Se encuentra usted aquí

Blogs y opiniones de economia en ingles

Minnesota Black School Choice Movement "Explicitly Rejects" Narrative That America Is Racist

Minnesota Black School Choice Movement "Explicitly Rejects" Narrative That America Is Racist

Authored by GQ Pan via The Epoch Times,

A school choice movement aimed at serving Minnesota’s black community has vowed to tackle the notion that the United States is a racist nation, saying such narratives are “structured to undermine the lives of black Americans.”

{kind=link}

The newly founded organization, TakeCharge Minnesota, describes itself on its website as seeking to “inspire and educate the black community and other minority groups in the Twin Cities to take charge of their own lives, the lives of the families and communities, as citizens fully granted to them in the Constitution.”

“We acknowledge that racist people exist in the country, but explicitly reject the notion that the United States of America is a racist country,” the organization states.

“We also denounce the idea that the country is guilty of systemic racism, white privilege and abhor the concept of identity politics and the promotion of victimhood in minority communities.”

According to the website, the organization is headed by Kendall Qualls, a health care executive and Army veteran. He was also a Republican contender for Minnesota’s 3rd Congressional District, which remains occupied by incumbent Democrat Rep. Dean Phillips following the 2020 election.

“People who helped me in life were black and white, rich and poor, male and female, gay and straight,” Qualls said in March in an interview with the Minnesota Reformer.

“Americans help each other when they see someone trying to better their lot in life, and most Americans don’t put a filter on it based on skin color.”

“To me, it’s insulting to hear that black people can’t get ahead because of systemic racism,” he told the outlet.

TakeCharge Minnesota also lists five core doctrines it wants to promote, including the one that says “restoring the two-parent black family should be a priority both locally and nationally,” a belief in opposition to that of the Black Lives Matter organization, which calls for an end to the “Western-prescribed nuclear family structure.”

“The nuclear family is the bedrock of any society and it has been decimated and ignored in the Black community for five decades,”

TakeCharge Minnesota declares, adding that raising children in a marriage is “the best way to reduce poverty, combat inequality, and develop socially productive children.”

School choice programs have gained popularity in recent years among the nation’s black families, plenty of which have been benefited from the expansion of high-quality public school alternatives, especially those in low-income neighborhoods. An October 2020 survey by conservative think tank Manhattan Institute found that between 51 and 62 percent of all respondents supported state funding of charter schools. This support was higher for black respondents in all states and ranged from 58 to 67 percent.

Tyler Durden Fri, 05/14/2021 - 21:00

Categorías: Blogs y opiniones de economia en ingles

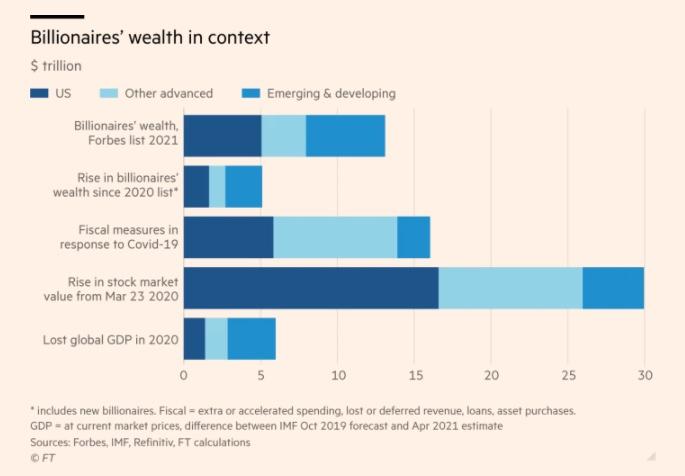

COVID 'Billionaire Boom' Has Seen Aggregate Wealth More Than Double To $13 Trillion

COVID 'Billionaire Boom' Has Seen Aggregate Wealth More Than Double To $13 Trillion

America's billionaire class is now the second most "bloated" in the world after...Sweden?

If that sounds strange, it's just one example of how the global explosion in wealth is impacting the world in unexpected ways.

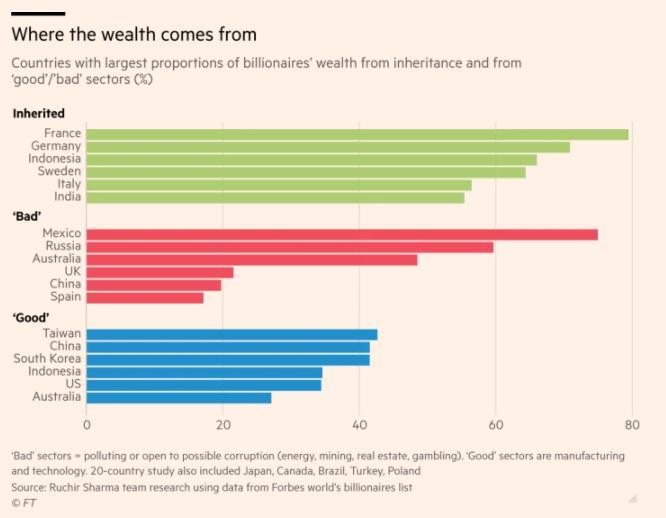

This is according to research by FT contributing editor Ruchir Sharma, who has been tracking the global rise of billionaires over the past decade while devising metrics to allow for an apples-to-apples comparison. In this way, Sharma has been able to determine whether individual billionaires derived their wealth from "good" sources ("clean" industries like tech or manufacturing) vs. "bad" billionaires who inherited their wealth, or built it in more corrupt corners of the economy, like real-estate or natural resources (primarily oil).

{kind=link}

The tremendous surge in prices of assets from stocks, to homes, to used cars to collectibles has benefited the wealthy most of all. Last year, China led the world in billionaire-creation, with 238 billionaires created, roughly one every 36 hours, bringing the country's total to 626. In aggregate, billionaire wealth climbed to $13 trillion from $5 trillion in the span of a year.

Sharma highlighted wealth inequality across a group of developed and developing economies by comparing total billionaire wealth to GDP, the annual aggregate value of goods and services produced in a given economy.

{kind=link}

Source: FT

The surge in equity valuations over the past year accrued primarily to "good" billionaires, as Sharma characterized them (though of course AOC and those like her believe that there are no 'good' billionaires, and that billionaires' existence is a 'policy error'). "'Good' billionaires still rule the class," he said.

{kind=link}

Sharma also found that national reputation had little bearing on billionaire wealth accumulation over the past year, which saw billionaires in left-leaning France see their total assets jump from 11% to 17% of French GDP. Meanwhile, in conservative Britain, billionaires share of wealth remained flat.

While the population of billionaires exploded in China (something that may have informed Beijing's crackdown on its tech billionaires) inequality in the US actually decreased slightly, perhaps due to the stimulus that stuffed bank accounts of working-class Americans and those who lost work.

{kind=link}

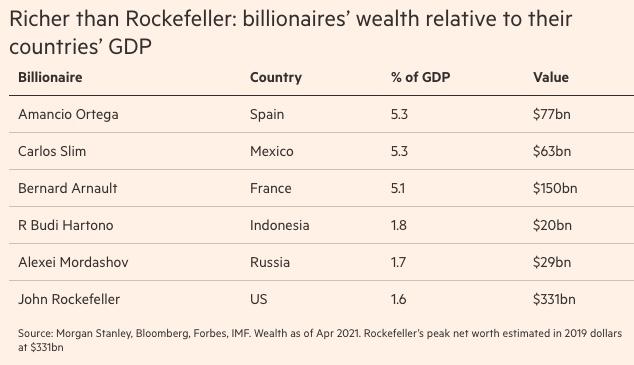

While Jeff Bezos gets a lot of hate as a modern-day robber-baron, Sharma points out that Bezos' wealth is actually smaller than the Rockefeller fortune in its heyday.

The scale of American wealth is also worth considering in context. As the world’s richest man, Jeff Bezos’s $177bn may seem mind-boggling. But at 0.8 per cent of GDP, it is far from Rockefeller wealth, which at his peak amounted to 1.6 per cent of GDP. There are, however, many real Rockefellers in other countries, including five in Sweden, two each in Mexico, France, India and Indonesia, and one each in Spain, Canada, Italy and Russia. Top of the Rockefellers list are self-made fashion king Amancio Ortega of Spain, telecom titan Carlos Slim of Mexico and Bernard Arnault of France; each has a fortune equivalent to more than 5 per cent of his home country’s GDP.

But there are some billionaires who are more wealthy than Rockefeller, using a ratio of their total wealth to the annual GDP of their respective home economy.

{kind=link}

One notable recent development: In the emerging world, Russia has long held the title of world capital for "bad" billionaires. But last year, it ceded that title to Mexico. The 2020 surge took Mexico's share of "bad" billionaire wealth up to 75%, leaving Russia second worst among the big developing nations, at 60%, or 3x the average for emerging nations.

{kind=link}

The backlash to the "billionaire class" typically increases in correlation with the pace of their wealth accumulation. Whatever happens next in terms of the evolution of public attitudes toward the concentration of wealth in family fortunes will depend on where the boom goes from here.

Tyler Durden Fri, 05/14/2021 - 20:40

Categorías: Blogs y opiniones de economia en ingles

Buchanan: Are The Halcyon Days Over For Joe Biden?

Buchanan: Are The Halcyon Days Over For Joe Biden?

On taking the oath of office, Jan. 20, Joe Biden may not have realized it, but history had dealt him a pair of aces.

The COVID-19 pandemic had reached its apex, infecting a quarter of a million Americans every day. Yet, due to the discovery and distribution of the Pfizer and Moderna vaccines, the incidence of infections had crested and was about to turn sharply down.

By May, the infection rate had fallen 80%, as had the death toll.

Thanks to the Operation Warp Speed program driven by President Donald Trump, the country made amazing strides in Biden’s first 100 days toward solving the major crises he inherited: the worst pandemic since the Spanish flu of 1918-1919 and the economic crash it had engendered.

{kind=link}

But Biden’s pace car has hit the wall.

Where economists had predicted employment gains of a million new jobs in April, the jolting figure came in at about a fourth of that number.

One explanation: The $300-a-week in bonus unemployment checks the Biden recovery plan provides may have been a sufficient inducement for workers to stay home until their benefits ran out.

Workers might reasonably ask: Why go back to work when we can take the summer off, with full unemployment, plus $300 a week?

After the crushing jobs report came the inflation figure from April.

Consumer prices had risen 4.2%, the highest rate in a dozen years.

April’s combination of inflation and near-stagnant job growth recalls the “stagflation” of the Jimmy Carter years, which led to the Democratic rout of 1980 at the hands of Ronald Reagan.

And while we may not be suffering from stagflation just yet, the present symptoms in the U.S. economy are certainly consistent with it.

The bad news from the inflation front also sent the Dow and other markets plunging and raised fears of future Fed intervention to raise interest rates to choke off the inflation.

Moreover, rising prices, driven in part by our historic federal deficits, stiffened the spines of Republicans in their resistance to Biden’s $2.3 trillion infrastructure and jobs program, his $1.8 trillion in added domestic spending and his $4 trillion in taxes to pay for it all.

Sen. Mitch McConnell came out of Wednesday’s White House meeting with Biden to say that any tampering with the Trump tax cuts crosses a “red line” for him and Senate Republicans.

The odds on Biden getting any of his taxes has just fallen dramatically. And he may be forced to come down closer to the GOP proposal if he hopes to get any of his infrastructure package through.

At present, Biden does not have a single sure Republican vote for his spending proposals — and even some Democrats in the evenly divided Senate oppose his plans for social spending and higher taxes.

Added to this economic news was a stunning ransomware attack on Colonial Pipeline, which feeds fuel to states from Texas to New Jersey.

Within days, the shutdown of the pipeline had induced panic buying of gas at the pumps, resulting in a sweeping closure of gas stations from Delaware to the Gulf Coast.

As alarming as the ransomware attack was, more alarming is what it portends if cybercriminals abroad can, with the flick of a switch, inflict such instant damage on the U.S. economy.

If cybercriminals can pull this off, what can our adversaries, with their sophisticated and superior weapons of cyberwarfare, not do to the United States?

But that was not the end of the bad news for Biden this week.

A shooting war erupted between Hamas and Israel after a dispute over ownership of homes in East Jerusalem led to clashes between Arab protesters and Israeli police at the al-Aqsa Mosque on the Temple Mount.

The clashes brought barrages of over 1,000 rockets directed at Israeli towns and cities including Jerusalem and Tel Aviv. The Ben Gurion International Airport was forced to shut down.

Those who believed Trump’s Abraham Accords, where Israel was recognized by the UAE, Bahrain and Morocco, had ensured a more tranquil future suddenly seemed to have been as wrong as previous generations of optimists.

Today, even inside Israel, Arabs and Jews, both Israeli citizens, are battling in the streets.

Meanwhile, in Kabul, three bombs outside a high school killed 50 people and wounded scores more, many of them teenage girls — a portent of what may be coming when the Americans and allied troops are gone from the country by the 20th anniversary of 9/11.

But the defining crisis of the Biden presidency may be the crisis on America’s southern border, where another 170,000 illegal immigrants entered the country in April after an equally high number in March.

{kind=link}

That is an annual rate of 2 million people walking into our country uninvited, the advance guard of a Third World invasion that will change the character and composition of the United States.

The America we grew up in is disappearing — without our consent.

Tyler Durden Fri, 05/14/2021 - 20:20

Categorías: Blogs y opiniones de economia en ingles

Demand For Active Shooter Insurance Soars As Post-Pandemic America Reopens

Demand For Active Shooter Insurance Soars As Post-Pandemic America Reopens

As the US returns to some normalcy after a year of the virus pandemic, demand for active shooter insurance has surged following a spate of mass shootings across the country, according to Reuters.

Tarique Nageer, Terrorism Placement Advisory Leader at Marsh, the world's largest insurance broker, reports client requests for active shooter policies have surged by 50% year on year in the past six weeks. These policies cover victim lawsuits, building repairs, legal fees, medical expenses, and trauma counseling.

Chris Kirby, head of political violence cover at insurer Optio, said active shooter policy rates have doubled for some clients due to recent mass shootings. He wasn't specific about what industries the policy rates jumped.

Other insurer brokers are saying hospitals, retail businesses, schools, universities, restaurants, and places of worship are purchasing the special insurance with coverage ranging between $1 million and $75 million.

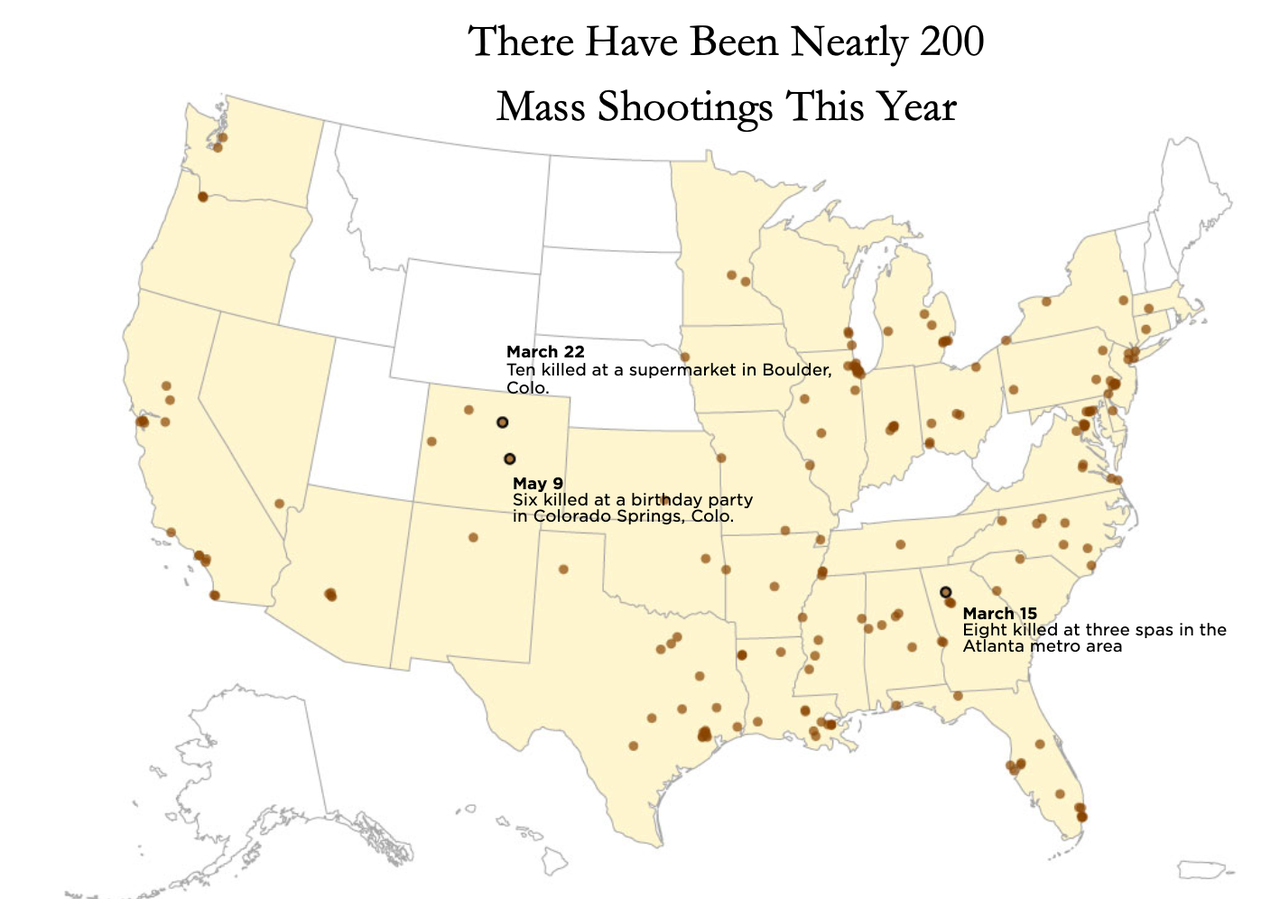

A shocking report from Gun Violence Archive, a non-profit research group, says in the first 132 days of 2021, there were 200 mass shootings in the US, averaging more than one per day.

{kind=link}

Hart Brown, senior vice president of R3 Continuum, a crisis management consultancy, said violence shifted from public spaces into homes in 2020. He said demand for his company's services is up by 20%, adding that the reopening of businesses in a post-pandemic world has brought violence back to the workplace.

"The environment that was created by the pandemic, with the social distancing, the lockdown, and so forth and the compounding stressors is really what's driving much of the violence that we see right now," Brown said.

We've noted forced lockdowns and economic depression with high unemployment would result in a lapse in American's mental health. A recent survey by Kaiser Family Foundation provides more concrete evidence Americans are experiencing high levels of anxiety or depressive disorders.

President Biden has called the wave of mass shootings a "national embarrassment," and his only solution is to ban military-style "assault" weapons and large-capacity ammunition magazines. What is that exactly going to solve when civilians own more than 390 million guns. Even with a potential ban, people are still going to make ghost guns and 3D-printed weapons.

A mental health crisis rages in America as mass killings are out of control. Whatever happened to Biden's "unity" calls?

Tyler Durden Fri, 05/14/2021 - 20:00

Categorías: Blogs y opiniones de economia en ingles

Biden Admin Sued Over Alleged Discrimination Against Certain Bar And Restaurant Owners

Biden Admin Sued Over Alleged Discrimination Against Certain Bar And Restaurant Owners

Authored by Janita Kan via The Epoch Times,

A Texas cafe owner is taking the Biden administration to court over alleged discrimination that prevents him from receiving COVID-19 relief grants because of his race and gender.

Philip Greer, the owner of Greer’s Ranch Café, has sued the Small Business Administration (SBA), alleging that he would miss out on receiving a Restaurant Revitalization Fund grant because the federal law requires the agency to prioritize awarding grants to women and racial minorities.

Section 5003 of the American Rescue Plan Act requires the agency prioritize women, veterans, and socially and economically disadvantaged business owners applying to receive a portion of the $28.6 billion appropriated to create the Restaurant Revitalization Fund.

According to Small Business Administration regulations, socially disadvantaged individuals are individuals “who have been subjected to racial or ethnic prejudice or cultural bias within American society because of their identities as members of groups and without regard to their individual qualities. The social disadvantage must stem from circumstances beyond their control.”

Meanwhile, economically disadvantaged individuals are considered to be those whose “ability to compete in the free enterprise system has been impaired due to diminished capital and credit opportunities as compared to others in the same or similar line of business who are not socially disadvantaged.”

Greer, who is represented by America First Legal and Texas Public Policy Foundation, argues that such policy actively excludes entire classes of Americans not mentioned in the “priority” group who are also suffering significant financial losses caused by the pandemic.

“The Small Business Administration lurches America dangerously backward, reversing the clock on American progress, and violating our most sacred and revered principles by actively and invidiously discriminating against American citizens solely based upon their race and sex. This is illegal, it is unconstitutional, it is wrong, and it must stop,” the lawsuit states (pdf).

The lawsuit calls on the court to block the enforcement of any policy that would discriminate against certain classes of Americans, arguing that this would be necessary to “promote equal rights under the law for all American citizens and promote efforts to stop racial discrimination.”

“The decision from the Biden Administration to determine eligibility and priority for restaurant relief funds based upon race is profoundly illegal and morally outrageous,” AFL President and former Trump adviser Stephen Miller said in a statement. “It is an affront to our laws, our Constitution, and our most dearly-held values.”

SBA administrator Isabella Casillas Guzman was also named in the suit as a defendant. The SBA’s press office said it is their policy to not comment on pending litigation when reached for comment.

{kind=link}

Small Business Administration chief Isabel Guzman attends a Cabinet meeting with President Joe Biden in the East Room of the White House in Washington, D.C., on April 1, 2021. (ANDREW CABALLERO-REYNOLDS/AFP/Getty Images)

On Thursday, the SBA announced that they had received 147,000 applications from women, veterans, and socially and economically disadvantaged business owners who requested a total of $29 billion in relief funds.

“The numbers show that we’ve been particularly successful at reaching the smallest restaurants and underserved communities that have struggled to access relief. These businesses are the pillars of our nation’s neighborhoods and communities,” Guzman said in a statement.

Tyler Durden Fri, 05/14/2021 - 19:40

Categorías: Blogs y opiniones de economia en ingles

Bill Gross's 44-Year-Old Successor Quits To Spend Time With Kids "While They Still Like Me"

Bill Gross's 44-Year-Old Successor Quits To Spend Time With Kids "While They Still Like Me"

In the wake of Friday's underwhelming jobs number, the media has been hungry for stories about people quitting prestigious jobs - like the Goldman MD who reportedly quit after making a fortune off dogecoin.

The latest example comes courtesy of Bloomberg, which reported last night that the man who succeeded legendary 'Bond King' Bill Gross as the head of global bonds at Janus Henderson (which oversees some $400 billion) has abruptly quit the firm to 'spend more time with family'.

{kind=link}

And while that familiar line is closely associated with departing executives looking to obscure the unsavory nature of their departure, in Nick Maroutsos' case, it's not only genuine, but the subject of a profiled by Bloomberg as a prominent example of how "the YOLO economy" - as the NYT recently termed it - is inspiring high-paid employees to "take risks" and "embrace life".

Already wealthy at 44, Maroutsos said he planned to take time off from his career - at least a year, he said - to travel the country with his young children "while they still like me."

At just 44, Nick Maroutsos has one of the most elite jobs in money management: the head of global bonds at Janus Henderson Investors, a firm that oversees some $400 billion.

But he’s walking away from it in October to consider his second act and hit the road for cross-country trips with his young children while - as he put it - "they still like me."

Maroutsos, best known as the successor to former bond king Bill Gross, says he hasn’t quite decided what he’ll do next. But whatever it is, it will involve following his 14-year-old daughter to lacrosse tournaments around the country and spending time with his wife and two other young children.

The bond head is joining the legions of well-off Americans who are casting off the shackles of their day jobs, spurred by a “life-is-short” mentality galvanized by a year of effective hibernation. It’s just one of the unexpected outcomes of the pandemic era, which has empowered some to jettison corporate life.

"I will work again at some point," he said in a phone interview on Wednesday. "In a year’s time, I will probably resurface in some capacity. I’m looking at things potentially outside of fixed income. But I’m not good enough at other things, like either music or cooking, to do them."

After receiving his master's at UCLA, Maroutsos started at PIMCO (the firm that Gross built) as an analys before leaving in 2007 to launch Kapstream Capital, his own fixed-income investing firm that was acquired by Janus eight years later, not long after Gross left/was fired by PIMCO over what colleagues complained was increasingly erratic behavior.

Despite the public legal fallout and disturbing stories about Gross's often antagonistic personal behavior, Gross took a top job at Janus where he sought to burnish his legacy. Unfortunately, a few wrong-way bets in Gross's unconstrained strategy fund precipitated Gross's retirement from the industry, though he has continued to trade, recently announcing a bet against GameStop.

After Gross's retirement, Maroutsos and his team mixed the various strategies he employed with some of their own. The biggest fund that Maroutsos helps oversee is the Janus Henderson Short Duration Income ETF, which has a market capitalization of almost $3 billion and total return of 2.5% since the since pandemic lockdowns started in mid-March 2020. He is also co-manager of the Absolute Return Income Opportunities Fund, which has seen a 2.4% return over the past year.

As for his decision to follow Gross out the door, Maroutsos said the pandemic gave him a lot of time to think about "where I want to be in the next 10 years". And ultimately he decided to follow Gross out the door.

"I had reached a point in my career where I had been in fixed-income markets for the last 20 years, and was looking at what the future holds," he says. "I was looking at my own career progress and decided now is as good a time as any to take a step back and hit the reset button."

"The pandemic has caused everybody to sort of reevaluate not just their career paths, but goals in life," Maroutsos added. "I spent a lot of time thinking about that and where I want to be in the next 10 years. I’m quite fortunate to be able to do this at my age."

Perhaps Maroutsos is simply hoping to avoid the acrimony that has famously afflicted Gross and his family?

Tyler Durden Fri, 05/14/2021 - 19:20

Categorías: Blogs y opiniones de economia en ingles

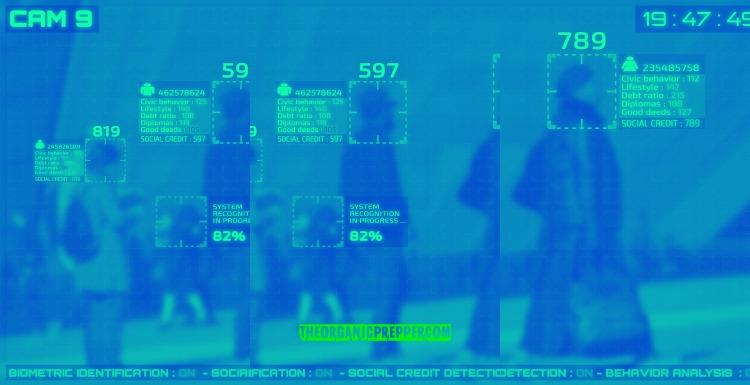

A Society Based On The Social Credit System Is Closer Than You Think

A Society Based On The Social Credit System Is Closer Than You Think

Authored by Robert Wheeler via The Organic Prepper blog,

The social credit system took yet another step forward—this time, from Down Under. Under the guise of a welfare crackdown, Australia moved 25,000 people onto a cashless card system that restricts non-essential purchases.

Aussie welfare recipients only access to funds is via a cashless debit card{kind=link}

Australia’s government forced thousands of welfare recipients on to Centrelink, a cashless debit card. Under a massive expansion of the plan and new Federal Budget, immigrants have no access to most kinds of welfare for four years after attaining residency. However, the most crucial aspect of Centrelink is Aussies cannot use the cards for gambling, alcohol, or cigarettes. Only necessities like groceries and food can be purchased with the cards.

East Kimberley and Goldfields in Western Australia, Ceduna in South Australia, and the Bundaberg-Hervey Bay region of Queensland trialed the cards beginning in 2016. Under this scheme, 80 percent of welfare recipients’ Centrelink payment will go directly to the card rather than a bank account. That is supposed to keep recipients from wasting the welfare on unnecessary items.

Treasurer Josh Frydenberg unveiled the plan to make the scheme permanent in the trial locations. The plan also includes extending it to 25,000 people in the Northern Territory and Cape York.

The Australian government’s recent budget includes a $30 million package to “upskill” people at the trial sites and offer a jobs fund to boost employment opportunities. The plan includes funding for drug and alcohol rehabilitation services in the cashless debit card locations as well.

Don’t be so quick to judge. This plan is not what it seemsMany people will rejoice, happy that the “welfare queens” can no longer lie about drinking beer and smoking while others toil away at work to pay for those luxuries. However, the truth is that this scheme is much more insidious than it may at first appear.

No one wants to pay higher taxes so that those who do not want to work can squander welfare benefits. But knee-jerk reactions that lend support to schemes like this will ultimately lead to a social credit system, UBI, and financial allotmentt entirely controlled by the government. Implementation of these schemes is likely not only in Australia but across the world.

What is a social credit system?For those unaware of what a “social credit system” is, Business Insider’s article summarizes it well. In the article “China has started ranking citizens with a creepy ‘social credit’ system — here’s what you can do wrong, and the embarrassing, demeaning ways they can punish you,” Alexandra Ma writes:

The Chinese state is setting up a vast ranking system that will monitor the behavior of its enormous population and rank them all based on their “social credit.”

The “social credit system,” first announced in 2014, aims to reinforce the idea that “keeping trust is glorious and breaking trust is disgraceful,” according to a government document.

The program is due to be fully operational nationwide by 2020 but is being piloted for millions of people across the country already. The scheme will be mandatory.

At the moment, the system is piecemeal — some are run by city councils, others are scored by private tech platforms which hold personal data.

Like private credit scores, a person’s social score can move up and down depending on their behavior. The exact methodology is a secret — but examples of infractions include bad driving, smoking in non-smoking zones, buying too many video games, and posting fake news online.

That system is coming to the United States and the rest of the world soonBrandon Turbeville mentions the coming merger of the social credit and UBI systems here:

While most Americans have scarcely noticed their descent into a police state, they are quick to dismiss the idea that such a system could be implemented in the land they still perceive to be free. However, all the moving parts are in place in the United States. They only need to come together to form the Social Credit System here.

And they ARE coming together.

Social media is a critical method of judging “social scores.” Mainly because of the willful posting of social media users on virtually every aspect of their lives. Users give away the most personal and intimate details of their lives and do so without charge.

This data is extremely useful to governments who monitor and store the freely acquired information. Whether it is political opinions, pictures of yourself and your food, or private conversations, that data is sent directly to the corporation. Respective governments then have access to that data via various means and put that data to good use.

In this article, Daisy offers insight into the data collection in the United States.

People seem blind to what is comingThe UBI, of course, is an old idea and one so old that philosopher/activist Bertrand Russell even discussed it. The UBI, cashless society, and social credit system will soon combine to create the largest, most effective police state ever known to man. A society where any criticism or resistance of the government will result in an immediate shut down of credits and the trespasser being frozen entirely out of society.

It may feel good now, but soon it won’t. When it no longer does, well, you were warned.

Tyler Durden Fri, 05/14/2021 - 19:00

Categorías: Blogs y opiniones de economia en ingles

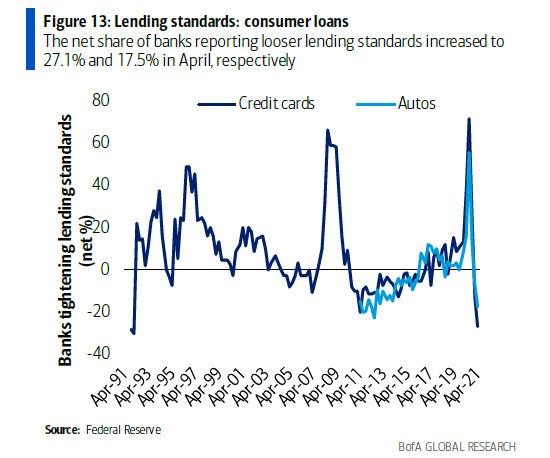

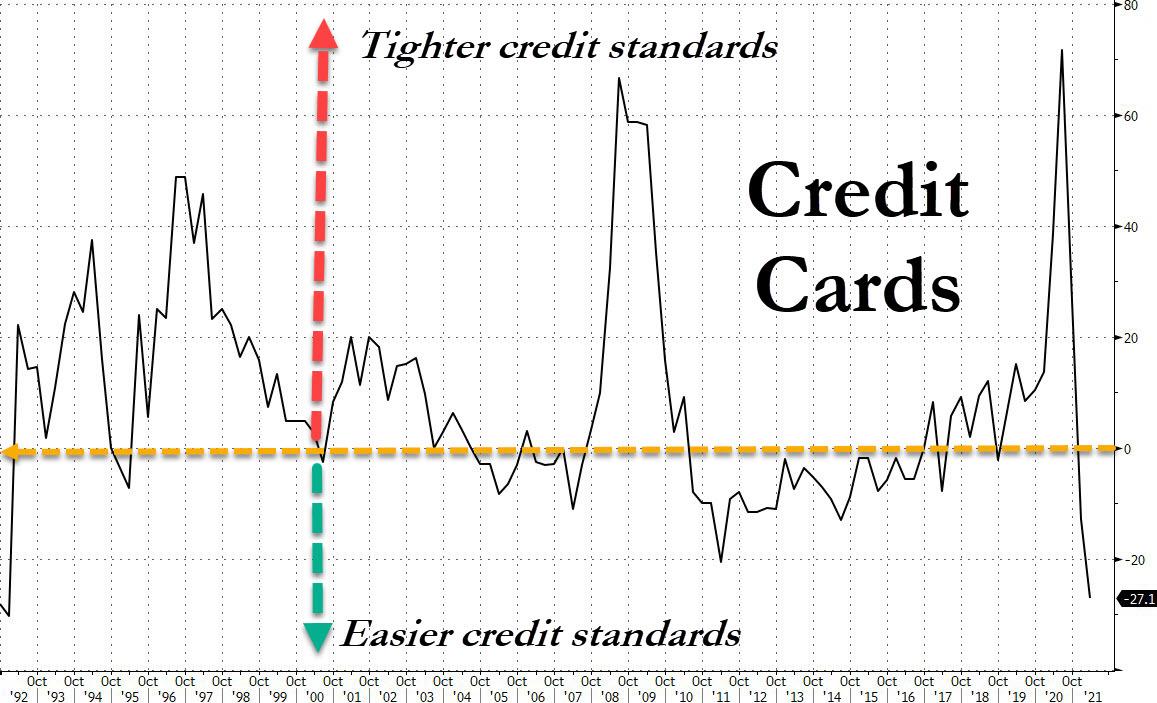

JPMorgan, Others To Unveil Credit Cards For People With No Credit Scores

JPMorgan, Others To Unveil Credit Cards For People With No Credit Scores

After a year of clamping down on new credit card, mortgage, and commercial loan issuance in the aftermath of the COVID pandemic, US commercial banks are planning to issue credit cards to people with no credit scores.

WSJ reports JPMorgan, Wells Fargo, and US Bancorp, and others will extend credit to people who cannot obtain a credit card. Instead of using credit scores to vet an applicant, these banks will use other factors, including checking or savings accounts, to increase their chances of being approved.

{kind=link}

Sources told WSJ the pilot program to give credit cards to people with no credit would begin this year. There was no mention of the start date.

This comes as consumer lending standards have never been this loose since around the time records began in 1991, while auto loans are similarly among the loosest on record.

{kind=link}

And here is a chart looking at just the record loose print in credit card standards:

{kind=link}

As explained by WSJ's source, the pilot program aims at "individuals who don't have credit scores but who are financially responsible."

According to Fair Isaac Corp., the creator of FICO credit scores, some 53 million American adults don't have traditional credit scores. Many are often rejected by banks and have to use payday loans, a costlier way to finance money.

A 2015 report by the Consumer Financial Protection Bureau said Black and Hispanic adults in the US have higher probabilities of lacking credit scores than White or Asians. So perhaps the new pilot program by the fat cats on Wall Street opens the credit spigot to minorities.

More details about the program include JPMorgan might approve a credit-card application from a person who has a checking account at Wells Fargo but doesn't have a credit score.

JPMorgan is expected to be the first to use the deposit-account data to extend credit to people.

Wall Street's push to flood credit cards to people who don't have credit scores comes as consumer credit explodes higher, and it's never been easier to obtain a plastic card.

Tyler Durden Fri, 05/14/2021 - 18:40

Categorías: Blogs y opiniones de economia en ingles

Psaki: Teaching "1619 Project" Critical Race Theory In College Is "Responsible"

Psaki: Teaching "1619 Project" Critical Race Theory In College Is "Responsible"

Authored by GQ Pan via The Epoch Times,

White House press secretary Jen Psaki on Thursday said it is responsible for colleges to teach the idea that racism is embedded in the American system, dismissing criticism that such teaching aims at indoctrinating American youth.

{kind=link}

In a White House press briefing, Psaki was asked about a proposed legislation by Sen. Tom Cotton (R-Ark.) that would place an one percent tax on the value of the endowments of the country’s wealthiest private colleges, and use that money to support vocational education and training.

The reporter noted that Cotton’s proposal would affect institutions that teach “un-American ideas” such as those of critical race theory and the New York Times’s “1619 Project,” which argue the United States was founded as, and remains, a racist nation.

“Without much detail of where he thinks our youth are being indoctrinated, it sounds very mysterious and dangerous,” Psaki said after asking what exactly Cotton means by un-American indoctrination and what he plans to do with the money.

“I don’t think we believe that educating the youth and the future leaders of the country on systemic racism is indoctrination. That’s actually responsible.”

“But, I would say, if he’s trying to raise money for something, then our view is there’s lots of ways to do that,” she continued.

“We know that a number of corporations hugely benefited financially during the pandemic. They could pay more taxes. We think the highest one percent of Americans can pay more taxes.”

Cotton’s proposal, known as the Ivory Tower Tax Act, was introduced earlier this week.

“Our wealthiest colleges and universities have amassed billions of dollars, virtually tax-free, all while indoctrinating our youth with un-American ideas,” the senator said in a press release.

“This bill will impose a tax on university mega-endowments and support vocational and apprenticeship training programs in order to create high paying, working-class jobs.”

An outspoken critic of the 1619 Project, Cotton last year introduced the “Saving American History Act of 2020” that would reduce federal funding to public schools where the highly controversial narrative is taught as actual U.S. history. The bill is currently in consideration in the Senate Education and Labor Committee.

Spearheaded by the New York Times’ Nikole Hannah-Jones, the 1619 Project is known for portraying the United States as an inherently racist nation founded on slavery. It consists of a collection of essays that argue, among many other controversial claims, that the real reason for the American Revolution was to preserve slavery, and that slavery was the primary driver of American capitalism during the 19th century.

The integrity of the 1619 Project has been questioned by a variety of scholars, most notably those on the Trump administration’s advisory 1776 Commission. In its first and last report, the commission criticized the project for promoting a distorted account of the nation’s founders, and called for a return to “patriotic education” focusing on how generations of Americans overcame racism to live up to the ideals enshrined in the Declaration of Independence and the Constitution.

Tyler Durden Fri, 05/14/2021 - 18:20

Categorías: Blogs y opiniones de economia en ingles

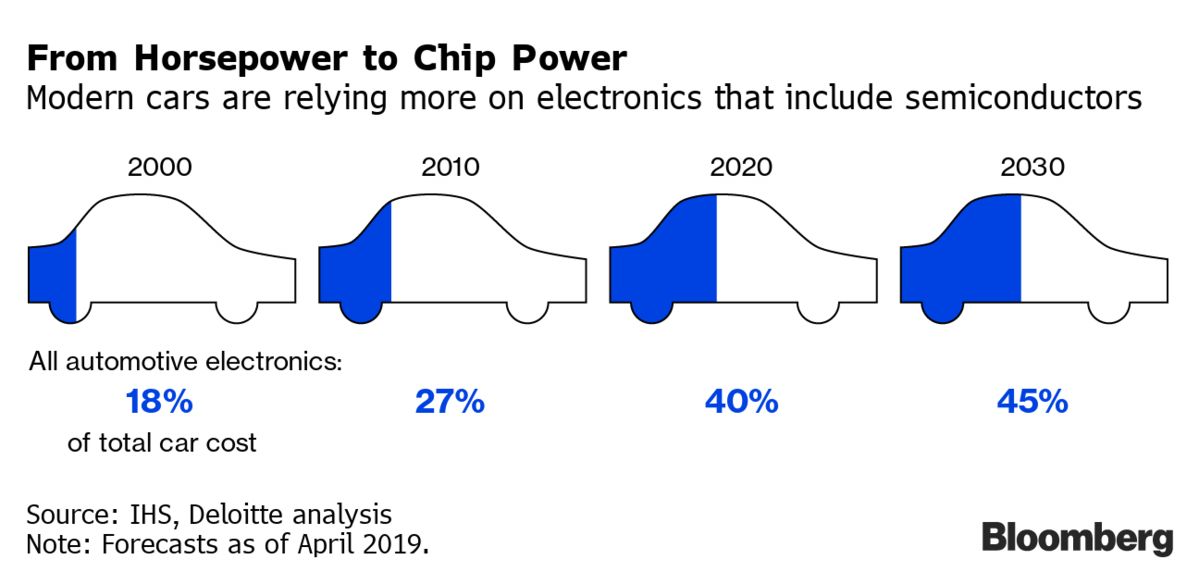

TSMC Set To "Double Down" And Vastly Increase U.S. Semi Production Investment In Arizona

TSMC Set To "Double Down" And Vastly Increase U.S. Semi Production Investment In Arizona

At the beginning of May, we noted that Taiwan Semiconductor was considering bolstering its production in the U.S., and that President Biden's Commerce Secretary was urging more domestic production. Now, it looks like TSMC could be within striking distance of a serious U.S. expansion.

The chipmaking giant is "weighing plans to pump tens of billions of dollars more into cutting-edge chip factories in the U.S. state of Arizona than it had previously disclosed", a Reuters exclusive revealed Friday morning.

The company had already said it was going to invest $10 billion to $12 billion in Arizona. Now, the company is mulling a more advanced 3 nanometer plant that could cost between $23 billion and $25 billion, sources said. The changes would come over the next 10 to 15 years, as the company builds out its Phoenix campus, the report notes.

The move would put TSMC in direct competition with Intel and Samsung for subsidies from the U.S. government. President Joe Biden has proposed $50 billion in funding for domestic chip manufacturing - a proposal the Senate could act on as soon as this week. Intel has also committed to two new fabs in Arizona and Samsung is planning a $17 billion factory in Austin, Texas.

{kind=link}

TSMC CEO C.C. Wei said on a call last month: "But in fact, we have acquired a large piece of land in Arizona to provide flexibility. So further expansion is possible, but we will ramp up to Phase 1 first, then based on the operation efficiency and cost economics and also the customers' demand, to decide what the next steps we are going to do."

TSMC has also said that talks in Europe regarding expansion have gone "very poorly", increasing the likelihood that the chip giant will be focused more on the U.S.

There are no plans for a plant in Europe, a TSMC spokesperson said.

TSMC has, however, been poaching talent from companies like Intel. The company recently hired 25 year Intel veteran Benjamin Miller to head up its human resources in Arizona. TSMC chairman and founder Morris Chang has warned about a thin talent pool in the U.S., stating: "In the United States, the level of professional dedication is no match to that in Taiwan, at least for engineers."

Commerce Secretary Gina Raimondo, earlier this month, called for a "major increase" in U.S. production capacity of semiconductors. She commented: “Right now we make 0% of leading-edge chips in the United States. That’s a problem. We ought to be making 30%, because that matches our demand. So, we will promise to work hard every day, and in the short term also see if we can have more chips available so the automakers can reopen their factories.”

{kind=link}

“In the process of building another half a dozen fabs in America, that’s thousands of Americans that get put to work,” Raimondo commented.

Just last week we noted how automakers were being forced to leave some high tech features out of new vehicles as a result of the semi shortage. Days before that, we pointed out "thousands" of Ford trucks sitting along the highway in Kentucky, awaiting semi chips for completion of assembly.We also noted recently that Stellantis said there would be "no end in sight" to the shortage and that the company was making changes to its lineup, including changing the dashboard of the Peugeot 308, to try and adapt to the crisis. Ford was another auto manufacturer to slash its expectations for full year production as a result of the shortage this year.

{kind=link}

The chip crisis has hit the auto industry so hard that it has forced rental car companies - already under immense pressure from ride sharing companies - to buy up used cars at auction to fulfill their inventory needs, Bloomberg also noted earlier this month.

Intel's CEO, speaking on 60 Minutes earlier this month, said: “We have a couple of years until we catch up to this surging demand across every aspect of the business.” Days prior, we wrote that Morgan Stanley had also suggested the shortage could continue "well into 2022".

Prior to Ford's report, we wrote about how the chip shortage was becoming a self-fulfilling prophecy, due to a shortage of chipmaking equipment. In the days leading up to that report, we wrote that Taiwan

In early April, we wrote that U.S. exporters of semiconductor chipmaking tools were struggling to get licenses to sell to China. The U.S. government had been dragging its feet in approving licenses for companies to sell chipmaking equipment to Chinese semi company SMIC, we noted at the time.

Tyler Durden Fri, 05/14/2021 - 18:00

Categorías: Blogs y opiniones de economia en ingles

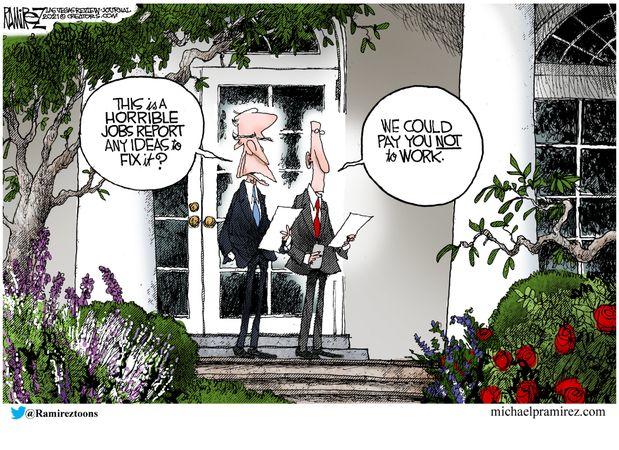

Biden's State-Sponsored Labor Shortage

Biden's State-Sponsored Labor Shortage

Authored by Greg Orman via RealClearPolitics.com,

President Biden spoke at the White House earlier this week to address an unsettling national trend – millions of jobs going unfilled in an economy still struggling to right itself. The president couldn’t deny the existence of the paradox: His own administration’s numbers show that millions of Americans are drawing unemployment while millions of jobs are going unfilled.

But he and his top economic officials dismissed the most obvious explanation for April’s dismal job numbers – generous unemployment benefits eroding the incentive to work.

“We don’t see much evidence of that,” Biden said.

{kind=link}

It was a line dutifully echoed by his designee to run the Commerce Department, the Cabinet department tasked with compiling employment numbers. But it’s a disingenuous argument. The Commerce Department, through the Bureau of Labor Statistics, derives employment numbers by compiling two surveys of employment – one completed by roughly 144,000 employers and another completed by approximately 54,000 American citizens. Neither of these surveys actually ask if an employee has been offered a job and turned it down. And it’s awfully hard to find evidence of something when you’re not actually looking for it.

The president’s remarks Monday were in response to an April jobs report showing that only 266,000 Americans rejoined the workforce at a time when employers coast to coast are reporting that they have job openings but can’t find willing workers. As if to underscore the sheer perverseness of the situation, the following day the government released data showing that job openings in March are up by 597,000 – to a staggering 8.1 million. This is the highest number of job openings since the government started tracking them at the turn of the century. It could be the highest ever.

You don’t need evidence to know that incentives matter. Common sense will suffice. But there is evidence, which I’ve witnessed first-hand.

In April 2020, as businesses were grappling with how to navigate the pandemic and associated shutdowns, I was involved in helping half a dozen businesses plan for the unknown. Their stories are instructive. In one instance, the CEO of an Idaho firm had to lay off a significant number of manufacturing staffers as orders declined precipitously. As he gathered everyone in the plant and shared the sobering news that all but three employees were going to be furloughed, one of those being kept on audibly groaned when his name was called. Roughly eight weeks later he persuaded the CEO to lay him off -- saying that he, too, deserved an extended “paid vacation” -- and call back one of the other employees.

As the pandemic progressed into the summer and fall, a Kansas City manufacturer that prints invitations and promotional items (neither big sellers in an age of Zoom meetings and social distancing) was finally able to call back furloughed workers. All his employees were offered their job back, but 20% declined (three out of four of those were still receiving unemployment compensation). The company, which pays its press operators starting pay of $22 an hour and provides benefits including health insurance, disability, and a 401(k) match, is now relying on temp agencies to fill vacancies.

Anyone with light industrial jobs, such as another Kansas City employer I aided, is likely also struggling to fill roles. In the near term, they’re hoping college students on their summer breaks will fill vacancies. A recent discussion with a local light industrial placement company revealed that it has over 200 job openings and no prospects for filling them.

This isn’t to say that there aren’t many Americans who are legitimately claiming benefits as they search for work and try to stay afloat from the significant economic pain incurred during the pandemic. But the stories articulated above, and thousands of similar ones, paint a compelling and ominous picture. The purposeful constriction of the labor market by the federal government constitutes a state-sponsored labor strike. And we don’t need signs and picket lines to see the evidence – Democrats are happy to read their party’s stage directions out loud.

“Let’s get one thing straight: there is no labor shortage,” tweeted Robert Reich, who headed the Department of Labor in Bill Clinton’s administration.

“There is a shortage of employers willing to pay their workers a living wage.”

On Monday, the president regurgitated Reich’s talking point: “People will come back to work if they’re paid a decent wage.”

Spoken like a true union boss.

So that’s the endgame here? Using government money, all of it borrowed, to jack up wages? The problem with this state-sponsored labor shortage is that the pain is one-sided. Strikes work precisely because both sides have something obvious to lose if they don’t work out an agreement. With generous unemployment benefits (largely tax-free), paid health care (employers are now required to provide, free of charge, six months of COBRA coverage to laid off employees, which the government theoretically will reimburse), and no enforceable requirement to look for a job, there’s no real monetary incentive to go back to work. In some cases, it may not even be a rational act: A married woman with two kids, who is her family’s only breadwinner and making the average national wage of $30 an hour will have an after-tax income that’s within a dollar an hour of her old wage if she remains unemployed. She’ll also have paid health insurance, likely a huge benefit. And she won’t have to worry about day care, either, which is an issue in the many places where teacher unions (and school districts controlled by them) are refusing to return to the classroom.

Those people on the front lines of providing social welfare services to poorer Americans often decry the “benefits cliff” that greets Americans trying to improve their lives. The argument is that if we take away a dollar of benefits for every dollar someone earns, we leave them with no incentive to improve their lot in life. It’s an argument I fully embrace and have used to argue for a more gradual reduction in benefits as Americans pull themselves out of poverty. Biden has created an enormous benefits cliff and is now arguing the other side of the coin.

Biden’s hope that this labor force constriction will permanently raise wages is a dangerous gamble. All three of the companies mentioned above are now implementing automation and other strategies to improve their operations without adding workers. While they are all growing and will have roles for each of their current workers long into the future, other employees at different companies may not be so lucky. Not everyone can work for the government, but if we continue with these policies, millions more will be dependent on a government check.

The real answer to lifting up American workers lies not in more unemployment benefits but in helping them obtain the skills they need to perform higher value work. This will require a whole host of changes to our educational system. A good place to start would be re-examining our guaranteed student loan programs to ensure kids getting welding and machining certificates qualify on the same basis as university students. It will require public/private partnerships between employers and professional colleges to train workers in relevant skills. Importantly, it will require evaluating K-12 education to ensure kids are prepared for the world they are entering. Those changes and many other similar ones should be the focus of the Biden administration’s efforts to lift people up. Short-term strategies that artificially distort markets will only work so long before they come crashing down on the people they’re intended to help.

Tyler Durden Fri, 05/14/2021 - 17:40

Categorías: Blogs y opiniones de economia en ingles

Will Crypto Weakness Push Silver Higher

Will Crypto Weakness Push Silver Higher

By Larry McDonald of The Bear Traps Report

Crypto down! Silver up?We think a growing forward trend is a combination of pressure on crypto currencies, particularly Bitcoin (Ethereum has software applications that work and becoming more popular so isn't just a one trick pony like Bitcoin) with some of that flowing into precious metals, particularly silver.

Why? If in fact there has been crypto currency substitution for precious metals to some non quantifiable and therefore non verifiable extent, then that certainly allows for reverse substitution on a crypto drawdown in a similar scale. There have been three 70% crashes in crypto. As Aristotle said in his Metaphysics, "If it happened before, it can happen again."

So surely if something has happened three times, it can happen a fourth time. If crypto represents a flight from fiat currency, then a move out of crypto should lead into the ultimate non fiat currency: gold (and gold's playmate, silver).

Remember! Gold and silver are not substitutes for fiat currencies. Fiat currencies are substitutes for gold and silver. As readers know, we like precious metals and we like copper. Palladium made a new high the other day. Between deficit spending, upcoming yield curve control, opening up of the economy, and the U.S. infrastructure spend, inflation havens should work, to gold and silver's benefit.

Furthermore, because of electric vehicle and solar panel production growth, silver has additional demand drivers that should push it to new recovery highs. So, now we see an additional reason to play long precious metals: a potential kick in the pants for Bitcoin.

{kind=link}

SLV Silver is breaking out to the upside. SLV broke above the 50 day moving average on 163% average volume on Wednesday...

{kind=link}

After peaking in early June (shortly before gold peak), the ratio of Newmont to gold is breaking out to the upside. Gold miner outperformance is a sign of a healthy precious metal bull market.

Tyler Durden Mon, 04/26/2021 - 08:45

Categorías: Blogs y opiniones de economia en ingles

Durable Goods Orders Significantly Disappoint In March

Durable Goods Orders Significantly Disappoint In March

After February's surprise (weather-impacted) tumble, Durable Goods Orders were expected to rebound strongly in preliminary March data but they were disappointed. Against expectations of a sturdy 2.3% MoM jump, Durable Goods Orders rose just 0.5% MoM (orders were revised up modestly to -0.9% for Feb. from -1.2%)...

{kind=link}

Source: Bloomberg

Due to base effects, Durable Goods Orders surged 25.6% YoY, the biggest jump since 2014 (big Boeing orders).

Core capital goods orders, a category that excludes aircraft and military hardware and is seen as a barometer of business investment, rose just 0.9% (almost half the expected 1.7% jump) after a revised 0.8% decline.

Tyler Durden Mon, 04/26/2021 - 08:37

Categorías: Blogs y opiniones de economia en ingles

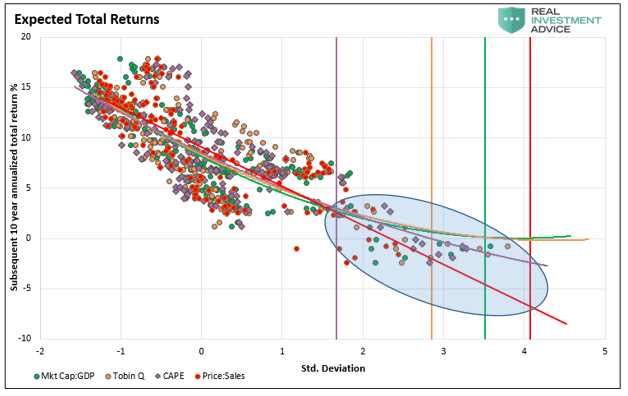

The Fed Cannot Fix This & The Next "Bear Market" Will Not Be Like The Last...

The Fed Cannot Fix This & The Next "Bear Market" Will Not Be Like The Last...

Authored by Lance Roberts via RealInvestmentAdvice.com,

When there is a discussion of low future returns due to valuations, what gets missed is that such requires a bear market.

Let me explain.

In “Do You Feel Lucky,” Michael Lebowitz compiled a series of valuation metrics and their correlation to future returns. To wit:

“The average of the 10-year expected returns from the four gauges is -0.75%. When the Fed backs off, whether by its design or due to inflation, slower economic growth, or massive debt overhead, rich valuations will matter.”

{kind=link}

The mistake many investors make is assuming that such means every year, over the next decade, returns will be near zero. As we will discuss, it is not every year, but one or two awful years, impacting the whole.

Fun With MathThe vital point to understand is that over the long-term investing period, “value” and “returns” are both inextricably linked and opposed. As shown above, forward return expectations are lower than the long-term average given current valuation levels.

Let’s review what “low forward returns” does and does not mean before looking at different valuation measures.

-

It does NOT mean the stock market will have annual rates of return of sub-3% each year over the next 10-years.

-

It DOES mean the stock market will have stellar gains in some years, a big crash somewhere in between, or several smaller ones, and the average return over the decade will be low.

“This is shown in the table and chart below which compares a 7% annual return (as often promised) to a series of positive returns with a loss, or two, along the way. (Note: the annual average return without the crashes is 7% annually also.)”

{kind=link}

“From current valuation levels, two-percent forward rates of return are a real possibility. As shown, all it takes is a correction, or crash, along the way to make it a reality.”

Such isn’t a prediction; it is just statistical probability and simple math.

Most importantly, as stated above, none of these factors or measures mean the markets will produce single-digit rates of return each year for the next decade. The reality is there will be some strong return years during that period. Unfortunately, the bulk of those years will get spent making up previous losses.

That is the nature of investing in the markets. It is just part of the full-market cycle.

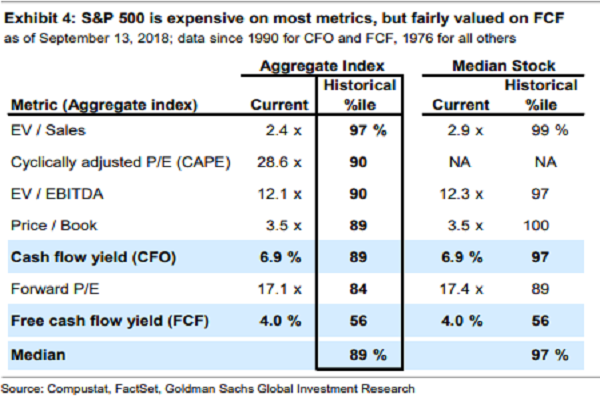

Why A 50% Correction Is RequiredOne of the essential issues overhanging the market is simply that of valuations. As Goldman Sachs pointed out recently, the market is pushing the 89% percentile or higher in 6 out of 7 valuation metrics.

{kind=link}

So, just how big of a correction would be required to revert valuations to long-term means? Michael Lebowitz recently did some analysis for RIA PRO:

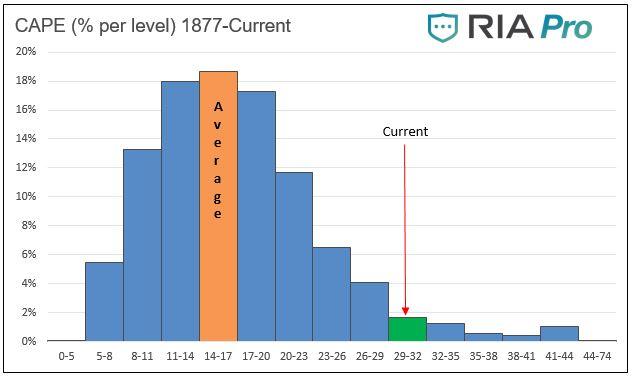

“Since 1877 there are 1654 monthly measurements of Cyclically Adjusted Price -to- Earnings (CAPE 10). Of these 82, only about 5%, have been the same or greater than current CAPE levels (30.5). Other than a few instances over the last two years and two others which occurred in 1929, the rest occurred during the late 1990’s tech boom. The graph below charts the percentage of time the market has traded at various ranges of CAPE levels.”

{kind=link}

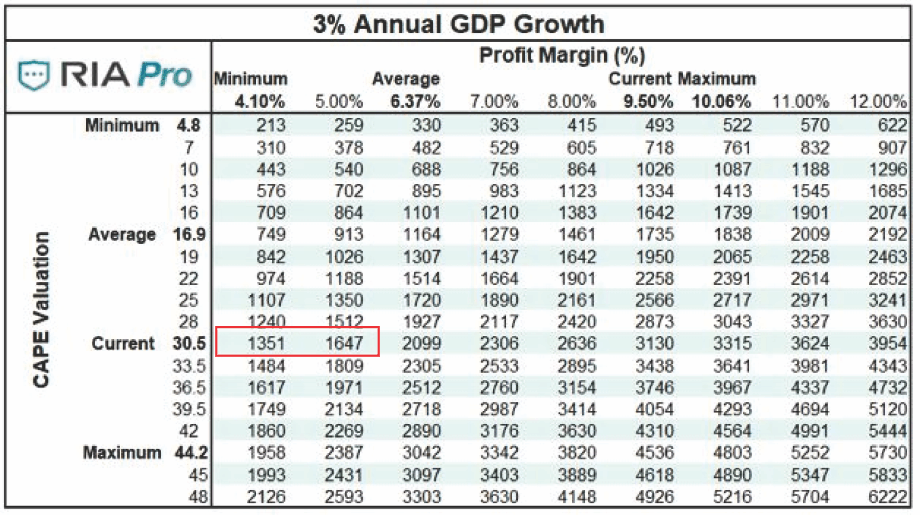

Given that valuations are at 30.5x earnings and that profit growth tracks closely with economic growth, a reversion in valuations would entail a decline in asset prices from current levels to somewhere between 1350 and 1650 on the S&P (See table below). From the recent market highs, such would entail a 54% to 44% decline, respectively. (To learn how to use the table below to create your own S&P 500 forecast, give RIA Pro a 14-day free trial run.)

{kind=link}

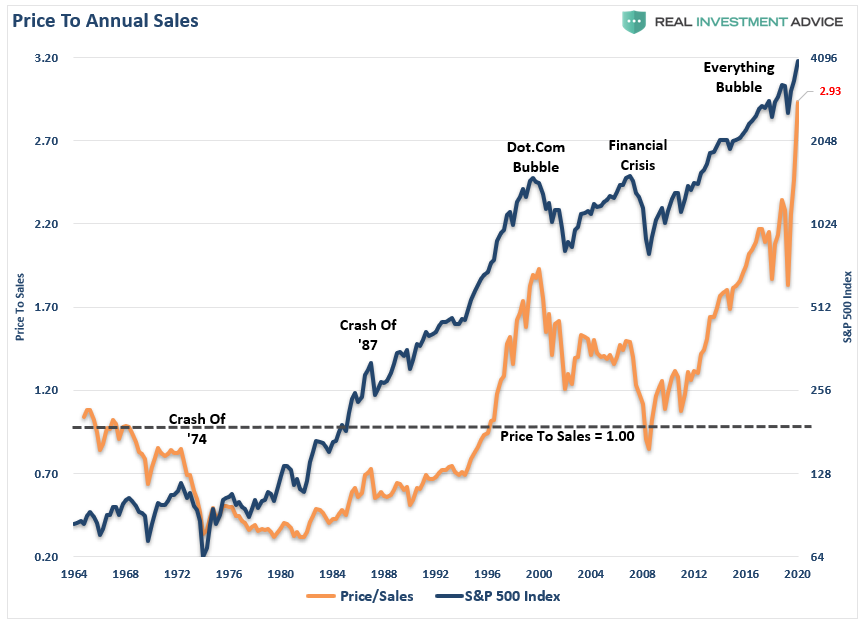

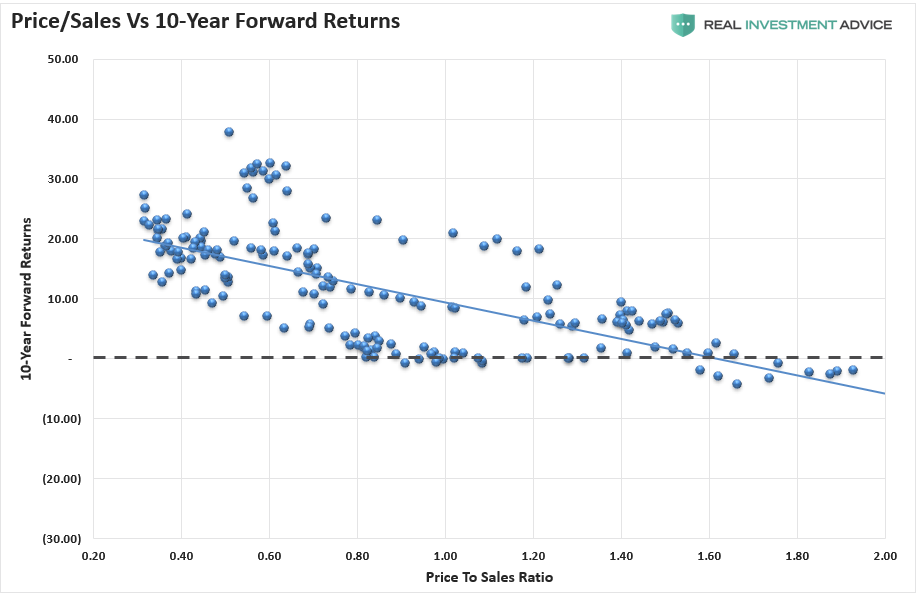

Such also corresponds with the currently elevated “Price to Revenue” levels, which are now higher than at any point in previous market history. Given the longer-term norm is 1.0, a reversion as seen in 2000 and 2008, each required a price decline of 50% or more.

{kind=link}

As expected, 10-year forward returns are below zero historically when the price-to-sales ratio is at 2x. There has never been a previous period with the ratio climbing to near 3x.

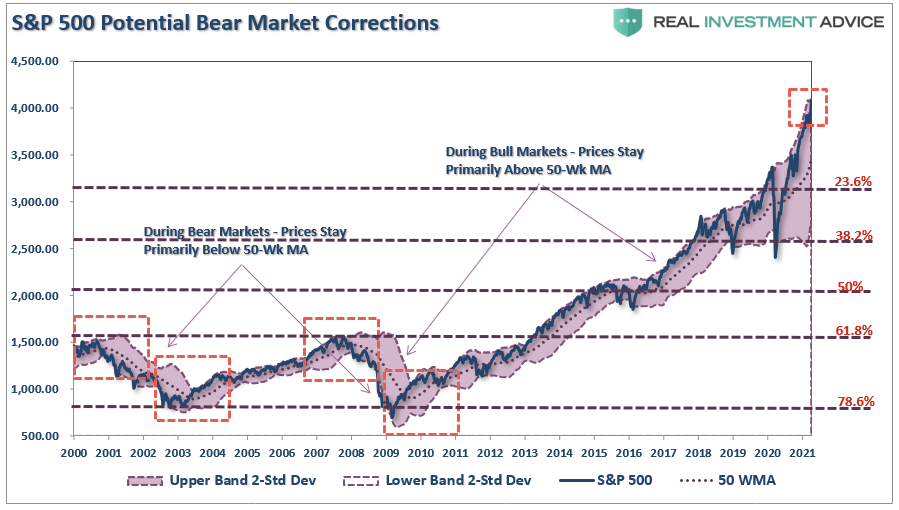

What Would A Mean Reversion Entail?{kind=link}

The chart below uses Fibonacci retracement measurements as potential reversion levels. It is worth pointing out markets are currently pushing 2-standard deviations above the 50-week moving average. As noted, markets trend above the 50-week moving average during bull markets. Bear markets trend below that average.

Importantly, corrections during bull markets can temporarily break below that average but quickly rise back above it. Such is why March of 2020 was a “correction” and not a “bear market,” as price trends did not change.

{kind=link}

Using those Fibonacci retracement levels:

-

A 23.6% correction would pull markets back to roughly 3100, leaving the current bull market intact.

-

The 38.2% retracement level would start retesting the March 2020 lows. Such will begin pushing the early boundaries of a “bear market” if prices do not recover quickly.

-

A bear market will be well entrenched at the 50% retracement level. Valuation levels will approach more reasonable levels of “fair value,” and sentiment will turn negative.

-

At a 61.8% retracement level, it will erase a majority of the last decades bull market. While many will suggest such a retracement is unlikely, history suggests such is indeed possible.

-

If the 74.6% retracement level gets reached, there will not be many investors left in the market. However, valuations will have reverted to historically cheap levels, which have been the foundation for long-term secular bull markets to begin.

Such a level certainly seems unthinkable, but as Shawn Langlois previous penned:

“I recognize the notion of a two-thirds market loss seems preposterous. Then again, so did similar projections before the 2000-2002 and 2007-09 collapses.”

While the current belief is that such declines are no longer a possibility due to Central Bank interventions, we had two 50% declines just since the turn of the century. The cause was different, but the result was the same.

The next major market decline will get fueled by the massive levels of corporate debt, underfunded pensions, and record “margin debt,” and the lack of “market liquidity.”

What Will Cause It?The real problem with discussing corrections is three-fold:

-

It is has been so long since we have had a bear market, many investors have forgotten what happens, and more importantly, how they reacted previously.

-

The majority of mainstream media advice gets written by individuals who don’t manage money for a living, have no substantial investment capital at risk, and have never actually been through a bear market.

-

Given the extremely long market expansion, many investors have genuinely come to believe “this time is different.”

What will cause the next bear market?

I do not have a clue. Nor does anyone else.

Numerous catalysts could pressure such a downturn in the equity markets:

-

An exogenous geopolitical event

-

A credit-related event (most likely)

-

Failure of a major financial institution

-

Recession

-

Falling profits and earnings

-

An inflationary or deflationary spike

-

A loss of confidence by corporations that contracts share buybacks

Whatever the event is, which is currently unexpected and unanticipated, the decline in asset prices will initiate a “chain reaction.”

-

Investors will begin to panic as asset prices drop, curtailing economic activity and further pressuring economic growth.

-

The pressure on asset prices and weaker economic growth, which impairs corporate earnings, shifts corporate views from “share repurchases” to “liquidity preservation.” Such removes critical support of asset prices.

-

As asset prices decline further and economic growth deteriorates, credit defaults begin triggering a near $5 Trillion corporate bond market problem.

-

The bond market decline will pressure asset prices lower, which triggers an aging demographic who fears the loss of pension benefits, sparks the $6 trillion pension problem.

-

As the market continues to cascade lower at this point, the Fed is monetizing nearly 100% of all debt issuance and has to resort to even more drastic measures to stem selling and defaults.

-

Those actions lead to a further loss of confidence and pressure markets further.

The Federal Reserve can not fix this problem, and the next “bear market” will NOT be like that last.

It will be worse.

Low Future Returns Only Require OneOver the next decade, it is unlikely that a 50-61.8% correction will happen without a credit-related event occurring. The question becomes the limits of the Fed’s ability to continue to “bailout” banks and markets once again.

Maybe they can, but I am not sure I want to ride the markets down trying to find out.

The point here is that it only takes one “mean reverting” event over the next decade to lower your annualized returns close to zero. Such does not bode well for retirement plans banking on 6-8% annualized returns or more.

As noted, over the next decade, there will be some terrific “bull market” years to increase portfolio valuations. However, one essential truth is indisputable, irrefutable, and undeniable: “mean reversions” are the only constant in the financial markets over time.

The problem is that the next “mean reverting” event will remove most, if not all, of the gains investors have made over the last five years. Possibly, even more.

Still don’t think it can happen?

“Stock prices have reached what looks like a permanently high plateau. I do not feel there will be soon if ever a 50 or 60 point break from present levels, such as they have predicted. I expect to see the stock market a good deal higher within a few months.” – Dr. Irving Fisher, Economist at Yale University 1929

Tyler Durden Mon, 04/26/2021 - 08:27

Categorías: Blogs y opiniones de economia en ingles

JP Morgan Launches Bitcoin Fund For Rich Clients After Years Of Bashing Crypto

JP Morgan Launches Bitcoin Fund For Rich Clients After Years Of Bashing Crypto

Ever since JP Morgan CEO Jamie Dimon first denounced bitcoin waaaaay back during the heady crypto-rally of 2017 (shortly before we revealed that JP Morgan's asset-management arm was seemingly buying the dip on behalf of its wealthy clients via a Scandinavian ETN), teams of strategists employed by the bank have produced a steady stream of bearish reports warning its clients about the risks of investing in bitcoin.

JPMorgan's daily bitcoin hitpiece is out. Just how bad does JPM prop want to be long this?

— zerohedge (@zerohedge) January 25, 2021But in a sudden reversal, JPMorgan's traders - once threatened with firing should they dare touch bitcoin - will soon get their chance to trade the pioneering cryptocurrency on the bank's behalf. In news that's hitting just as bitcoin prices climb back from a Sunday dip, CoinDesk reported Monday morning that JP Morgan Chase will soon launch its own actively managed bitcoin fund, making JPM the latest US megabank to embrace hawking crypto assets (rather than struggling to co-opt blockchain technology for its own purposes).

JPMORGAN TO OFFER ACTIVELY MANAGED BITCOIN FUND: COINDESK

Oh so THAT'S WHY JPMorgan was talking down bitcoin for the past 3 months

The fund, which could launch as soon as this summer, will reportedly involve institutional ship NYDIG, which will serve as JPM's bitcoin custody provider. In a notable break from other passively managed bitcoin funds offered by Galaxy Digital and Grayscale, JPM's crypto fund will be "actively managed" (allowing the bank to charge higher fees).

{kind=link}

Like those other funds, the JP Morgan fund will allow institutions and wealthy clients to buy exposure to bitcoin without actually having to buy, store and secure their own coins. The fund will be offered to the bank's "private wealth" clients, which mostly caters to wealthy individuals and family offices.

JPM has come close to offering bitcoin-linked products before. Back in March, its investment bank issued its first crypto-adjacent investment product, a structured note tied to the performance of bitcoin proxy stocks like MicroStrategy and Riot Blockchain.

Now that the bank has been exposed for quietly accumulating its own bitcoin position, we couldn't help but notice that JPM - which was bashing bitcoin as recently on Friday - hasn't published a new note arguing that downward momentum might reemerge. Dimon infamously warned that he would "fire in a second" any JPM trader who touched bitcoin. "If you’re stupid enough to buy it, you’ll pay the price for it one day," he said at the time. Though Dimon quickly walked back these comments at the time, we would love to hear JPM explain away these comments while pitching its new bitcoin product to some of its most lucrative private clients.

We're also curious to see what fees JPM charges clients for this new actively managed product, which we imagine will put Coinbase's commissions to shame.

Tyler Durden Mon, 04/26/2021 - 08:11

Categorías: Blogs y opiniones de economia en ingles

Stock Buyback Monster Apple Commits To Invest $430BN In The US Over Five Years

Stock Buyback Monster Apple Commits To Invest $430BN In The US Over Five Years

The company that has repurchased more stock than any other corporation in the history of the world, Apple, buying back a whopping $67BN in 2019 alone, appears to be preparing to unleash another tidal wave of stock buybacks which explains why it is busy engaging in virtue signaling diversions this morning, when three years after its initial pledge to invest in the US, it recommitted this morning to plunking billions more into the US over the next five years, and now expects to spend $430BN by 2026, a 20% increase compared to its initial estimate.

The iPhone maker - which was quick to note that it is the largest taxpayer in the US and has paid almost $45 billion in domestic corporate income taxes over the past five years alone, or about 20% of how much stocks it repurchased - will create 20,000 new jobs in innovative fields like silicon engineering and 5G technology across the country - or roughly how many part-time jobs each new Amazon warehouse creates - and fund a new campus in North Carolina, the company said in a statement Monday.

“At this moment of recovery and rebuilding, Apple is doubling down on our commitment to U.S. innovation and manufacturing with a generational investment reaching communities across all 50 states,” said Chief Executive Officer Tim Cook.

"Apple today announced an acceleration of its US investments, with plans to make new contributions of more than $430 billion and add 20,000 new jobs across the country over the next five years. Over the past three years, Apple’s contributions in the US have significantly outpaced the company’s original five-year goal of $350 billion set in 2018. Apple is now raising its level of commitment by 20 percent over the next five years, supporting American innovation and driving economic benefits in every state. This includes tens of billions of dollars for next-generation silicon development and 5G innovation across nine US states."

Apple plans to make new contributions of more than $430 billion in the US and add 20,000 jobs across the country over the next five years.{kind=link}

In the past three years, Apple’s investments have outpaced its original five-year goal of $350 billion in investments set in 2018 although it wasn't clear just how much it has actually invested, with the bulk of this capital likely spent on the company's new UFO-like headquarters.

As part of its expansion, Apple plans to invest more than $1 billion in North Carolina to build a new campus and engineering hub in the Research Triangle area. The investment will create at least 3,000 new jobs in machine learning, artificial intelligence, software engineering, and other advanced fields.

According to the release, Apple supports more than 2.7 million jobs across the country through direct employment, spending with US suppliers and manufacturers, and developer jobs in the thriving iOS app economy.

Tyler Durden Mon, 04/26/2021 - 08:10

Categorías: Blogs y opiniones de economia en ingles

S&P Futures Flat Ahead Of Earnings Deluge; Nasdaq Drops As Tesla Looms

S&P Futures Flat Ahead Of Earnings Deluge; Nasdaq Drops As Tesla Looms

S&P futures were flat, Nasdaq futures dipped ahead of FAAMG earnings while European stocks clawed their way higher on Monday and Asia rose as world markets began the week in a relatively upbeat - if quiet - mood following further signs last week that economies are recovering rapidly. There were no major moves, however, as investors refrained from taking on large positions ahead of this week's Federal Reserve meeting, US GDP print and corporate earnings barrage.

At 7:30 a.m. ET, Dow e-minis were up 30 points, or 0.09%, S&P 500 e-minis were down 3.75points, or 0.08%, and Nasdaq 100 e-minis were down 48.75 points, or 0.37%.

{kind=link}

Nasdaq 100 futures dropped to as much as 0.4%, reversing earlier gain of as much as 0.1%, as big technology stocks retreated ahead of first-quarter results later this week, while Treasury yields rose. Nasdaq was also weaker following a weekend report that investors had pulled a whopping $6BN from the QQQ ETF in the past five days, the most since the dot com bubble burst.

High-flying firms, including Amazon, Facebook, Alphabet and Microsoft slipped between 0.2% and 0.4% in premarket trading. Tesla edged higher as analysts expect the electric automaker to report a rise in first-quarter revenue when it reports after markets close following record deliveries for the period.

Of the 123 companies in the S&P 500 that have published results so far, 85.4% have reported earnings above analysts’ estimates, with Refinitiv IBES data now predicting a 33.9% jump in profit growth.

With risk bid, safe havens including the dollar and government bonds were under pressure while copper, seen as a barometer of growth, surged to the highest in a decade. The U.S. 10-year rate bounced back from its 50-day moving average, underscoring the reflation trade is still alive, but remained below the 1.60% level, sustaining a risk-on bid for global assets including emerging markets.

{kind=link}

Global stocks have been basking in a massive rally - the MSCI world index has suffered only three down months in the past 12 and is up nearly 5% this month and 9% for the year as investors bet on a rapid post-pandemic economic rebound turbocharged by vast government and central bank stimulus. General sentiment remained bullish to start the week, with Wall Street hitting another intraday record-high on Friday and European shares not far off record highs in early Monday trading.

However, as we noted over the weekend, sellside analysts are turning increasingly bearish and say stocks look a little too confident and that the rally will run into hurdles after setting such a lightning pace and with so much of the recovery and fiscal stimulus splurge already priced in. Analysts at Goldman Sachs, Morgan Stanley, Deutsche Bank and now, JPMorgan, have warned of some turbulence ahead, after a rally that has taken the S&P 500 and Dow to fresh records this year

“The real crux of the issue, however, is what’s in the price. The year-to-date rally has increasingly eliminated upside to our targets,” noted Morgan Stanley strategist Andrew Sheets. “Across four major global equity markets (the U.S., Europe, Japan and emerging markets), only Japan is currently below our end-2021 strategy forecast.”

That did not prevent investors from bidding risk up, however, and the broader Euro STOXX 600 was just barely in the green while Germany’s DAX rose 0.22%. Britain’s FTSE 100 climbed 0.21%. European stocks were little changed Monday, as gains for banks and travel companies offset losses for carmakers and technology companies. Here are some of the biggest European movers today:

- IMI shares gain as much as 7.9% to the highest since July 2014 after the company raised guidance for FY21 and announced a GBP200m buyback in first-quarter update.

- Hensoldt shares rise as much as 18% in Frankfurt after Italy’s Leonardo agreed to buy a 25% stake in the German defense company for EU606m, or about 23 euros a share.

- Tate & Lyle shares climb as much as 7%, the most since early November, as the company explores selling a controlling stake in its primary products business.

- Kuehne + Nagel shares rise as much as 3.2%, extending its record high, after reporting first-quarter results that were “stunning,” according to Vontobel.

- AMS shares fall as much as 5.1% to the lowest since Aug. 2020 after Credit Suisse double downgrades to underperform from outperform, citing concern over the chipmaker potentially losing two out of three sources of business with Apple.

- Philips shares drop as much as 3.4% following the company’s first-quarter results. Analysts say investor responses to the beat and guidance raise are tempered by a reported quality issue in a component used in some sleep and respiratory products.

Earlier in the session, Asia stocks rose as investors continued to keep a close eye on the ongoing earnings season globally and U.S. data for clues on economic recovery. The MSCI Asia Pacific Index rose 0.6% led by tech and material shares.

India shares were among the biggest gainers with the S&P BSE Sensex Index up about 1%. As the index on Friday capped its third consecutive weekly decline amid a surge in Covid-19 infections, funds such as Fidelity International and Invesco were seeking opportunities to add stocks, seeing India’s vaccination campaign and less-disruptive lockdown measures as offering some support.

Meanwhile, China’s CSI 300 Index closed down 1.1% after rising as much as 0.9%, as investors await a key gathering of the country’s top leaders expected to take place this week for signals on liquidity policies. Consumer staples and financial stocks led the loss, with Kweichow Moutai and China Merchants Bank among the biggest drags on the gauge. The gauge’s decline came after a bumpy rebound in recent weeks that has set April up for the first monthly rise since January. The rebound may have some lasting power, according to CSC Financial, which recommends investors hold onto shares rather than cash ahead of a five-day May holiday that starts this weekend. The recent strength in stocks was partly due to lower borrowing costs after China’s first-quarter economic growth slightly missed analysts’ estimates, the brokerage’s analysts including Zhang Yulong wrote in a Monday note. Chinese authorities are stepping up effort to support the country’s small firms, with the banking regulator urging five large lenders to boost loans to the sector by more than 30% this year. Traders are also closely watching the Politburo meeting expected to be held this week for clues on liquidity conditions and broader economic policies in the months ahead. Foreign investors bought a net 3.2 billion yuan of A shares via the trading link with Hong Kong, less than half of their purchases on Friday. However, total trading volume in Shanghai and Shenzhen jumped to the highest since March 9 at 868 billion yuan. The Shanghai Composite also slid in the afternoon to close 1% lower. Hong Kong’s Hang Seng Index lost 0.4%.

Japanese shares eked out gains with the Topix rising 0.2%, rising for the second day in three, despite Tokyo and other prefectures imposing a state of emergency. SoftBank Group and Fast Retailing provided the biggest boosts to the Nikkei 225 Stock Average. Railway operators and machinery makers gave the most support to the Topix. Both gauges completed a weekly drop of more than 2% on Friday. “From a global perspective, we’re in a risk-on market,” said Tetsuo Seshimo, a fund manager at Saison Asset Management Co. in Tokyo. “With easy monetary policies sustained, the upward trend in global equities is the main scenario.” Despite today’s advance, Japanese shares may fall behind globally due to the nation’s slow pace of vaccinations and the impact of restrictions on the economy, Seshimo said. A new state of emergency started Sunday for Tokyo, Osaka and two other prefectures due to rising infections. Mitsushige Akino, a senior executive officer at Ichiyoshi Asset Management, said further gains may face headwinds as coronavirus-driven sentiment causes Japan’s equity market to fall behind the U.S. and Europe. “Japanese equities will likely rebound, but apart from solid U.S. data, the market is devoid of fresh leads and the upside will remain tough,” Akino said.

In Vietnam, the stock benchmark fell 2.6% after the country’s Health Minister Nguyen Thanh Long said the risk of Covid-19 spreading in the country is “very high and worrying.” New Zealand’s stock market was closed for a local holiday.

“While positive surprises have supported the stock market, the trend on earnings is even more important,” David Kelly, chief global market strategist at JPMorgan Asset Management, wrote in a note. “Investors will continue to watch the earnings season with 181 of the S&P 500 companies set to announce their first-quarter results this week.”

In bond markets, government debt yields rose as investors dumped safer assets. The U.S. 10-year Treasury yield rose 3 basis points to 1.59% trading near highs of the day, cheaper by more than 3bp at long-end, ahead of this week’s front-loaded auction cycle which includes 2- and 5-year note sales Monday. FOMC rate decision on Wednesday is week’s main event after the auction cycle. 10-year yields around 1.59%, higher by 3.6bp vs Friday’s close, are ~1bp cheaper vs bunds and gilts; S&P 500 futures are down 0.1% after cash gained 1.1% Friday. Peripheral spreads widen with 30y Italian yields rising to 1.83%, highest since Sept. 2020.

In currencies, the dollar extended a two-month low, heading for the biggest monthly loss since November. The euro was steady after touching a two-month high of $1.2117 while European government bonds were lower, with the periphery underperforming bunds The Bloomberg Dollar Spot Index is at a crossroads and chances are the euro’s performance will define the outcome. The pound advanced; the U.K. economy will see “very rapid growth at least over the next couple of quarters,” Bank of England Deputy Governor Ben Broadbent told the Telegraph in an interview. The Australian dollar was the top performer among G-10 currencies amid strong gains in stocks and iron ore. Norway’s krone fell against most G-10 peers as oil declined ahead of a key OPEC+ meeting later this week