Se encuentra usted aquí

Agregador de canales de noticias

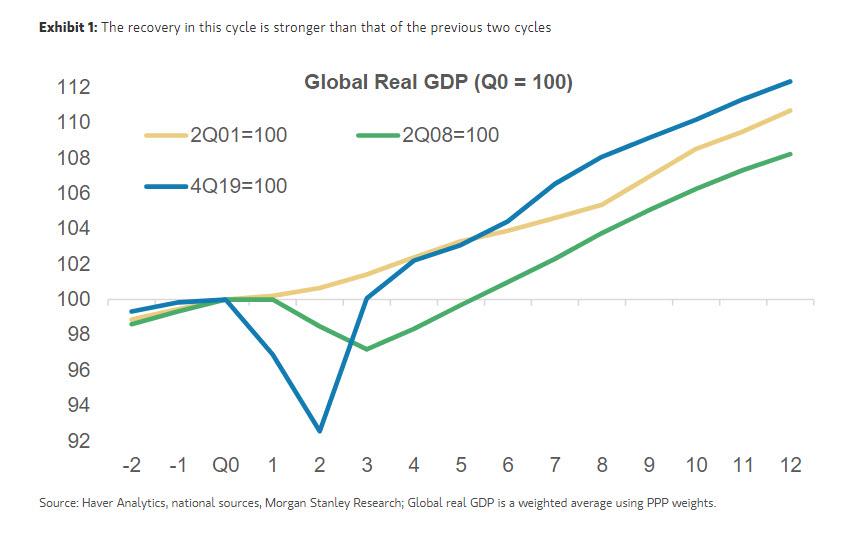

Morgan Stanley: Today We Are Facing Another Growth Scare, And It Too Will Fade

Morgan Stanley: Today We Are Facing Another Growth Scare, And It Too Will Fade

By Chetan Ahya, Morgan Stanley's Chief Economist and Global Head of Economics

Nearly a year ago, we wrote in the Sunday Start about the first growth scare of the new cycle (see Three Reasons Why the Recovery Is on Track, July 26, 2020). Then, a rise in COVID-19 cases sparked fears of renewed lockdowns, and the delay in passing additional fiscal stimulus in the US led to concerns that the consumption recovery would sputter.

Today, we are facing another growth scare. Just like the last time, we see good reasons why these fears will fade.

#1 – The virus/economy equation continues to evolve

The more transmissible Delta variant is leading to a renewed rise in cases, particularly among unvaccinated populations. Encouragingly, while case counts are rising, all indications are that existing vaccines are still highly effective in preventing severe illness and, more importantly, hospitalisations.

{kind=link}

Hence, for economies with relatively high vaccination rates, like the US, UK and euro area, we don’t expect hospital system capacity to be overwhelmed and thus see a low probability of strict lockdowns returning. For economies which are lagging in their vaccination efforts, for instance parts of Asia, the risk is that variants will delay a full relaxation of restrictions. While the recovery in external demand and capex is advancing for these economies, we see domestic consumption being held back over the next 3-4 months. However, vaccinations are expected to pick up, which would give policy-makers greater flexibility to reopen their economies, setting the stage for a broad-based recovery to take hold late this year.

#2 – US: Withdrawal of policy support is not as premature as you think

As recoveries progress and economies move towards a self-sustaining path, it is only natural for policy-makers to start thinking about exit strategies. However, we believe that neither fiscal nor monetary policy support will be removed at a faster pace than warranted.

The US economy is already on a strong footing. Wage incomes stand at 105% of pre-COVID-19 levels, real investment is already 4% higher and GDP has reached its pre-COVID-19 path.

While the fiscal impulse is turning negative this year, its impact on growth has been overstated. That’s because fiscal measures have largely taken the form of transfers to households. In fact, the excess transfers are still sitting on household balance sheets, waiting to be spent. US households have accumulated US$2.3 trillion in excess saving, and our strong US GDP growth forecasts of 7.1%Y for 2021 and 4.9%Y for 2022 don’t assume that this stock will have to be drawn down.

{kind=link}

As regards the Fed, our chief US economist Ellen Zentner continues to expect forward guidance in September and an official announcement of tapering in March, with the risks skewed towards an earlier start. By the time tapering starts, we forecast that the US economy will be well above its pre-COVID-19 path, core PCE inflation will exceed 2%Y sustainably (adjusted for base effects and transitory factors) and U-6 unemployment (the broadest measure) will reach ~8.5% (versus a pre-pandemic low of 7%) as compared to 13% during the time of tapering in December 2013 – hardly conditions that indicate the withdrawal of accommodation is premature.

#3 – China: From tightening to modest easing

While growth is usually sustained by external demand and capex during periods of counter-cyclical tightening, COVID-19 flare-ups have hampered the private consumption recovery in this cycle. Accordingly, policy-makers are beginning to fine-tune their policy stance to offset the effects of the resulting small growth downside. Our chief China economist Robin Xing expects modest fiscal easing, complemented by liquidity injection and the cut in the reserve requirement ratio on July 9. We remain confident that China’s GDP will grow by 8.7%Y this year.

#4 – Supply-side constraints are transitory

Supply-side constraints continue to be reflected in the sub-indices of the manufacturing PMIs – supplier delivery times and inventories. What’s more, these obstacles have dampened production, with a shortage of chips crimping auto production and leading to downside surprises in Japan and Korea’s industrial production growth. Similarly, labour shortages have hampered services sector growth, especially in the US, where labour participation has been held back in part because generous unemployment benefits are still in effect in some states and schools have yet to fully resume in-person learning. However, we expect labour supply conditions to improve over the next 3-4 months, enabling production to ramp up and inventories to return to more normalised levels, providing a strong boost to GDP growth.

Overall, we see this growth scare as just that – a scare. Indeed, while there have been some downside growth surprises in economies like China and India, they have been offset by upside surprises in Europe and Latin America, keeping our global growth forecasts unchanged (at 6.5%Y for 2021 and 4.9%Y for 2022) since we published our mid-year outlook. More fundamentally, the outlook for demand is strong, and we remain convinced that the unfolding of a red-hot capex cycle will sustain global GDP above its pre-COVID-19 path from this quarter on through to end-2022.

Tyler Durden Sun, 07/11/2021 - 12:30

Categorías: Blogs y opiniones de economia en ingles

Trends que hacen del gas natural la energía del futuro

Debido a la preocupacion mundial por la emisión de gases contaminantes y el cambio climatico, se ha empezado a hacer algunos cambios en el mix energético de los paises occidentales. Compromisos como el protocolo de Kyoto o el Acuerdo de París han oficilializado esto.

Comment on Rising Rents, Rising Fortunes For Landlords, But Is It Fair? by Olaf, the Mile High Finance Guy

In reply to Rob.

It is wishful thinking, in our current political climate this will not get passed through. Coupled with the fact that high end homes are selling like hot cakes, there is little organic potential for this to happen. Nonetheless, recognizing the problem is the first step.

Categorías: Blogs y opiniones de economia en ingles

Opiniones sobre MyInvestor

esbufega:

No paro de llamar y mandar mails al servicio cliente y no se dignan ni a responderme. No sé cuál es el problema ni cómo solucionarlo.

Lamento mucho su situación, sé la incertidumbre que genera ; para mi pienso que los correos electrónicos llegan a un lugar sin responsable y por lo tanto nadie los atiende.

En mi periplo estos son los teléfonos que he recopilado, algunos son Myinvestor, otros de Inversis ( creo que una mesa de contratación ) y el último de Andbank, pruebe a ver.

-900154401

-900800555

-910005981

-910005961

-918228420

Deseo que pueda resolver pronto su situación e insista, en mi caso la llave fue dar con una persona que lo enfoco de otra manera, suerte.

Brussels set to delay digital levy plan after G20 backs tax deal

Move intended to defuse US criticism and smooth path to final agreement

Categorías: 3 Noticias economicas ingles

Brussels set to delay digital levy plan after G20 backs tax deal

Move intended to defuse US criticism and smooth path to final agreement

Categorías: 3 Noticias economicas ingles

Tech Companies to Buy Covid-19 Vaccines on Behalf of Taiwan

The roundabout arrangement with TSMC and Foxconn effectively ends a monthslong geopolitical impasse over whether Taiwan could buy vaccines directly from BioNTech.

Categorías: 3 Noticias economicas ingles

Affinium Internacional FI - Hilo oficial

kr1pt0man:

no veo el problema en “fusilar” partes de un artículo si les sirve para explicar en qué se basan

¿No ve el problema en fusilar partes de un artículo hecho por un tercero haciendo creer que es propio y negándolo posteriormente cuando alguien lo descubre?

Fondos: Numantia Patrimonio Global

kr1pt0man:

Posiblemente se equivocara, se diera cuenta a posteriori y deshizo posición al darse cuenta y admitir su error.

Seguramente tenga ud. razón y fue ese un caso aislado en los que el gestor invirtió en un sector que, aparentemente, desconocía profundamente (dos veces). Saludos.

Biden Stakes Out Position in Debate Over Power of Big Companies

A body of academic research shows the U.S. economy has become less competitive as power swells in large firms, but not everyone agrees.

Categorías: 3 Noticias economicas ingles

Tencent Offers 30%+ Upside Following Beijing's Crackdown On Big Data

Categorías: Blogs y opiniones de economia en ingles

Fondos: Numantia Patrimonio Global

Underhill:

No es que no me convenzan las bromas, lo que no me convencen son las incoherencias, y en sus inversiones (y rotaciones) hay múltiples. Puede ver su tesis de inversión en IMB en la que se demuestra que no sabía nada del sector en el que invertía, seguida de su compra (y venta casi automática) de PM que aún resulta más incomprensible.

Posiblemente se equivocara, se diera cuenta a posteriori y deshizo posición al darse cuenta y admitir su error. Quizás lo respetable y admirado sea la postura de otros gestores con mayor prestigio, persistiendo en el extraordinario valor de su cartera con empresas “imbatibles” como Dixons o comprando más y más pan suizo a pesar de estar en mal estado, por poner un ejemplo…

Son puntos de vista… Lo malo es que la verdad a veces no se llega a saber nunca, y en otras ocasiones, cuando se sabe, ya es muy, muy a posteriori y resulta irrelevante después de un -64% pero con un gran proceso detrás…

Saludos

Realty Income: Fairly Valued And Market Timing Based On Yield Spread

Categorías: Blogs y opiniones de economia en ingles

Affinium Internacional FI - Hilo oficial

fisherB:

Creo que ya lo comenté antes, copiar e inspirarse lo hacen quizás todos, o casi todos. Lo que me chocó es cuando se les dice: “uy, esto suyo se parece muy mucho a esto de otros que salió unos años antes” y lo niegan por lo civil y lo criminal y se arma la marimorena.

Sinceramente, no veo el problema en “fusilar” partes de un artículo si les sirve para explicar en qué se basan. ¿Estamos en el colegio a ver si alguien copia a alguien? - Al final, TODOS nos basamos en los conocimientos de los que estudiaron las cosas antes que nosotros. Sinceramente, creo que esto es sacar las cosas de quicio, o como decían antes, “ser más papistas que el Papa”. No estamos en un entorno académico corrigiendo exámenes. Si estos señores se basan en el ejemplo y los datos de ese paper para explicar lo que hacen, pues estupendo. ¿Qué problema hay? - TODOS, repito: TODOS bebemos de las fuentes y al final el conocimiento humano se basa en reutilizar lo que los que nos antecedieron investigaron y aprendieron antes que nosotros. Desde Pitágoras…

La respuesta de estos señores ha sido perfectamente lógica. Lo que no veo sensato son este tipo de acusaciones pueriles y estériles que a lo único que conducen es a que se larguen pensando que somos una panda de críos infantilizados. (Que parece que lo somos).

Un saludo

Sun Communities Stock Is Estimated To Be Modestly Overvalued

Related Stocks: SUI,

Categorías: Blogs y opiniones de economia en ingles

"Tear Up The Streets, Not The Planet" - Dodge To Unveil World's First Electric Muscle Car In 2024

"Tear Up The Streets, Not The Planet" - Dodge To Unveil World's First Electric Muscle Car In 2024

Dodge, an American brand of automobiles and a division of Stellantis, used its time during Stellantis' EV Day to announce the world's first electric muscle car will hit the streets in 2024.

Dodge CEO Tim Kuniskis was featured in a 5 min video, talking about the company's multi-decade muscle-car heritage. He said the company must adapt to the changing times as millennials become a more significant part of the overall US population with more spending power, adding this generation embraces electric cars the most.

With that being said, Kuniskis revealed that Dodge has plans to sell the world's first electric muscle car in 2024. He said, "Tear Up the Streets … Not the Planet."

However, only a conceptual version of what the new electric muscle car would look like was revealed in the video. Even then, the lighting was too dark to capture what the overall design of the car would look like but certainly had some "retro-inspired styling cues, with a fastback roofline and blunt fascia that look vaguely reminiscent of the iconic 1969 Dodge Charger," said Autoblog.

The front of the concept car sports a unique lighting profile, with what looks to be an LED light bar that mimics the square-jawed shape of the classic muscle car but with the addition of a lighted emblem directly in the center. Several jump cuts showed some very wide-looking wheels with meaty tires ... and we're certain that all four of those tires go up in smoke at the end.

{kind=link}

The car will be built on the STLA Large platform, one of four battery electric vehicle platforms announced by Stellantis, with a 0-to-60 time as low as 2 seconds and a range of up to 500 miles, Stellantis said. The automaker also hinted at a maximum power output of as high as 886 horsepower courtesy of a pair of 330-kilowatt electric motors.

{kind=link}

-Autoblog

With Dodge engineers hitting the limit of what they can pump out of Hemi engines, it appears the company must embrace electrification for more horsepower to take on the Tesla Model S Plaid.

The next Tesla killer?

Tyler Durden Sun, 07/11/2021 - 12:00

Categorías: Blogs y opiniones de economia en ingles

Yields Plunge. Dollar Surges. The Reflation Trade Unravels.

Categorías: Blogs y opiniones de economia en ingles

Páginas

Custom Search