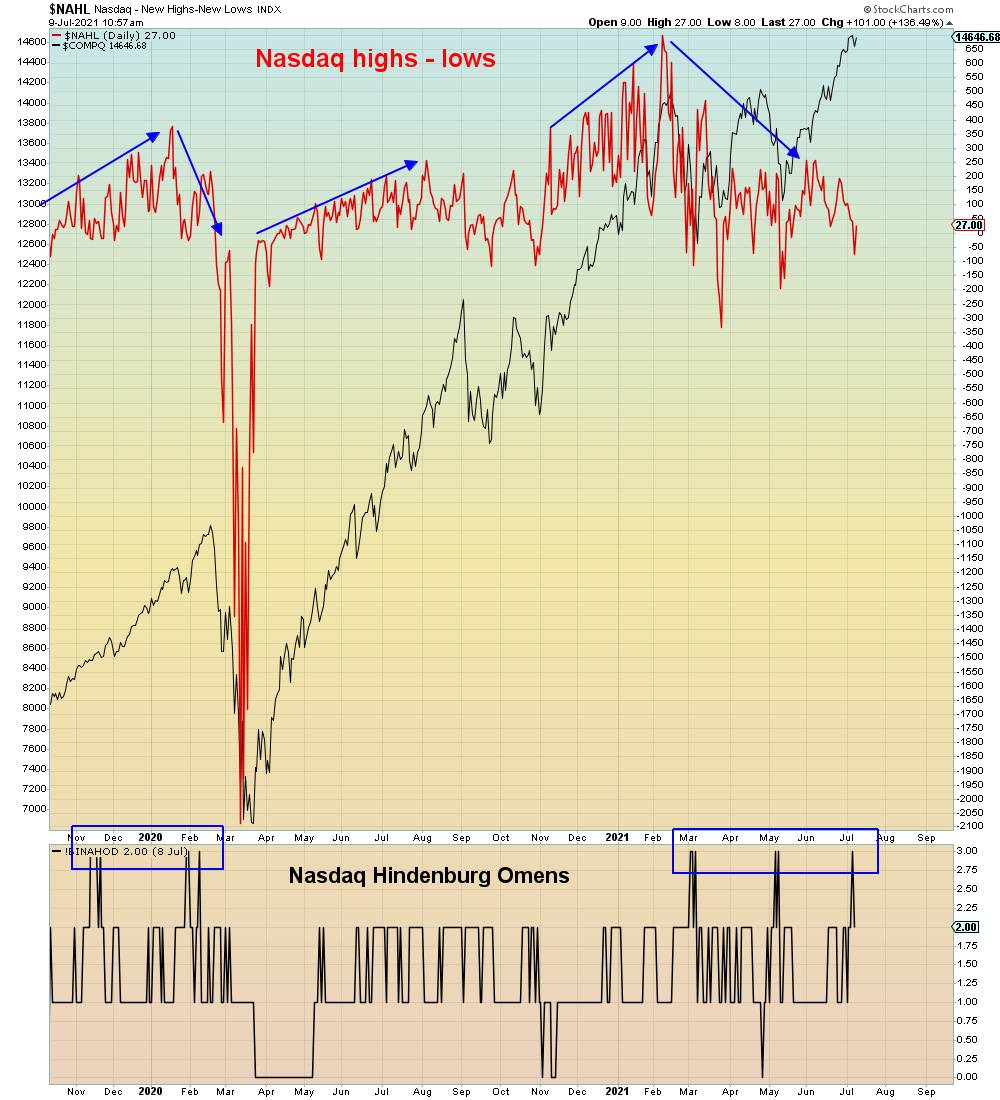

Amid all of this rampant denial, delusion, and mostly subscription based disinformation, it's also ironic that these dunces are now attempting to rotate BACK to the Tech bubble that imploded in February.

This week we got another Hindenburg Omen on the Nasdaq. Which indicates that the bifurcation in the overall market has now spread to the Nasdaq itself.

{kind=link}

In summary, every dunce you ever met is betting this will have a happy ending.

Position accordingly.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

El juez abre juicio oral contra el presidente de Urbas por ampliación de capital en 2015

La causa queda sobreseída provisionalmente contra la sociedad, Urbas Grupo Financiero, Grant Thorton y otros ocho más. Leer

Categorías: 1 Noticias economicas en español

Disney's French Revolution, and What It Might Mean for a Theme Park Near You

A new plan for “premier access” in Disneyland Paris will allow guests who pay extra to skip ride lines, and some see a potential preview of policy in the U.S.

Categorías: 3 Noticias economicas ingles

I’m a Twitter addict and I don’t care

The social networking site is a place to make pithy jokes, improve writing skills and connect with people

Categorías: 3 Noticias economicas ingles

En casa o en la oficina, la incógnita de cómo y dónde trabajar en la 'normalidad'

El próximo septiembre se cumplirá un año de lo que en 2020 se auguraba como la vuelta a una 'normalidad' laboral que aún es una incógnita. El modelo híbrido no acaba de cuajar en muchas empresas que viven aletargadas, confiando en la vacunación y en el regreso a un escenario preCovid. Leer

Categorías: 1 Noticias economicas en español

Ketonico recauda 1,1 millones de euros para dar a conocer los beneficios de la alimentación 'keto'

En la operación de esta 'start up', creada por Vicenç Martí, Nico Andonakis y Víctor Sala, han participado los 'family offices' Synarchy Ventures y 183 Invest AB. La catalana Xocolating 1944, impulsora de Body Genius, también ha apostado por esta firma con la que ha cerrado un acuerdo, así como varios 'business angels' como Lluis Seguí, Andrea Pereira y Luis del Val. Leer

Categorías: 1 Noticias economicas en español

German psychologists finally discover how you can stop buying things you don’t need

Impulse buying and overspending defeat all of us on occasion. But no longer! The good people of the psychology department at Germany’s Julius-Maximilians-Universität have found a solution: It all comes down to understanding your type.

- Pleasure seekers crave enjoyment, and are frequently driven by spontaneity or curiosity, such as wanting to treat themselves to a truffle they’ve never tried before, or add a great pair of jeans to their wardrobe. They are reaching for pleasure. So curbing those expenditures is a matter of curbing the spontaneity by forcing a pause between the urge and the purchase. The solutions here are low tech, such as keeping a note on your wallet that says “STOP,” or limiting immediate access to money (by locking cash or credit cards in a desk drawer or car, for instance). The goal is to halt the impulse.

- Security seekers are slower to buy. They’ll stand in front of an object and think, Will this taste as good as it looks? or spend 10 minutes hovering over the “buy” button online. For them, the key is to simply not give themselves the time to consider: They need to walk away, or stand up and take a break from their computer.

These findings are based on two research studies—recently published in PLoS One—carried out on 250 participants. Interestingly, security seekers were just as likely to impulse buy, and just as likely to want to treat themselves. But the motivational state of the would-be consumer also plays a large role. For example, the researchers found that someone who has just studied their dwindling bank balances is less likely to buy, while a pleasure seeker who just got a promotion may well celebrate further via consumerism. You can manipulate your own mood before shopping accordingly.

Categorías: 3 Noticias economicas ingles

Elvis (Your Waiter) Has Left the Building

An endless series of articles have been discussing America’s Labor shortages, especially in foodservice and hospitality. Blame has been spasmodically assigned to everything from too generous unemployment benefits, fear of Covid, lack of childcare, skills mismatch, and more (see this LOL Hamptons piece).

I have a different theory: Waitstaff, bartenders, hotel maids, busboys, dishwashers (and others) used the year of lockdown to level up, gain new skills, find not new jobs, but new careers. They have exited difficult, thankless, dead-end jobs for a chance at the American Dream.

Elvis has left the building... *

Can you blame them? I worked my way through college mostly as a waiter, but also anything else I could do (tending bar, making ice cream sundaes, short-order chef). It was exhausting, on your feet work, and your comp was mostly tip-based, and highly dependant on factors beyond your control: How many people came into the restaurant, which was affected by weather, reviews, etc.

The CARES Act monies flowed to people mandated to shelter in place at home. Many of them did not spend the year sitting around with their feet up, collecting bennies — they improved their lot in life. Some learned new skills, got degrees online, trained themselves for new careers.

Every time I hear about restaurants being unable to find workers, my first response is to ask if they raised wages; if they did, I ask if they were getting a lot of teenage applicants.

I suspect the people who have been blaming the worker shortage on lazy workers have gotten it exactly backward: It’s not that these folks do not want work, it is that they have been motivated to improve their lot in life. Many have changed careers, and not only that, lots of these people have been launching new businesses to capitalize on their newfound skills, and to pursue a better life for themselves. New business formation has been huge, and in 2020 it was near record-breaking pace.

Blame or credit? I hold no doubt that unemployment benefits are a factor here — just not in the way that so many people think.

Previously:

Wages in America

Table Stakes (June 10, 2021)

What Makes Teen Employment Data So Interesting… (June 9, 2021)

Finding it Hard to Hire? Try Raising Your Wages (May 6, 2021)

___________________

* The origin of the title phrase literally refers to Elvis Presley exiting the stadium after a show. Read about it at Wikipedia or The Idioms.

The post Elvis (Your Waiter) Has Left the Building appeared first on The Big Picture.

Categorías: Blogs y opiniones de economia en ingles

Bruselas da luz verde con condiciones a la compra de Willis por Aon

El Ejecutivo comunitario de su aprobación a la mayor compra de la historia en el sector de los seguros con la condición de que Aon venda una gran parte del negocio de intermediación de Willis a la estadounidense Arthur J.Gallagher Leer

Categorías: 1 Noticias economicas en español

New CDC school guidance weighs in on masks, vaccines, ventilation, and more

Summertime is in full swing but during the COVID-19 era, fall is of chief concern as the virus’s delta variant rises and Americans remember the case surges of last autumn. As we fight on and into this next season, the Centers for Disease Control and Prevention is reminding us that of all things the pandemic can take, learning shouldn’t be one of them.

For kids, that means getting the best education possible—which is most likely to happen in-person. When K-12 schools reopen this fall, the CDC and federal officials are urging that all students, vaccinated or unvaccinated, be welcomed back into their hallways and classrooms. The agency has released its newest guidance for COVID-19 safety in grade schools, and the report recommends typical precautions including testing, ventilation, social distancing, and contact tracing, but also mentions “the importance of offering in-person learning, regardless of whether all of the prevention strategies can be implemented at the school.”

Here are some key takeaways:

- The CDC recommends that people who are not fully vaccinated wear face masks indoors. However, it suggests that people who are fully vaccinated do not need to wear masks, which is in line with its nationwide guidance.

- Masks are generally not necessary outdoors.

- The CDC also recommends maintaining at least three feet of distance between students within classrooms wherever possible. Schools without enough space to place every student’s desk this far apart should focus on other strategies such as indoor masking.

- COVID-19 screening should be done regularly.

- Students, teachers, and staff should stay home if they show any symptoms of infectious illness.

- Vaccines, it stresses, are the leading public health initiative for a safe return to schools, extracurricular activities, and sports. Currently, children and teens aged 12 and over are eligible.

- As children under 12 years of age are still not eligible for the vaccine, schools should layer other precautions.

- Localities should monitor community outbreaks and make calls on strengthening the level of prevention as needed.

- The guidance, it reminds, is secondary to any federal, state, local, territorial, or tribal health and safety laws, with which schools must comply.

Categorías: 3 Noticias economicas ingles

Dos factores que desplomaron al mercado de valores americano

Noticias bolsa EEUU -

El mercado de valores americano está lejos de entrar en crisis, pero ayer hubo dos factores que preocuparon a los inversores: la variante delta del Covid-19 y la reducción de compra de bonos por parte de la Fed.

Categorías: Blogs y opiniones de economia en español

EU authorities clear $30bn Aon and Willis merger

Approval is fillip for insurance brokers whose combination is facing a US investigation

Categorías: 3 Noticias economicas ingles

Jointer injury

Well, it finally happened. I lost part of my right ring finger to the jointer. This couldve been avoided, but I was rushing and not paying close enough attention to what I was doing and where my hands were while jointing the edge of a 5 wide board. The guard was also not retracting all the way and needed repair, which I knew about. Just a couple of quick cuts, I thought. Not looking for sympathy; nobody to blame but myself. Please learn from my mistake and take some time to review safety practices in your shop. Stay safe out there!

(.-.)

Categorías: Blogs y foros de trabajar madera en ingles

Carbonomics

The amount of capital that has and will continue to be deployed into the Carbonomics Sector is mind boggling.

It’s in the hundreds of billions and will reach the trillions.

But few of the corporations that have committed to reducing their carbon emissions have actual plans to reach their committed targets.

Billions of dollars and major company pivots are being deployed towards making net zero carbon emissions a reality.

In fact, I believe Nobel Peace Prizes will be handed out for the efforts.

Just recently…

- Shell, one of the biggest oil producers in the world, lost a Dutch court ruling and must now legally be responsible to cut their greenhouse emissions by 45% by 2030.

What does that mean?

Pay close attention to these next 3 lines…

It means that Shell needs to buy (and/or create) over 100 million carbon credits a year for the next decade.

Let’s put that in perspective…

In 2020, 223 million voluntary carbon market credits were issued

Read that again:

- To meet target emission cuts, Shell would need to buy 45% of ALL the voluntary carbon market credits issued last year. EVERY YEAR.

That’s just the ONE oil giant, Shell.

You can see immediately how the Shell ruling will have implications for climate cases around the world.

Is Shell just a one off?

Not even close.

24 hours after the Shell court ruling, Exxon’s board of directors had a massive shakeup.

Two board seats were won in a bitter proxy fight by an unknown climate fund called Engine No.1. Changes in climate action by the executives at Exxon are underway.

Then the shareholders of Chevron voted, and changes will happen there as well.

Dirty Oil and the Green Bond BonanzaIt’s only a matter of time before other oil companies and large resource miners follow suit.

But here’s my main point—it’s not a bad thing.

The old guard has resisted, yet they overlook the benefits that will come from this.

- For the first time, the oil and metal miners can tap into the low-cost source of capital available in the green bond market.

A major positive will be that their borrowing costs decrease.

Companies who lower their carbon footprint will attract new investors – who have avoided the extraction industries, that create a large carbon footprint relative to their share price…

And thus increase the demand for their shares.

By reducing their carbon footprint there are major benefits to both the cost of interest in the bond markets and the share price of the shares.

It’s a real win-win.

Whether you agree with this or not, there is an opportunity to make a lot of money from this movement.

We’re fine with others getting the credit, awards, and recognition.

Alligators only care about making money while doing positive things that better society.

So how much is at stake?

Here’s what got me very interested…

The amount of money flowing into the space is simply unstoppable…According to Bloomberg Intelligence, ESG debt issuance recently surpassed $3 trillion this week.

It took 12 years to issue the first trillion dollars and 1 year for the second trillion.

In the past 6 months, a third trillion has been added.

- Already in 2021, more ESG debt has been issued than in the prior year.

Make no mistake, the ESG sector is scorching hot…

Even Russian companies such as PolyMetal are tapping into the Green Bond market.

They are doing this to reduce their cost of capital by committing to reduce their carbon footprint.

Are Carbon Credits a Tax?There’s a major misconception and wrong belief that carbon credits are a tax or a tariff.

They’re not.

They’re an output commodity cost, and by reducing their footprint, corporations can make money.

How you ask?

By reducing their cost of capital and increasing their potential shareholder audience.

Debt raised with an ESG focus is cheaper on average than non ESG debt.

Don’t believe me? Ask the VP of Treasury of one of the world’s largest pipeline companies…

Max Chan, stated its recent sustainability linked debt came in 5 basis points lower than where regular debt would have priced.

Telus, one of Canada’s largest telecom providers, issued a sustainability linked note. And it came in 6 basis points lower than would be expected in the regular debt markets.

Scope Emissions: Going Green Is Good BusinessNow let’s return to some further carbon reduction considerations.

There are more than 5,200 companies with $1 billion+ market caps that are publicly listed and trade on the North American and European stock exchanges.

Of those, 2,410 companies report their Scope 1 greenhouse gas emissions.

A little background:

- Scope 1 Emissions are the direct greenhouse gas emissions from company operations.

- Scope 2 Emissions are the indirect greenhouse gas emissions from energy purchased by the company.

Scope 1 and Scope 2 emissions are within the direct control of a company.

The criteria for identifying and reporting them is well established, transparent, and consistent across industries.

- Scope 3 emissions include the indirect emissions (not included in Scope 2) that occur in the value chain of the company (this includes both downstream and upstream emissions). These remain underreported.

There needs to be more legislation and international body governance on Scope 3 emissions as they include many “grey” areas open to interpretation and debate.

The chart above only includes Scope 1 carbon emissions, as there are no debates or discrepancies concerning these.

- The fact that only 46 percent of large-cap companies report their Scope 1 emissions will change.

Regulatory authorities such as the SEC are on the case.

And it’s only a matter of time before they mandate that all companies include a Scope 1 emissions report in their financial statements.

Scope 2 reporting will follow, and perhaps eventually Scope 3.

But reporting is one thing—action another.

Currently, out of those 5,230 companies with $1 billion+ valuations that are publicly listed in North America and Europe…

- Only 457 (8.7%) companies have publicly announced some kind of plan to reduce GHG emissions as of May 25, 2021.

This does not mean that the companies have actually achieved any reductions…

Only that they are talking about trying to implement strategies (many of which they have not even started).

Again, this will change.

In the meantime, my major focus right now (aside from resources) is the hottest commodity sector right now.

I believe the Carbon Credit market is in its infancy…

And there is MUCH more information that I’m not sharing here in this alert to you.

I cannot tell you how many calls and contacts my team and I have fielded in this emerging sector.

Just as technology underpins almost every market from grocery stores to car manufacturers…

Carbon credits, emission reduction and green bonds will affect EVERY industry.

I’ve never seen a market quite like this in my career.

And if it sounds like I’m excited and talking my own book – that’s because I am.

After taking profits and free rides in many of our portfolio positions in my premium research service – Katusa’s Resource Opportunities…

I have a significant portion of my net worth allocated in the Carbon sector.

This is only the beginning.

And you don’t get too many asymmetric shots like this. So do yourself a favor and get up to speed ASAP.

Regards,

Marin Katusa

The post Carbonomics appeared first on Katusa Research.

Categorías: Blogs y foros de trabajar madera en ingles

Apertura en Wall Street: el Dow Jones rebota este viernes y sube más de 200 puntos

Noticias bolsa EEUU -

Wall Street arranca la sesión con tono positivo tras una jornada en la renta variable teñida de rojo con abultadas caídas en todos los continentes. No obstante, de fondo, el temor a la desaceleración del crecimiento debido a la variante Delta. El euro se aprecia frente al dólar y los precios del crudo suben en torno a un 1,8%. Bank of America sube un 1,5%, por detrás de Royal Caribbean y Carnival, con un 2%.

Categorías: Blogs y opiniones de economia en español

Páginas

Custom Search