Se encuentra usted aquí

zerohedge

Government's Global Response To COVID Has Absolutely Decimated The Middle Class

Government's Global Response To COVID Has Absolutely Decimated The Middle Class

Very few, if any, financial outlets have been more outspoken over the last decade about the harm that governments can do micromanaging (and in this case, shutting down) economies than we have been.

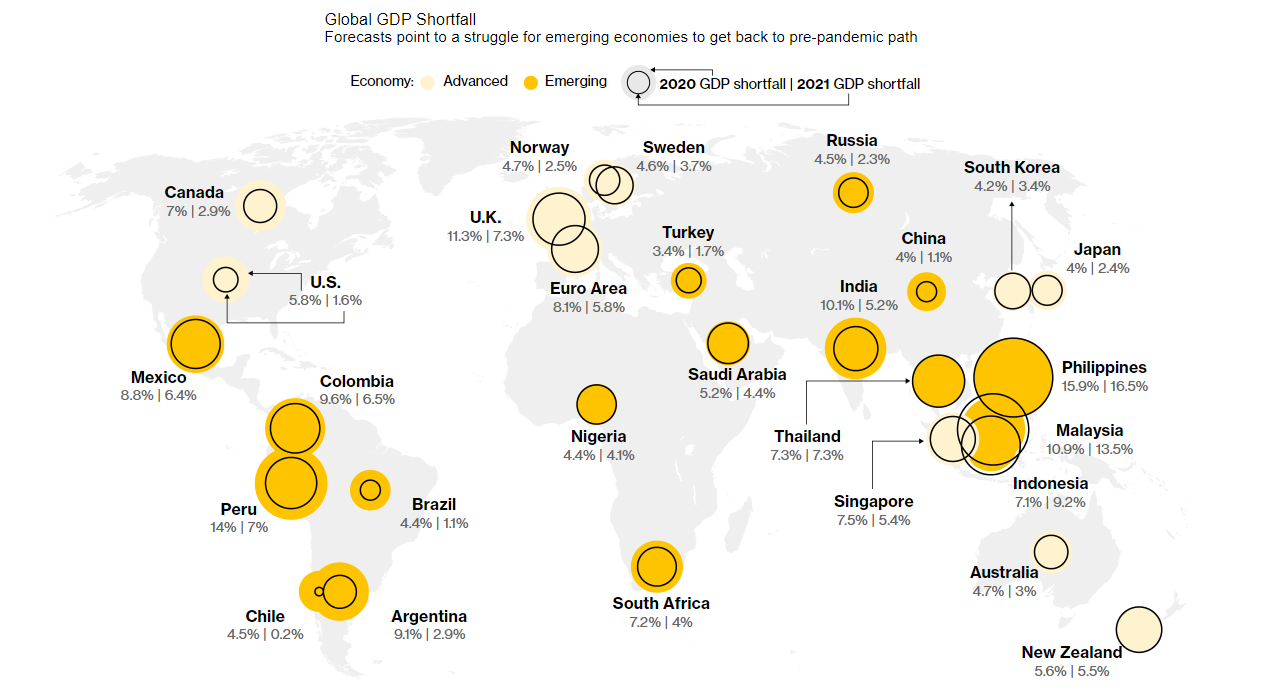

Which is why we weren't surprised to see a brand new report noting that due to the pandemic (and the ensuing global 'stimulus' response) more people than ever are falling out of the middle class. Published by Bloomberg, the report defines 'middle income' earners as those making from $10 to $20 per day, smoothed out across geographical borders. Those making $20 to $50 per day are considered "upper middle income".

These two brackets make up 2.5 billion people, or about 33% of the world's population. And of that group are numerous stories from numerous countries of what Bloomberg calls "hard won successes that evaporated overnight".

{kind=link}

The outlook for the future doesn't look promising, either. The IMF predicts that the global economy in 2024 will be 3% smaller than it would have been if Covid hadn't happened. For example, India's GDP will be 5.2% smaller than it would have otherwise been. (And we're sure no one will do anything to hold China accountable for this massive global dent to GDP, either).

{kind=link}

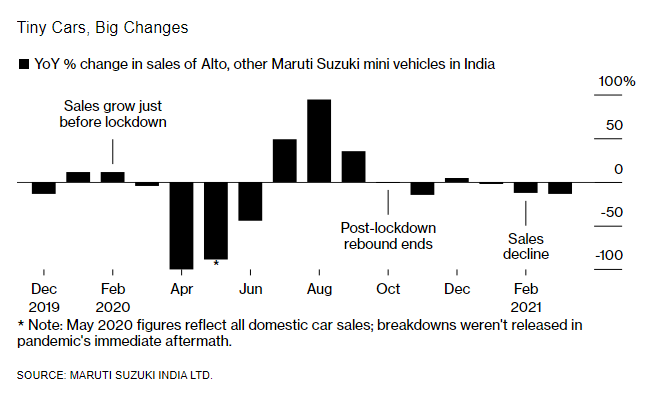

In India, the report highlighted Ravi Kant Sharma, who had spent "more than a decade" saving up to buy a car. He started 2020 with enough for a down payment and plans to celebrate his wedding anniversary. By the end of the year, he had lost his job, ate into his savings and had to put his car on hold.

{kind=link}

“I have exhausted all my savings. We are finding it difficult to pay installments of existing loans,” he said. “My life has been set back by at least three years, even as my dreams have moved beyond my reach."

Francinete Alves of Brazil is also making sacrifices, eating kidney, tongue, liver and other organ meat sporadically as egg consumption in the meat-heavy country rises. Alves is still employed, making about $881 per month, but soaring food prices have caused her to make changes in her diet. She now looks for discounts at butcher shops before she goes grocery shopping.

“In the past, 20 reais was enough for you to leave here with a lot of things. I keep thinking about people who have a family to support and receive only a minimum wage,” Alves says. “I honestly don’t know how they live”

In South Africa, 26 year old Mosima Kganyane had finally just leased her own apartment. After Covid hit, her employer faced bankruptcy and laid her off, contributing to the country's 32.5% unemployment rate. She paid a $271 fee to break her lease and move back in with her family. She now works a temp job and has spent $1,000 to put an addition on her parents house so she could rent a room.

{kind=link}

She told Bloomberg: “Covid-19 taught me not to relax and that I need to fight, to fight for survival because I don’t know what tomorrow holds.”

In Bangkok, food vendors like Yada Pornpetrumpa are dealing with a smaller, laid back crowd of tourists to sell to late after losing 75% of thier business. She now lives on government assistance and her income has plunged 90% per day.

{kind=link}

“Before all of this, when I started setting up my shop, there would already be a line for fruit juice,” she says. “I had a 50% profit on everything I sold.”

Sadly, she concluded with an affirmation that despite having few assets, she remains happy: “Having a car or a house is just what society tells us we should value, but it doesn’t define the middle class. I have no assets now. But I have peace of mind.”

Categorías: Blogs y opiniones de economia en ingles

Newsom Neutered Again - Supreme Court Blocks California's Restrictions On In-home Religious Gatherings

Newsom Neutered Again - Supreme Court Blocks California's Restrictions On In-home Religious Gatherings

Authored by Zachary Stieber via The Epoch Times,

The Supreme Court late Friday ruled against California, blocking the restrictions ban on in-home Bible studies and other religious gatherings.

The court’s narrow 5–4 ruling was in favor of a group of Santa Clara residents who asserted the restrictions violated the First and Fourteenth Amendments of the U.S. Constitution.

“Applicants are likely to succeed on the merits of their free exercise claim; they are irreparably harmed by the loss of free exercise rights ‘for even minimal periods of time’; the State has not shown that ‘public health would be imperiled’ by employing less restrictive measures,” an unsigned opinion of the court’s majority said in its opinion.

The ruling is the fifth time the nation’s highest court has overruled the Ninth Circuit Court of Appeals on California COVID-19 fueled restrictions, including a February ruling that saw the court grant a worshipper’s application asking for restrictions on in-person religious services be rolled back.

“It is unsurprising that such litigants are entitled to relief. California’s Blueprint System contains myriad exceptions and accommodations for comparable activities, thus requiring the application of strict scrutiny,” the majority wrote on Friday.

{kind=link}

The blueprint system is the statewide criteria for loosening or tightening restrictions based on the level of CCP virus spread.

Justices Samuel Alito, Clarence Thomas, Brett Kavanaugh, Neil Gorsuch, and Amy Coney Barrett made up the majority.

Chief Justice John Roberts, another Republican-nominated justice, joined the court’s liberal wing in dissenting, though he did not sign on to the dissenting opinion authored by Justice Elena Kagan.

Kagan said she would have rejected the application for relief because she felt the state complied with the First Amendment in its limiting religious gatherings in homes to three households since the state had the same restrictions on secular gatherings in homes.

“It has adopted a blanket restriction on at-home gatherings of all kinds, religious and secular alike. California need not, as the per curiam insists, treat at-home religious gatherings the same as hardware stores and hair salons—and thus unlike at-home secular gatherings, the obvious comparator here,” she wrote.

The original order in the case denying the application for relief came from U.S. District Judge Lucy Koh, who said that in light of “the unique risks of gatherings in spreading COVID-19; the deaths and serious illnesses that result from COVID-19; and the overwhelming strain on the healthcare system,” enjoining the state and county restrictions on in-home religious gatherings “would not be in the public interest.”

The Ninth Circuit’s panel upheld Koh’s ruling, writing last month that “appellants had not satisfied the requirements for the extraordinary remedy of an injunction pending appeal.”

“Specifically, the panel held that appellants had not demonstrated a likelihood of success on the merits for their free exercise, due process, or equal protection claims, nor had they demonstrated that injunctive relief was necessary for their free speech claims,” the panel wrote.

Lawyers for the plaintiffs and defense did not immediately respond to requests for comment. California had argued in a brief on Thursday that its policy regarding in-home gatherings applied to all gatherings, no matter their purpose, while also offering the Supreme Court did not need to intervene because the state will relax restrictions later this month.

Tyler Durden Sat, 04/10/2021 - 12:00

Categorías: Blogs y opiniones de economia en ingles

Debt-Fueled Spending Won't Create Growth

Debt-Fueled Spending Won't Create Growth

Authored by Lance Roberts via RealInvestmentAdvice.com,

More debt equals less growth. In October, I discussed the “2nd Derivative Effect” and the ongoing cost of the stimulus. With the passage of the $1.9 trillion “American Rescue Plan,” will the math of debt to growth change?

Now, even Deutsche Bank credit strategist, Stuart Sparks, got the memo.

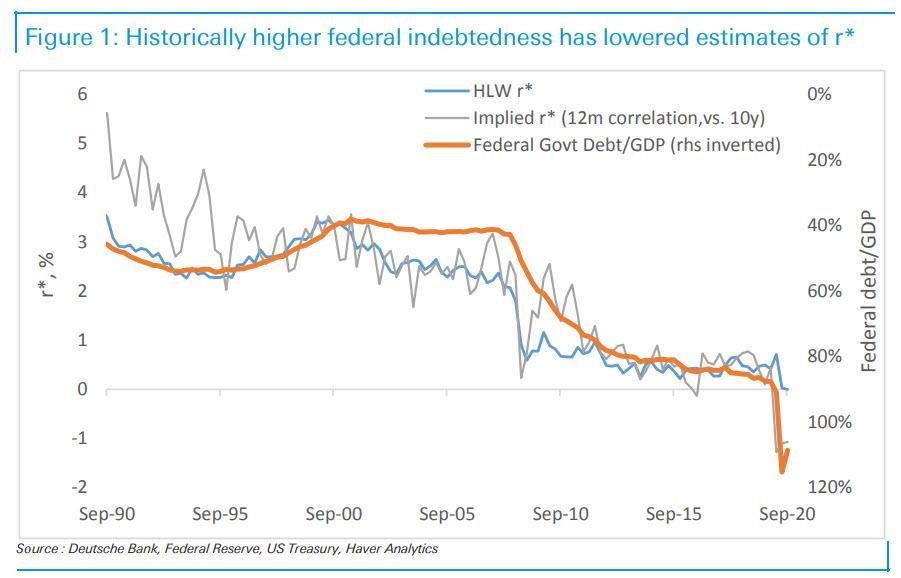

“History teaches us that although investments in productive capacity can in principle raise potential growth and r* in such a way that the debt incurred to finance fiscal stimulus is paid down over time (r-g<0), it turns out that there is little evidence that it has ever been achieved in the past.

The chart below illustrates that a rising federal debt as a percentage of GDP has historically been associated with declines in estimates of r* – the need to save to service debt depresses potential growth. The broad point is that aggressive spending is necessary, but not sufficient. Spending must be designed to raise productive capacity, potential growth, and r*. Absent true investment, public spending can lower r*, passively tightening for a fixed monetary stance.”

{kind=link}

Such is a logical conclusion, but one widely dismissed by economists and politicians. However, some fundamental analysis will underscore Mr. Sparks’ comments.

A ReviewTo keep some consistency in the analysis, let’s review the actions to date.

As the economy shut down in March of last year due to the pandemic, the Federal Reserve flooded the system with liquidity. At the same time, Congress passed a massive fiscal stimulus bill that extended Unemployment Benefits by $600 per week and sent $1200 checks directly to households.

In December, Congress passed another $900 stimulus bill extending unemployment benefits at a reduced amount of $300 per week, plus sending $600 checks to households once again.

Now, the latest iteration of Government largesse comes in a solely Democrat supported $1.9 trillion “spend-fest.” Out of the total, only about $900 billion goes to consumers in the form of $400 extended unemployment benefits and $1400 checks directly to households. The remaining $1.1 trillion will have little economic value as bailing out municipalities and funding pet projects doesn’t boost consumption.

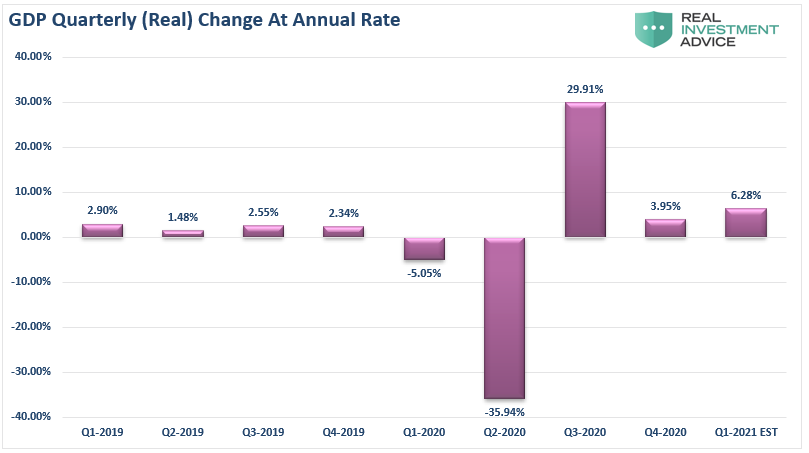

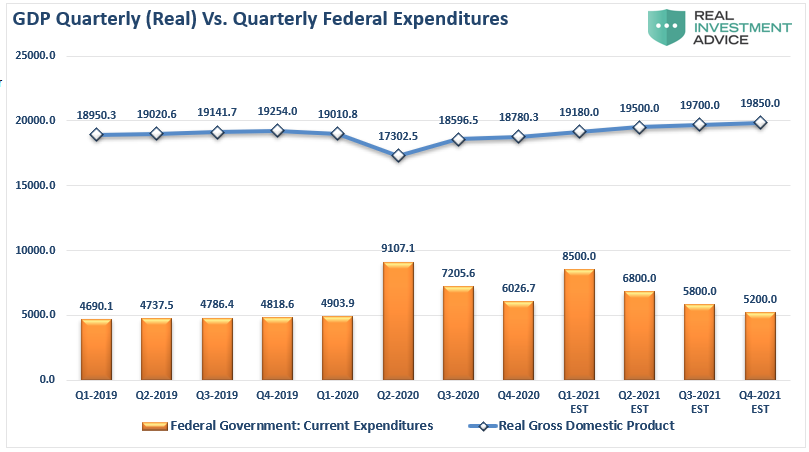

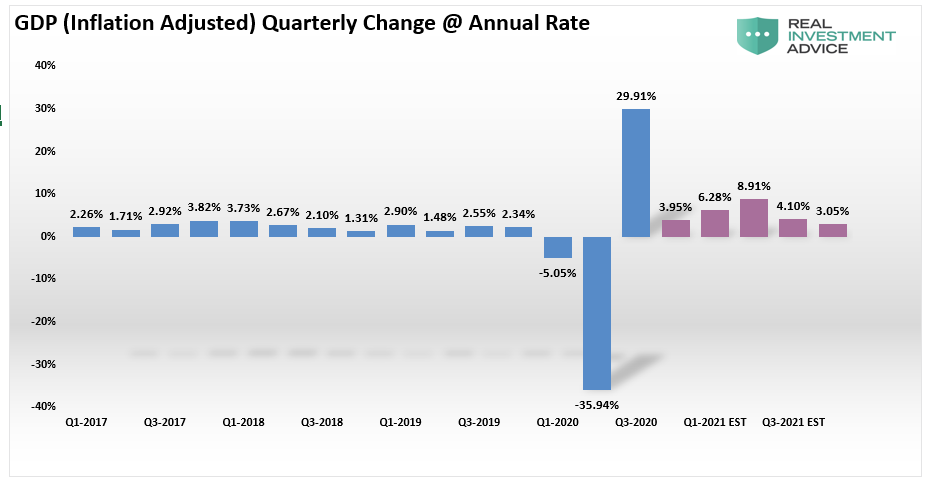

Using current economic data, we can calculate estimates for the estimated impact of the economy’s stimulus through 2021. As shown in the chart below, in Q3, the inflation-adjusted GDP surged 29.91% from the Q2 reading of -35.94%. As stimulus ran out, Q4 GDP only increased by 3.95%. If we assume that Q1 will increase by the Atlanta Fed GDPNow estimate, GDP will show an 6.2% advance. That advance is the result of the $900 billion stimulus bill in December.

Add-In Federal Spending{kind=link}

If we assume the next round of direct checks to households hit by April, GDP will rise by 6.67% in the second quarter. In other words, the “2nd derivative effect” of a larger economy reduces the rate of change from the stimulus and its ability to create growth.

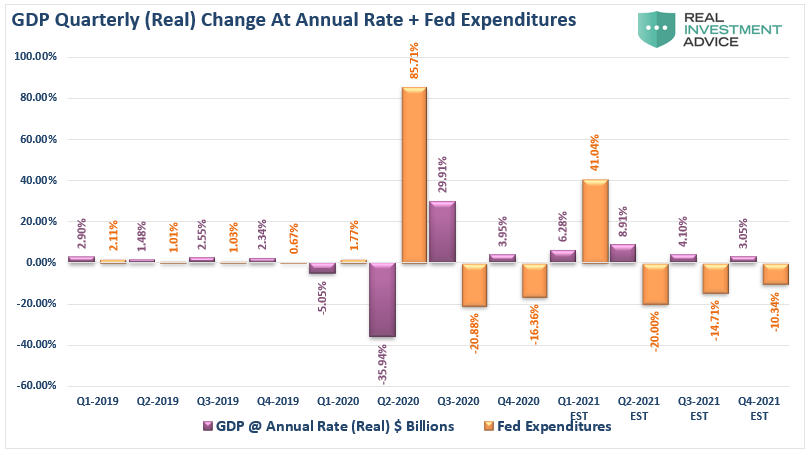

The chart below adds the percentage change in Federal expenditures to the chart for comparison. The 41% jump in expenditures in Q1 is from the combined $900 billion and 1/3rd of the latest stimulus bill. The remainder of the newest bill is then spread into Q2 and ending in Q3 of 2021. At such time Federal spending is assumed to return to is $4.5 trillion quarterly run rate.

{kind=link}

We will revise these estimates as data becomes available. However, based on previous stimulus bills’ impact, we have a relatively high degree of confidence in our forecasts.

Estimated ImpactEconomists estimate the latest stimulus bill could add nearly $1 trillion to nominal growth (before inflation) during 2021. While such a surge in growth would be welcome, it represents just $0.50 of growth for each dollar of new debt.

Such a high growth estimate also assumes that individuals will quickly spend their checks in the economy. The hope is that as vaccines become available, individuals will unleash their “pent-up” demand from the last year.

While that could indeed be the case, there are also other facts to consider.

For example, following the initial stimulus bill’s passage, following the shutdown of the economy, many workers assumed their job loss was temporary. However, a year later, unemployment remains high, and many temporary layoffs have become permanent. Such may well change individuals’ spending behavior, leading them to pay off debt, back rent, late mortgage payments, or save just in case employment remains elusive.

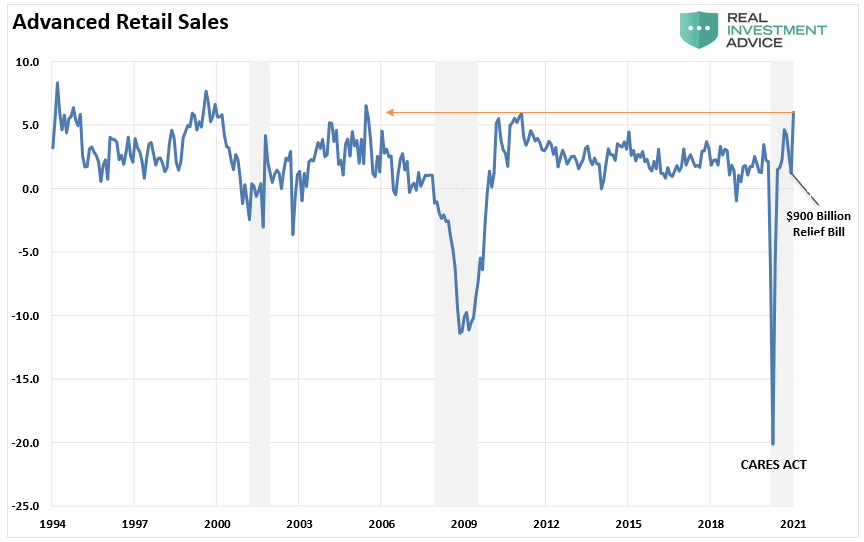

Furthermore, much of the “pent up” demand was already pulled forward by the previous two stimulus plans. We have already witnessed robust increases in manufacturing and services data suggesting consumers have been at work spending money over the last few quarters. The recent surge in retail sales confirms the same.

{kind=link}

As discussed previously, while the next American Rescue Plan will be roughly the same size as the original CARES Act, its impact on the economy will be less.

The Second Derivative{kind=link}

Such is the “second derivative” effect we explained previously.

“In calculus, the second derivative, or the second-order derivative, of a function (f) is the derivative of the derivative of (f.)” – Wikipedia

In English, the “second derivative” measures how the change rate of a quantity is itself changing.

I know, still confusing.

Let’s run an example:

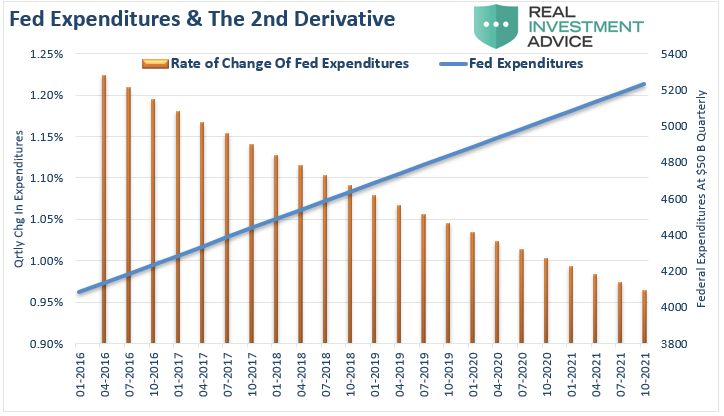

As Government spending grows sequentially larger, each additional round of expenditures will have less and less impact on the total. Going back to 2016, not including the CARES Act, the Government increased spending by roughly $50 billion each quarter on average. If we run a hypothetical model of Government expenditures at $50 billion per quarter, you can see the issue of the “second derivative.”

{kind=link}

In this case, even though Federal expenditures are increasing at $50 Billion per quarter, the rate of change declines as the total spending increase.

More Leads To LessThe following chart shows how the “second derivative” is already undermining both fiscal and monetary stimulus. Using actual data going back to Q1-2019, Federal Expenditures remained relatively stable through Q1-2020, along with real economic growth. However, in Q2-2020, with our estimates through 2021, Federal Expenditures will double. However, economic growth rates will slow quickly after the stimulus expires.

{kind=link}

The chart below shows the inherent problem. While the additional fiscal stimulus may boost short-term economic growth, its impact becomes less over time.

{kind=link}

However, this is ultimately the problem with all debt-supported fiscal and monetary programs.

A Slower Growth TrendAs stated, even with the additional stimulus package, the outcome will be muted. If we assume our current estimates for GDP growth over the next 4-quarters, which align with mainstream consensus, growth will quickly fade back to long-term trends.

{kind=link}

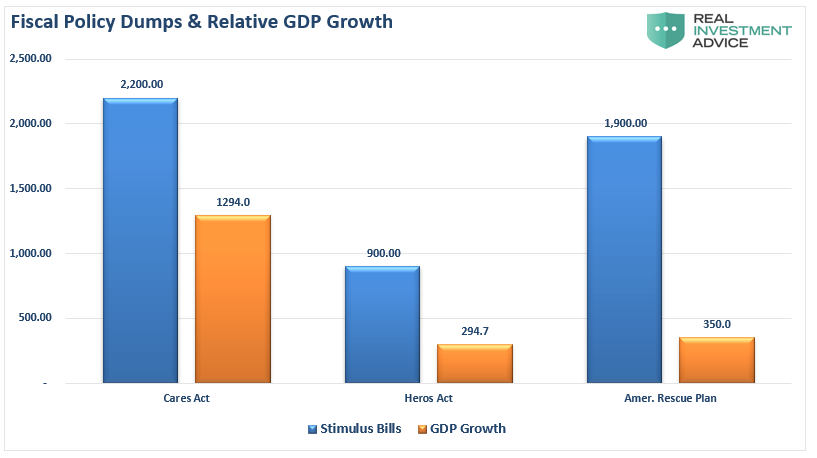

As noted above, it requires increasing levels of debt to generate lower rates of economic growth. The chart below shows the previous and estimated CARES Acts and their impact on GDP growth.

{kind=link}

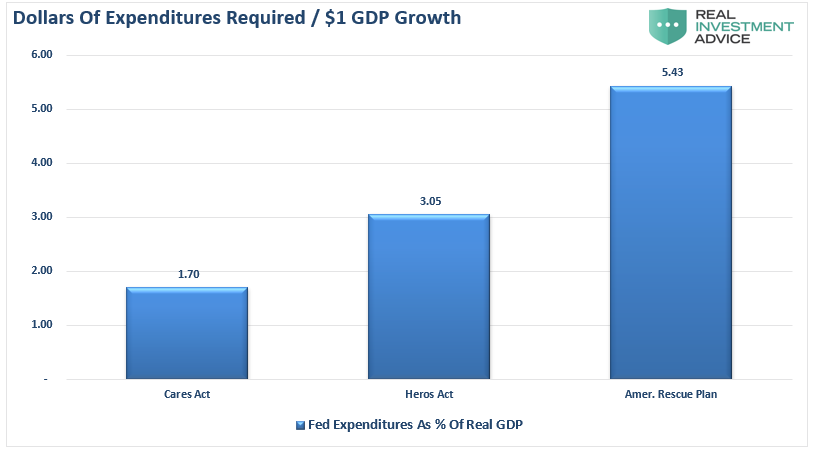

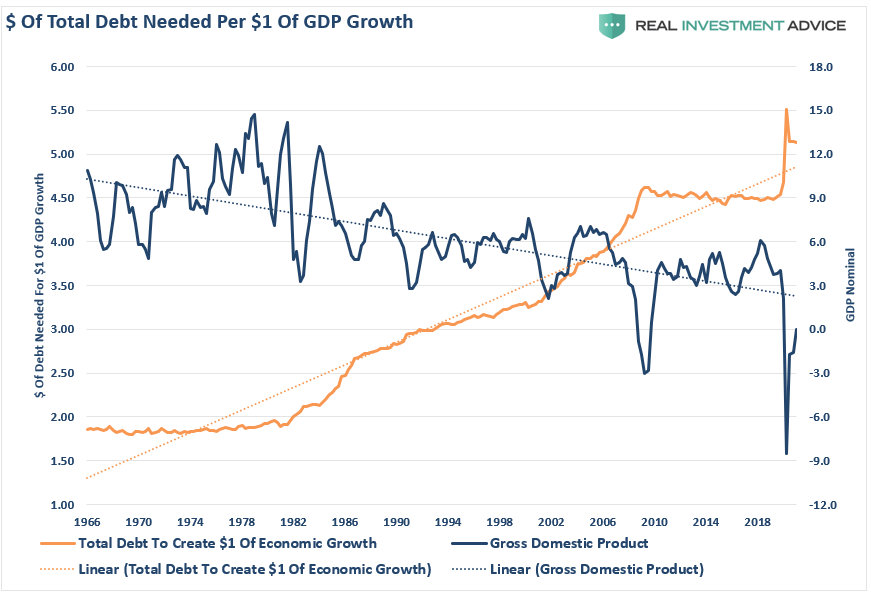

To understand this better, we can view it from how many dollars it requires to generate $1 of economic growth. Following the economic shutdown, when economic activity went to zero, each dollar of input had a more considerable impact as the economy restarted. However, going into 2021, economic activity has already recovered and started to stabilize at a slightly lower level than seen previously.

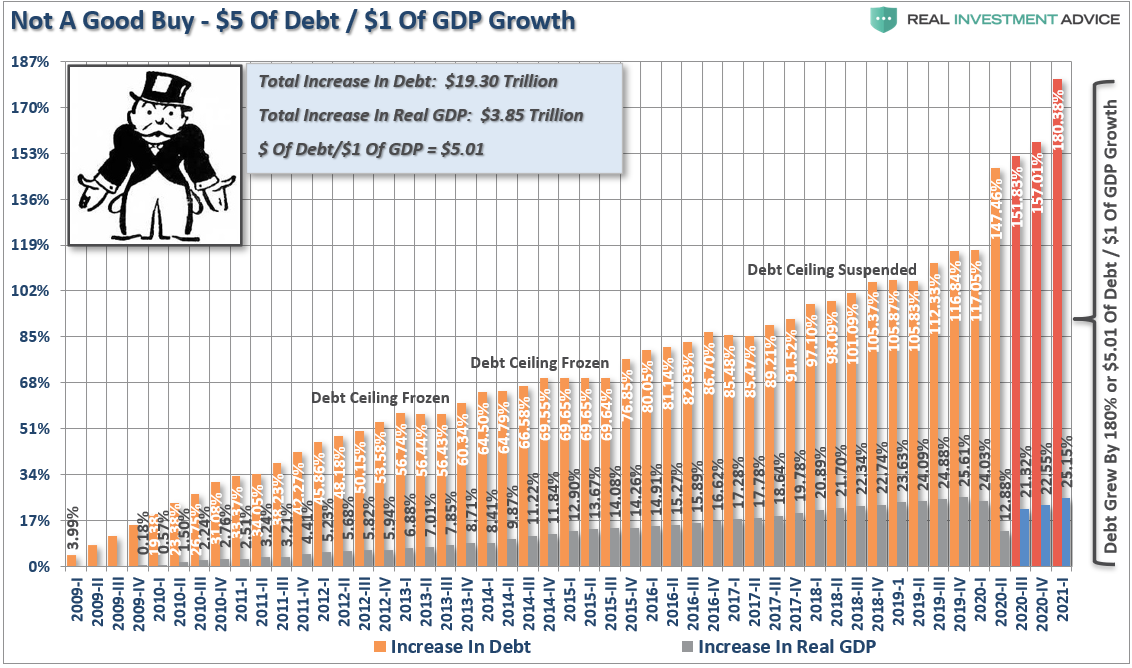

Given that stabilization of activity, it will require more dollars to generate economic growth in the future. As shown, it will need nearly $5.50 of debt-supported expenditures to create $1 of economic growth.

{kind=link}

Here is the exciting part. That is NOT a new thing. As I discussed previously, “The One-Way Trip Of American Debt,” the economy requires $5.01 of debt to create $1 of growth. While not a great return on investment, it will worsen as debt continues to retard economic growth.

You Can’t Use Debt To Create Growth.{kind=link}

As Mr. Sparks states, more debt doesn’t lead to more robust economic growth rates or prosperity. Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. With economic growth rates now at the lowest levels on record, the change in debt continues to divert more tax dollars away from productive investments into the service of debt and social welfare.

{kind=link}

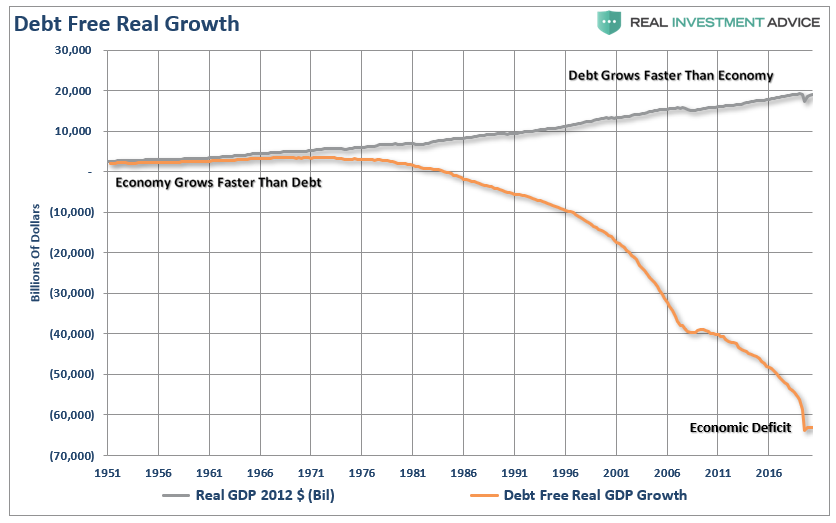

Another way to view the impact of debt on the economy is to look at what “debt-free” economic growth would be. In other words, without debt, there has been no organic economic growth.

{kind=link}

The economic deficit has never been more significant. For the 30 years from 1952 to 1982, the economic surplus fostered a rising economic growth rate, which averaged roughly 8% during that period. Such is why the Federal Reserve has found itself in a “liquidity trap.”

Interest rates MUST remain low, and debt MUST grow faster than the economy, just to keep the economy from stalling out.

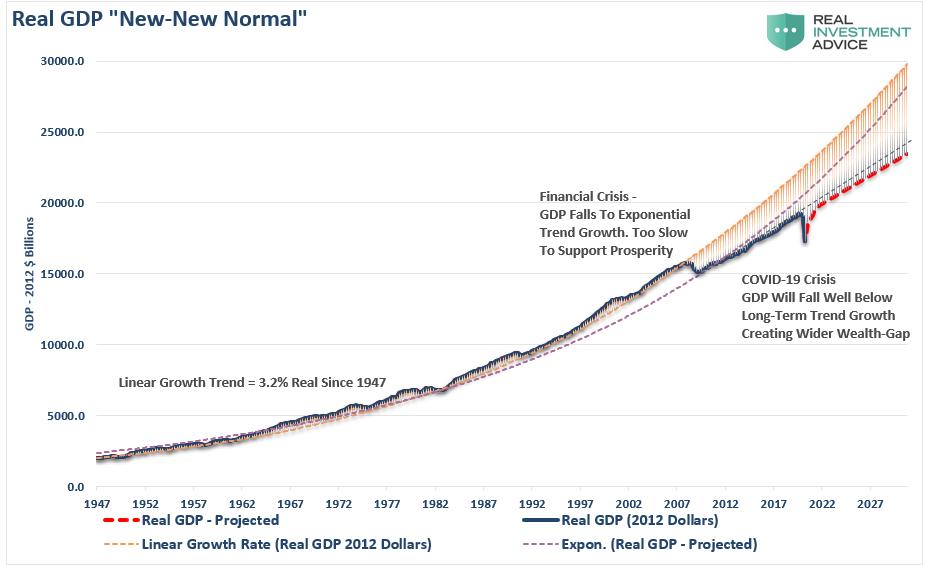

The deterioration of economic growth is seen more clearly in the chart below.

From 1947 to 2008, the U.S. economy had real, inflation-adjusted economic growth than had a linear growth trend of 3.2%.

However, following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Unfortunately, instead of reducing outstanding debt problems, the Federal Reserve provided policies that fostered even greater unproductive debt and leverage levels.

{kind=link}

Following the 2020 recession, the economic growth trend will again decline below the previous growth trend. Even with our more optimistic assumptions about economic recovery, the trend of economic growth will weaken. Such is simply a function of the massive amounts of debt added to the overall system, which will retard future economic growth.

Pulling Forward Consumption Isn’t Sustainable.Our conclusions from the initial analysis remain the same:

“The ‘trap’ that lawmakers, along with the Fed, have now fallen into is that ‘stimulus’ only pulls forward ‘future consumption.’ As we saw after the initial CARES act, as soon as financial supports evaporated, so did economic growth.

The hope over the last decade was the economy would eventually “catch fire” grow organically. Such would allow Central Banks to reverse monetary supports. However, such has never occurred. Each time Central Banks reduce monetary supports, the economy stalls or worse.

It is likely that “something has gone wrong” for the Federal Reserve. The limit of its ability to pull-forward future consumption through monetary interventions has been reached. Despite ongoing hopes of ‘higher growth rates’ in the future, such will likely not be the case until the debt overhang gets cleared.”

While the U.S. economy will indeed exit the recession in 2021, it may be a statistical result rather than an economic recovery leading to broader prosperity.

The most significant risk of the latest stimulus package is a surge in inflationary pressures, which undermines the stimulus’s benefit. That concern will manifest itself as a stagflationary environment where wages remain suppressed while costs of living rise.

Due to the debt, demographics, and monetary and fiscal policy failures, the long-term economic growth rate will run well below long-term trends. Such will only continue to widen the wealth gap, increase welfare dependency, and socialism continuing to usurp the “golden goose” of capitalism.

Tyler Durden Sat, 04/10/2021 - 11:10

Categorías: Blogs y opiniones de economia en ingles

Alibaba Slapped With $2.8 Billion Anti-Trust Fine As Analysts Ponder Whether Worst Is Over

Alibaba Slapped With $2.8 Billion Anti-Trust Fine As Analysts Ponder Whether Worst Is Over

Chinese anti-trust regulators have just slapped Alibaba with a record RMB18.2 billion ($2.8 billion) fine after concluding that the Chinese e-commerce giant had abused its market dominance for the sake of profit at the expense of Chinese society.

{kind=link}

The FT reported that China's State Administration of Market Regulation announced the penalty on Saturday. It was set at 4% of Alibaba's 2019 revenues, amounting to a slap on the wrist. Alibaba was meant to "carry out a comprehensive rectification" drive on its platform, a reference to what antitrust regulators deemed the company's primary sin: forcing merchants to sell exclusively on its Tmall and Taobao online shopping platforms. The review is intended to force Alibaba to strengthen its legal controls and compliance with the new antitrust framework. Alibaba has 15 days to submit a report detailing changes to this "illegal behavior. In a statement, Alibaba said it "sincerely accepted" the penalty.

A Chinese antitrust lawyer, who asked to remain anonymous, said the fine "was meant to teach Alibaba 'don’t think you can do whatever you want,' but [would] not materially harm the business." He noted the penalty was not as large as it could have been and was limited to Alibaba’s ecommerce operations, rather than its other industry-spanning operations.

In a roundup of commentary from domestic lawyers, academics and analysts, Reuters quoted Wu Ge, director at the Beijing Zhongwen law firm, who cautioned that the fine was a message not only to Alibaba, but to Chinese consumers.

“The fine indicates that internet platforms should also obey the laws and create real value for consumers - not just chase profits or make profitability their top priority.

The Communist party’s People’s Daily, the party's most influential mouthpiece inside China, said the fine represented a "normative correction for the company’s development, a clean-up and purification of the industry environment, and a strong defence of fair competition."

"It is an important action to safeguard fair market competition and quality development of internet platform economies," the company said. "It reflects the regulators’ thoughtful and normative expectations."

Analysts said the fine alone would not significantly affect Alibaba’s operations. The company has $48 billion of cash on its balance sheet as of the end of 2020 and earned $24 billion in net profit last year alone, another reason the fine is merely a slap on the wrist.

But Li Chengdong, chief executive of Dolphin Think Tank, was the fact that Alibaba had been found guilty of serious abuses, meaning it would be more likely to yield in future regulatory disputes over tax and counterfeit goods. "Whereas Alibaba used to have a strong, assertive stance with regulators, now it will be on the back foot," Li said.

The fine likely won't be the last handed down by anti-trust regulators to one of China's dominant tech behemoths: Tencent, whose stock is still reeling from the Archegos blowup, has also been targeted for an anti-trust 'review'.

The crackdown, which burst into public view last October after the CCP scuttled the IPO/spinoff of BABA's Ant Group, a financial group focused on providing payments and loan services to the Chinese population via smartphone apps. Ant is now facing restrictive new regulations that analysts say will hamstring its growth.

Investors will be watching to see how the fine impacts BABA's shares, which have been struggling in recent months as the anti-trust crackdown and broader pressures facing Chinese stocks weighed on demand.

{kind=link}

While some analysts dared to suggest that the "worst is over" for Alibaba, others pointed out that China's shifting regulatory framework would likely help empower Alibaba competitors like Pinduoduo, an upstart online retailer that overtook Alibaba's annual shopper count last year, with 788 million people buying on its platform, vs. 779 million for Alibaba.

Whatever regulators have in store for Alibaba, it appears Beijing isn't yet finished punishing the company's founder and longtime leader, Jack Ma, as authorities have just halted enrollment at a business school Ma founded a few years back that has become one of the most prestigious academic institutions in the country.

Tyler Durden Sat, 04/10/2021 - 10:45

Categorías: Blogs y opiniones de economia en ingles

What Could Go Wrong? 5 Ideas...

What Could Go Wrong? 5 Ideas...

From Nicholas Colas of DataTrek Research

Today we offer up a list of 5 negative scenarios for US/global equities. In no particular order: 1) markedly higher interest rates, 2) below-expectation US consumer spending, 3) heightened geopolitical risks once militaries/non-state actors are vaccinated, 4) US Big Tech regulation and 5) a raft of better investment opportunities that take capital away from global equities. We’re still bullish because we believe fiscal/monetary policy more than compensates for expected value of these downside scenarios.

* * *

Today’s Markets topic is "What could go wrong in US/global equity markets over the next 12-24 months?" As much as we’re still positive on risk assets, it always pays to consider the downside case.

Five scenarios to consider: #1: The easiest negative argument for stocks is also the simplest: materially higher interest rates begin to hurt equity valuations.Back in the 1980s, the Shiller PE for the S&P 500 was 15-20x when 10-year Treasury yields were 8-9 percent. That PE is now 30-35x in large part because yields are 1.5 – 2.0 percent. Even though the S&P today is dominated by stronger companies (Big Tech has big moats) now than in the 1980s, higher discount rates will absolutely hurt equity valuations. Maybe not a lot, but everything in capital markets happens at the margin.

Future Federal Reserve policy is also a potential pitfall. Yes, Chair Powell has promised to keep rates low, but that can’t go on forever and markets know that. That’s why we focus on 5-year Treasury yields as an early warning sign. Keeping Fed Funds at zero for the next 2 years means very little if there’s a series of 50 basis point rate hikes in the offing during 2023 – 2024.

Summary: higher rates will come because of higher inflation and, while there’s good arguments on both sides of the “low vs. high” debate, in the end “higher inflation/rates” is a very real possibility. It has been decades since that was the case, and how badly equity markets respond to this new framework is very hard to predict.

#2: US consumers’ spending patterns prove less predictable than consensus expectations.There’s a “roaring 20s” analogy making the rounds which posits that the 2020s will resemble the post-WW I 1920s, but that’s a fundamental misreading of history. Wartime, for all its horrors, is typically a period of full employment. The 2020 pandemic era was certainly not that. Further, in the 1920s the US repaid several large war bond offerings which spurred both consumer spending and stock market speculation. While that may sound familiar, there was virtually no consumer debt at the start of the roaring 1920s, unlike today.

The more correct analogy might be to what the Great Depression did to US consumer psychology: increasing the propensity to save and shunning unnecessary debt and expenses. Much of the market’s enthusiasm over future earnings increases relies on the US consumer returning to pre-pandemic form as soon as they are able. Being long the US consumer over the last 40 years has been a great bet, to be sure. But simply assuming that everything will quickly return to the status quo ante is potentially a serious blind spot for markets.

Summary: the weight of the global post-pandemic recovery rests entirely on the US consumer. Europe is in no place to shoulder any of that load, and China is not running its 2010 playbook. Markets think they have this call down pat, hence the recent rally to new highs. At a +21x forward multiple on the S&P 500, they’d better be right.

#3: The end of the “Pandemic Peace Dividend”.As long as the virus was circulating around the world and there was no proven vaccine, no country could sensibly consider large scale military action. First, putting thousands of people in close contact would spread the disease. Second, every medical professional was needed to treat virus patients and that included military doctors and nurses. Now that vaccinations are underway, countries and non-state actors can inoculate military personnel and execute Clausewitz’s “diplomacy by other means”.

Summary: geopolitical risk is always out there, but last year it was forced as far to the sidelines as it has been in decades or perhaps even centuries. How, if, or when it comes to the fore is always hard to predict, but 2021 – 2022’s odds of a geopolitical shock are materially worse than 2020’s.

#4: Tech regulation/index concentrations.Large Cap Tech + AMZN, FB, GOOG and TSLA is 38 percent of the S&P 500 and 35 percent of total US equity market cap. The industry faces a very unfriendly US/global regulatory environment at the moment, even if stock prices say otherwise.

China presents a cautionary tale on this count. The MSCI China Index is down 16 percent from its February highs. Leading that decline are Tencent and Alibaba, which are each down 17 percent and have a collective 29 percent weighting in the index. Note that they are not really underperforming. Rather, the Chinese government’s sudden increase in tech sector regulatory scrutiny is hitting overall investor confidence.

Summary: markets are relying on Big Tech’s phenomenal profitability to fully offset the business risk created by stronger regulation, but that has not worked in China so it’s valid to ask if it will insulate US tech stocks once Washington gets in gear on this issue.

#5: Winning ideas may not be the “right” ideas in terms of index-based investing.For example, which would you rather own for the next 2 years:

-

The virtual currency that begins with “B”, or a major global stock market index like the S&P 500, MSCI EAFE or Emerging Markets?

-

A newly IPO-ed Coinbase, or JP Morgan? Even though Coinbase is very profitable, it won’t be in the S&P 500 for a year due to seasoning requirements. JPM is 1.4 pct of the index right now.

-

PayPal, or the S&P large cap Financials sector? PYPL is just 0.9 pct of the S&P; Financials are 11.2 pct.

-

A basket of late-stage VC-funded disruptive tech companies, or the NASDAQ 100 (QQQs)?

Virtual currencies alone are a $2 trillion parking lot, and the recent NFT craze shows this ecosystem can still pull in fresh capital. We’ll likely have a record year for US IPOs, but none of them will hit the S&P 500 until 2022 at the earliest. In other words, a lot of financial assets can do well without the S&P seeing any benefit since correlations typically remain low during the middle part of an economic recovery. In fact, capital may leave US stock indices looking for greener pastures elsewhere.

Pulling all this together: the goal today was to present 5 reasonable bear cases and let you decide how likely they might be. From our perspective, they’re all valid to some degree and others (like US tax policy) may not be as discounted in stock prices as we think. Ultimately, we’re still positive on US stocks because we believe fiscal and monetary policy plus corporate earnings leverage offsets these potential outcomes sufficiently to make the risk-reward calculus favorable. Put another way, the expected return from policy actions is greater than the expected return of the risk factors we’ve outlined today.

Tyler Durden Sat, 04/10/2021 - 10:20

Categorías: Blogs y opiniones de economia en ingles

US Homes "Snatched Up Right Away" As Market Drained Of Supply

US Homes "Snatched Up Right Away" As Market Drained Of Supply

There has been a clear shift in market mood and sentiment ever since the COVID pandemic: whereas the Fed smashed mortgage rates to record lows, and the federal government delayed the foreclosure wave via forbearances. On top of this, socio-economic chaos in major metro areas resulted in an urban exodus like never before.

This has led to a shortage in supply and a fierce bidding war that almost half of US homes are selling within a week of hitting the market, according to a new Redfin report.

Daryl Fairweather, Redfin's chief economist, said, "new listings are getting snatched up right away."

"First it was, the faster you move, the more of an edge you have. Now if you don't put in an offer five days after it's listed, you're not going to be considered at all," said Fairweather

In the report, he said the housing market "is more competitive than we've ever seen it." More or less, today's housing market is a speculative frenzy powered by super cheap borrowing rates (thanks Powell) and ultra-low supply.

Fairweather indicates the red hot demand can't continue forever and warns: "we're nearing a peak in terms of how fast demand and prices can grow."

Besides record-low mortgage rates and tight supply, the implosion of liberal cities, spiraling into an epidemic of violence following last year's defund the police movement, resulted in one of the most significant urban exoduses of city dwellers. This has fueled housing markets in suburbs and rural communities, pushing prices up even further.

With builders unable to build fast enough, more and more prospective homebuyers fight over a smaller pie of listed homes. Redfin data shows the average US home is selling above the listing price as a fierce bidding war has ensued in the spring housing market cycle. In areas like Northern California, homes sell for 107% of the asking prices.

Source: Bloomberg{kind=link}

Buyers have become desperate and offer to wave inspections, pay seller costs, and throw in extra perks to lock in a deal.

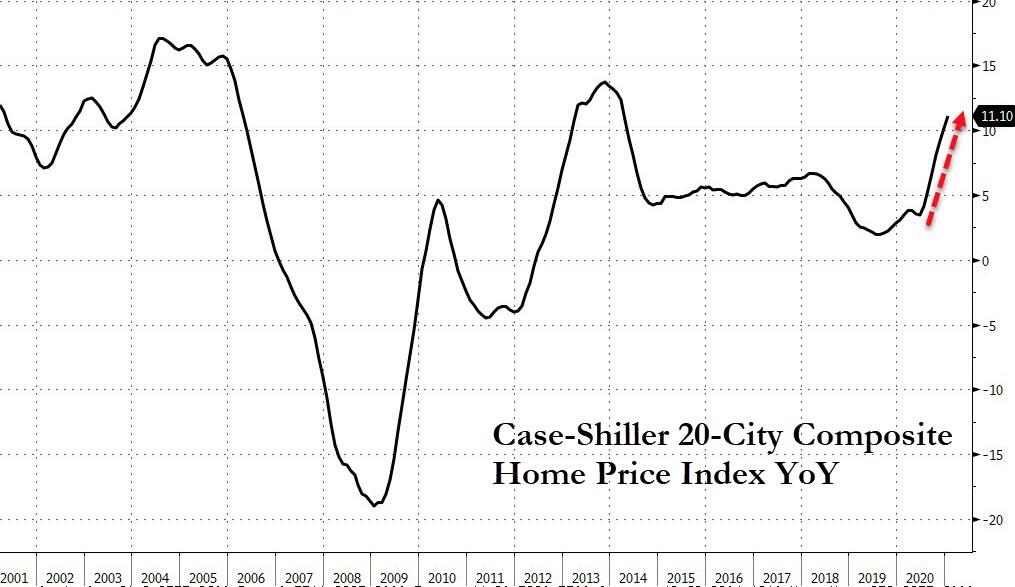

The speculative frenzy has ignited US home prices in 20 major cities, up a shocking 11.10% year-over-year.

{kind=link}

This is the fastest YoY rise since March 2014.

Away from the 20 major cities, prices are rising even faster, up 11.22% - the fastest YoY price appreciation since Feb 2006...

{kind=link}

Jim Black, a broker who works in Worcester, Massachusetts, told Bloomberg many houses "are selling in a couple of days with multiple offers, sometimes 10% over list price."

"It's as crazy as it has ever been," Black said.

There have been reports of buyers in Atlanta writing personal letters and offering gifts of as much as $2,000 just for accepting their offer, said Andrew Kolodey, a Redfin agent.

Allison Health, a realtor with Baltimore-based Northrop Realty, said the housing market is absolutely on fire, and low inventories in the Baltimore Metropolitan Area have unleashed bidding wars that have resulted in soaring home prices. She said the only way to secure a deal is to put in a contract well above the listing price, offer to pay closing costs and wave inspections.

Readers may recall, one home in Toronto saw 112 showings and received more than 17 offers.

While Redfin's chief economist Fairweather warns the housing market is possibly overheating, there are early indications homebuyer demand could soon be waning. We've seen this story before, and it never ends well.

Tyler Durden Sat, 04/10/2021 - 09:50

Categorías: Blogs y opiniones de economia en ingles

Frederick Forsyth Says Government Has Launched "Campaign Of Mass Fear" Against British Public

Frederick Forsyth Says Government Has Launched "Campaign Of Mass Fear" Against British Public

Authored by Paul Joseph Watson via Summit News,

Iconic author Frederick Forsyth has accused the UK government of waging a “campaign of mass fear” against the British public by using psychological methods to ensure compliance with lockdown that resemble those used against East Berliners in the 1960’s.

{kind=link}

Forsyth was responding to an article published in the Telegraph which exposed the “covert tactics” being used by the British government to frighten the public into complying with COVID regulations.

The article quoted a retired NHS consultant clinical psychologist who warned that there was “growing concern within my field about using fear and shame as a driver of behaviour change.”

Gary Sidley and 46 of his colleagues wrote to the British Psychological Society to express “concerns about the activities of Government-employed psychologists … in their mission to gain the public’s mass compliance with the ongoing coronavirus restrictions.”

The letter states that the UK government is deploying “covert psychological strategies – that operate below the level of people’s awareness – to ‘nudge’ citizens to conform to a contentious and unprecedented public health policy.”

Commenting on the article, Frederick Forsyth, author of classic thrillers such as The Day of the Jackal and The Odessa File, wrote to the Telegraph to express his alarm about how the British public had been terrorized by lockdown propaganda.

“Congratulations to the Telegraph and Gordon Rayner for revealing that the campaign of mass fear that reduced a once brave nation to trembling terror was deliberately organised to secure obedience to the policy of lockdown,” wrote Forsyth.

“I have only once before seen anything like it. This was when I was posted to East Germany in 1962. Such a brainwashing tactic was employed to frighten East Berliners into believing that the Berlin Wall was a defensive measure to protect them from tiny West Berlin, and that the Stasi was their guardian. The wall was of course an instrument of enslavement.”

“I never thought that the government of a country whose uniform I once wore with such pride would sink so low. Those responsible should be identified without delay and ousted from all office over us.”

* * *

Brand new merch now available! Get it at https://www.pjwshop.com/

* * *

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown. Also, I urgently need your financial support here.

Tyler Durden Sat, 04/10/2021 - 09:20

Categorías: Blogs y opiniones de economia en ingles

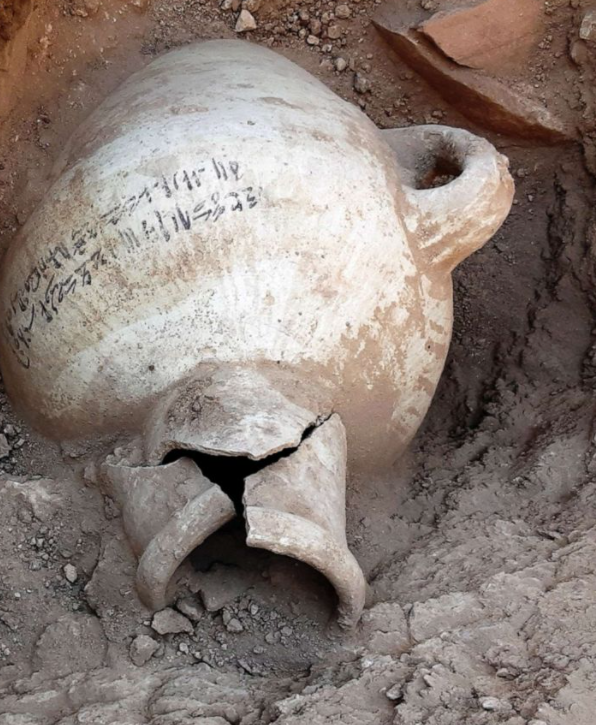

"Lost Golden City" Rises From The Egyptian Sand

"Lost Golden City" Rises From The Egyptian Sand

Archaeologists unearthed a 3,000-year-old city in Egypt known by some as the "lost golden city." The ancient city's actual name is called "The Rise of Aten," which is located in the desert outskirts of Luxor, a city on the east bank of the Nile River in southern Egypt.

{kind=link}

"The Egyptian mission under Dr. Zahi Hawass found the city that was lost under the sands," the excavation team told CBS News. "The city is 3,000 years old, dates to the reign of Amenhotep III, and continued to be used by Tutankhamun and Ay."

{kind=link}

Hawass said the discovery is one of the "largest" ancient cities ever found in Egypt that dates back to the golden age when pharaohs ruled the land.

{kind=link}

The excavation crew began operations in September 2020, between the temples of Ramses III and Amenhotep III near Luxor, and within weeks, they uncovered parts of the city.

"Within weeks, to the team's great surprise, formations of mud bricks began to appear in all directions," he said.

Amenhotep III, one of Egypt's most powerful pharaohs, ruled between 1391 to 1353 BC.

"The discovery of this lost city is the second most important archaeological discovery since the tomb of Tutankhamun," Betsy Brian, professor of Egyptology at Johns Hopkins University in Baltimore, US, said.

Brian said the ancient city "gives us a glimpse into the ancient Egyptians' life" when Egypt was at its most prosperous.

{kind=link}

Following seven months of excavations, the team has uncovered multiple neighborhoods, and within, it has found a complete bakery with ovens and storage containers. The team also found administrative and residential districts.

"What they unearthed was the site of a large city in good condition of preservation, with almost complete walls, and with rooms filled with tools of daily life," Hawass said.

CBS noted the team also found pottery vessels, jewelry, scarab beetle amulets, and bricks with the seal of Amenhotep III.

{kind=link}

The excavation team's next objective is to "uncover untouched tombs filled with treasure," said Hawass.

Only further excavations will uncover what lead to the demise of the ancient city more than 3,000 years ago.

Video: Inside "Lost" Egyptian City

You never know what the sands of Egypt will hide - apparently a lost city that may rewrite history books.

Tyler Durden Sat, 04/10/2021 - 08:45

Categorías: Blogs y opiniones de economia en ingles

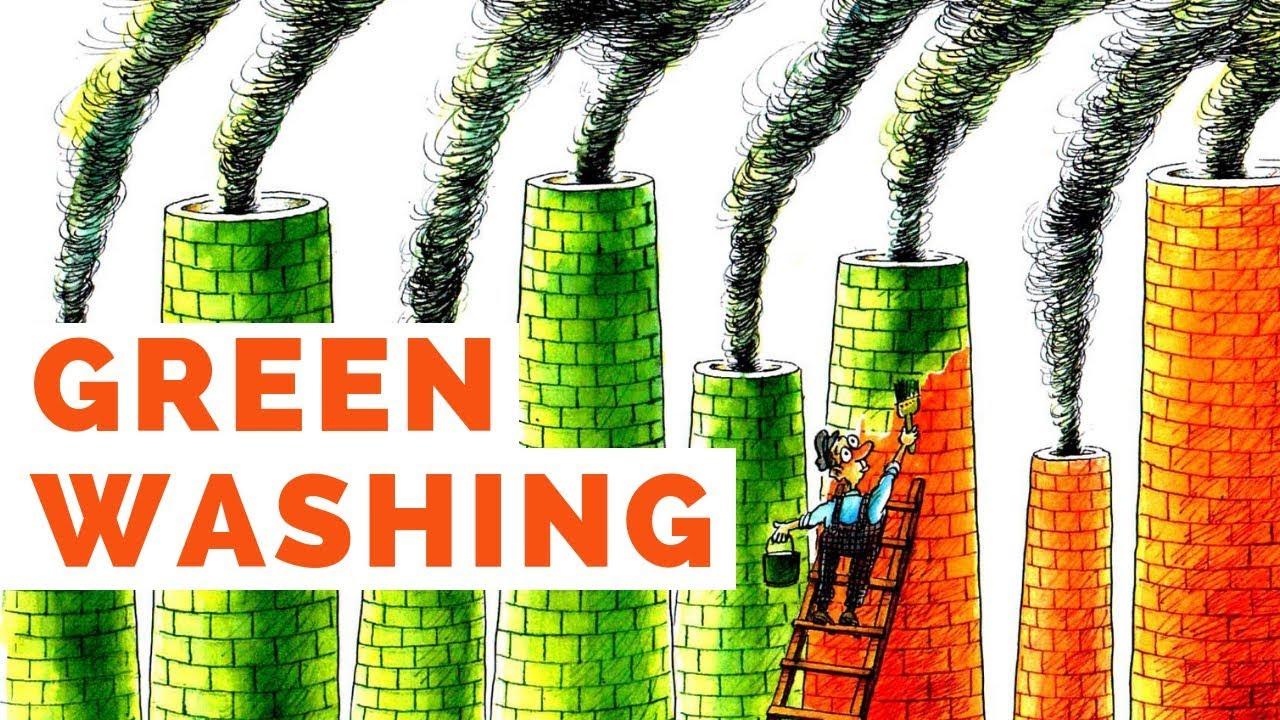

Greenwashing The Ugly Truth: Box-Ticking ESG Investment Stupidity Exposed

Greenwashing The Ugly Truth: Box-Ticking ESG Investment Stupidity Exposed

Authored by Bill Blain via MorningPorridge.com,

“Give a man a fish and he will eat for a day, teach him to fish and he will destroy the planet...”

Seaspiracy is a shocking, flawed, yet critical film. It should set the market thinking about what sustainability really means, addressing how we skirt the real issues on climate change and environmental degredation. It should provide a much-needed kick up the a**e to box-ticking ESG investment stupidity.

It’s the weekend, so I am allowed to have a rant...

If you haven’t yet watched Seaspiracy, the Netflix shock documentary about the global fishing industry – then I suggest you do. It is an impact film. It might just be the most important documentary you watch this year. If you think the global environment matters, and you aren’t watching what’s happening to the oceans, then you are looking in the wrong direction.

{kind=link}

Ostensibly Seaspiracy is a shock-doc about how the fishing industry is destroying the planet. For the purposes of the Morning Porridge, it’s about the exposure of greenfoolery on a massive scale – waking us up to difference between what we think we know, and what we don’t. We unquestioningly accept fishing is good and wholesome, enabling bogus ideas and concepts that claim to support the environment, but which are little more than environmental, and often financial rip-offs.

Seaspiracy should set you thinking about the scale of damage being done to the global environment and economy that we are doing nothing about in the Oceans. It is going to shake many long-held opinions about focus, direction and sanctions within the ethical investment industry. Basically, forget saving the planet if we don’t save the oceans first.

Last night I sat down to watch Seaspiracy. I’d already read about it. It was not easy viewing.

There have been a lash of accusations that interviewees have been taken out of context, their quotes misused and manipulated to make them appear foolish. Many of the facts it glibly presents have been questioned. It’s been made in the style of Michael Moore on crack-cocaine, spiced up with exaggerated naivety and fantastically done shocking cinematography. Call me a cynic, but it feels like the young director Ali Tabrizi, a Brit, carefully choregraphed his run-ins with authorities for best dramatic effect. For every positive comment about the film, there is dissent.

None of that matters. It is still a film you must watch.

What matters is the film raises some very real, troubling and difficult questions for an investment community besotted with buzzword concepts like sustainability, environmental protection and social responsibility. If you are stressing about planting a tree every time you fill up the Range Rover – as I do – then you are probably worrying about all the wrong things. The environmental damage inflicted on the oceans is a magnitude higher than everything happening on land – and we are doing nothing about it.

If we want to clear CO2 from the atmosphere – then protecting the oceans will be the way to do it.

I’ve written before about the need for ocean clean-up and protecting it from plastic pollution. As a sailor, I’ve seen plastic floating in the English Channel and Irish Seas. I’ve joined beach-clean ups. I’ve refused plastic straws and use metal drinks bottles. And I’ve been pretty much sating my conscience and doing zero good.

The reality is the bulk of plastic pollution at sea is from the fishing industry. 46% of the plastic floating in the oceans is discarded fishing nets. (I should know that; I got one wrapped around my keel a few years ago, it took lumps out the trailing edge.) Plastic straws are 0.03%, but it’s good for the middle classes to feel they are doing something. Mrs Middle-Class Putney will stop her kids drinking SunnyD with its little plastic straw, tell her friends to join her in saving the planet, while feeding her little darlings fish fingers caught by the Atlantic Dawn – check out the trawler from hell.

We really do need to think about the oceans and the effect we are having on them. 70% of the planet’s surface is Ocean. Its role in CO2 absorption is increasingly understood to dwarf rain forests. It’s an incredibly complex biosphere. It relies on whale poo to fertilise plankton, which sequester carbon before sinking to the bottom, aided by the movement of marine like up and down the water column creating powerful downdrafts. It’s a delicate organic machine we barely understand. Yet we rip it up on a daily basis – as the documentary makes absolutely clear.

Some of the filming is shocking – like the butchery of whales in Japan and The Faroes. However unpalatable watching whales being slaughtered is, Mr Tabrizi gives a thoughtful Faroe whaler time to make ethical points questioning the moral equivalency of the killing of a single porpoise versus the death of a 1000 chickens. It’s a very moot point – man is an omnivore, we kill animals as part of our diet. There are sustainability implications around the killing of a wild animal for versus the costs of raising and then slaughtering thousands of battery chickens.

But what’s going on in the oceans beggars belief. 2.7 trillion fish being hoovered up from the seas every year, much of it being “by-catch” which is thrown away dead. Bottom crawling trawlers ripping up 3.9 bln acres of sea-bed and everything living on and off it every year. The unsustainability of “sustainable” fish farming and the waste it produces. The destruction of coastal mangroves to factory farm shrimps and prawns. The social costs of fishing slavery. It’s all there in the film.

Then there is the money being made from sticking “dolphin friendly” or “sustainably caught” on tins of fish. None of it means anything. Spokesmen for the organisations that validate such claims were interviewed and said some foolish things – which are used in the film. They were unfairly ambushed – but that’s not the point. There is no guarantee that tin of tuna didn’t cost dozens of dolphins and hundreds of sharks their lives.

Claims that current industrial scale fishing is “sustainable” were conclusively debunked by the programme. Sustainability is a buzzword glibly used around the globe to greenwash environmental destruction. It’s been very easy for the markets to persuade itself its doing good because it uses terms like sustainable. That is not enough.

{kind=link}

I’ve gotten myself into trouble a number of times over ESG investment, Corporate Social Responsibility and Sustainability.

I was asked to take part in an ESG panel last year, but the invite evaporated after I sent the organisers some Morning Porridges criticising the basis of ESG investment, suggesting it has become a series of formulaic, bureaucratic box-ticking excuses for ill-considered investment decisions.

I’m happy to say it again. Whole swathes of the “ethical investment overlay” are anything but. They dominate investment committee thinking. Much of it is overkill, stifling debate and discouraging questions. To me, it’s dead simple: invest in companies where the management understands and commits to doing good.

I got into particular trouble with one fund last week after I suggested BAT might deserve a second look. Yes, tobacco is bad, and smoking kills. But, smoking is a personal choice, BAT pays its farmer suppliers in developing nations fairly, supports them to farm sustainably, and is investing heavily in less unhealthy smoking options. The fund manager unsubscribed – offended I would suggest it.

If you are sitting on a bank’s ESG desk, or a CSR investment committee, or claim to care about climate, the environment, social or animal welfare…. then you really need to keep learning about it in the broad sense. I think Seaspiracy is a flawed film, it looks and feels staged, and it’s clear some of it is out of context – but it’s still a critically important documentary that should set you thinking…

This morning’s rant is not about the small fishermen we see on TV plying their trade from quaint Cornish harbours, but the industrial pillage of the sea by massive factory trawlers. Yet, the local guys will no doubt suffer as the middle classes turn on them.

This morning I “trawled” the internet for reviews of the programme. It was fascinating – I came across well written articles from popular mass-market magazines like Hello and Marie-Claire that chock full of quotes from readers who’ve watched Seaspiracy saying things like: “have given up eating fish with immediate effect”, “fishing is responsible for climate change”, “we’ve been kept in the dark”, or “the world is ignorant to the truth”. My daughter – who demanded I watch it – isn’t going to eat fish ever again.

It’s a film that is already having an impact.

Personally – I live near to a brilliant fishmonger, and I know they collect direct from small local boats. But I might not be buying frozen prawns again, and I’ve gone right off the sashimi-quality tuna that’s sustained us through lockdowns.

Tyler Durden Sat, 04/10/2021 - 08:10

Categorías: Blogs y opiniones de economia en ingles

Northern Ireland Violence Worst In Decades; Fears Of "The Troubles" Return

Northern Ireland Violence Worst In Decades; Fears Of "The Troubles" Return

Sporadic rioting across several cities and towns in Northern Ireland has resulted in at least 70 injured police officers. The violence is some of the worst in decades as governments in Belfast, London, and Dublin have denounced the social unrest, according to BBC.

{kind=link}

Unrest broke out a week ago amid rising post-Brexit tensions. A more immediate catalyst was a decision a few weeks back by public prosecutors not to charge anyone with alleged breaches of COVID regulations at an IRA funeral that sparked unionist outrage.

The unrest began on Mar. 29 in a small city in Northern Ireland called Londonderry. Since then, protests and rioting have spread to Belfast, Carrickfergus, Ballymena, and Newtownabbey.

Source: BBC{kind=link}

The rioting has mainly been loyalist youths hurling petrol bombs, bricks, and fireworks at police officers and their vehicles. But on Wednesday, the chaos intensified into sectarian fighting over a peace wall in west Belfast that separates Protestant loyalist communities from predominantly Catholic nationalist communities who want unification with Ireland.

Source: BBC{kind=link}

Irish nationalist and pro-British loyalists clashed at the peace wall, igniting fears about the revival of the "The Troubles," a dark period when both sides fought a low-level war against each other late 1960s to the late 1990s. The conflict claimed the lives of nearly 3,600 people as nationalists and unionists fought. At times, the conflict spilled over into the Republic of Ireland, England, and mainland Europe.

"We are gravely concerned by the scenes we have all witnessed on our streets," the compulsory coalition, led by rival pro-Irish Catholic nationalists and pro-British Protestant unionists, wrote in a statement.

"While our political positions are very different on many issues, we are all united in our support for law and order and we collectively state our support for policing," the statement continued.

Northern Ireland's assistant chief constable, Jonathan Roberts, said several hundred people on both sides of the wall were responsible the violence, and he accused outlawed paramilitary groups of inciting it.

"We saw young people participating in serious disorder and committing serious criminal offenses, and they were supported and encouraged, and the actions were orchestrated by adults at certain times," he said.

"Last night was at a scale we haven't seen in Belfast or further afield in Northern Ireland for a number of years," Roberts said.

In a tweet, the Police Federation for Northern Ireland called for calm, saying, "These are scenes we hoped had been confined to history."

Violence on both sides of the interface at Lanark Way now. Calm is needed on BOTH sides of the gates before we are looking at a tragedy. These are scenes we hoped had been confined to history. @NIPolicingBoard @NIOgov @PoliceServiceNI pic.twitter.com/SjtWq10UFo

— Police Federation for Northern Ireland (@PoliceFedforNI) April 7, 2021Tensions in Northern Ireland have been growing since the United Kingdom voted to leave the European Union, creating a potential trade border between the British-ruled north and the Republican of Ireland in the south. The lack of a trade border has been the main reason why a peace deal has remained in place since 1998.

Under the Northern Ireland Protocol of the Brexit withdrawal agreement, a trade border was placed around the Irish Sea with goods entering Northern Ireland from mainland Britain subject to European Union checks. This move infuriated unionists, who have accused London of abandoning them.

The British and Irish prime ministers held talks this week, while the Biden administration was concerned about the ongoing violence.

British Prime Minister Boris Johnson said, "The way to resolve difference is through dialogue, not violence or criminality."

Meanwhile, Ireland's foreign minister, Simon Coveney, has called on local leaders to ease tensions.

As Philip McGowan writes, these protests have not suddenly appeared out of nowhere, but neither are they all about Brexit and the Northern Ireland Protocol. They are the culmination of a complex mix of change and a deep-rooted resistance to it, and an ingrained political and social inertia particular to this place. It’s true that some things in Northern Ireland have changed enormously for the better on a day-to-day basis since the signing of the Good Friday Agreement in 1998, but look behind that surface improvement and quickly you will see evidence that other things have not changed that much at all. Meanwhile, our politics has atrophied as it has polarised in the intervening decades.

The point remains, however, that there are huge social issues here that are not being addressed by politicians: 120,000 children are living in poverty in Northern Ireland and more than 40,000 people are on the social housing waiting list – a rise of 10% in the past year. Between 1998 and 2014, more people died by suicide in Northern Ireland than were killed during the Troubles (and of those there were 3,600), and that devastating statistic keeps growing. An endemic lack of social and economic opportunity has been added to the load carried by a new generation, who are the children of the children of the Troubles.

Could things spiral backwards? Yes, if there is a continued absence of political leadership willing to take the forward steps needed to stabilise a volatile situation. Northern Ireland has never needed better political leadership than it does right now. It also needs the UK and Irish governments to accept and adhere to their responsibilities as set out in the Agreement, because the Agreement is the roadmap to resolve Northern Ireland’s status as we move away from violence and toward peace. For the Agreement to have been overwhelmingly supported across all of this island (71% in Northern Ireland, 94% in the Republic of Ireland) was a remarkable feat. Stagnation politics since then has nurtured complacency about exactly what was achieved in 1998. Peace is an extraordinarily brittle entity. Democracy is a daily commitment to hearing and addressing the issues in front of us as they arise. It needs constant vigilance and it needs tolerance. It doesn’t always produce the desired result, so it also requires compromise. But in terms of the problems that face us, we already have the solution in our hands: we worked it out after decades of pain and loss, but we still need to implement all the Agreement’s commitments.

Northern Ireland needs leaders who accept the complexities at play in this new reality: our grave social deprivation and economic disadvantages; our shared peripheral status for decades; and the political inertia that defines our situation. All of this means economic and social problems are not being addressed, which, in turn, plays into the hands of criminal and gang elements happy to keep communities at the mercy of irresponsible and divisive forces who, I’m afraid, haven’t gone away.

Tyler Durden Sat, 04/10/2021 - 07:35

Categorías: Blogs y opiniones de economia en ingles

Escobar: Ukraine Redux - War, Russophobia, & Pipelineistan

Escobar: Ukraine Redux - War, Russophobia, & Pipelineistan

Authored by Pepe Escobar via The Asia Times,

The deep state/NATO combo's using Kiev to start a war to bury Nord Stream 2 and German-Russian relations...

{kind=link}

A Ukrainian serviceman walks in a fortified position at the front line with Russia-backed separatists not far away, in Avdiivka, Donetsk region, on April 5, 2021. Photo: AFP

Ukraine and Russia may be on the brink of war – with dire consequences for the whole of Eurasia. Let’s cut to the chase, and plunge head-on into the fog of war.

On March 24, Ukrainian President Zelensky, for all practical purposes, signed a declaration of war against Russia, via decree No. 117/2021.

{kind=link}

Ukrainian President Volodymyr Zelensky speaks during a joint press conference with European Council President in Kiev on March 3, 2021. Photo: AFP / Sergey Dolzhenko

The decree establishes that retaking Crimea from Russia is now Kiev’s official policy. That’s exactly what prompted an array of Ukrainian battle tanks to be shipped east on flatbed rail cars, following the saturation of the Ukrainian army by the US with military equipment including unmanned aerial vehicles, electronic warfare systems, anti-tank systems and man-portable air defense systems (MANPADS).

More crucially, the Zelensky decree is the proof any subsequent war will have been prompted by Kiev, debunking the proverbial claims of “Russian aggression.” Crimea, since the referendum of March 2014, is part of the Russian Federation.

It was this (italics mine) de facto declaration of war, which Moscow took very seriously, that prompted the deployment of extra Russian forces to Crimea and closer to the Russian border with Donbass. Significantly, these include the crack 76th Guards Air Assault Brigade, known as the Pskov paratroopers and, according to an intel report quoted to me, capable of taking Ukraine in only six hours.

It certainly does not help that in early April US Secretary of Defense Lloyd Austin, fresh from his former position as a board member of missile manufacturer Raytheon, called Zelensky to promise “unwavering US support for Ukraine’s sovereignty.” That ties in with Moscow’s interpretation that Zelensky would never have signed his decree without a green light from Washington.

{kind=link}

On March 8, 2021, US Defense Secretary Lloyd Austin speaks during observance of International Women’s Day in the East Room of the White House in Washington, DC. Photo: AFP / Mandel Ngan

Controlling the narrativeSevastopol, already when I visited in December 2018, is one of the most heavily defended places on the planet, impervious even to a NATO attack. In his decree, Zelensky specifically identifies Sevastopol as a prime target.

Once again, we’re back to 2014 post-Maidan unfinished business.

To contain Russia, the US deep state/NATO combo needs to control the Black Sea – which, for all practical purposes, is now a Russian lake. And to control the Black Sea, they need to “neutralize” Crimea.

If any extra proof was necessary, it was provided by Zelensky himself on Tuesday this week in a phone call with NATO secretary-general and docile puppet Jens Stoltenberg.

{kind=link}

NATO Secretary-General Jens Stoltenberg gives a press conference at the end of a NATO Foreign Ministers’ meeting at the Alliance’s headquarters in Brussels on March 24, 2021. Photo: AFP / Olivier Hoslet

Zelensky uttered the key phrase: “NATO is the only way to end the war in Donbass” – which means, in practice, NATO expanding its “presence” in the Black Sea. “Such a permanent presence should be a powerful deterrent to Russia, which continues the large-scale militarization of the region and hinders merchant shipping.”

All of these crucial developments are and will continue to be invisible to global public opinion when it comes to the predominant, hegemon-controlled narrative.

The deep state/NATO combo is imprinting 24/7 that whatever happens next is due to “Russian aggression.” Even if the Ukrainian Armed Forces (UAF) launch a blitzkrieg against the Lugansk and Donetsk People’s Republics. (To do so against Sevastopol in Crimea would be certified mass suicide).

In the United States, Ron Paul has been one of the very few voices to state the obvious:

“According to the media branch of the US military-industrial-congressional-media complex, Russian troop movements are not a response to clear threats from a neighbor, but instead are just more ‘Russian aggression.’”

What’s implied is that Washington/Brussels don’t have a clear tactical, much less strategic game plan: only total narrative control.

And that is fueled by rabid Russophobia – masterfully deconstructed by the indispensable Andrei Martyanov, one of the world’s top military analysts.

A possibly hopeful sign is that on March 31, the chief of the General Staff of the Russian Armed Forces, General Valery Gerasimov, and the chairman of the Joint Chiefs of Staff, General Mark Milley, talked on the phone about the proverbial “issues of mutual interest.”

Days later, a Franco-German statement came out, calling on “all parties” to de-escalate. Merkel and Macron seem to have gotten the message in their videoconference with Putin – who must have subtly alluded to the effect generated by Kalibrs, Kinzhals and assorted hypersonic weapons if the going gets tough and the Europeans sanction a Kiev blitzkrieg.

{kind=link}

French President Emmanuel Macron speaks as German Chancellor Angela Merkel looks on after a German-French Security Council video conference at the Elysee Palace in Paris, on February 5, 2021. Photo: AFP / Thibault Camus

The problem is Merkel and Macron don’t control NATO. Yet Merkel and Macron at least are fully aware that if the US/NATO combo attacks Russian forces or Russian passport holders who live in Donbass, the devastating response will target the command centers that coordinated the attacks.

What does the hegemon want?As part of his current Energizer bunny act, Zelensky made an extra eyebrow-raising move. This past Monday, he visited Qatar with a lofty delegation and clinched a raft of deals, not circumscribed to LNG but also including direct Kiev-Doha flights; Doha leasing or buying a Black Sea port; and strong “defense/military ties” – which could be a lovely euphemism for a possible transfer of jihadis from Libya and Syria to fight Russian infidels in Donbass.

Right on cue, Zelensly meets Turkey’s Erdogan next Monday. Erdogan’s intel services run the jihadi proxies in Idlib, and dodgy Qatari funds are still part of the picture. Arguably, the Turks are already transferring those “moderate rebels” to Ukraine. Russian intel is meticulously monitoring all this activity.

A series of informed discussions – see, for instance, here and here – is converging on what may be the top three targets for the hegemon amid all this mess, short of war: to provoke an irreparable fissure between Russia and the EU, under NATO auspices; to crash the Nord Steam 2 pipeline; and to boost profits in the weapons business for the military-industral complex.

So the key question then is whether Moscow would be able to apply a Sun Tzu move short of being lured into a hot war in the Donbass.

On the ground, the outlook is grim. Denis Pushilin, one of the top leaders of the Lugansk and Donetsk people’s republics, has stated that the chances of avoiding war are “extremely small.” Serbian sniper Dejan Beric – whom I met in Donetsk in 2015 and who is a certified expert on the ground – expects a Kiev attack in early May.

The extremely controversial Igor Strelkov, who may be termed an exponent of “orthodox socialism,” a sharp critic of the Kremlin’s policies who is one of the very few warlords who survived after 2014, has unequivocally stated that the only chance for peace is for the Russian army to control Ukrainian territory at least up to the Dnieper river. He stresses that a war in April is “very likely”; for Russia war “now” is better than war later; and there’s a 99% possibility that Washington will not fight for Ukraine.

On this last item at least Strelkov has a point; Washington and NATO want a war fought to the last Ukrainian.

Rostislav Ischenko, the top Russian analyst of Ukraine whom I had the pleasure of meeting in Moscow in late 2018, persuasively argues that, “the overall diplomatic, military, political, financial and economic situation powerfully requires the Kiev authorities to intensify combat operations in Donbass.

“By the way,” Ischenko added, “the Americans do not give a damn whether Ukraine will hold out for any time or whether it will be blown to pieces in an instant. They believe they stand to gain from either outcome.”

Gotta defend EuropeLet’s assume the worst in Donbass. Kiev launches its blitzkrieg. Russian intel documents everything. Moscow instantly announces it is using the full authority conferred by the UNSC to enforce the Minsk 2 ceasefire.

In what would be a matter of 8 hours or a maximum 48 hours, Russian forces smash the whole blitzkrieg apparatus to smithereens and send the Ukrainians back to their sandbox, which is approximately 75km north of the established contact zone.

In the Black Sea, incidentally, there’s no contact zone. This means Russia may send out all its advanced subs plus the surface fleet anywhere around the “Russian lake”: They are already deployed anyway.

{kind=link}

Russian President Vladimir Putin looks on as Novator Design Bureau director-general Farid Abdrakhmanov and Deputy Defense Minister Alexei Krivoruchko shake hands during a signing ceremony for government contracts in Alabino, Moscow region, Russia. on June 27, 2019. Photo: AFP / Alexei Druzhinin / Sputnik

Once again Martyanov lays down the law when he predicts, referring to a group of Russian missiles developed by the Novator Design Bureau: “Crushing Ukies’ command and control system is a matter of few hours, be that near border or in the operational and strategic Uki depth. Basically speaking, the whole of the Ukrainian ‘navy’ is worth less than the salvo of 3M54 or 3M14 which will be required to sink it. I think couple of Tarantuls will be enough to finish it off in or near Odessa and then give Kiev, especially its government district, a taste of modern stand-off weapons.”

The absolutely key issue, which cannot be emphasized enough, is that Russia will not (italics mine) “invade” Ukraine. It doesn’t need to, and it doesn’t want to. What Moscow will do for sure is to support the Novorossiya people’s republics with equipment, intel, electronic warfare, control of airspace and special forces. Even a no-fly zone will not be necessary; the “message” will be clear that were a NATO fighter jet to show up near the frontline, it would be summarily shot down.

And that brings us to the open “secret” whispered only in informal dinners in Brussels, and chancelleries across Eurasia: NATO puppets do not have the balls to get into an open conflict with Russia.

One thing is to have yapping dogs like Poland, Romania, the Baltic gang and Ukraine amplified by corporate media on their “Russian aggression” script. Factually, NATO had its collective behind unceremoniously kicked in Afghanistan. It shivered when it had to fight the Serbs in the late 1990s. And in the 2010s, it did not dare fight the Damascus and Axis of Resistance forces.

When all fails, myth prevails. Enter the US Army occupying parts of Europe to “defend” it against – who else? – those pesky Russians.

That’s the rationale behind the annual US Army DEFENDER-Europe 21, now on till the end of June, mobilizing 28,000 soldiers from the US and 25 NATO allies and “partners.”

This month, men and heavy equipment pre-positioned in three US Army depots in Italy, Germany and the Netherlands will be transferred to multiple “training areas” in 12 countries. Oh, the joys of travel, no lockdown in an open air exercise since everyone has been fully vaccinated against Covid-19.

Pipelineistan uber allesNord Stream 2 is not a big deal for Moscow; it’s a Pipelineistan inconvenience at best. After all the Russian economy did not make a single ruble out of the not yet existent pipeline during the 2010s – and still it did fine. If NS2 is canceled, there are plans on the table to redirect the bulk of Russian gas shipments towards Eurasia, especially China.

{kind=link}

Connecting German infrastructure for Nord Stream 2 is in place. In this handout photo released February 4, 2020, by the press service of Eugal, a view shows the Eugal pipeline, in Germany. The Eugal pipeline, which will receive gas from Nord Stream 2 in the future, has reached full pumping capacity, and the second line of the pipeline has been introduced. Photo: AFP / Press-service of Eugal / Sputnik

In parallel, Berlin knows very well that canceling NS2 will be an extremely serious breach of contract – involving hundreds of billions of euros; it was Germany that requested the pipeline to be built in the first place.

Germany’s energiewende (“energy transition” policy) has been a disaster. German industrialists know very well that natural gas is the only alternative to nuclear energy. They are not exactly fond of Berlin becoming a mere hostage, condemned to buy ridiculously expensive shale gas from the hegemon – even assuming the egemon will be able to deliver, as its fracking industry is in shambles. Merkel explaining to German public opinion why they must revert to using coal or buy shale from the US will be a sight to see.

As it stands, NATO provocations against NS2 proceed unabated – via warships and helicopters. NS2 needed a permit to work in Danish waters, and it was granted only a month ago. Even as Russian ships are not as fast in laying pipes as the previous ships from Swiss-based Allseas, which backed down, intimidated by US sanctions, the Russian Fortuna is making steady progress, as noted by analyst Petri Krohn: one kilometer a day on its best days, at least 800 meters a day. With 35 km left, that should not take more than 50 days.

Conversations with German analysts reveal a fascinating shadowplay on the energy front between Berlin and Moscow – not to mention Beijing. Compare it with Washington: EU diplomats complain there’s absolutely no one to negotiate with regarding NS2. And even assuming there would be some sort of deal, Berlin is inclined to admit Putin’s judgment is correct: the Americans are “not agreement-capable.” One just needs to look at the record.

Behind the fog of war, though, a clear scenario emerges: the deep state/NATO combo using Kiev to start a war as a Hail Mary pass to ultimately bury NS2, and thus German-Russian relations.

At the same time, the situation is evolving towards a possible new alignment in the heart of the “West”: US/UK pitted against Germany/France. Some Anglosphere exceptionals are certainly more Russophobic than others.

The toxic encounter between Russophobia and Pipelineistan will not be over even if NS2 is completed. There will be more sanctions. There will be an attempt to exclude Russia from SWIFT. The proxy war in Syria will intensify. The hegemon will go no holds barred to keep creating all sorts of geopolitical harassment against Russia.

What a nice wag-the-dog op to distract domestic public opinion from massive money printing masking a looming economic collapse. As the empire crumbles, the narrative is set in stone: it’s all the fault of “Russian aggression.”

Tyler Durden Sat, 04/10/2021 - 07:00

Categorías: Blogs y opiniones de economia en ingles

Daily Mail Exposes Hunter Biden Bombshells After 'Tell-All' Book Holds Back

Daily Mail Exposes Hunter Biden Bombshells After 'Tell-All' Book Holds Back

With Hunter Biden on a serious image rehabilitation tour - a 'tell all' book combined with television interviews from friendly outlets designed to invoke pity over the First Son's crack and hooker habits, the Daily Mail is now telling the rest of the story regarding the contents of his abandoned laptop after Hunter admitted it 'certainly' could be his in a Sunday interview with CBS.

If you've seen the laptop photos which leaked last October, you can probably stop here. The Mail did spare us from blurred pictures of Hunter's wang, along with several sex tapes released by exiled Chinese billionaire Guo Wengui.

After obtaining a copy of the hard drive, DailyMail.com commissioned top cyber forensics experts Maryman & Associates to analyze its data and determine whether the laptop's contents were real.

The firm's founder, Brad Maryman, is a 29-year FBI veteran Supervisory Special Agent who served as an Information Security Officer and founded its first computer forensics lab. -Daily Mail

The Mail obtained over 100,000 text messages, 154,000 emails and over 2,000 photos which were verified by top forensics experts, which reveal that Joe 'became a punching bag for Hunter's drug-fueled rants,' and 'paid his grandchildren's bills when Hunter had drained his bank accounts with prostitutes and crack cocaine.'

{kind=link}

{kind=link}

Hunter appeared to be obsessed with making and starring in porn films with prostitutes, videos and photos on his laptop show.

The hard drive contains hundreds of pictures of naked women and naked selfies of Hunter, as well as dozens of videos.

Hunter photographed and filmed himself, often with two prostitutes at a time, in explicit videos that he then posted on adult website Pornhub under the username 'RHEast'.

Hunter filmed himself with the women from his laptop webcam, sometimes shooting at different angles using an iPad and cell phone. -Daily Mail

{kind=link}

{kind=link}

The Mail also promises to release more Hunter laptop drops:

Hunter's laptop is a pandora's box of shocking revelations, explicit photos and intimate communications.In the following days, DailyMail.com will publish more shocking stories from Hunter's laptop, including:

- How Hunter blew hundreds of thousands on prostitutes, drugs and luxury cars, leaving him scrambling to avoid jail for $320k in unpaid taxes

- How five members of the Biden family have been to rehab for drug or alcohol abuse – and a stunning admission by Joe to his son

- The OTHER Biden family member planning to buy and cook crack, after falling into the disastrous addiction with Hunter

- Hunter's unconventional and unlikely relationship with his well-known psychiatrist

- The whispered bedroom conversation with a prostitute caught on Hunter's webcam, in which he confesses he had a previous laptop stolen – by Russians for blackmail

The president's son left his 2017 MacBook Pro laptop at a Wilmington, Delaware computer repair shop in April 2019 and never returned for it.

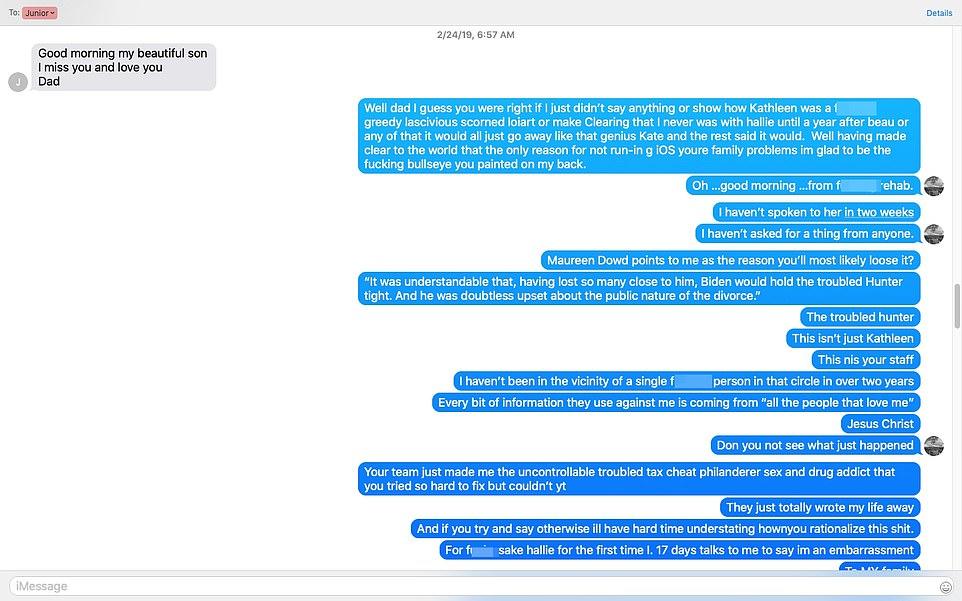

In one text exchange between Joe and Hunter, Joe wrote "Good morning my beautiful son. I miss you and love you. Dad." To which a petulant Hunter raged at his father for "having made clear to the world that the only reason for not [running for president is your] family problems im glad to be the f***ing bullseye you painted on my back."

In another exchange, Hunter complained that Joe's advice not to defend himself publicly during his expensive divorce with ex-wife Kathleen Biden, or his affair with his brother's widow Hallie, had backfired.

"Your team just made me the uncontrollable troubled tax cheat philanderer sex and drug addict that you tried so hard to fix but couldn't yt. They just totally wrote my life away," Hunter wrote, adding "If you dont run [for president] ill never have a chance at redemption."

{kind=link}

Joe replied with a promise to run, though hinted that maybe Hunter should probably stop getting so dramatic over texts due to them being a target.

"I'll run but I need you,' he wrote. 'H[allie] is wrong. Only focus is recovery. Nothing else... When you can and feel like it call. Positive my text etc a target. Love."

Joe Biden would announce his run for president two months later - during which Hunter's laptop contents would leak, defeating the purpose of rehabilitating the crack addict's image.

Joe would again warn Hunter not to spill his life story over text, writing "Be careful what you text. Likely I'm being hacked."

Read the rest of the report here.

And then there's this other thing Hunter failed to mention in his book or his interviews...

“Hunter Biden purchased a handgun illegally, he lied on a federal background check..”

“The question is will David Chipman arrest the President’s son? If he doesn’t... how exactly are you obligated to follow these rules?”

Great questions, Tucker. pic.twitter.com/mNbYAwzOHN

Categorías: Blogs y opiniones de economia en ingles

24 World Leaders Call For More Globalism In Wake Of Pandemic

24 World Leaders Call For More Globalism In Wake Of Pandemic

Authored by Steve Watson via Summit News,

Twenty four world leaders have signed a letter calling for more globalism to combat future pandemics, citing the the coronavirus outbreak as an opportunity to consign nationalism to the dustbin of history.

{kind=link}

UK prime minister Boris Johnson, German chancellor Angela Merkel, and French president Emmanuel Macron are the leading figures behind the pledge, with 21 other heads of state signing the letter.