Se encuentra usted aquí

www.valuewalk.com

Breaking news and in-depth analysis on everything hedge funds and value investing

Actualizado: hace 3 años 5 meses

SVN Capital Fund H1 2021 Commentary

SVN Capital’s commentary for the first quarter ended June 30, 2021.

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Warren Buffett Series in PDF

Get the entire 10-part series on Warren Buffett in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

Dear Partner,

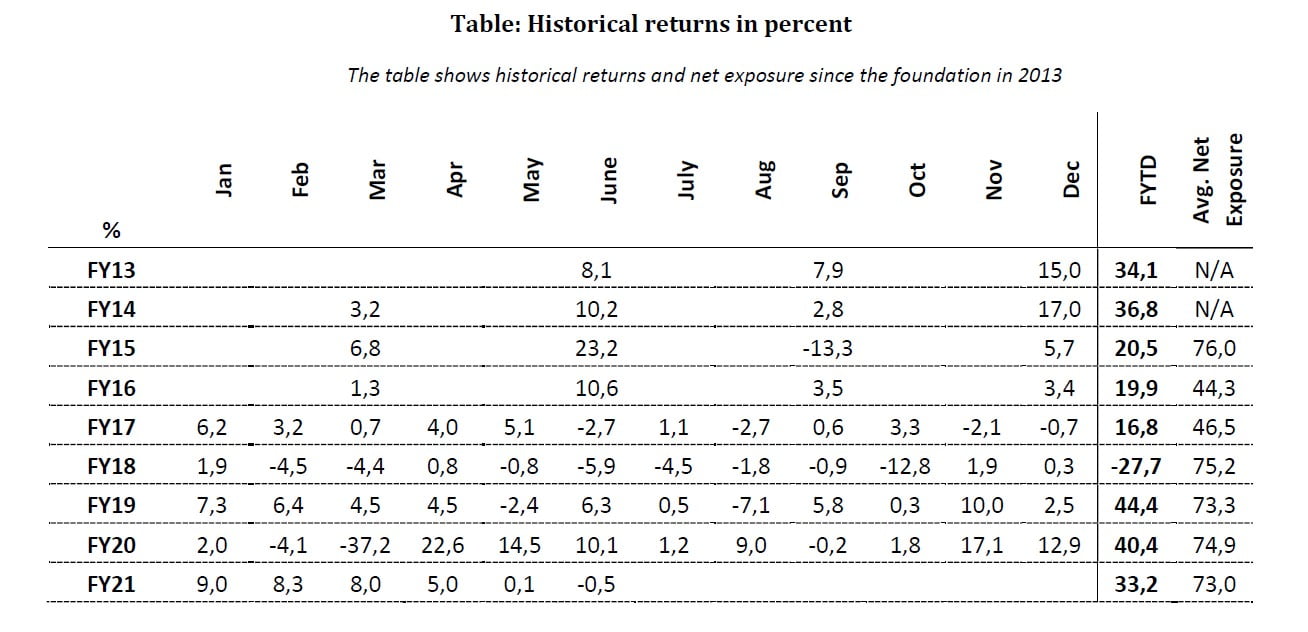

SVN Capital Fund’s portfolio returned 16.7% gross and 15.3% net of all fees in the first half of 2021. Your return will be different depending upon when you invested.

In the following pages, I will walk you through changes to the portfolio, the top three holdings, and market musings. Before I get started with the portfolio, please allow me to digress a bit to talk about investing lessons from mountain climbing, specifically the 8,000ers.

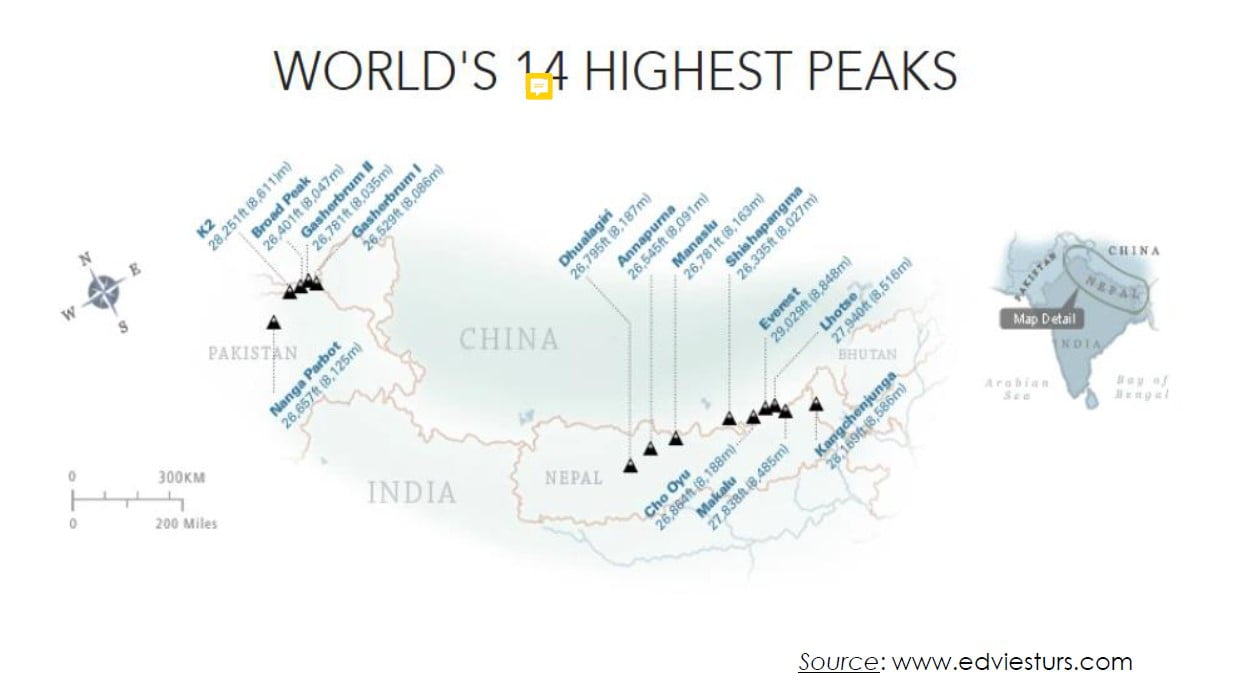

We All Have Our Own AnnapurnaOn a hot summer day in Rockford, IL, after a grueling three-set Boys-18 tennis match that my son won, I decided to take him to the local public library to cool down before getting back on the court for his next match. Flipping through an old stack of Rockford Register Star, a local newspaper, an article celebrating a local son caught my attention. “Ed Viesturs makes history on highest peaks” (July 21, 2013). Ed is the only American to have reached the summit of all fourteen 8,000-meter (26,247 feet) peaks in the world...without the aid of supplemental oxygen. I am not sure why, but I was immediately intrigued by this man and his many accomplishments. Perhaps it is because, as Robert Pirsig says in his wonderful book Zen and the Art of Motorcycle Maintenance, “The allegory of a physical mountain for the spiritual one that stands between each soul and its goal is an easy and natural one to make.”

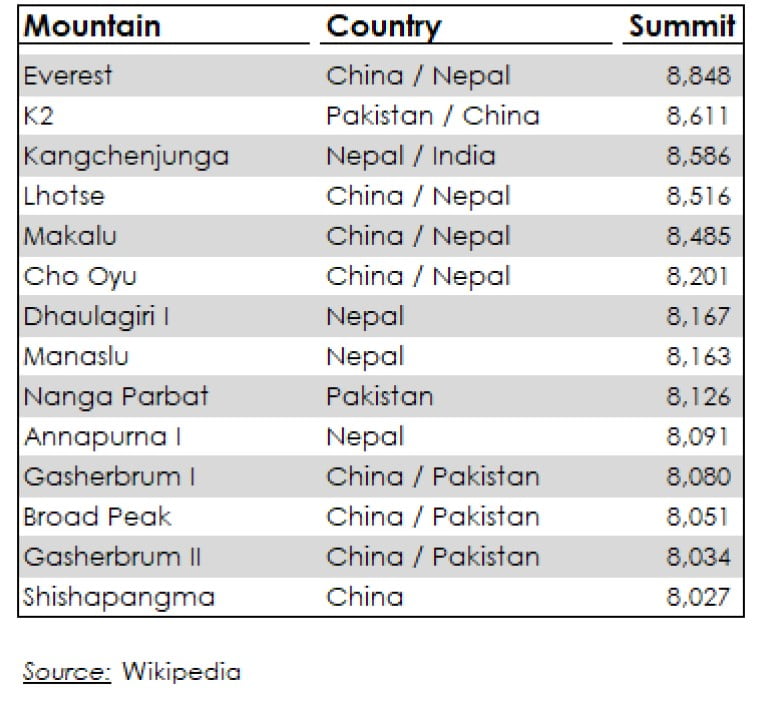

While Mt. Everest is the tallest mountain in the world at 8,848 meters (29,029 feet), 13 other mountains tower more than 8,000 meters above sea level; all of them are in the Himalayan and Karakoram Mountain ranges in Asia (see Appendix 1). Maurice Herzog, a French alpinist, reached the summit of Annapurna, 10th tallest, in 1950 and wrote a book by the same name. Annapurna is said to be the most influential book on mountain climbing ever written. Ed Viesturs was inspired by this book.

Rockford, IL, located about 90 miles west of Chicago, IL, is the epitome of a Euclidean plane, with no hill or bump within a 100-mile radius. Growing up in this flatland, Ed decided that he wanted to climb Mt. Everest. More than 10 years after moving to Seattle, WA, for college, Ed accomplished his dream of summitting Mt. Everest. During his 18-year career, he reached the summit of Mt. Everest five times, three of which were without supplemental oxygen. On May 12, 2005, Ed Viesturs capped his climbing career with the ascent of Annapurna, which had started it all for him as a high-school student in Rockford, IL, and happens to be one of the world’s most treacherous peaks.

Ed’s philosophy, his approach to the craft of mountain climbing, and his strategy for accomplishing his “Endeavor 8,000”1 goals, resonated well with me and how I think about the craft of investing. For example, when Starbucks asked for his motto that it would print on eight million coffee cups, he described his philosophy as follows:

I’ve learned in climbing that you don’t “conquer” anything. Mountains are not conquered and should be treated with respect and humility. If we take what the mountain gives, have patience and desire, and are prepared, then the mountains will permit us to reach their highest peaks. I believe a lot of things are like that in life.

Intense preparation and patience are tools I deploy in managing the investment portfolio.

Fortunately, Ed is a prolific writer (he has written three books about his experience as a mountain climber) and spends his time as a motivational speaker covering topics such as risk management and decision-making under pressure2. While there are many lessons in these materials, I would summarize his principles down to the following:

- Safety Before Success. In 2002, after his second unsuccessful attempt at summitting Annapurna, he said, “In our own evaluation, the level of risk was increasing and the margin of safety was decreasing. There are some risks involved when you climb these mountains, but …it’s ultra-important that you have a very conservative attitude.”

- Independent Judgment. Listening to the mountain is a unique skill that helped him avoid potential disasters over the years. He said:

Among my 30 expeditions, I’ve reached the summits of 8,000ers an even 20 times. But that means that I had to—or decided it was only safe to—turn back 10 times…And four of those 10 turnarounds came when I was within 350 vertical feet of the top. I’m also proud of the fact that I have never turned around because of lack of preparation, strength, or desire. It was always the conditions that caused me to pause and retreat.

- Risk Management. In 1996, a statistically minded journalist had concluded that, based on conditional probability, Ed’s risk of death increased with every attempt at an 8,000-meter summit, just as risk rises in a game of Russian roulette with a gun with one bullet and six chambers. Ed responded to the journalist through his wonderful book No Shortcuts to the Top that “…the odds do not accumulate after each climb, as they do for a set of successive pulls of a trigger. Each expedition is separate from the previous one. If I learn something from a previous climb and become a better mountaineer—smarter, faster, stronger, more efficient—then the next climb will be safer. The risk actually goes down.”

These are some of the core tenets of my own investing style at SVN Capital. Margin of safety is the focus as I consider the business risk, financial leverage risk, and valuation risk of any investment. Even after spending several months researching a particular investment, if I’m not convinced about the opportunity, then I “turn around” and get back to base camp. Fortunately, knowledge gained from “climbing” (researching) a business is cumulative and helps me become a better “climber” (analyst and portfolio manager).

In the last sentence of the book Annapurna, Maurice Herzog says, “We all have our own Annapurna.” It is a great metaphor for life, which is a series of peaks and valleys. It certainly is for mine and SVN Capital’s.

After a quiet second half of 2020, I added two new businesses to the portfolio in 2021. Both are outside the US. One of the unique aspects of our fund is our ability to invest in great businesses around the world. Irrespective of the geography, I look for the following features in our portfolio companies:

- businesses I can understand;

- high returns on incremental capital and the ability to reinvest at a similar or better rate;

- honest, competent management teams with “skin in the game”; and

- reasonable valuations.

The first one is Evolution AB in Stockholm, Sweden. In late March 2021, I wrote about this company which you can find here.

Evolution ABEvolution AB (STO:EVO): Stockholm, Sweden-based Evolution is the leading Business-to-Business (B2B) provider of “live” casino systems to operators. Here are a couple of updates to my March write-up.

First, in April 2021, the company made a €460 million acquisition of Australia-based Big Time Gaming Pty Ltd. While the size of the deal is small relative to the size of EVO, this acquisition is expected to further widen its lead in the slots market. Evolution is already a behemoth in its space, but it’s growing at breakneck speed. Consider the following two data points: 1) the three-year average free cash flow growth was 90%; and 2) free cash flow in 2020 was higher than the revenue it generated in 2018.

Second, as a Malta-based operation, EVO currently incurs ~5% in taxes. Under the guidance of the Biden administration, a global minimum tax of ~15% has gained momentum. As it takes shape, and as the company expands in the US, I expect the company’s taxes to go up. Despite the potential tax headwind, I believe EVO has terrific growth potential—particularly in the US and Asia—and is trading at an attractive valuation relative to its long-term earnings potential.

Automatic Bank ServicesNext is Tel Aviv, Israel-based Automatic Bank Services Limited (TASE: SHVA). Electronic payment systems are some of the most profitable businesses in the world. Businesses that act as toll booths, collecting from the trafficking commuters and needing little to no capital, generate high returns; Visa (V) and Mastercard (MA) are two good examples. Automatic Bank Services Limited (SHVA), trading on the Tel Aviv stock exchange in Israel, is the only card network operator in Israel, much like V and MA here in the US. Thanks to my friends Pat Srinivas, a fellow University of Chicago alum, for bringing this idea to my attention, and Adi Soglowek in Tel Aviv, Israel, for helping me with due diligence during the pandemic.

The company was founded in 1978 as a private company but was controlled by five Israeli banks. Due to certain regulatory changes in Israel, these banks were required to sell down their interest to a maximum of only 10% of the outstanding shares. SHVA was taken public in 2019, with four Israeli banks owning 10% each. Later, V and MA bought 10% each. As a result of this structural change, public float remains low.

The following description of the business model of V and MA from 2014 accurately captures the business model of SHVA today3.

At their core, these businesses act as a “toll road” upon which any card-based payment has to “travel”: transaction data has to be “switched” (authorized, cleared, settled) by the network before it is passed between acquirer/issuer/merchant. As the number of transactions in a (successful) card network increases exponentially, the operator earns an increasing return on the (relatively) fixed investment which cleared the network in the first place.

To act as the “toll booth” in the Israeli payment ecosystem, SHVA collects transaction-based fees (charges assessed per transaction; 2 Agorot/transaction4) and infrastructure-based fees (charges assessed to connect the point-of-sale terminals in shops to the system; 15 or 19 Shekels/month/terminal).

Israel is a small country with only 9.0 million people; but it has an advanced economy GDP per capita of $43,600 and a growth rate of approximately 3.5% per year. However, when it comes to cash vs. credit card spending, Israelis exhibit a developing-economy preference for Shekels over cards. For example, only 38% of transaction volume in Israel is handled through credit and debit cards, compared to the US where almost 70% of transaction volume is card based. I believe there is significant room for credit and debit card usage to increase in Israel and for SHVA to collect more tolls.

Following are some of the reasons I believe the stock continues to trade at an attractive valuation.

- SHVA is a microcap company with a low public float, as referenced above.

- SHVA trades on the Tel Aviv stock exchange and files its financials in Hebrew before they get translated into English several weeks/months later.

- Mr. Moshe Wolf (CEO, 64 years of age) has announced his retirement and the company has yet to announce his successor.

Despite these issues, I like the monopoly toll collector with a significant growth tailwind, generating a healthy return on capital while maintaining a balance sheet with excess cash.

PortfolioWhat a difference a year makes! In the midyear 2020 letter I said:

At midyear, the best that can be said is that the first great wave of the pandemic appears to be abating, and the economy is slowly reopening. We are here, of course, as a result of the worst global public health crisis in a century—in response to which, the world locked down, putting its economy into a kind of medically induced coma.

While not fully recovered, the global economy is certainly out of the medically induced coma as of midyear 2021. It feels good to be able to meet with family and friends again. It is quite satisfying to see most of our portfolio companies adapt well to the new reality and show improved operating results. Standouts include Newell Brands Inc., which improved its free cash flow in 2020 by ~50%, Italy-based DiaSorin S.p.A. (see below), and KKR & Co. Inc. (see below).

A few of our companies made major capital commitments in 2020 through acquisitions. DiaSorin announced the acquisition of Luminex Corporation for $2.1 billion in April 2021, Evolution announced the acquisition of NetEnt AB for $2.4 billion in June 2020, Intuit announced the acquisition of Credit Karma for $7.8 billion in February 2020, and KKR acquired Global Atlantic Financial Group for $4.7 billion in July 2020. Poland-based LiveChat Software returned ~100% of its free cash flow as dividends, and Verisign returned ~100% of its free cash flow through share repurchases.

Travel is one area that has not fully recovered but is poised to do well as economies reopen. Two companies within our portfolio felt the brunt of the pandemic: UK-based InterContinental Hotels Group, which franchises Holiday Inn and other branded hotels; and HEICO Corporation (see below), whose Flight Services Group segment sells spare parts to airlines. Overall, our portfolio of businesses did exceptionally well in the post-pandemic world, and the trend continues.

We currently own 11 investments. Cash is less than 1.0%.

The top five holdings account for approximately 60% of the portfolio. Our portfolio is concentrated and geographically diversified. 55% of our portfolio is listed in the US, while the rest is spread among Sweden, Italy, Poland, Israel, and the UK. Of course, what matters is not where these companies are listed, but where they generate their revenue and incur costs. In aggregate, our portfolio companies generate approximately 50% of their revenue in North America while the rest is geographically spread even more widely than the countries listed above.

Here is a brief overview of three of the top five positions, arranged alphabetically:

DiaSorinDiaSorin S.p.A. (BIT:DIA): Turin, Italy-based DiaSorin is a global leader in the laboratory diagnostics market. In vitro diagnostics are tests done to detect the presence of certain molecules that are indicative of certain diseases in a patient’s biological fluids such as blood, urine, and cerebrospinal fluid. Such fluids are put in a test tube (hence the term “in vitro”) with some chemical substances to create a reaction. DiaSorin provides such reagent kits (chemical substances) for conducting more than 130 different tests in laboratories and hospitals. The company is active in two areas of in vitro diagnostics: Immunodiagnostics (~75% of revenue), which detects particular disease molecules with the use of antibodies, and Molecular Diagnostics (~15% of revenue), which detects the DNA and RNA that are specific to certain diseases.

DiaSorin is a highly profitable diagnostics company that has doubled its annual revenue and more than tripled its free cash flow while generating ~15% cash return on capital over the last 10 years. However, with the onset of the global pandemic, most diagnostic testing ceased except for COVID-19. DiaSorin, an innovative and opportunistic company, developed two molecular diagnostic tests and three immunodiagnostic tests for COVID-19 in 2020. While the average revenue growth over the previous nine years was 6.5%, in 2020, the company grew its revenue by almost 25% and generated cash return on capital of 18.2%, much of it from COVID-19 tests! The market reacted favorably, and the stock was up ~46% in 2020.

However, in 2021, DiaSorin has been the worst performer in the portfolio declining by approximately 6.0% YTD. Perhaps the market’s reaction is due to businesses and countries reopening, as well as some of its competitors releasing their own COVID-19 tests. However, unlike some of its COVID-testing competitors, DiaSorin has a diversified portfolio of tests for diseases like latent tuberculosis, the hepatitis variants, Lyme Disease, and many more. Management has consistently highlighted the company’s capabilities well beyond COVID-19. Historically, the company has grown through acquisitions and partnerships. In April 2021, the company announced its biggest acquisition to date—Luminex Corporation (LMNX) for $2.1 billion in cash. This acquisition, expected to close in Q3 2021, will bulk up its multiplex molecular diagnostics segment, which I believe will be a strong driver in the future. I have added to the name opportunistically during the year.

HEICOHEICO Corporation (NYSE:HEI): HEICO is a diversified aerospace and defense component supplier. It operates through two segments. In the Flight Support Group (FSG) segment, it manufactures aircraft parts for sale directly into the aftermarket via third-party parts manufacturer approval (PMA). In the Electronics Technologies Group (ETG), it sells to defense, space, and healthcare companies.

I added HEICO to the portfolio during the early stages of the pandemic in 2020 and wrote about it in the mid-year 2020 letter, which you can find here. Before the pandemic, the FSG segment, which sells directly to airlines and maintenance, repair, and operations, was the bigger of the two segments, generating almost 60% of total revenue. With the onset of the pandemic, this segment was hit hard. In the most recent quarter, which ended on April 30, 2021, the company announced an improvement in revenue and margins in this segment, much of it due to increased flight activity as vaccinated individuals resumed leisure travel.

As more airlines nurse their financial wounds on their way to recovery, I expect them to find HEICO’s products, sold at a significant discount to original equipment manufacturers’ cost, to be attractive.

Historically, the company has grown through acquisitions; it completed one in 2021 and has completed five in the past year. In this pandemic-impacted travel market, the company is being selective and is finding high-quality targets of various sizes.

Even though the stock has almost doubled from its low during the pandemic, I find the PMA business, unique acquisition strategy of not acquiring 100% of the target, decentralized operations, valuation, and cash-flow-focused culture of this owner-operated company to be attractive.

KKRKKR & Co. Inc. (NYSE:KKR): KKR is one of the largest alternative asset managers in the world, with $367 billion in assets under management, but it is better known for its private equity business which is only one of 26 strategies that it manages.

Asset management has been compared to farming: raise capital, put it to work, cultivate, and then harvest. While the fund is operating (putting it to work and cultivating, which is usually seven to 10 years), KKR gets a management fee (~2% of the fund/year) and an incentive fee (cultivating and harvesting, ~20% of profits over a specific hurdle rate). The bigger the fund and the better the performance, KKR gets to collect a healthy management and incentive fee.

The alternative asset management industry, which is currently $14 trillion, has grown at 11% CAGR5 over the last six years, while KKR has grown at almost 22% over the same period. One of the reasons for the industry’s growth is due to the superior return profile and lower reported volatility when compared to traditional public equities. One of the reasons for KKR’s growth is its ability to execute each one of the steps in the farming analogy above, and to do so well. For example, KKR expects to raise more than $100 billion in 2021/2022. In terms of “cultivating,” KKR announced the acquisition of Global Atlantic, a leader in annuities, for $4.7 billion, increasing its permanent capital base. I expect this owner-operated asset manager to continue growing for a long time to come.

A typical strategy takes about seven to 10 years to reach maturity before it starts generating a healthy incentive fee. The management fee has grown at a 15% CAGR over the last six years, while the incentive fee has grown at a 42% CAGR over the last three years. At KKR, almost 50% of the strategies are less than six years old, setting up a significant fee-growth opportunity in the future.

Even though the stock has gone up 3x since the pandemic in 2020, I believe KKR is one of the most attractive businesses within the portfolio; it has a significant asset growth tailwind, immense opportunities to grow many of the existing strategies to scale, and to reinvest in new strategies.

Market Musings:Inflation is the current bugaboo as it relates to investing. According to the media, it is the next “crisis” that will lead the equity market to the next crash. With equity markets, there is always an impending crisis, never a period of peace and quiet. We have had a few of these crises over the last couple of years: COVID-19, the presidential election, oil price decline…into negative territory, excessive monetary stimulus, excessive fiscal stimulus, and much more. Since the pain of a loss is twice as intense as the pleasure of a gain, and because the media is ever-present in our lives to remind us about the upcoming crisis, it is difficult to not worry about it. After all, the S&P 500 stayed flat over 11 years from 1967 to 1978 (Oct 1967: 95.66…Dec 1978: 96.11), one of the periods of sustained inflation, bordering on hyperinflation, in the country’s history. The topic has seeped into many of my recent conversations with investors and friends.

No country can continue to grow its debt faster than its GDP growth rate. Since the financial crisis, the Fed has been trying to shoot for 2% inflation while keeping interest rates close to zero. We are in the midst of an unprecedented experiment in both fiscal and monetary policy, the outcome of which remains impossible to forecast. The possibility that we have overstimulated the economy was highlighted this spring by a significant increase in prices across commodities, homes, and much more. After a sharp rise in the bellwether 10-year US Treasury rate from 0.50% in 2020 to 1.75% by spring 2021, it has now retreated to around 1.40%.

With prices rising followed by interest rates, many say that the future is here and inflation has arrived. Some even say that it is not temporary. For me, it remains an open question whether the recent increase in prices is merely a response to pent-up demand, or whether it will persist and usher out the low-inflation environment to which the markets have grown accustomed. One does not want to read too much into short-term phenomena like these.

But first, how does the stock market react in an inflationary period? The simple answer is, “not well.” Ben Carlson, a prolific writer on financial markets observed the following6:

{kind=link}

Why is that? In its simplest terms, the value of any business is the sum of all its future cash flows, discounted back to the present at an assumed discount rate. This discount rate is a function of interest rates, which ultimately respond to inflation. The same stream of future earnings is worth more in a low-rate, low-inflation environment than in a higher one. Stock prices come under pressure as inflation rises for two reasons: 1) the possible lag between the time when companies’ costs rise and when they can raise prices and pass it to their customers; or 2) the increase in the discount rate at which the market discounts their future cash flows.

So, how do we hedge against inflation? Warren Buffett has written extensively on this topic and described inflation as a “gigantic corporate tapeworm.” In a FORTUNE article from May 1977, he said, “The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures.” His recommendation is to own “wonderful” businesses, defined as those that do not need much capital for future growth (capital-light) or good brands that can maintain their price discipline.

Our portfolio is well-endowed with capital-light businesses. For example, all the software businesses—Automatic Bank Services (SHVA) in Israel, Evolution AB (EVO) in Sweden, LiveChat Software (LVC) in Poland, and Intuit (INTU) here in the US—are capital-light. EVO and INTU also happen to be popular brands in their respective industries. Most of the companies that I am currently researching also happen to be capital-light. A final point on this topic is that great companies wage constant war against rising costs by innovating and becoming more productive. That, I believe, is ultimately the best hedge against inflation.

I am excited about the collection of quality businesses we own; and I am just as excited about many of the quality businesses I am currently evaluating. I continue to remain patient and invest with a long-time horizon.

Please be in touch with any and all questions and concerns. In the meantime, thank you for giving me the privilege of serving you.

Sincerely,

Shreekkanth (“Shree”) Viswanathan

APPENDIX 1 (function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});{kind=link}

{kind=link}

The post SVN Capital Fund H1 2021 Commentary appeared first on ValueWalk.

Categorías: Blogs y opiniones de economia en ingles

Symmetry Invest A/S 1H21 Commentary

Symmetry Invest A/S commentary for the second half ended June 30, 2021.

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Series in PDF

Get the entire 10-part series on Charlie Munger in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

In this newsletter, we will take a closer look at the effect of optimizing work processes and how to use social media as an advantage instead of a disadvantage. In addition, we will look at how we believe a management's ability to allocate capital should be assessed in a growth company.

H1 2021:{kind=link}

As always, returns and portfolio updates are sent out to shareholders monthly via the website.

{kind=link}

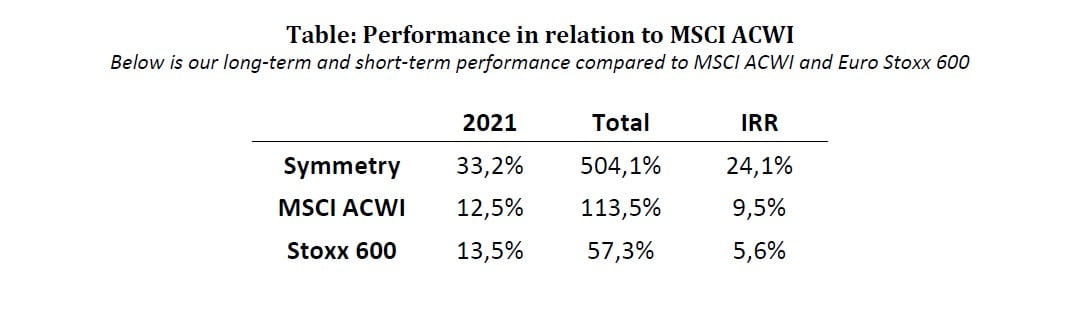

Our returns in the first half of 2021 were once again very satisfactory. Both in absolute and relative terms, compared to the rest of the market. Even more satisfying is the fact that our returns stemmed from a wide range of equities, and not just a few good outliers. The most important factor for our returns has been our adaptability. In the middle of last year, and towards the end, we made solid returns from our bet on online companies, but as the autumn drew closer, we shifted over more and more to classic value stocks, such as Cambria Automotive, Protector Forsikring, etc. As we also noticed that inflation could become a problem, we chose to buy commodity contracts as a hedge. We are not macro experts at Symmetry, so our goal is not to time the market based on the overall picture. We try to keep an eye on market trends and continuously rebalance and hedge our portfolio considering the scenarios we see unfold. As I’ve mentioned earlier, we try to create an “all-weather” portfolio that can perform in most market conditions. It also means that we never went all-in on eCommerce last year, that we have not gone all-in on the green agenda or have completely switched to classic value stocks such as banks etc. We try to always have a little of each in the portfolio and rebalance when we see significant shifts. In this way, we hope to be able to perform well under most market conditions.

Deep work:Throughout the spring, I had the pleasure of reading Carl Newport's fantastic book "Deep Work". As I consider myself a constant student, I always work on finding ways to optimize my daily life and make Symmetry's and my own productivity greater. As can also be seen from our work and research on Franklin Covey, "human behavior" is an area we spend a lot of time studying.

In our H1 2020 newsletter (Q2 2020 Newsletter) I reviewed how sleep, exercise, diet and a good family life could be a strong reason to improve the productivity at work. In addition, I reviewed some initiatives that could help with productivity improvements during working hours. After reading "Deep Work" I have been able to take this to a whole new level.

Deep Work is fundamentally a book about the importance of being able to do in-depth work with high concentration and solid output by focusing 100% on specific tasks and removing all outside noise.

”…this understanding is important because it provides a neurological foundation for why deliberate practice works. By focusing intensively on a specific skill, you’re forcing the specific relevant circuit to fire, again and again, in isolation. This repetitive use of a specific circuit triggers cells called oligodendrocytes to begin wrapping layers of myelin around the neurons in the circuits – effectively cementing the skill. The reason, therefore, why It’s important to focus intensely on the task on hand while avoiding distraction is because this is the only way to isolate the relevant neural circuit through useful myelination. By contrast, if you are trying to learn a new complex skill (say, QXL database management) in a state of low concentration (perhaps with Facebook open), you’re firing to many circuits simultaneously and haphazardly to isolate the group of neurons you actually want to strengthen.”1

The investment business is one of the most dynamic out there. Share prices are moving like crazy on a daily basis and there is an almost constant flow of news, opinions and new data that can influence things. This can lead to the feeling of never wanting to miss out, i.e., constantly being up to date with everything. But by constantly seeking new input to already specified ideas, not enough space is given to seeking out new ones. One of the things I have done far more of is to focus exclusively and intensively on one individual tasks at a time. Previously, I could listen to a conference call while building an excel sheet. I thought that I could kill two birds with one stone and complete the tasks faster. But the end result was often that it took longer to make the excel sheet and I did not listen properly to the conference call.

Today I make sure to have several hours where I only focus on specific areas such as reading 3-5 annual reports for a new company back-to-back, listening to a lot of conference calls in a row etc.

Another solution I use is to turn off ALL the push notifications on my phone. That included email, apps, social media and even text messages. If people want my attention, straight away, they will have to call me. Otherwise, I have to actively choose to access the various channels to use them.

The book also puts great emphasis on the use of social media and the way it distracts us in everyday life:

If you can find some extra benefit in using a service like Facebook – even if it’s small, then why not use it? I call this way of thinking the any-benefit mindset, as it identifies any possible benefit as sufficient justification for using a network tool. The problem with this approach, of course, Is that it ignores all the negatives that come along with the tools in question. These services are engineered to be addictive, robbing time and attention from activities that more directly support your professional and personal goals. The use of network tools can be harmful. If you don’t attempt to weigh pros against cons, but instead use any glimpse of some potential benefit as justification for unrestrained use of a tool, then you’re unwittingly crippling your ability to success in the world of knowledge work”. 2

Those who know me know that I am a big fan of twitter in terms of networking, finding potential investment ideas and sharing news about Symmetry. However, I can easily recognize and agree with Carl Newport's point about the tendency to defend the use of various apps by the positive qualities they have, without regarding the negative ones. If you do a proper cost/benefit analysis, most people will probably find that most of the time is a pure waste of time.

“But part of what makes social media insidious is that the companies that profit from your attention have succeeded with a masterful marketing coup. Convincing our culture that if you don’t use their products, you might miss out”. 3

This is one of the reasons why it’s so hard to turn off the apps. What if I receive an important email? What if there’s news on Twitter that I miss? What if my friends are writing something on Facebook that I would like to see? The feeling that someone might have information that you don’t, or that something is going on that you don’t know of is anxiety-provoking for many. I have solved this by explaining to people in my close circle of friends, my investors etc. that if they need me immediately, they must call me. Otherwise, they should expect it to take up to 24 hours before I respond. Other "tricks" I can recommend are:

1) As mentioned, turn off all push notifications.

2) Turn off/hide bookmarks. My initial idea behind having them on my favorite bar was that I would save time by more easily reaching my email, trading platform etc. But in reality, they constantly entice you to access them every time you use your browser to search for relevant information you need for a research project. By hiding them away, you must actively click 2-3 times to access them, which significantly reduces this tendency and allows you to focus on more important tasks.

3) Set a time window in which it’s OK to use social media. As mentioned before, I’m a big fan of Twitter, and therefore I don’t want to shut it down, nor do I think it makes sense for Symmetry to do so. Instead, I have times during the day where I can use the service. Usually I will check the news, email, company updates, twitter feeds, and PMs etc. from 7-9 in the morning before the market opens. This assures me I’m up to date on things that are important to our portfolio. Then I will focus my time on active research and other projects that require my focus. At noon (often around or during lunch) I will skim my emails again. I will also usually do the first check of stock prices around this time. If there is nothing important that requires my immediate focus, I will go back to research again in the afternoon until I go home. When my wife and kids are asleep at night, I will usually take an hour or two answering the day’s emails, read through my twitter feed for important news, answer any PM I might have received during the day, etc. I will also check the closing prices for the stock market to see how the day has gone and whether I should email my broker with trading orders the following day. These procedures have personally helped me free up significant time (6-8 hours daily) to carry out real research and analysis. This has worked for me, although it might not work for everyone. Besides, I'm still not perfect. I still sometimes get to check twitter outside of the set time slots for example, but I have made great progress. And the direction is the important part.

4) Focus on reading, listening, and learning during the morning hours. Personally, I spend this time of day reading reports, financials, analysis, listening to conference calls and taking notes. While in the afternoon I’m usually more engaged in building spreadsheets, talking on the phone, holding online meetings, etc. It has worked well to use the mornings, when the brain is most alert, to absorb information.

5) Take advantage of other activities such as exercising or walking the dog. I often use my jogs or walks with the dog to listen to podcasts or in some cases conference calls. However, it is worth noting that if you do not feel you can take in the information in the meantime, you should not do it.

Another important point from the book is that it is okey to get bored. Said another way; take time to reflect. I have previously mentioned in my newsletter that I think one of the most important edges one can have in the market nowadays is not informational (who has the most data/information) but rather an analytical or in particular a behavioral edge. I therefore agree with Carl Newport about the idea of taking the time to reflect on available information, instead of constantly seeking new information. To give the brain the peace it needs to process information impressions and draw conclusions is an important basis for making the right investment decisions.

In 2013, the British TV licensing authority surveyed television watchers about their habits. The twentyfive- to thirty-five-year-olds taking the survey estimated that they spend somewhere between fifteen and sixteen hours per week watching TV. This sounds like a lot, but it’s actually a significant underestimate. We know this because when it comes to television-watching habits, we have access to the ground truth. The broadcaster’s audience research board, places meters in a representative sample of households. The meters record, without bias or wishful thinking, exactly how much people actually watch. The twenty ive-to-thirty-five-year old’s who thought they watched fifteen hours a week, watched more like twentyeight hours or close to double up”. This bad estimate of time usage is not unique to British television watching. When you consider different groups self-estimating different behaviors, similar gaps stubbornly remain. In a Wall Street journal article on the topic, business writer Laura Vanderkam pointed out several more such examples… Another study found that people who claimed to work sixty to sixtyfour hours per week were actually averaging more like forty-four hours per week…the examples underscore an important point. We spend much of our day on autopilot – not giving much thought to what we’re doing with our time. This is a problem. It’s difficult to prevent the trivial from creeping into every corner of your schedule if you don’t face, without flinching, your current balance between deep work and shallow work, and then adopt the habit of pausing before action and asking, “What makes the most sense tight now”. 4

It’s rather eye catching. People spend on average 15 hours more than they think watching TV, while at the same time working 20 hours less than they think. No wonder many people have no idea where their time is going? When I read this, I made up an example that readers can try on themselves. On a piece of paper, I wrote down how many hours I think I have used my phone over the last 7 days. For those with an iPhone, you can check this by clicking on “screen time”. It was almost shocking how much I underestimated my own use of the phone. Fortunately, I have also changed this greatly, as I will explain later.

On a different topic, the same is true for my kids’ use of iPads. They spend (spent) far more time on them than me and my wife thought. Most parents agree that their kids should not spend too much time on their iPads and computers, and most of them do not think that the kids do. Today we use parental controls that will lock the screens on our kids iPads when they have used up their time. This way they can learn to utilize their assigned time over their days.

I have personally been able to cut down on my screen time with 60-80% over the last few months by a few easy methods:

1) As mentioned before, I turn off all push notifications, i.e., things that attract you to the phone.

2) While in the office, I always keep the phone on a 3–5-meter distance from my workspace. Since I do not receive any notifications (beeps, sounds or vibrations) from text messages or apps, I have no reason to grab it unless someone calls me. Hence, most of the time during work (while in the office), I only use the phone when someone calls me.

3) When I get home, I actively chose to leave my phone in the car. I only have my iWatch (without any apps or email installed) on me, so I can answer potential “emergency” calls. This means that I can have 100% focus on being present with my family when I’m home, and not be tempted to “just take a look at the phone”. It also allows me to justify coming home a little later (and thus freeing up time in the office where I can do real work) because I am actually home when I am at home.

4) Do not put your phone on the bedside table when you go to bed. If you do not have your phone lying at your bedside you will not be tempted to take it. As I brought up in my H1 2020 newsletter, Matthew Walker also mentions this technique in the book “Why We Sleep”, as a way to achieve better sleep. Your subconscious is drawn towards the phone even when you are sleeping if it is right next to it, tempting you to check news in the middle of the night, etc.

Do i sometimes look at the phone while playing with the kids? For sure. Do i sometime have my phone close to my bed? For sure. But have I become significantly better at not doing it? For sure. Investing is all about constant improvements. As the head of Evolution Martin Carlesund would say” we just want to be a little bit better every single day and extend the gap to competition”.

Internal capital allocationOne of the things we increasingly spend time on while investing is studying the companies’ capital allocation. And we don’t think of capital allocation in a traditional sense. Usually, the conversation concerns how the company should work with M&A, buy-backs, dividends, and internal investments. These decisions are of course very important and can be the difference between an 8% or 14% yearly return. What we have found however, is that almost all the companies we invest in always have the best opportunity for capital allocation internally. It is therefore rarely a question of whether they should pay dividends or invest internally. Instead, it is more important for us to understand whether the companies know how to allocate capital internally in the best possible way. The companies we invest in often have opportunities to allocate capital to a 30-100% internal ROIC. We therefore spend time talking to management about their priorities and thoughts on this.

Naked Wines is a great example. They really have 3 areas in the company which they must constantly assess in terms of capital allocation. As Naked Wines grows, they achieve economies of scale in their business. This constantly increases their contribution margins. They must therefore assess how they should relate to these growing margins:

1) Should they keep these increasing margins within the company, deploying the cash internally

2) Should they lower prices on their wine to create a better experience for their Angels, giving them more value for their money

3) Should they raise the price paid to their suppliers, incentivizing them to produce more and better wine for Naked’s platform?

Once they have on their contribution margin, they generate capital to invest. This capital can be invested in getting new Angels to the platform. In sales and marketing, they have many different channels, such as insert marketing (vouchers), digital platform (Facebook etc.), influencers, refer a friend programs, and more. WINE should therefore constantly focus on investing their marketing budget in areas with the highest potential return. Their goal is to invest as much as they possibly can within an LTV/CAC of approximately 2x (5 years). They therefore constantly seek to invest as much as they possibly can as long as they can reach the payback they are targeting. This is regardless of how these investments affect their performance in the short run.

On the other hand, they must assess how much they should invest in fixed expenses. This could be better IT, website development, better customer support etc. These expenses are of course the most difficult to measure ROIC on because they help to improve the overall experience for the business.

But WINE should not only assess ROIC in these areas, they also must understand how decisions in one single area interacts with another. For example, if they choose to lower the prices of their wine or invest in better IT, they will have less money available to acquire more customers. Conversely, it will also make it easier to acquire more customers cheaply when investing in your product. Similarly, investing in more customers will increase the scale of their network, which in turn will free up more money to invest. WINE must constantly assess how they can strengthen these network effects and create the strongest ROIC based on the available capital. At the same time, they must continuously determine if they have so many opportunities in all areas that it would be wise to raise extra capital from shareholders.

We have spent a long time discussing this with CEO Nick Devlin and other people from WINE. Based on this, and our external due diligence in this area, we are 100% convinced that Nick and the team fully understand this. Otherwise, we would not have allocated such a large portion of our capital to WINE.

”There is nothing new on Wall Street or in stock speculation. What has happened in the past will happen again and again. This is because human nature does not change, and it is human emotion that always get in the way of human intelligence”5

Portfolio Update:

Our holdings have, overall, continued to perform well in 2021 which of course also will be reflected in our performance.

We recently made public our latest investment in JDC Group AG. JDC is a stock we expect very much from the coming 3-5 years. We can see a future where this company becomes a multi-bagger. We are super happy to have partnered with Sebastian and Ralph. Below is a link to our Q&A with the management.

https://www.symmetry.dk/wp-content/uploads/2021/06/zoom_0.mp4

And to our news email about the stock:

https://preview.mailerlite.com/g8c2b2

Another stock we mentioned for the first time in H1 2021 was Franklin Covey where we published a report in February. The report and presentation can be found here:

Galleri - SymmetryFranklin Covey has already done well with a return of approx. 40% in just 4 months. Our investment case was most recently confirmed when Franklin Covey reported their Q3 financial statements:

The Q3 report was what I would call a blowout quarter. It was significantly better than what everyone had dared to hope for. People can read my analysis where I estimate that the shares are worth $80, and where I estimate an EBITDA of around 22 in 2021. The current guidance is around 26-27, so it is already markedly ahead of my optimistic dreams. We believe that Franklin Covey has the potential to become a home-run investment. One can see that their unit economics are super strong, and they are firing on all cylinders in terms of hiring new client partners to accelerate sales, making acquisitions to strengthen their platform (Strive) and continuously add more content which strengthens their network effects. We look forward to updating on the case after their Q4 report in November.

Of the other shares in our portfolio, we still have large shareholdings in Gaming Innovation Group Inc (STO:GIGSEK), Naked Wines (LON:WINE), Protector Forsikring ASA (FRA:PR4) and Kambi Group PLC (FRA:7KB).

We were super happy with Kambi's Capital Markets Day they held a few weeks ago. We have always been a little critical of the management's tendency to always underplay themselves too much. It was therefore wonderfully refreshing to see them be more positive about the future. At the same time, they provided a very in-depth review of their technology and why they should have lasting competitive advantages and why they should be able to continue to take market share.

Naked Wines was at first traded down quite heavily on their annual report. The reports were, as we already knew, good, but the company’s guidance for FY22 disappointed the market initially. Since then, the stock has rebounded strongly. This is most likely because people have been able to dig deeper into the case. First of all, we think they are guiding conservatively as they do not know how their customers will react after a full reopening (although the first signs look super good). Secondly, their trading update for the first 2 months was actually very strong. There is thus a 30% growth in sales to existing customers despite very difficult comparative figures. When you also include a currency headwind, it is not hard to imagine that Naked Wines will deliver 15-20% CC growth in FY22 despite very difficult comparative figures. Against this backdrop, their long-term guidance for 20% annual growth does not look strained either. In our opinion, several UK analysts and investors do not properly understand the company. They are disappointed with the high costs, but we see the company's costs as investments that will strengthen the company in the long run.

We still think GiG is way too cheap. This is despite the fact that the stock has already had a nice upturn since our analysis last November. It is therefore still one of our largest holdings. Their Media business is running excellently and growing rapidly, and their platform business is starting to capitalize on the regulatory changes that are happening all around the world while at the same time being profitable. Based on the current share price of around NOK 18, GiG is trading at 8x 2021 EBITDA and 5x 2022 EBITDA. It is absurdly cheap for a company with high organic growth in a structural growth industry.

Protector Forsikring recently presented their Q2 report which again showed that they have good momentum in the business. They managed to maintain a high revenue growth (+20 % organic), an exceptionally strong combined ratio, and a good investment result. At the same time, they are now paying dividends because they are overcapitalizing. They maintain good risk management on their investments and are disciplined to sell when the shares reach fair value. We have a hard time seeing why Protector is still trading at a normalized6 P/E of 6-7 with double-digit organic growth and a dividend yield of approx. 8-10%. Protector could appreciate 100% from here and still trade at a discount to competitors.

The reason that capital markets are, have always been, and will always be inefficient is not because of a shortage of timely information, the lack of analytical tools, or inadequate capital. The internet will not make the market efficient, even though it makes far more information available, faster than ever before, right at everyone’s fingertips. Market is inefficient because of human nature – innate, deep-rooted, permanent. People don’t consciously choose to invest with emotion – they simply can’t help it”7

I wish you all a continued good summer.

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});The post Symmetry Invest A/S 1H21 Commentary appeared first on ValueWalk.

Categorías: Blogs y opiniones de economia en ingles

What Exactly Bitcoin Is And What Is Its Value

People confuse “intrinsic value” with “price” most of the time. Financial history is full of periods when asset groups (tulips, metals, railroads, dotcom etc etc) explode in value only to crash to reality. There are tons of very smart people who believe in cryptos and just as many very smart ones do not. My main problem with it is the prediction fiat currencies fail and cryptos become a “global currency”. If we ever as a world gets to the point major national currencies begin to fail (no, I’m not talking Venezuela, Zimbabwe etc), the debate over cryptos will be irrelevant as my belief is national militaries will be doing their thing at that point (global panic/unrest). We’ve seen this already in every single nation that has ever had a serious currency crisis. So, if it really can’t replace national currencies, then isn’t it really simply a money order with a floating value that can be used for speculation?

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Henry Singleton Series in PDF

Get the entire 4-part series on Henry Singleton in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

The other argument for them is their scarcity (ie governments just can’t “print more”). Again, the issue is we have gone from 1 crypto to more than I can count so the scarcity argument also fails.

One thing is for sure, fortunes will be/have been made and lost with this given the extreme price fluctuations.

Personally, I am not for or against them, I’m just putting money in other places because I admittedly don’t get it and don’t invest in things I do not 100% understand because that is just gambling.

What Is Bitcoin's Value“Davidson” submits:

The markets have lived with Bitcoin adding other crypto currencies since 2014. Many claims have been made, new companies have been created to offer, trade this entity, it has been called a currency, “Gold” and received serious attention by analysts regarding its use and price predictions galore. Crypto-art worth $60mil was just paid for by funds generated by investment returns from Bitcoin. Lost in the discussion is a definition by users as to what exactly Bitcoin is and what is its value. The price history from Coinbase for Bitcoin is even carried on the FRED data site at the St Louis Fed.

{kind=link}

Rob Cheng, CEO and founder of PC Matic, was on “Squawk Box” this morning Thursday, Jul 8, 2021, to discuss how businesses can take action to protect themselves from cybersecurity threats. As part ofhis discussion he made a single comment on Bitcoin which explains much of the hype the media/markets have produced about what is not!

At 3:19minutes into the CNBC interview Cheng says “… right now, as everybody knows, bitcoin is the most popular for ransom wear and other transactions if you knockdown one, the barrier to create another cryptocurrency is quite low.”

Bitcoin is an algorithmic token, created mathematically using computers. It is a blank check and carries no intrinsic value itself. What it is in effect is an electronic bar code that can be attached to digital transactions used to identify the sender’s veracity. In short, an authentication token. It reduces the cost and speed when used in financial transactions when authenticating the value represented in the transaction. As used, a particular Bitcoin carries the history of every past transaction which renews its use as a blank check for the next transaction.

Cryptocurrencies are not currencies which reflect value of their societies, but tokens of transfer which can be reused trillions of times to assure the security of transfer agents. They are easy to make which is what CEO Cheng indicated with his “…the barrier to create another cryptocurrency is quite low.” The question of what they are worth is further complicated in being a token arises as every use imparts additional uniqueness from the last transaction. Without that added uniqueness the next use of a Bitcoin is no longer secure. Who owns this value? With trillions of transactions does every user now have partial ownership?

Bitcoin is not gold, nor currency, nor that unique on their own as they are fairly easy to produce and hundreds of counterfeits are apparently being produce globally. As a token in digital transfer of something to which they can be attached they can be useful to assure the proper transfer occurred. There has potential use as a secure token in currency transfer. This use is being explored by global financial systems.

Does Bitcoin by itself have value? CEO Cheng says it simply, if the barrier to entry is low it is not much more than the value of a slice of white bread in holding together a peanut butter and jelly sandwich.

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});The post What Exactly Bitcoin Is And What Is Its Value appeared first on ValueWalk.

Categorías: Blogs y opiniones de economia en ingles

AutoZone, Inc. (AZO): The Mistakes Of Omission

Whitney Tilson’s email to investors discussing the mistakes of omission; his AutoZone, Inc. (NYSE:AZO) whiff; and Buffett & Munger‘s comments.

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Series in PDF

Get the entire 10-part series on Charlie Munger in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

The Mistakes Of Omission1) These tweets by my friend Yen Liow of hedge fund Aravt Global had me thinking...

AutoZone WhiffAs I look back over my career, I can't think of too many examples in which an investment was so blindingly obvious, but I missed it.

One of the most glaring was auto parts retailer AutoZone. I liked it so much more in early 2001, and I even wrote about it in an article, Three Boring Stocks to Consider. Excerpt:

AutoZone, via its 2,915 stores in 42 states and 13 stores in Mexico, dominates the business of selling car parts and accessories to do-it-yourself customers. The company has solid financials and has demonstrated impressive growth. In FY 00 (ended August 2000), AutoZone had a 6.0% profit margin (up from 5.9% the year before) and 23% return on equity (up from 19% the year before; the figure has ranged from 19% to 31% since 1991). Sales rose 9% in 2000, on a 7.5% increase in stores and a 5% increase in same-store sales. Earnings per share ("EPS") rose 22.7%, thanks to a 9.3% increase in net income and a 10.9% decline in the number of diluted shares outstanding.

Sales and EPS have risen every year since 1990, compounding at an average rate of 21% and 27%, respectively. Analysts project EPS growth of 13% for each of the next two years. Yet AutoZone's stock has been flat for nearly eight years, and at yesterday's close of $27.08, it trades near all-time lows of 13.1 times trailing earnings and 12.0 times analysts' estimates for FY 01.

These characteristics lead me to believe that AutoZone is a good company whose stock is trading at a reasonable price. There are plenty of companies that meet this description. However, I think AutoZone is particularly interesting for three reasons. First, the company is more effectively managing its working capital, freeing up cash. In FY 00, AutoZone reduced its inventory per store by 9%, yet increased sales by 9%. This was the major reason operating cash flow rose 64.6% to $513 million.

Second, AutoZone is using its robust free cash flow – and is even taking on debt – to buy back shares by the bushel. In the past six quarters, the company has spent $898 million repurchasing shares, reducing diluted shares outstanding by 22%. Finally, one has to be concerned about the impact of a slowing economy on any retailer. But AutoZone actually stands to benefit from tough times, as people are both more likely to hang onto their cars rather than buy new ones and are also more likely to do their own repairs rather than pay for a mechanic.

Since then, the stock has risen more than 58 times, from $26.80 to $1,560, as you can see in this chart:

So how much of that did I capture? Precisely none... For reasons I cannot recall, I gave this spectacular idea to my readers – but didn't invest in it myself – ARRRRRHHHHH!

However, it's easy to overlook these mistakes because you tend to forget them – and, if you manage money, your investors never know about them...

Buffett & Munger's Comments2) Even the greatest investors make this kind of mistake. At the 2004 Berkshire Hathaway (BRK-B) annual meeting, CEO Warren Buffett admitted:

The main mistakes we've made – some of them big time – are: 1) Ones when we didn't invest at all, even when we understood it was cheap; and 2) Starting in on an investment and not maximizing it... We're more likely to make mistakes of omission, not commission.

Berkshire Hathaway vice chairman Charlie Munger elaborated at the 2001 annual meeting:

The mistakes that have been most extreme in Berkshire's history are mistakes of omission. They don't show up in our figures. They show up in opportunity costs.

I don't like mentioning the specific companies, because the – you know, we may, in due course, want to buy them again and have an opportunity to do so at our price. But practically everywhere in life, and in corporate life, too, what really costs, in comparison with what easily might have been, are the blown opportunities. I mean, it just – it's an awesome amount of money.

When I was somewhat younger, I was offered 300 shares of Belridge Oil. Any idiot could've told there was no possibility of losing money, and a large possibility of making money. I bought it.

The guy called me back three days later and offered me 1,500 more shares. But this time, I had to sell something to buy the damn Belridge Oil.

That mistake, if you traced it through, has cost me $200 million. And it was all because I had to go to a slight inconvenience and sell something.

Berkshire does that kind of thing, too. We never get over it.

Best regards,

Whitney

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});The post AutoZone, Inc. (AZO): The Mistakes Of Omission appeared first on ValueWalk.

Categorías: Blogs y opiniones de economia en ingles

These Are The Top Ten Large Growth Mutual Funds

Investing in big and established companies is considered to be less risky. This is because shares of established companies are usually less volatile than those of other companies. Thus, if you are starting or learning to trade, then investing in such companies is a good strategy. However, these companies usually command a higher per-share price, putting them out of reach for many retail investors. Thus, one way to invest in these companies is through mutual funds, especially large growth mutual funds. These funds invest in big companies that are expected to grow faster than other large-cap companies. Let’s take a look at the top ten large growth mutual funds.

.first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Ray Dalio Series in PDF

Get the entire 10-part series on Ray Dalio in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

Top Ten Large Growth Mutual FundsWe have looked at the past three years of return data from U.S. News to rank these top ten large growth mutual funds.

- Permanent Portfolio Aggressive Gr Port (PAGDX, 103%)

PAGDX primarily invest in stocks and stock warrants of U.S. and foreign companies that exhibit higher profit potential than the stock market. It has returned 10.58% in the last three months and over 18% in the last three years. The top four holdings of this fund are: Freeport-McMoRan, Twilio, NVIDIA and Lockheed Martin.

- Baron Opportunity Fund (BIOPX, 104%)

BIOPX usually invests in growth companies that benefit from innovations and advancements in technology. This fund primarily invests in equity securities. It has returned 0.82% in the last three months and over 38% in the last three years. The top four holdings of this fund are: Microsoft, Alphabet, Amazon and TripAdvisor.

- Fidelity Advisor® Series Growth Opps Fd (FAOFX, 105%)

FAOFX normally invests in the common stocks of companies it believes show above-average growth potential. This fund may invest in domestic and foreign issuers. It has returned 3.31% in the last three months and over 40% in the last three years. The top four holdings of this fund are: Microsoft, Amazon, Alphabet and Apple.

- Virtus Zevenbergen Innovative Gr Stk Fd (SAGAX, 107%)

SAGAX primarily invests in large-cap stocks, but it does have significant exposure to mid-cap and even small-cap firms. It seems to be more focused on the hardware, telecommunications and consumer services sectors. It has returned -7.87% in the last three months and over 40% in the last three years. The top four holdings of this fund are: Tesla, MercadoLibre, Shopify and The Trade Desk.

- Zevenbergen Growth Fund (ZVNIX, 109%)

ZVNIX usually invests in companies that are industry leaders. This fund may invest in 30-60 stocks of any market capitalization and in IPOs. It has returned -8% in the last three months and over 40% in the last three years. The top four holdings of this fund are: Tesla, Shopify, MercadoLibre and Exact Sciences.

- Transamerica Capital Growth Fund (IALAX, 115%)

IALAX has invested more than half of its portfolio in large-cap companies. This fund has also made significant investments in mid-cap and small-cap companies. It has returned -2.42% in the last three months and over 34% in the last three years. The top four holdings of this fund are: Twitter, Shopify, Amazon and Square.

- Morgan Stanley Inst Growth Port (MSEGX, 120%)

MSEGX primarily invests in companies whose capitalization is within the range of the companies that are part of the Russell 1000® Growth Index. It may also invest in emerging companies. It has returned -1.84% in the last three months and over 36% in the last three years. The top four holdings of this fund are: Morgan Stanley InstlLqdty TrsSecs Instl, Amazon, Square and Shopify.

- Morgan Stanley Insight Fund (CPOAX, 124%)

CPOAX usually puts money in the common stocks of companies within the capitalization range of the companies in the Russell 3000® Growth Index. Along with established firms, it may also invest in emerging companies. It has returned -0.52% in the last three months and over 43% in the last three years. The top four holdings of this fund are: Morgan Stanley InstlLqdty TrsSecs Instl, Amazon, Square and Shopify.

- Baillie Gifford US Equity Growth Fund (BGGSX, 142%)

BGGSX normally invests in the common stocks and other equity securities of companies with their main operations in the U.S. It generally invests in companies with a market cap of over $1.5 billion. It has returned -0.73% in the last three months and over 41% in the last three years. The top four holdings of this fund are: Shopify, Amazon, Wayfair and Tesla.

- Zevenbergen Genea Fund (ZVGIX, 148%)

ZVGIX usually invests in companies that benefit from advancements in technology. This fund normally invests in 20-40 stocks. It may also invest in IPOs. It has returned more than -6% in the last three months and over 40% in the last three years. The top four holdings of this fund are: Tesla, MercadoLibre, Amazon and Shopify.

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});The post These Are The Top Ten Large Growth Mutual Funds appeared first on ValueWalk.

Categorías: Blogs y opiniones de economia en ingles

Global Activism Volumes Dip In The First Half

This week we published Shareholder Activism in H1 2021, our statistical analysis of shareholder activism, short activism, and proxy voting data year-to-date. Here are some of the highlights.

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get Our Activist Investing Case Study!

Get the entire 10-part series on our in-depth study on activist investing in PDF. Save it to your desktop, read it on your tablet, or print it out to read anywhere! Sign up below!

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

Global Activism Volumes DipGlobal activism volumes continued to dip in the first six months of 2021, with the 518 companies publicly subjected to activist demands representing a modest dip on the nearly 600 companies targeted in the same period of last year. Only in the consumer defensive and technology sectors were more companies targeted in absolute terms.

One reason many advisers say that the end of 2020 and the start of this year has been busier is that the proportion of targets valued at more than $2 billion is up four percentage points. Another is that proxy fights have been a focal point of this year’s activity, with increased numbers going to a vote in Europe and Asia and the U.S. practically level when a few late meetings are accounted for (Box, GeoPark, and Genesco fights are ongoing).

As we’ve previously noted, M&A opposition is at elevated levels. Europe and Asia have also seen proportionately higher levels of balance sheet activism, so it’s fair to say that companies are having to deal with more contentious and urgent forms of activism than pre-pandemic.

Less and less activism is professional, however, at least judging by our count of impactful campaigns (those run by investors with a primary, partial, or occasional focus on activism). The proportion of companies targeted in H1 that found one of these investors on the opposite side of the table fell to 47% from 49% last year, making for more unpredictable campaigns.

Meanwhile, activist short sellers have had a field day going after frauds and stock promotions, according to Activist Insight Shorts, while racking up an average one-month campaign return of 10% for the first time. Yet even in that field, campaign numbers are down – perhaps more understandably, given the perilous market.

In proxy voting news from our colleagues at Proxy Insight Online, companies in the consumer and financial services sectors saw a recent record number of pay revolts in H1 2021 (>20% against), while there was also a record number of environmental- and social-related shareholder proposals over the same time period.

For more analysis, look out for The Activist Investing Half-Year Review 2021, in association with Olshan Frome Wolosky, coming soon.

Josh Black, Editor-in-Chief, Insightia