Se encuentra usted aquí

Blogs y opiniones de economia en ingles

Journey to 100X

When’s the last time you made 100X on an investment? Not 100% on your initial investment, 100 times your initial investment. That means you sink $10,000 into an investment and pull out a cool $1,000,000…for many investors this could be a life-changing outcome. That’s a 100X return, and in the investment community, we refer to […]

The post Journey to 100X appeared first on Meb Faber Research - Stock Market and Investing Blog.

Categorías: Blogs y opiniones de economia en ingles

Letters to the editor

A selection of correspondence

Categorías: Blogs y opiniones de economia en ingles

Early Retirement For Dividend Investors

There are a lot of stories about people who become financially independent these days in their 30s or 40s. While these are isolated instances in the grand scheme of things, they are part of a broader movement online, where people want to take ownership of their time and retire to something more meaningful in their lives. Some call it retirement, others call it financial independence, and a lot of...

To read the whole article, please click on the article title above.

To read the whole article, please click on the article title above.

Categorías: Blogs y opiniones de economia en ingles

A little planning goes a long way

What’s the job of a financial planner? While there is probably no consensus of the job of a financial planner in general, one part of the job, I think most people could agree on, is to help investors achieve their retirement goals.

Saving for retirement is one of the most important financial planning exercises we all have to do, and it gains in importance as government and corporate pension funds become increasingly thinly stretched. Even more so, we live in a world where employees of a company no longer have access to defined benefit plans but have to make do with defined contribution plans, which means that the employee bears the investment risk of the pension plan. Making the right decisions with your pension fund investments is crucial as is the effort to make the right decision in how much to save etc.

Unfortunately, I know too many financial advisers who define their job as helping people achieve their retirement goals and then translate this as helping them to pick outperforming funds or stocks. And that is not going well, as a study by researchers from the University of Missouri has shown. They looked at 2,000 pension plans in the United States and the performance of the funds and the plans overall between 2013 and 2015. Crucially, they split the plans between the c80% plans that provided advisory services to the investors and the 20% of plans that provided no such advisory assistance.

Their results show that when it comes to picking outperforming funds within a retirement plan, the advisors are no better than chance. While the average return of employees in plans with advisers was about the same as the return for employees in plans without advisers, the volatility and downside risks of the portfolios of employees in advisor-supported plans was somewhat higher. Thus, advisers moved investors into funds with higher risk but no compensation for that extra risk.

We could all chime into the usual song and dance how advisers are useless and unable to pick stocks or funds, but that’s not the point. The point is that achieving your retirement goals has nothing to do with picking stocks or funds. The true value add of an adviser lies in the actual planning process, not the selection of investments.

Already a decade ago, Annamaria Lusardi and Olivia Mitchel published what I consider to be one of the most important papers on financial planning of all time. They looked at the type of planning individuals engaged in and how that influenced their net worth at retirement. They distinguished between non-planners, simple planners (people who roughly knew how much of their income to save each month or each year), serious planners (people who have a proper financial plan) and successful planners (people who have a financial plan in place and managed to stick to it throughout their career, aka fairies, unicorns and otherwise unimaginably disciplined investors). The chart below shows that just moving from non-planners to a simple planning exercise increases net wealth at retirement by a factor of two to three. Engaging in serious planning then adds another 25% to 35% in extra wealth at retirement.

This is where the true value of financial planning lies and where advisers really add value: Making investors aware that they need to safe, how much they need to save and how best to manage their income and expenses to achieve their savings goals. Everything else is just noise and not worth your time.

Net wealth at retirement at retirement

a.image2.image-link.image2-510-960 { padding-bottom: 53.125%; padding-bottom: min(53.125%, 510px); width: 100%; height: 0; } a.image2.image-link.image2-510-960 img { max-width: 960px; max-height: 510px; }Source: Lusardi and Mitchell (2011)

Categorías: Blogs y opiniones de economia en ingles

When Genius Failed To Exist

Today's financial pundits are mental midgets standing on the shoulders of intellectual giants. Therefore they are oblivious to the fact that this gamified alchemy is the exact opposite of what created prosperity in the past...

The stock market just closed out its (Second) best first half since 1998 which directly preceded the LTCM (Long Term Capital Management) debacle. We also learned back in April that more money poured into stocks since the election than in the prior 12 years combined. Since that time, inflows have continued their record pace - ETF inflows are almost at a new record only six months into the year. What we are witnessing is the ideal recipe for panic meltdown.

Going back to 1998, Long Term Capital Management (LTCM) was a massively leveraged hedge fund managed by financial PhDs who were considered geniuses on Wall Street and in academia. The collapse of their fund in the second half of 1998 almost brought down the global financial system. They had made various asinine assumptions about the correlation of risk assets that were true most of the time but categorically failed when markets went into meltdown mode following the 1997 Asian Financial crisis. In other words they were oblivious data miners who assumed the past could be endlessly extrapolated into the future, hence they blindly ignored all imminent signs of risk and focused solely upon statistical probabilities. Which is the way all of today's quantitative/algorithmic trading programs work. Ignorance is bliss. More on that later. The book that described the entire debacle was called "When Genius Failed". Hence, the title of this post. The net result of that collapse was a massive Fed bailout that inadvertently lubricated the melt-up phase of the brewing Dotcom bubble.

The Dotcom bubble itself was abided by the asinine belief that valuations, profits, and even sales no longer matter. All that matters is internet page views aka. "eyeballs". That new "business model" consisting of massively unprofitable companies going public at a record rate soon found the natural limit of fools with money to burn on worthless IPOs. At that point, the "smart money" rotated to the Big Cap safe havens - Microsoft, Intel, Dell, and Cisco. And then those stocks imploded bringing down the entire casino.

A divergence very similar to what is happening today:

When the Fed sponsored DotCom bubble collapsed, they lowered rates to a multi-decade low 1.5% which set off the melt-up stage of the brewing housing bubble. At the time, Fed Chairman Greenspan lauded the "financial innovations" taking place in the subprime lending market and he encouraged borrowers to load up on adjustable rate mortgages (ARMs). ARMs had been previously unpopular in the U.S. market because they shift all interest rate risk from the lender to the borrower, offset by a minor interest rate reduction. Within months, Greenspan jacked up rates 17 meetings in a row and imploded everyone who took his advice. But not before Wall Street had figured out how to package subprime dog shit into self-destructing weapons of mass destruction that inadvertently imploded the global financial system.

And here we are again in the midst of a monetary fueled housing bubble:

So, what to do? The Fed bailed out Wall Street on the systemic meltdown they had created. AND paid them in full on their bets that the whole shit show would collapse. Then the Fed lowered interest rates to 0% and started pumping money directly into financial markets. Thus inventing socialism for the rich.

Fast forward to today and the Idiocratic beliefs that attend this post-pandemic bubble are first and foremost the ubiquitous faith that assets are worth whatever price the last fool paid for them. In addition, the belief that central banks are omnipotent. The other obligatory delusion is the studied ignorance of accumulated market fragility which is a net result of 13 years of continuous monetary bailouts.

At this lethal juncture, low volatility is conflated with low risk. Which has been proven to be an asinine assumption over and over again these past years and decades. Nevertheless, serial bailouts have kept this critical hypothesis alive.

Introduction To Volatility Targeting"Volatility is the most common risk metric of a stock. The main aim of the volatility targeting technique is to manage the portfolio’s exposure in such a way that the volatility of a portfolio is as close to the target value as possible. In other words, to ensure that the amount of dollar risk remains the same. To do this, the portfolio manager has to increase or decrease the amount of leverage, depending on the volatility"

Here we see that S&P 500 volatility is at a three year low:

Here we see that these algo controlled "volatility targeted" markets are making new all time highs this week amid the lowest number of stocks confirming this rally in 18 years. I calculate the number of stocks BELOW the 50 day moving average at every S&P all time high:

Below we now see that this past month June 2021 officially has all top ten highest option skew values in recorded history going back 30 years. Which from a statistical point of view is a Black Swan outlier event. In a random distribution, the probability that a top ten skew value will appear in a given month over 30 years is 1 in 36 (2.7%). The chance that all ten would be in the same month is .027 to the tenth power: (0.00000000000000027). In other words, "someone" is making massive bets that this gong show is ending.

As a reminder, skew represents deep out of the money option bets on a "Black Swan" market event:

"The SKEW index is a measure of potential risk in financial markets.

SKEW values generally range from 100 to 150 where the higher the rating, the higher the perceived tail risk and chance of a black swan event"

As we see the highest values happen to be the last four trading days of the best half since 1998:

Amid all of this asinine risk, it's ironic that FINRA finally got around to fining Robinhood for causing "widespread and significant harm to customers" during the Gamestop debacle. Which incited the suicide of one young trader who woke up to an erroneous -$720,000 account balance.

However, in the meantime since that debacle in late January, the Robinhood platform has added record numbers of new users, Congress has officially sanctioned Reddit pump and dump schemes, and margin debt has reached new all time highs. In other words, this fine is totally meaningless with respect to addressing the increasing fragility of market structure. A fragility that is hidden behind the collapsed volumes and volatility that have been extremely profitable for options market makers.

Suffice to say that the number of young people who are now at risk of waking up to negative account balances is quite unthinkable. All aided and abetted by a profoundly corrupt financial services cartel that has now captured regulators and effectively neutered them.

Which ensures that they are always barking up the wrong tree. Penalizing the pissant Robinhood platform while the real risk is officially sanctioned.

"This week alone, 18 companies are seeking to go public, including Chinese ride-hailing company Didi Global in what will be the biggest IPO of the year...That’s the most companies in a single week since 2004"

June was also the busiest single month since August 2000"

The majority of the returns are going to the (pre-IPO) institutional buyers.”

FOMO [Fear of Missing Out] is the biggest thing"

(FYI, my IPO data includes SPAC IPOs)https://stockanalysis.com/ipos/statistics/

The stock market just closed out its (Second) best first half since 1998 which directly preceded the LTCM (Long Term Capital Management) debacle. We also learned back in April that more money poured into stocks since the election than in the prior 12 years combined. Since that time, inflows have continued their record pace - ETF inflows are almost at a new record only six months into the year. What we are witnessing is the ideal recipe for panic meltdown.

{kind=link}

Going back to 1998, Long Term Capital Management (LTCM) was a massively leveraged hedge fund managed by financial PhDs who were considered geniuses on Wall Street and in academia. The collapse of their fund in the second half of 1998 almost brought down the global financial system. They had made various asinine assumptions about the correlation of risk assets that were true most of the time but categorically failed when markets went into meltdown mode following the 1997 Asian Financial crisis. In other words they were oblivious data miners who assumed the past could be endlessly extrapolated into the future, hence they blindly ignored all imminent signs of risk and focused solely upon statistical probabilities. Which is the way all of today's quantitative/algorithmic trading programs work. Ignorance is bliss. More on that later. The book that described the entire debacle was called "When Genius Failed". Hence, the title of this post. The net result of that collapse was a massive Fed bailout that inadvertently lubricated the melt-up phase of the brewing Dotcom bubble.

The Dotcom bubble itself was abided by the asinine belief that valuations, profits, and even sales no longer matter. All that matters is internet page views aka. "eyeballs". That new "business model" consisting of massively unprofitable companies going public at a record rate soon found the natural limit of fools with money to burn on worthless IPOs. At that point, the "smart money" rotated to the Big Cap safe havens - Microsoft, Intel, Dell, and Cisco. And then those stocks imploded bringing down the entire casino.

A divergence very similar to what is happening today:

{kind=link}

When the Fed sponsored DotCom bubble collapsed, they lowered rates to a multi-decade low 1.5% which set off the melt-up stage of the brewing housing bubble. At the time, Fed Chairman Greenspan lauded the "financial innovations" taking place in the subprime lending market and he encouraged borrowers to load up on adjustable rate mortgages (ARMs). ARMs had been previously unpopular in the U.S. market because they shift all interest rate risk from the lender to the borrower, offset by a minor interest rate reduction. Within months, Greenspan jacked up rates 17 meetings in a row and imploded everyone who took his advice. But not before Wall Street had figured out how to package subprime dog shit into self-destructing weapons of mass destruction that inadvertently imploded the global financial system.

And here we are again in the midst of a monetary fueled housing bubble:

So, what to do? The Fed bailed out Wall Street on the systemic meltdown they had created. AND paid them in full on their bets that the whole shit show would collapse. Then the Fed lowered interest rates to 0% and started pumping money directly into financial markets. Thus inventing socialism for the rich.

Fast forward to today and the Idiocratic beliefs that attend this post-pandemic bubble are first and foremost the ubiquitous faith that assets are worth whatever price the last fool paid for them. In addition, the belief that central banks are omnipotent. The other obligatory delusion is the studied ignorance of accumulated market fragility which is a net result of 13 years of continuous monetary bailouts.

At this lethal juncture, low volatility is conflated with low risk. Which has been proven to be an asinine assumption over and over again these past years and decades. Nevertheless, serial bailouts have kept this critical hypothesis alive.

Introduction To Volatility Targeting"Volatility is the most common risk metric of a stock. The main aim of the volatility targeting technique is to manage the portfolio’s exposure in such a way that the volatility of a portfolio is as close to the target value as possible. In other words, to ensure that the amount of dollar risk remains the same. To do this, the portfolio manager has to increase or decrease the amount of leverage, depending on the volatility"

Here we see that S&P 500 volatility is at a three year low:

{kind=link}

Here we see that these algo controlled "volatility targeted" markets are making new all time highs this week amid the lowest number of stocks confirming this rally in 18 years. I calculate the number of stocks BELOW the 50 day moving average at every S&P all time high:

{kind=link}

Below we now see that this past month June 2021 officially has all top ten highest option skew values in recorded history going back 30 years. Which from a statistical point of view is a Black Swan outlier event. In a random distribution, the probability that a top ten skew value will appear in a given month over 30 years is 1 in 36 (2.7%). The chance that all ten would be in the same month is .027 to the tenth power: (0.00000000000000027). In other words, "someone" is making massive bets that this gong show is ending.

As a reminder, skew represents deep out of the money option bets on a "Black Swan" market event:

"The SKEW index is a measure of potential risk in financial markets.

SKEW values generally range from 100 to 150 where the higher the rating, the higher the perceived tail risk and chance of a black swan event"

As we see the highest values happen to be the last four trading days of the best half since 1998:

{kind=link}

Amid all of this asinine risk, it's ironic that FINRA finally got around to fining Robinhood for causing "widespread and significant harm to customers" during the Gamestop debacle. Which incited the suicide of one young trader who woke up to an erroneous -$720,000 account balance.

However, in the meantime since that debacle in late January, the Robinhood platform has added record numbers of new users, Congress has officially sanctioned Reddit pump and dump schemes, and margin debt has reached new all time highs. In other words, this fine is totally meaningless with respect to addressing the increasing fragility of market structure. A fragility that is hidden behind the collapsed volumes and volatility that have been extremely profitable for options market makers.

Suffice to say that the number of young people who are now at risk of waking up to negative account balances is quite unthinkable. All aided and abetted by a profoundly corrupt financial services cartel that has now captured regulators and effectively neutered them.

Which ensures that they are always barking up the wrong tree. Penalizing the pissant Robinhood platform while the real risk is officially sanctioned.

"This week alone, 18 companies are seeking to go public, including Chinese ride-hailing company Didi Global in what will be the biggest IPO of the year...That’s the most companies in a single week since 2004"

June was also the busiest single month since August 2000"

The majority of the returns are going to the (pre-IPO) institutional buyers.”

FOMO [Fear of Missing Out] is the biggest thing"

(FYI, my IPO data includes SPAC IPOs)https://stockanalysis.com/ipos/statistics/

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Actualización de cartera 2021 – Primer semestre

Ya estamos de nuevo a mitad de año, con el aire acondicionado a tope, el precio de la luz disparado y con otra actualización más de cartera. Antes de nada, quiero mandar un saludo especial a los que, como yo, les ha tocado pagar hoy a Hacienda (por la declaración de la renta). También quiero … Sigue leyendo Actualización de cartera 2021 – Primer semestre →

Categorías: Blogs y opiniones de economia en ingles

Casualties of Perfection

The key thing about evolution is that everything dies. Ninety-nine percent of species are already extinct; the rest will be eventually.

There is no perfect species, one adapted to everything at all times. The best any species can do is to be good at some things until the things it’s not good at suddenly matter more. And then it dies.

A century ago a Russian biologist named Ivan Schmalhausen described how this works. A species that evolves to become very good at one thing tends to become vulnerable at another. A bigger lion can kill more prey, but it’s also a larger target for hunters to shoot at. A taller tree captures more sunlight but becomes vulnerable to wind damage. There is always some inefficiency.

So species rarely evolve to become perfect at anything, because perfecting one skill comes at the expense of another skill that will eventually be critical to survival. The lion could be bigger; the tree could be taller. But they’re not, because it would backfire.

So they’re all a little imperfect.

Nature’s answer is a lot of good enough, below-potential traits across all species. Biologist Anthony Bradshaw says that evolution’s successes get all the attention, but its failures are equally important. And that’s how it should be: Not maximizing your potential is actually the sweet spot in a world where perfecting one skill compromises another.

Evolution has spent 3.5 billion years testing and proving the idea that some inefficiency is good. We know it’s right.

So maybe the rest of us should pay more attention to it.

So many people strive for efficient lives, where no hour is wasted. But an overlooked skill that doesn’t get enough attention is the idea that wasting time can be a great thing.

Psychologist Amos Tversky once said “the secret to doing good research is always to be a little underemployed. You waste years by not being able to waste hours.”

A successful person purposely leaving gaps of free time on their schedule to do nothing in particular can feel inefficient. And it is, so not many people do it.

But Tversky’s point is that if your job is to be creative and think through a tough problem, then time spent wandering around a park or aimlessly lounging on a couch might be your most valuable hours. A little inefficiency is wonderful.

The New York Times once wrote of former Secretary of State George Shultz:

His hour of solitude was the only way he could find time to think about the strategic aspects of his job. Otherwise, he would be constantly pulled into moment-to-moment tactical issues, never able to focus on larger questions of the national interest.

Albert Einstein put it this way:

I take time to go for long walks on the beach so that I can listen to what is going on inside my head. If my work isn’t going well, I lie down in the middle of a workday and gaze at the ceiling while I listen and visualize what goes on in my imagination.

Mozart felt the same way:

When I am traveling in a carriage or walking after a good meal or during the night when I cannot sleep–it is on such occasions that my ideas flow best and most abundantly.

Someone once asked Charlie Munger what Warren Buffett’s secret was. “I would say half of all the time he spends is sitting on his ass and reading. He has a lot of time to think.”

This is the opposite of “hustle porn,” where people want to look busy at all times because they think it’s noble.

Nassim Taleb says, “My only measure of success is how much time you have to kill.” More than a measure of success, I think it’s a key ingredient. The most efficient calendar in the world – one where every minute is packed with productivity – comes at the expense of curious wandering and uninterrupted thinking, which eventually become the biggest contributors of success.

Another form of helpful inefficiency is a business whose operations have some slack built in.

Just-in-time manufacturing – where companies don’t stock the parts they need to build products, relying instead on last-minute shipments of components – was the epitome of efficient operations over the last 20 years. Then Covid hit, and virtually every manufacturer found itself dreadfully short of what it needs.

Super-efficient supply chains increase vulnerability to any disruption. And history is just a constant chain of disruptions. So you can imagine that we’ll hear stories of companies who increased their earnings by, say, 5% by maximizing supply efficiencies only to see earnings fall 20% or more due to having no slack when trouble hit. We are in the biggest post-WW2 consumer boom and car companies are shutting down production because they’re out of chips. A little inefficiency across the whole supply chain would have been the sweet spot.

Same in investing. Cash is an inefficient drag during bull markets and as valuable as oxygen during bear markets, either because you need it to survive a recession or because it’s the raw material of opportunity. Leverage is the most efficient way to maximize your balance sheet, and the easiest way to lose everything. Concentration is the best way to maximize returns, but diversification is the best way to increase the odds of owning a company capable of delivering returns. On and on, if you’re honest with yourself you’ll see that a little inefficiency is the ideal spot to be in.

Just like evolution, the key is realizing that the more perfect you try to become the more vulnerable you generally are.

Categorías: Blogs y opiniones de economia en ingles

Episode #325: Bhu Srinivasan, Author, Americana, “Is The Entrepreneur More Important Or Is The Movement And Moment More Important?”

Episode #325: Bhu Srinivasan, Author, Americana, “Is The Entrepreneur More Important Or Is The Movement And Moment More Important?” Guest: Bhu Srinivasan is the first-time author of Americana: A 400-Year History of American Capitalism. He’s currently the founder and CEO of SCORETRADE, which is developing the fastest and […]

The post Episode #325: Bhu Srinivasan, Author, Americana, “Is The Entrepreneur More Important Or Is The Movement And Moment More Important?” appeared first on Meb Faber Research - Stock Market and Investing Blog.

Categorías: Blogs y opiniones de economia en ingles

The Long View: Jason Zweig - Temperament is Everything for Most Investors

Categorías: Blogs y opiniones de economia en ingles

Short-term reversal or short-term momentum?

Momentum investors know that in order to exploit the momentum factor it is best to ignore last month’s returns. While stocks that have had positive returns over the last six or twelve months tend to outperform in the coming month or so, stocks that outperformed in the previous month tend to underperform the next. This short-term reversal effect is well known and if you are interested in how big it is, you can download it from Ken French’s database.

Short-term reversal is typically explained with investor overreaction to news that is reversed, once the news has been digested. Stocks thus overreact to positive news and correct afterwards, creating short-term reversals.

Short-term reversal is why momentum investors typically calculate past price momentum as the performance over the last 12 months minus the performance in the previous month to get better results than by just looking at the return over the previous 12 months.

But what if I told you that there is a group of stocks that does not exhibit short-term reversals? What if I told you that this group of stocks in exhibits short-term momentum, that is stocks that outperformed last month continue to outperform the subsequent month?

In a fascinating paper, Medhat and Schmeling show that while the average stock exhibits short-term reversal, the most highly traded stocks exhibit short-term momentum. Only the stocks with low volume in the previous month show short-term reversal. And the differences are so strong that this short-term momentum effect survives transaction costs implementation lags. And they found it not just in the United States but across 22 developed countries.

Short-term reversal and short-term momentum

a.image2.image-link.image2-1183-1456 { padding-bottom: 81.25%; padding-bottom: min(81.25%, 1183px); width: 100%; height: 0; } a.image2.image-link.image2-1183-1456 img { max-width: 1456px; max-height: 1183px; }Source: Medhat and Schmeling (2021).

So far, this is just an observation and there is no clear theory why this happens. It seems that short-term momentum exists in high turnover stocks because these tend to be stocks that have many investors with a large variety of opinions trading in the same stocks. And the divergence of opinions creates and underreaction to news and hence short-term momentum as prices digest news more slowly. But that is just a theory. For now, all we have is a fascinating and very large new stock market anomaly that I will be eager to learn more about.

Categorías: Blogs y opiniones de economia en ingles

Animal Spirits: The Wealthiest Generation

Today’s Animal Spirits is brought to you by Acre Trader, Investing in Farmland. Simplified. Visit acretrader.com to learn more

On today’s show we discuss:

Marc Andreesen is smart

a16z is launching a $2 billion crypto fund

Tital insurance is a scam

The free money in Bitcoin is disappearing

“Risk free” 18%

Jeremy Grantham is bearish

Robinhood IPO delayed

Home prices still climbing

Blackstone is buying h...

The post Animal Spirits: The Wealthiest Generation appeared first on The Irrelevant Investor.

Categorías: Blogs y opiniones de economia en ingles

MISSION ACCOMPLISHED

To read today's Idiocratic news, one would believe that everything is back on track in the economy. Unfortunately, nothing could be further from the inconvenient truth. However, we CAN assume that the Wall Street recovery is complete...

"It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way—in short, the period was so far like the present period"

It's a testament to the attention deficit of this gambling addicted society that they conflate manipulated stock market prices with the underlying economy. For the past 13 years since the 2008 bailout, stocks have rallied at every sign of a weakening economy, because it meant more central bank socialism for the rich. Which also explains from an archaeological standpoint why a global pandemic at the end of the longest cycle in U.S. history was viewed as a reason to go ALL IN.

No surprise, Biden's economic plans have been roundly derided by the right as socialism for the middle class. Zerohedge and their patented inflation hysteria have been at the forefront of this disinformation campaign regarding the economy. When they run short of their own in-house fiction they quote Wall Street's liars to bolster their credibility. Now, at this most parlous juncture they are declaring victory for the GOP states that ended the Federal pandemic unemployment benefits early. They cite a sharp dropoff in unemployment claims as proof that cutting people off from unemployment programs worked. I suggest that declining unemployment claims are a direct result of the programs ending, not proof that the GOP economy is "fixed".

The long-term problem with the U.S. economy derives not from emergency unemployment programs, but instead from the habitual mass layoffs that have attended every downturn of the past several decades. Each time mass layoffs occur, there is far less labor participation in the economy, as people retire early or are forced to take part time jobs. Good jobs are traded for junk jobs. This fact is captured in the Job Quality Index which has been falling for 30 years straight.

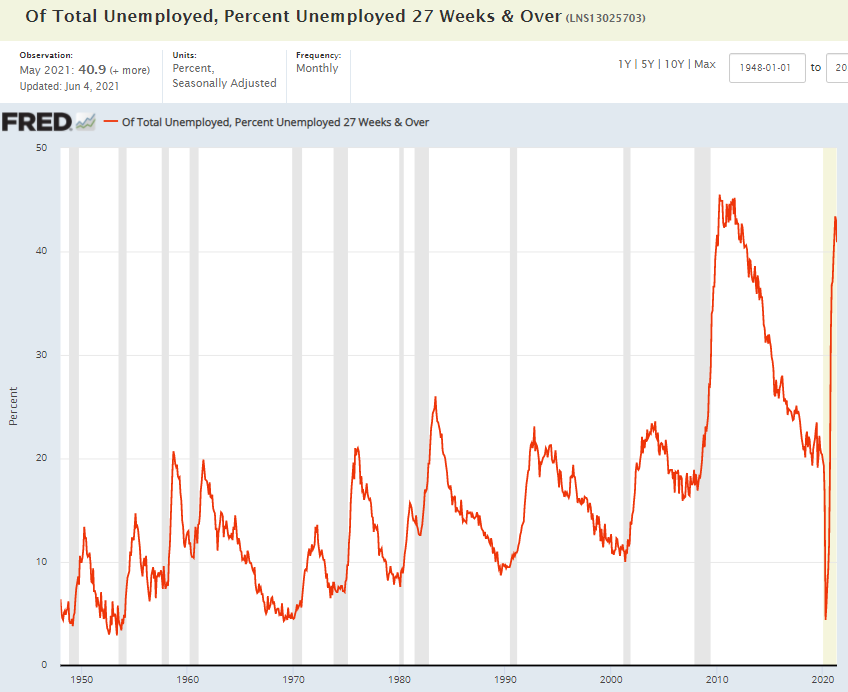

Another way of looking at the problem is via the long term unemployment ratio below:

The % of unemployed over 27 weeks has sky-rocketed back to global financial crisis levels. Which is an indicator of how many people are on the verge of "retiring" early. When they "retire" they will be conveniently removed from the official unemployment rate. Problem solved.

As we see above, what happened during the pandemic is that once again U.S. companies panicked and laid off large swaths of their workforce. Arguably, the ranks of low wage unskilled workers are the easy problem to "fix" as Zerohedge gleefully points out. But, the harder problem to fix will be in the highly paid skilled workforce which is now facing an acute labor shortage that unfortunately won't be fixed by McDonald's help wanted signs.

What do Boeing and GE have in common? Weak balance sheets due to massive stock buybacks. So what did they do in the pandemic? They laid off tens of thousands of workers.

"Aerospace companies relied heavily on layoffs to cut costs and save cash. U.S. aerospace and defense companies have announced more than 115,000 job cuts since the World Health Organization declared the Covid-19 outbreak a pandemic last March"

it’s hard to imagine that many skilled workers would give preference to the aerospace manufacturers that laid them off when the going got tough"

Indeed. Loyalty cuts both ways.

Today's inflation pundits are praying for stagflation, both to prove Biden wrong AND to keep a bid under their collapsing reflation trades. In today's terms they are "right" only in their proven ability to attract legions of useful idiots.

A skill I have yet to obtain.

Sadly, all of this delusion is running on glue fumes. Which means that the REAL test for this skydive into economic pavement is pending global margin call.

At that time I predict a sea change in attitude towards bailing out the rich is on tap. Today's amnesiacs must be reminded of the fact that 13 years of monetary socialism for the rich has only "saved" capitalism by making the divergence between wealthy and poor far greater in the meantime.

I believe that such an unforeseen event will be sufficiently cataclysmic to ensure that apologists for epic greed and criminality are silenced.

For good.

"It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way—in short, the period was so far like the present period"

{kind=link}

It's a testament to the attention deficit of this gambling addicted society that they conflate manipulated stock market prices with the underlying economy. For the past 13 years since the 2008 bailout, stocks have rallied at every sign of a weakening economy, because it meant more central bank socialism for the rich. Which also explains from an archaeological standpoint why a global pandemic at the end of the longest cycle in U.S. history was viewed as a reason to go ALL IN.

No surprise, Biden's economic plans have been roundly derided by the right as socialism for the middle class. Zerohedge and their patented inflation hysteria have been at the forefront of this disinformation campaign regarding the economy. When they run short of their own in-house fiction they quote Wall Street's liars to bolster their credibility. Now, at this most parlous juncture they are declaring victory for the GOP states that ended the Federal pandemic unemployment benefits early. They cite a sharp dropoff in unemployment claims as proof that cutting people off from unemployment programs worked. I suggest that declining unemployment claims are a direct result of the programs ending, not proof that the GOP economy is "fixed".

The long-term problem with the U.S. economy derives not from emergency unemployment programs, but instead from the habitual mass layoffs that have attended every downturn of the past several decades. Each time mass layoffs occur, there is far less labor participation in the economy, as people retire early or are forced to take part time jobs. Good jobs are traded for junk jobs. This fact is captured in the Job Quality Index which has been falling for 30 years straight.

Another way of looking at the problem is via the long term unemployment ratio below:

The % of unemployed over 27 weeks has sky-rocketed back to global financial crisis levels. Which is an indicator of how many people are on the verge of "retiring" early. When they "retire" they will be conveniently removed from the official unemployment rate. Problem solved.

{kind=link}

As we see above, what happened during the pandemic is that once again U.S. companies panicked and laid off large swaths of their workforce. Arguably, the ranks of low wage unskilled workers are the easy problem to "fix" as Zerohedge gleefully points out. But, the harder problem to fix will be in the highly paid skilled workforce which is now facing an acute labor shortage that unfortunately won't be fixed by McDonald's help wanted signs.

What do Boeing and GE have in common? Weak balance sheets due to massive stock buybacks. So what did they do in the pandemic? They laid off tens of thousands of workers.

"Aerospace companies relied heavily on layoffs to cut costs and save cash. U.S. aerospace and defense companies have announced more than 115,000 job cuts since the World Health Organization declared the Covid-19 outbreak a pandemic last March"

it’s hard to imagine that many skilled workers would give preference to the aerospace manufacturers that laid them off when the going got tough"

Indeed. Loyalty cuts both ways.

Today's inflation pundits are praying for stagflation, both to prove Biden wrong AND to keep a bid under their collapsing reflation trades. In today's terms they are "right" only in their proven ability to attract legions of useful idiots.

A skill I have yet to obtain.

Sadly, all of this delusion is running on glue fumes. Which means that the REAL test for this skydive into economic pavement is pending global margin call.

At that time I predict a sea change in attitude towards bailing out the rich is on tap. Today's amnesiacs must be reminded of the fact that 13 years of monetary socialism for the rich has only "saved" capitalism by making the divergence between wealthy and poor far greater in the meantime.

I believe that such an unforeseen event will be sufficiently cataclysmic to ensure that apologists for epic greed and criminality are silenced.

For good.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Why I don’t read the Wall Street Journal

There is a bit of a divide in the community of professional investors about financial news media like the Wall Street Journal, the Financial Times, or The Economist. Arguably, all these publications are extremely valuable to retail investors and people who are working in the financial industry but are not directly involved in investment decision making or security analysis. For these people, these publications are a good way to get information about markets. But for the folks who have an enormous amount of specialised financial data at their fingertips and spend their days analysing that data, there is nothing these publications can write that is truly new.

This is why I don’t read these publications. Not because they are bad (they aren’t) but because I cannot get an edge as an investor from anything that is written in them. The pushback, I get to this opinion is usually that it is worthwhile reading these publications to know what “the street” is thinking and how market sentiment swings. If you believe this, then let me show you some data that hopefully will convince you that you can just as well give up on reading that stuff.

Ioanna Lachana and David Schröder from Birkbeck College in London have looked at thousands of articles in the Wall Street Journal and the financial website Seeking Alpha about US stock markets to measure how they influence the S&P 500. They created a variable that measure how optimistic or pessimistic an article is about the market and tried to find out if there is an impact on S&P 500 returns the next day, or further in the future. Using a variable that measures net pessimism (which I have reversed into a net positivism variable) they found that more positive articles in the WSJ or on Seeking Alpha lead to higher S&P 500 returns the next day. But before you get excited, the impact is a whopping 0.05% to 0.1% difference in returns. And if you go beyond one day, there is absolutely zero impact (the chart below isn’t empty, it’s just that all the bars are zero).

Impact of more positive articles in financial media on the S&P 500

a.image2.image-link.image2-474-924 { padding-bottom: 51.298701298701296%; padding-bottom: min(51.298701298701296%, 474px); width: 100%; height: 0; } a.image2.image-link.image2-474-924 img { max-width: 924px; max-height: 474px; }Source: Lachana and Schröder (2021)

Using the New York Times archive, they could even show how the influence of news media on the market declined over time.

Declining impact of news articles on S&P 500 returns the next day

a.image2.image-link.image2-482-918 { padding-bottom: 52.505446623093675%; padding-bottom: min(52.505446623093675%, 482px); width: 100%; height: 0; } a.image2.image-link.image2-482-918 img { max-width: 918px; max-height: 482px; }Source: Lachana and Schröder (2021)

Since the 1960s markets, reading the news to get a “feel for the market” has been a waste of time. If you aren’t a professional investor, you get important information out of financial news, but if you are a professional, you are wasting your time reading that stuff. You cannot get an advantage from the FT, the Economist, or the WSJ.

Categorías: Blogs y opiniones de economia en ingles

Episode #324: Edward McQuarrie, Santa Clara University, “Sometimes Stocks Beat Bonds, Sometimes Bonds Beat Stocks”

Episode #324: Edward McQuarrie, Santa Clara University, “Sometimes Stocks Beat Bonds, Sometimes Bonds Beat Stocks” Guest: Edward F. McQuarrie is a Professor Emeritus in the Leavey School of Business at Santa Clara University. He received his Ph.D. in social psychology from the University of Cincinnati in 1985. Date Recorded: […]

The post Episode #324: Edward McQuarrie, Santa Clara University, “Sometimes Stocks Beat Bonds, Sometimes Bonds Beat Stocks” appeared first on Meb Faber Research - Stock Market and Investing Blog.

Categorías: Blogs y opiniones de economia en ingles

Facebook Continues Upward Trajectory

Facebook, Inc. (FB) saw continued growth over the past year, outperforming the S&P 500 and rising by approximately 66.3% compared to the S&P’s gain of about 32.5% since the beginning of 2020. However, hedge funds were actively selling the stock in the first quarter. Still, the company climbed to a ranking of sixteen on the WhaleWisdom Heatmap.

Facebook is a multinational conglomerate and provider of communication services that offer an online application and technologies to connect friends, families, and businesses. Facebook also provides products and services beyond its social networking platform and has acquired other companies such as Instagram, WhatsApp, and Giphy over the past several years.

{kind=link}

Hedge Funds Are Selling

Despite solid growth, Facebook saw declines in share ownership, with hedge funds and 13F filers dumping the stock in the first quarter of 2021. Overall, hedge funds decreased their aggregate holdings by about 1.5%, to approximately 439.2 million shares from 446 million. Likewise, the aggregate 13F shares held fell to about 1.85 billion from 1.89 billion. Of the hedge funds, 60 created new positions, 283 added to an existing holding, 40 exited, and 264 reduced their stakes.

{kind=link}

Additionally, long-term 13F metrics demonstrate an overall upward trend in stock prices over the past fifteen years, indicated investors have not only bought shares in Facebook but have held for the long-term.

{kind=link}

Encouraging Multi-year Figures

Analysts expect to see earnings rise over the next three years, with growth rates spanning 15.5% to 29.6%. These year-over-year estimated increases could bring earnings per share up to $17.69 in 2023, from $13.07 for 2021. In addition, it is estimated that year-over-year revenue growth will range from 16.9% to 34.2% between 2021 and 2023; this could bring revenue to $160.8 billion by 2023.

Analysts Share Favorable Price Targets

Facebook recently held its annual F8 developer conference, which brought together developers across the globe to celebrate innovation and share the latest on Facebook technologies. Following the annual meeting, analyst Brent Thill of Jefferies Equity commented that Facebook is building a comprehensive toolset beyond core advertising to bring greater value. Thill maintains a Buy rating on the stock and a $385 price target. Ivan Feinseth of Tigress Financial Partners LLC also gave Facebook a Buy rating and initiated a twelve-month target price of $430. Feinseth noted that Facebook continues to benefit from the massive growth in digital advertising.

Positive Outlook

Facebook’s potential continues to grow. Hedge funds may be selling, but analysts are optimistic about the stock, and investors appear to be long-term oriented. Moreover, estimates through 2023 are encouraging for investors, making the company an attractive investment for investors willing to hold shares long-term.

Categorías: Blogs y opiniones de economia en ingles

Why Europe leads on climate change

Reducing and mitigating the negative effects of climate change is first and foremost a technological problem. Yes, we all need to change our behaviour but in the end, these behavioural changes themselves are made easier if we have convenient technology to support them. Until a few years ago, the range of battery electric cars was so low and their price so high that no one except the biggest ecomentalists would spend the money to buy one. Today, the cost of electric cars is almost at par with internal combustion engine cars and their range has greatly expanded. As a result, people like me are going electric.

When it comes to electric cars, the revolution was driven by a US entrepreneur and Europe and China had to catch up. But in general, it is astonishing how little of the innovation in green technology is developed in the United States. When it comes to global leadership on greenhouse gas emissions reduction it is not the innovative United States or rising China, but sleepy old Europe that is leading the charge.

In my view, this is not a historical accident but a result of cultural and institutional differences that makes European countries much more likely to fight climate change.

The first observation I want to make is the institutional difference between how the economies in Europe, China, and the United States are run. The US is the land of the belief in free markets. Regulation is as light as possible and to be avoided at all costs. When it comes to green technology, this is a serious drawback. Green technology is expensive to develop, capital intensive, and takes a very long time to become cost-competitive with traditional technologies. It simply is not possible like in the software space to develop a new product and then roll it out aggressively to capture a large market share in a few years and then become profitable. Unless you have a backer with nearly limitless resources and an iron will to see this project through, a free-market economy will kill off this kind of innovation long before it can become competitive.

China with its guided capitalism would theoretically be a natural habitat for technological revolutions because the government could finance and protect emerging new technologies for long enough to make them competitive. However, over the last couple of decades, the Chinese government was mostly interested in improving the living standards of the Chinese as rapidly as possible. This meant focusing less on innovation and more on copying technologies from the West and reproducing them at a lower cost. It is what has turned South Korea and Japan into global industrial powerhouses. Now that China is at the crossroads where it has to escape the middle-income trap, the country focuses intensively on becoming a global leader on 21st century technologies like batteries and other green technologies. In my book on geo-economics, I have written in detail how China tries to do this and what that means for the coming decade. So, for the last two decades, China was out of the picture as well.

This leaves us with Europe and its focus on social market economy where regulations play a bigger role to avoid market failures. In Europe, it is common to introduce subsidies for new technologies or to foster market changes. Thus, subsidizing wind and solar energy until it became competitive was nothing new to European policymakers. And if it created jobs, politicians were quick to jump on board. IRENA reports that the total number of jobs in solar wind and biomass in 2019 was 9.5 million, up from 5.6 million in 2012. In the EU 1.25 million jobs depended on these technologies in 2019, almost twice as many as in the United States.

The second key reason for European leadership was cultural. The United States is the land of “move fast and break things”. It is the place where entrepreneurs can develop a new technology or a new product without much red tape, put it out in the market and see what happens. If it kills a few people or makes infringes on their privacy rights, so be it. The worst that can happen is you get sued, but most of the time, that doesn’t happen, or nobody can prove that it was your fault. This is why the United States is the land of Facebook and Google, of low food quality standards and fracking. Meanwhile, most European countries act based on the cautionary principle. First, you have to prove that your product does no harm, then you can roll it out. This “do no harm” principle is so ingrained in Europe that it is for example one of the three key principles for the new EU taxonomy on sustainable economic activities. If you run a business and you want it to be accredited as a sustainable business, you have to show that it does no harm to the environment and the climate.

This cautionary principle in Europe means that there is a much higher incentive to develop new technologies that solve existing or future problems. I tend to say that America has never met a problem that it couldn’t solve by throwing more money at it or using more energy. And in my view, most of what Silicon Valley does is solve problems for young white men with disposable income. Silicon Valley doesn’t solve hunger, fight malaria (or Covid, for that matter) or inequality because the people who work there aren’t hungry, have health insurance and money.

In a free-market economy, developing green technology puts you at a first-mover disadvantage. Much better to wait until someone else has made the investment and developed the technology until it is ready for primetime. But if everybody thinks that way, nobody ever tackles that problem. Unless you have a couple of stupid Europeans who care about more than just making money.

Categorías: Blogs y opiniones de economia en ingles

The Case for a Longer-Term Oil and Gas Bull Market

Published June 2021 The oil and gas sector has been one of the most disliked and out-of-favor sectors among investors for a while now. Some traders have played with it short-term due to the global reflationary rebound, but few investors are willing to commit to it long-term at this point. It’s nothing more than a […]

Categorías: Blogs y opiniones de economia en ingles

This Week in Women

Return to Office? Some Women of Color Aren’t Ready

“This was the first year that I haven’t had my hair commented on and touched without permission in my professional life,” she said. “I actually like not having to go into the office and be constantly reminded that I’m the only Black woman there.”

Simone Biles Tackles Her Trolls In New, Empowering Short Film Series From SK-II

Biles’s episode is just one wit...

The post This Week in Women appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

Letters to the editor

A selection of correspondence

Categorías: Blogs y opiniones de economia en ingles

Doge Upside Resistance Targets

Below are the upside resistance targets based on the work of Edson Gould. The targets, based on the $0.18 low, are: $0.43 $0.52 $0.60 Each of the upside resistance targets are levels to expect that the price will either trade … Continue reading →

Categorías: Blogs y opiniones de economia en ingles

Páginas

Custom Search