Se encuentra usted aquí

Blogs y opiniones de economia en ingles

Three-Year Anniversary Of Elon Musk’s ‘Funding Secured’ Tweet

Whitney Tilson’s email to investors discussing the three-year anniversary of Elon Musk’s ‘funding secured’ tweet; 100 biggest companies in the world; Freedom Holding Corp (NASDAQ:FRHC): the red flag factory in belize.

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Henry Singleton Series in PDF

Get the entire 4-part series on Henry Singleton in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

Elon Musk's 'Funding Secured' Tweet1) Tesla Inc (NASDAQ:TSLA) CEO Elon Musk posted his infamous "funding secured" tweet three years ago this week:

Of course, he didn't have funding secured, so he got in a lot of hot water with the U.S. Securities and Exchange Commission – but no matter: TSLA shares are up nearly 10 times since then.

While I would have given 100-to-1 odds against this outcome, at least I had the good sense to recognize that this open-ended situation was a bad short (as I said then – and continue to say)...

100 Biggest Companies In The World2) A hat tip to VisualCapitalist for this interesting graphic of the world's 100 biggest companies in 2021 by market cap, showing country and industry:

Freedom Holding: The Red Flag Factory In Belize3) In my January 5 e-mail, I wrote:

My friend Roddy Boyd at the Foundation for Financial Journalism recently exposed one of the most obvious promotions I've seen in quite some time – which has a $3 billion market cap! Freedom Holding: After 'Borat,' the Silliest Kazakh Import of the Century.

Since then, it's even clearer that the company is a promotion at best and fraud at worst, yet the stock is up 30%. Here's Roddy with an update: Freedom Holding: The Red Flag Factory in Belize. Excerpt:

Freedom Holding has some explaining to do.

The financial services firm has quite improbably become one of the fastest growing companies on the planet. It lists its shares on the Nasdaq, is incorporated in Las Vegas, but for all intents and purposes runs its operations mostly in Kazakhstan.

As a December investigation by the Foundation for Financial Journalism showed, Freedom Holding's ballooning profits have resulted from baffling and opaque business practices that its management is not keen to discuss.

Among the arrangements is Freedom Holding's close connection to FFIN Brokerage Services, a Belize-based securities trading firm owned by Timur Turlov. He also is Freedom Holding's billionaire founder and majority shareholder.

Even the most seasoned investor has probably not witnessed related-party transactions of the scope of FFIN's dealings with Freedom Holding.

Last year more than 56% of Freedom Holding's revenue came from FFIN commission payments, and in 2019 they represented over 65%. What Freedom Holding does to earn the commissions is not readily apparent, however. Yet the two companies are so intertwined – Freedom Holding's senior managers use FFIN email accounts – it's not clear the two companies are separate in any real sense.

Let me get this straight... This is a business incorporated in Las Vegas, headquartered in Kazakhstan, which earns the majority of its revenue in commissions from a Belize-based securities trading firm, and earns most of its profits from a unit in Cyprus...

How is this even allowed to trade on a U.S. exchange?

Best regards,

Whitney

P.S. I welcome your feedback at WTDfeedback@empirefinancialresearch.com.

Updated on Aug 13, 2021, 2:51 pm

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});

Categorías: Blogs y opiniones de economia en ingles

The Importance Of Investing For Retirement As Early As Possible

At the beginning of the 21st century most young people are told that social security won’t be there for them when they retire from the work force. Thus, in order to be able to completely retire from the workforce, a person has to invest as early as possible in order to take full advantage of the power of compounding.

if (typeof jQuery == 'undefined') { document.write(''); } .first{clear:both;margin-left:0}.one-third{width:31.034482758621%;float:left;margin-left:3.448275862069%}.two-thirds{width:65.51724137931%;float:left}form.ebook-styles .af-element input{border:0;border-radius:0;padding:8px}form.ebook-styles .af-element{width:220px;float:left}form.ebook-styles .af-element.buttonContainer{width:115px;float:left;margin-left: 6px;}form.ebook-styles .af-element.buttonContainer input.submit{width:115px;padding:10px 6px 8px;text-transform:uppercase;border-radius:0;border:0;font-size:15px}form.ebook-styles .af-body.af-standards input.submit{width:115px}form.ebook-styles .af-element.privacyPolicy{width:100%;font-size:12px;margin:10px auto 0}form.ebook-styles .af-element.privacyPolicy p{font-size:11px;margin-bottom:0}form.ebook-styles .af-body input.text{height:40px;padding:2px 10px !important} form.ebook-styles .error, form.ebook-styles #error { color:#d00; } form.ebook-styles .formfields h1, form.ebook-styles .formfields #mg-logo, form.ebook-styles .formfields #mg-footer { display: none; } form.ebook-styles .formfields { font-size: 12px; } form.ebook-styles .formfields p { margin: 4px 0; }Get The Full Henry Singleton Series in PDF

Get the entire 4-part series on Henry Singleton in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues

(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[0]='EMAIL';ftypes[0]='email';}(jQuery));var $mcj = jQuery.noConflict(true);Q2 2021 hedge fund letters, conferences and more

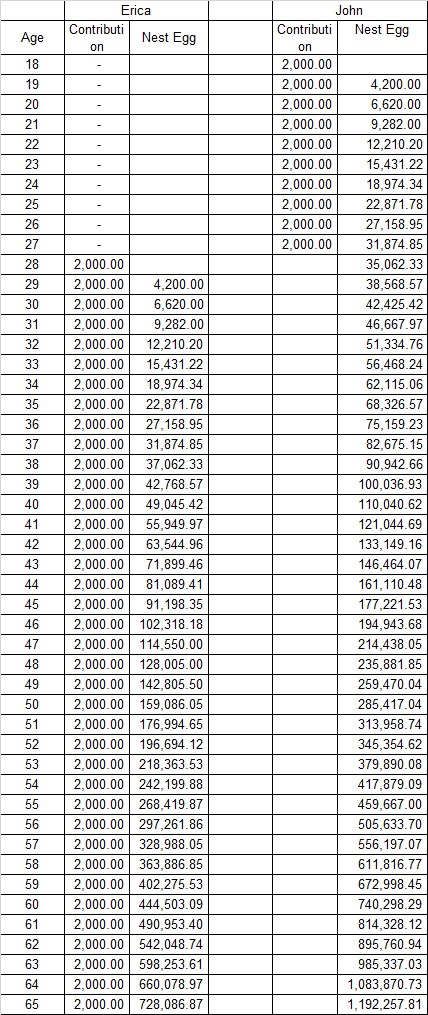

The Benefit Of Investing For Retirement EarlyLet’s follow the story of Erica and John. They both grew up on the same street in the same city. Their mothers gave birth to them at almost the same time. Erica and John went to the same high-school, after which their paths separated. They lost contact with each other for the next 40 years, at which point they found each other on Facebook, and met to reminiscence their childhood and talk about grandkids.

They quickly started talking about their retirement and the amount of money they had each had at the time of their retirement. John, who always saved the extra money he earned from jobs at college and his first job after college, started investing $2000/year in dividend stocks starting at the age of 18 and kept saving and investing the same amount until he was 28. At that point he had so many expenses in order to pay for the needs of his growing family that he couldn’t save anymore. Despite the fact that John couldn’t contribute any more to fund his retirement, he was very good at picking solid dividend growth stocks, and was able to generate annual returns of 10% for the next four decades.

Erica on the other hand had decided that she didn’t want to work in college since she wanted to concentrate on her studies while also enjoying the whole college experience. She then decided to go ahead and get a masters degree after which she was able to get a very good job with one of the largest companies in the USA. She did accumulate a large amount of student debt in the process, which she diligently paid off in a record time after she got her first job. After learning about the importance of saving for your own retirement, she started investing $2000/year in dividend stocks, and was able to also generate 10% in annual returns.

We then fast forward to the age of 65. At age of 65, John's net worth is 1,192,257.81. Erica's networth is $728,086.87 at the age of 65.

Despite the fact that John had invested only $20,000 in total, versus $76,000 that Erica had invested, he was able to achieve a higher amount of wealth because he had taken a full advantage of the power of compounding by investing his hard earned money as early as his freshman year in college. Even though Erica contributed money for over 37 years her nest egg was $400,000 lower than John’s, because she had ten years less to utilize the power of compounding. You could also access the spreadsheet from here.

{kind=link}

The most important point from this exercise is: start investing for your retirement as early as possible! Ask your kids to invest their first paychecks from high school jobs. And most importantly, let the money compound uninterruptedly for as long as possible. And if you want to take full advantage of compounding, Turbo Charge Your Portfolio With Reinvested Dividends.

Relevant Articles:

- Determining Withdrawal Rates Using Historical Data

- Why do I like Dividend Aristocrats?

- The case for dividend investing in retirement

- When to sell your dividend stocks?

Article by Dividend Growth Investor

Updated on Aug 13, 2021, 2:37 pm

(function() { var sc = document.createElement("script"); sc.type = "text/javascript"; sc.async = true;sc.src = "//mixi.media/data/js/95481.js"; sc.charset = "utf-8";var s = document.getElementsByTagName("script")[0]; s.parentNode.insertBefore(sc, s); }()); window._F20 = window._F20 || []; _F20.push({container: 'F20WidgetContainer', placement: '', count: 3}); _F20.push({finish: true});

Categorías: Blogs y opiniones de economia en ingles

Monthly Dividend Stock In Focus: Permianville Royalty Trust

Published on August 13th, 2021 by Bob Ciura Income investors looking to buy oil and gas stocks may want to gain exposure to the Permian and Haynesville Basins. Permianville Royalty Trust (PVL) is an oil and gas producer with properties in these two oil and gas producing areas. Weak oil and gas prices led to […]

The post Monthly Dividend Stock In Focus: Permianville Royalty Trust appeared first on Sure Dividend.

Categorías: Blogs y opiniones de economia en ingles

DELTA is Coming For Your Economic Recovery

{kind=link}

People, people, people: What must I do to get your attention?

Let’s try this:

If we do not radically improve our Vaxx rates ASAP, the entire economic recovery and precariously positioned, somewhat expensive market is put at risk of a 20-30% crash. This one will not have the trillion-dollar stimulus and rapid recovery of the 2020 edition, but rather, will be long, slow, and painful.

Are you paying attention yet?

The threat has been apparent for a while now and I have to admit being perplexed by the soft response from the Biden Admin, and the milquetoast leadership from the Corporate sector.

Are we really going to just ignore the worst Consumer Sentiment numbers in a decade?

We solved for Covid in a record time, and we are about to use artificial antibodies to beat malaria. Can we please do everything possible to use our scientific expertise to get past this pandemic?

~~~

Since the market crash in 2020, I have been steadfastly bullish on, well, everything: The economy, the vaccines, and of course the markets. The pandemic was an externality that caused markets to wobble but it did not end the secular bull market.

But I was at DEFCON 5 in 2006, DEFCON 3 most of 2007, and I went to DEFCON 1 Jan 1, 2008.

Are we going to risk this entire hard-won progress? Are we going to allow millions more to get infected, 1,000s of children die? When the economy returns to its fetal position, when the market gets punched in the throat, do not, under any circumstances, make the claim that “No one could see it coming.”

We are now at DEFCON 3. When a true and new market risk is identified, it is in your self-interest to pay attention.

Previously:

The Economic Risks from Anti-Vaxxers (July 15, 2021)

Missing: Corporate Leadership on Vaccines (August 12, 2021)

End of the Secular Bull? Not So Fast (April 3, 2020)

How Externalities Affect Systems (August 14, 2020)

The post DELTA is Coming For Your Economic Recovery appeared first on The Big Picture.

Categorías: Blogs y opiniones de economia en ingles

Investing Insights: What are the Signs of a Stable Dividend?

Categorías: Blogs y opiniones de economia en ingles

Venture Capital Babies

Welcome to the latest episode of The Compound & Friends, a new podcast from your favorite financial and investing commentators. This week, Michael Batnick, Allison Schrager, Sam Ro, and Downtown Josh Brown discuss:

►The stock market has actually gotten cheaper this year

►Labor has the upper hand

►Baby Bonds and Universal Basic Wealth

►What do we do with Chinese stocks?

►The social aspect of physically going...

The post Venture Capital Babies appeared first on The Reformed Broker.

Categorías: Blogs y opiniones de economia en ingles

10 Friday AM Reads

My end of week morning train WFH reads:

• MacKenzie Scott’s Money Bombs Are Single Handedly Reshaping America With almost $8.6 billion in gifts announced in just 12 months, Scott has vaulted to the tippy top of philanthropic giving, outspending the behemoth Gates and Ford Foundations’ annual grants — combined. But, for someone who is single handedly reshaping nonprofits, Scott, who declined to comment for this story, has only given the public glimpses into the thinking driving her decisions. (Bloomberg)

• Who Wants To Return To The Office? the question isn’t whether working from home will stick — it’s whether executives will take into account the findings of this widespread work-from-home experiment to reevaluate who the system is working for. (FiveThirtyEight)

• The Ultimate Diversifier: What Real Assets Are Gaining in Allocator Portfolios Infrastructure such as bridges and tunnels, plus farmland and other natural resources, is winning new favor. (Chief Investment Officer)

• Let’s Make A Deal: Who’s For Sale In Hollywood And For How Much? Studios behind hits like Godzilla Vs. Kong, La La Land and 8 Mile are ready to be gobbled up — and their price-tags are surprising. (Forbes)

• U.S. Inflation Is Normalizing: The temporary inflation spike associated with reopening is already beginning to fade as prices that were depressed during the pandemic continue to normalize and as consumer demand for motor vehicles continues to moderate.. (The Overshoot)

• This Is a Terrible Time for Savers In an upside-down world of financial markets, expected returns after inflation are at record lows. (New York Times)

• Smart Cities, Bad Metaphors, and a Better Urban Future Shannon Mattern’s new book, A City Is Not a Computer, digs into the data, dashboards, and language that keep people from building better, safer communities. (Wired)

• Reiki Can’t Possibly Work. So Why Does It? The energy therapy is now available in many hospitals. What its ascendance says about shifts in how American patients and doctors think about health care. We were putting adaptogens in our coffee, collagen in our smoothies, jade eggs in our vaginas. We were microdosing, supplementing, biohacking, juicing, cleansing, and generally trying to make ourselves immaculate from the inside out. (The Atlantic)

• America has a long history of vaccination mandates. Why should the worst plague in a century be any different? Ever since George Washington forced his troops to be inoculated against smallpox in 1777, Americans have routinely complied with vaccination mandates. Such mandates are, in fact, as American as apple pie. As Scientific American noted: “Every state and Washington, D.C., requires routine vaccinations, such as for measles, mumps and rubella, as a condition of school attendance.” (Washington Post) see also What Is Biden Waiting For? The Delta variant is making clear what the Administration should have done back in January: mandate vaccines, mandate passports and crack down on the denialists. Now time is running short. (Medium)

• This Boy Band Is the Joy That Hong Kong Needs Right Now The popularity of the group, called Mirror, has offered the city a rare burst of unity and pleasure after years of political upheaval. (New York Times)

Be sure to check out our Masters in Business interview this weekend with Greg Becker, CEO of Silicon Valley Bank. The bank has helped fund more than 30,000 start-ups, 50% of venture-backed tech and life science companies in the US, and 69% of U.S. VC-backed tech + life science companies with an IPO banked with SVB.

There’s a big shift happening in the housing market

Source: Fortune

Sign up for our reads-only mailing list here.

The post 10 Friday AM Reads appeared first on The Big Picture.

Categorías: Blogs y opiniones de economia en ingles

1939 Packard Twelve 1708 Convertible Sedan

Cars from the pre-war era are not where most of my automotive interests lays. But even I can appreciate the mechanical excellence and beauty of this giant Packard Twelve Convertible. It is an important milestone in America’s automobile history.

The car below was purchased new by Colonel Robert R. McCormick, owner of the Chicago Cubs and the Chicago Tribune. MSRP in 1939 was a heady $5,400. It was a chauffeur-driven model, and McCormick’s told his driver to get him from downtown Chicago to his home in Wheaton, Illinois in 45 minutes, which the big V12 was more than capable of.

Powered by a 473ci L-head V12 paired with a column-shifted three-speed manual transmission with overdrive, it made a big 175HP. The massive upright chromed grill, topped by the crystal eagle hood ornament, defines the elegant look of the car. This was the final year for Packard Twelve, the top-of-the-line production body style.

Only 446 were built in 1939, there are a dozen known left of the aptly named Twelve, making this a rare and desirable automobile.

These go for $100-200k, including recent sales og $170,500, $160,600, and $106,400. The version below was bid to $112,200, but RNM and was not sold. You can pick it up for $199k here.

{kind=link}

{kind=link}

Source: Bring A Trailer

The post 1939 Packard Twelve 1708 Convertible Sedan appeared first on The Big Picture.

Categorías: Blogs y opiniones de economia en ingles

Managers and directors will not like this

Before I begin with today’s post, please remember that on Friday’s I focus on quirky and weird results that are not meant to be taken seriously. But if you are a corporate executive or director of a company and can’t laugh about yourself, you shouldn’t read this one.

Okay, now that the people who have no sense of humour left, I want to show you a study that made me smile. There is growing evidence that there is a partial link between our genes and risk-taking in general. As I have described here, people with a specific genetic make-up of the Dopamine Receptor D4 gene take on 25% more risk in all kinds of risk tasks ranging from financial risk-taking to risky activities like para shooting or car racing. They are also more likely to become addicted to drugs and alcohol since they are constantly seeking the next thrill.

However, they are also more likely to become self-employed, entrepreneurs, or achieve high managerial positions in business. Risk-takers take on more risks (duh) in their profession and while many of them fail, there are some that will be successful, and they are rewarded with promotions.

Thus, when two researchers from Yale and Purdue University looked at the correlation between the genetic make-up of corporate managers, CEOs, and directors and other activities and skills, they found that these high achievers all were more likely to engage in riskier activities outside the boardroom. In fact, below is the list of traits that have the highest correlation with being a manager at a corporation. The factors that had the highest correlations were a tendency to speed while driving, drinking alcohol, having many sexual partners and a high metabolic rate (they are literally hot-blooded).

Correlation between being a manager and other activities and skills

a.image2.image-link.image2-492-1292 { padding-bottom: 38.080495356037154%; padding-bottom: min(38.080495356037154%, 492px); width: 100%; height: 0; } a.image2.image-link.image2-492-1292 img { max-width: 1292px; max-height: 492px; }Source: Lin and Zhao (2021).

The above chart shows correlations for all kinds of managers, but what if we restrict the sample to CEOs and directors? Well, the same traits emerge, just this time speeding while driving, having more sexual partners and a high metabolic rate are even more pronounced than other traits.

Correlation between being a CEO or director and other activities and skills

a.image2.image-link.image2-344-1204 { padding-bottom: 28.57142857142857%; padding-bottom: min(28.57142857142857%, 344px); width: 100%; height: 0; } a.image2.image-link.image2-344-1204 img { max-width: 1204px; max-height: 344px; }Source: Lin and Zhao (2021).

So, the next time you meet a sex-crazed, sports car-driving, drinking, and generally ill-tempered CEO, rest assured, he cannot help himself. He was born that way…

Categorías: Blogs y opiniones de economia en ingles

Clips From Today’s Halftime Report

Final Trades: Groupon, Fiserv, Alphabet & more from CNBC.

...

The post Clips From Today’s Halftime Report appeared first on The Reformed Broker.

Categorías: Blogs y opiniones de economia en ingles

Missing: Corporate Leadership on Vaccines

“In every well-ordered society charged with the duty of conserving the safety of its members, the rights of the individual in respect of his liberty may at times, under the pressure of great dangers, be subjected to such restraint, to be enforced by reasonable regulations, as the safety of the general public may demand.”

-Justice John Marshall Harlan, Jacobson v. Massachusetts (1905)

I noted back in February that America’s CEOs were “Having a Good Year.” Not just in their response to a deadly pandemic, or to the logistical challenges of remote work or feeding a nation stuck at home, but even their response to the January 6th attempted coup (Let’s stop pussyfooting around with equivocal words like “insurrection”).

The CEO crew congratulated the legitimate victor, dismissed nonsensical conspiracy theories, froze contributions to elected Capitol rioters, and generally behaved like responsible citizens facing a credible crisis of Democracy. Of course, there was some backsliding – I crossed Toyota off of my list never to be purchased or recommended again – but generally speaking, the corporate sector behaved rather well.

The Vaccine hesitancy that has been stoked by bad actors – an unseemly mix of malicious, opportunistic, and plain old stupid – has presented another chance for the corporate sector to demonstrate leadership. The track record is at best mixed.

If for no other reason than self-interest, it’s time for Corporate America to step up its Vax game – and fast. More than their new hires, companies need to get their customers, aka the public, vaccinated. Otherwise, we are going to be living through an echo of 2020, with Covid as an ongoing and perhaps even long-term drag on the economy. This will affect revenue and earnings at all companies.

Even better, as an exercise, let’s name names. Consider these 10 companies as well-situated to effect real social change relative to Vaccines. But really, any company can show leadership.

Here are the ~10 names I picked.

10 Companies That Can Improve National Vaccination Rates

1. McDonald’s

2. Uber/Lyft

3. Walmart/Target

4. Live Nation/TicketMaster

5. AirBnB

6. Disney

7. American Express

8. Delta

9. Apple

10. USPS

The list above includes companies that interact with the public on a regular basis. They are authoritative in their space, trusted, and above all have some leverage that can be used. It should go without saying that they should require all employees to get vaccinated or stay out of the office (Some jobs warrant firing the unvaxxed, like health care workers, but let’s save that discussion for another day).

What can these individual companies do? Here are some suggestions:

McDonald’s: Already under inflationary price pressures with a clientele that tends to be less well off and less vaccinated, a solution beckons: McDs should use allow inflation concerns to raise their prices across the board by 10% — but then offer a 15% discount for customers providing proof of vaccination. Other retail food establishments like Starbucks (whose upscale customers skew more vaxxed) can also do so. It is a win-win for everybody.

Uber/Lyft: Both ride-hailing services are public, which means there are no more VC subsidized rides. But the App is a great public interactive device, and it should show whether drivers are vaccinated or not. Customers can cancel a non-Vaxxed driver without cost. It is safer, sends a message, and gets drivers vaxxed sooner.

Walmart/Target: It is not fair to turn our frontline retail workers into enforcers; instead, companies can create an innovative program to reward the vaccinated. Proof of vaxx gets you additional bonus points on the company’s points/loyalty program. This works for all loyalty programs, from Credit Cards to Lowes/Home Depot.

Live Nation/TicketMaster: The company originally implied that vaccines were going to be required to buy tickets + attend events, but they have since moved away from this: LISTEN TO ME YOU IDIOTS WHAT ARE YOU GOING TO DO WHEN CONCERTS GET CANCELLED FOR ANOTHER YEAR? It’s so much in your own self-interest to take a leadership role here it’s practically malpractice they have yet to act. Use your mono0ploy power for good for a change.

AirBnB: This one is easy: Get vaxxed if you want to rent one of our homes. The disgusting filthy boorish behavior of AirBnBN guests is bad enough; must you leave your disease-ridden aerosolized virus in the air to boot? Another good use of an app that can provide info for consumers to make safer choices.

Disney: One of the few companies with tremendous ownership of their clients/audience. More than 400 children have died of Covid, it’s easy to position this as protecting the most vulnerable at their parks. They can bonus a free download of a first-run movie to new Disney+ subscribers who provide proof of vaxx.

American Express: A leader in corporate travel, there is an opportunity to provide advice, exhort in email or written communications, and generally advise users it’s much safer to travel if Vaxxed. Alternatively, JPM Chase’s Jamie Dimon can do it, continuing his streak of eating Amex’ lunch at every opportunity.

Delta: I flew Delta last week, and while the experience was good, it felt like a missed opportunity to require vaccines. The airline industry council should discuss and get everyone on board (sorry). It should be an industry-wide issue.

Apple: Long a leader in social issues, the tech giant can use their platform of Apple stores to hasten more vaccinations of their locked-in user base. And it’s the sort of thing that Apple and Google can agree to publicly — maybe even the entire FAANMG contingent.

USPS/Fed Ex/UPS.: The Postal service is not a private company, but it might as well be. It’s an opportunity to use their platform to encourage vaccinations — require all delivery people to be vaxxed and wear some patch or button along the lines of “I’m Vaxxed for your protection.”

Trip cancellation will affect Airlines, Hotels, Credit Cards, Theme Parks

Via Paul Kedrosky

~~~

This is obviously a short-list, and there are lots of other company CEOs who can step up. Leadership requires people of good-will to do the right thing for the greater good.

But there are also issues of self-interest to corporate America. If we don’t get this right, you can expect this economic recovery to be short-lived. Is that enough incentive for you corporate chieftains?

UPDATE August 13, 2021

The usually conservative The Hill writes that the costs for being “choosing not to be vaccinated” should fall on those making that decision:

Health insurance is pooled risk. If people opt-out of getting vaccinated, they are willingly exposing themselves to risks that those vaccinated are not assuming. As such, should they be paying the same health insurance premiums for their coverage? There is a precedent for differential health insurance costs, which exists between smokers and nonsmokers.

One way to manage this in the short term is to have unvaccinated people immediately be required to pay a higher deductible for any care that is primarily due to COVID-19. Cruel? Perhaps. But COVID-19 is cruel, and anyone who does not take precautions to protect themselves and others is being cruel — even unintentionally.

I missed health insurers, but it is another potential solution.

Previously:

America’s CEOs Are Having a Good Year (February 19, 2021)

The Economic Risks from Anti-Vaxxers (July 15, 2021)

The post Missing: Corporate Leadership on Vaccines appeared first on The Big Picture.

Categorías: Blogs y opiniones de economia en ingles

Monthly Dividend Stock In Focus: Chatham Lodging Trust

Updated on August 12th, 2021 by Bob Ciura Real Estate Investment Trusts are popular investments among income investors, and for obvious reasons. They are required to pass along the vast majority of their earnings in order to retain a favorable tax structure, which often results in very high dividend yields across the asset class. You […]

The post Monthly Dividend Stock In Focus: Chatham Lodging Trust appeared first on Sure Dividend.

Categorías: Blogs y opiniones de economia en ingles

Greed is good?

On Tuesday, I wrote about an experiment done by French and Russian researchers that showed that if short-termism becomes more common, then – at least in an artificial market – trends continue to last longer and momentum investing more profitable. One of the key concerns of momentum investing and trend following strategies is that they may lead to bubbles and crashes as longer trends create stocks that are severely mispriced relative to fundamentals. It turns out that the antidote to this risk may be greed.

In another setup of their market, the researchers programmed some of the bots trading stocks to have another psychological bias. Instead of making them more short-term oriented, they made them greedier, investing more money into stocks that are forecast to have higher returns. Note that this forecast doesn’t necessarily have to be based on past price momentum. It could be based on fundamental valuation, volatility or other factors. The only thing greedy investors have in common is that no matter the investment approach they use, they invest heavily in those stocks that are forecast to be more profitable and ignore the ones that are forecast to be less profitable. The result of a market with more and more greedy investors was a decline in crashes and stock market bubbles, not an increase as one may have expected.

Number of market crashes (drop > 20%) if greedy traders increase from 0% (P=0) to 100% (P=100)

a.image2.image-link.image2-718-1236 { padding-bottom: 58.090614886731395%; padding-bottom: min(58.090614886731395%, 718px); width: 100%; height: 0; } a.image2.image-link.image2-718-1236 img { max-width: 1236px; max-height: 718px; }Source: Lussange et al. (2019)

This kind of behaviour can be observed in markets with human investors as well. In an experiment, people were invited to participate in an artificial stock market and trade with other people. Unbeknownst to them, the participants were sorted into low greed and high greed groups and ten experiments were run in each group.

One fun side remark here is that it apparently is easy to find out who are the greedy people and who are not: Just ask them if they think they are greedy. If you calculate correlations between greedy behaviour in investments and everyday life with different questions, the questions “I always want more” and “Actually, I am kind of greedy” have the highest correlation with real-life behaviour.

In any case, the experimental markets with human investors showed that prices deviated more from the fundamental value in markets with less greedy investors than in markets with greedy investors. The maximum size of the price bubbles observed in these markets was also higher for markets full of less greedy investors than in markets with greedy investors.

Price bubbles and deviation from fundamentals with greedy and less greedy investors

a.image2.image-link.image2-490-928 { padding-bottom: 52.80172413793104%; padding-bottom: min(52.80172413793104%, 490px); width: 100%; height: 0; } a.image2.image-link.image2-490-928 img { max-width: 928px; max-height: 490px; }Source: Hoyer et al. (2021)

One key to understanding the higher efficiency in markets with greedier investors is to look at market turnover. There, we see that markets with higher turnover tend to have more efficient prices and smaller deviations from fundamentals.

Market turnover and deviation from fundamentals with greedy and less greedy investors

a.image2.image-link.image2-506-926 { padding-bottom: 54.64362850971922%; padding-bottom: min(54.64362850971922%, 506px); width: 100%; height: 0; } a.image2.image-link.image2-506-926 img { max-width: 926px; max-height: 506px; }Source: Hoyer et al. (2021)

What is happening here is that if investors are really greedy, they don’t stick with investments for too long; If they see a better opportunity elsewhere, they sell what they own and buy something else. Because we have a mix of fundamental investors and trend followers in the market, this means that if a stock becomes too detached from fundamentals, the trend followers will continue to buy that stock, but the fundamental investors will aggressively bet against it. That will slowly reduce the returns of that stocks and eventually reverse the previous trend. At this point, fundamental investors still bet aggressively against the stock because it is still overvalued, but momentum investors are switching sides and now bet against that stock, too. The result is that the stock quickly moves back towards fundamental value thanks to the greed of investors who want to make as much money as they can.

Thus, there are circumstances when greed can be a force for good in investing. But remember that this experiment assumes that people with many different opinions are around who follow different strategies. And it assumes that there are different assets available. If you go into a market where there is only one asset or one type of asset and there are no substitutes (e.g. CDOs in the run-up to the financial crisis 2008) then you can be as greedy as you want to, you can only invest in one thing and that means you are forced to push the price of overvalued assets even higher. Similarly, if there is no difference in opinion (e.g. if all investors in a market are momentum investors because there is no fundamental value) then there will be no investors betting against trend followers and momentum investors and prices can deviate massively from whatever the fundamental value is and bubbles and crashes become more likely.

Greed can be good, but it depends on the circumstances.

Categorías: Blogs y opiniones de economia en ingles

The importance of investing for retirement as early as possible

At the beginning of the 21st century most young people are told that social security won’t be there for them when they retire from the work force. Thus, in order to be able to completely retire from the workforce, a person has to invest as early as possible in order to take full advantage of the power of compounding.

Let’s follow the story of Erica and John. They both grew up on the same street...

To read the whole article, please click on the article title above.

To read the whole article, please click on the article title above.

Categorías: Blogs y opiniones de economia en ingles

Clips From Today’s Closing Bell

Fed may begin tapering as soon as October from CNBC.

...

The post Clips From Today’s Closing Bell appeared first on The Reformed Broker.

Categorías: Blogs y opiniones de economia en ingles

Hanging By A Thread

A big lesson from history is how chance encounters lead to both magic and mayhem in ways that would have been impossible to predict.

Let me show you three times history hung by a thread.

Giuseppe Zangara was tiny, barely five feet tall. He stood on a chair outside a Miami political rally in 1933 because that was the only way he could aim his gun across the crowd.

Zangara fired five shots. One of them hit Chicago mayor Anton Cermak, who was shaking hands with Zagara’s intended target. Cermak died. The target – Franklin Roosevelt – was sworn in as president two weeks later.

Within months of inauguration Roosevelt transformed the U.S. economy through the New Deal. John Nance Garner – who would have become president had Zangara hit his target – opposed most of the New Deal’s deficit spending. He almost certainly wouldn’t have enacted the same policies, some of which still shape today’s economy.

Captain William Turner invited his niece, actress Mercedes Desmore, to tour his massive ocean liner before it sailed from New York To Liverpool.

The ship’s crew, eager to leave on time, removed the gangway for departure while Desmore was still onboard. She was stuck on a ship about to begin a seven-day voyage. Her furious uncle made the crew re-dock the ship so she could get off.

The redocking delayed the ship’s departure. No one could have known that six days later the delay would mean that Turner’s ship – the Lusitania – would sail into the path of a German submarine at the very moment its periscope could finally see through the day’s diminishing fog.

The Lusitania was hit with a torpedo, killing 1,200 passengers and becoming the most important trigger to rally U.S. public support for entering World War I.

Had it sailed through the Celtic Sea half an hour earlier – had Desmore’s tour not caused a delay – the Lusitania would have been cloaked in heavy fog. The ship likely would have avoided attack. A country may have avoided a war that became the seed event for the rest of the 20th century.

Robert E. Lee had one last shot to escape Ulysses Grant’s troops and regroup to gain the upper hand in the Civil War. His plan was bold but totally plausible. All he needed was food for his hungry troops.

An order was put in to have rations delivered to a Virginia supply depot for Lee’s men.

But there was a communication error in Richmond, and the wagons delivered boxes of ammunition but not a morsel of food.

Lee said the mishap “was fatal, and could not be retrieved.” His troops were starving. The Civil War ended two days later.

History hangs by a thread.

You can play this game all day. Every big event could have turned out differently if a few little puffs of nothingness went the other direction. It’s so easy to prove how fragile big events are to trivia and accident that you start to wonder what the point is.

It’s even crazier when you realize that every modern event has its roots in big past events, some of which occurred decades ago.

Take a simple question like, “What caused the financial crisis?”

When asked that most people point to things like lending standards and the Federal Reserve.

But if you keep digging into the roots of what happened you go down a rabbit hole that never ends.

To understand the financial crisis you have to understand the mortgage market.

What shaped the modern mortgage market? Well, you have to understand the 30-year decline in interest rates that preceded it.

What caused falling interest rates? Well, you have to understand the inflation of the 1970s.

What caused that inflation? Well, you have to understand the monetary system of the 1970s and the hangover effects of the Vietnam War.

What caused the Vietnam War? Well, you have to understand the West’s fear of communism after World War II.

What caused World War II? Well, you have to understand World War I.

What caused World War I? Well, for the Americans’ participation, an actress toured her uncle’s boat and then …

That’s also a game you can play all day.

And an endless number of modern innovations were born out of those freak events. The modern grocery store was invented because food sellers were trying to survive the Great Depression. Penicillin owes its existence to World War II. So do radar, jets, nuclear energy, rockets, and helicopters. mRNA vaccines will owe their existence to Covid-19. All of those big events could have turned out completely differently if a few minor accidents had gone a different way.

So much of history hangs by a thread.

Finance professor Ellroy Dimson says, “risk means more things can happen than will happen.” An important point here is that if none of these big events occurred, something else just as wild and unpredictable could have taken their place. Even when some part of the outcome is the same, the context and little bits of trivia are different in a way that can totally change the final story. America may have joined World War I without the Lusitania’s sinking, but its participation could have been less, or later, or not as popular. That could have shifted how the interwar period in the 1920s and 1930s played out, which would have impacted how World War II occurred, which would have altered the course of the most promising inventions of the 20th century … on and on, endlessly.

I try to keep two things in mind in a world that’s this fragile to chance.

One is to base your predictions on how people behave vs. specific events. Predicting what the world will look like in, say, 2050, is just impossible. But predicting that people will still respond to greed, fear, opportunity, exploitation, risk, uncertainty, tribal affiliations and social persuasion in the same way is a bet I’d take.

Another – made so starkly in the last year and a half – is that no matter what the world looks like today, and what seems obvious today, everything can change tomorrow because of some tiny accident no one’s thinking about. Events, like money, compound. And the central feature of compounding is that it’s never intuitive how big something can grow from a small beginning.

Categorías: Blogs y opiniones de economia en ingles

101 Financial Ratios & Metrics To Improve Your Investing Skills

Updated on August 11th, 2021 by Bob Ciura This article covers 101 financial ratios and metrics investors need to know. This list is by no means all inclusive. It does however contain several interesting and informative metrics. You can use the links below to instantly jump to a specific section of the article. Table of […]

The post 101 Financial Ratios & Metrics To Improve Your Investing Skills appeared first on Sure Dividend.

Categorías: Blogs y opiniones de economia en ingles

Shock Doctrine 3.0: END GAME

The conservative movement has succeeded in dismantling government to the point at which proper governance no longer exists. This society is now fully at the mercy of the corporate Matrix whose main line of business is to monetize addiction...

Once again, the U.S. comes in dead last with respect to developed nation health outcomes as the COVID crisis revealed the fatal weakness of employer-sponsored healthcare.

It's least there when you most need it.

I know, this is all a communist plot to subvert greatness. The hubris that attends this bloated Idiocracy is by far the greatest threat to its existence:

"Government officials and health experts are leaning on the private sector to lead the U.S. out of a coronavirus surge caused by the highly infectious Delta variant"

Got that? We are now relying on corporations to navigate the U.S. through this ongoing pandemic. The same ones that are monetizing it to the greatest extent possible. This is analogous to the U.S. government handing over management of WWII to the military industrial complex. Is it any wonder why the healthcare sector keeps making new all time highs?

They are sucking this society dry.

At this juncture, the healthy populace that is fully vaccinated remains in deathly fear of the COVID virus. While the least healthy and unvaccinated population exhibits no fear whatsoever. This lowest IQ approach is producing the worst possible outcomes with respect to the economy and public health. And this ongoing disaster falls mainly on small business to the benefit of the large multinational oligopolies which have been gaining market share throughout this pandemic.

The ones that now own the government.

This is Shock Doctrine 3.0. The first rendition was 9/11 which hid the mass outsourcing of U.S. factories to China. The second edition of course was the Global Financial Crisis which further accelerated the Financialization of the economy. Libertarians should be up in arms at this latest subversion of liberty, but since it's coming from the private sector, it's A-OK. Yet again, they've been easily fooled by sleight of hand.

What does this have to do with the Casino? Good question. This ups the ante on the downside effects of this latest mega bubble. It's clear now that from an economic standpoint, the COVID crisis hid the impending end of cycle, which was beginning to exert downward pressure in late 2019. Now as the various stimuli recede, deflationary forces are once again exerting themselves on the global economy. Bear in mind, that in addition to the threat of monetary tapering, there is the fact that 7.5 million workers will lose unemployment within a few weeks.

"That’s more than five times the 1.3 million people who lost aid in December 2013 as the country walked away from the Great Recession"

The data indicate that the red states which already terminated Federal pandemic unemployment assistance are not seeing the re-employment they expected. Which portends disaster next month. On my recent road trip to Yellowstone, I saw help wanted signs everywhere. No Mexicans to be found.

So once again, economists, the Fed, salesmen, media pundits, and gamblers stand to be wrong when it hurts the most, as they use one time year over year price changes from a locked down economy to rationalize inflation hysteria.

This is the worst headfake "inflation" since they got it wrong last time:

"Buy a car now, before we run out"

"Buy a house now, before we run out"

In summary, in this bailout addicted society, criminality is expected.

Buyer be unaware.

{kind=link}

Once again, the U.S. comes in dead last with respect to developed nation health outcomes as the COVID crisis revealed the fatal weakness of employer-sponsored healthcare.

It's least there when you most need it.

{kind=link}

I know, this is all a communist plot to subvert greatness. The hubris that attends this bloated Idiocracy is by far the greatest threat to its existence:

"Government officials and health experts are leaning on the private sector to lead the U.S. out of a coronavirus surge caused by the highly infectious Delta variant"

Got that? We are now relying on corporations to navigate the U.S. through this ongoing pandemic. The same ones that are monetizing it to the greatest extent possible. This is analogous to the U.S. government handing over management of WWII to the military industrial complex. Is it any wonder why the healthcare sector keeps making new all time highs?

They are sucking this society dry.

At this juncture, the healthy populace that is fully vaccinated remains in deathly fear of the COVID virus. While the least healthy and unvaccinated population exhibits no fear whatsoever. This lowest IQ approach is producing the worst possible outcomes with respect to the economy and public health. And this ongoing disaster falls mainly on small business to the benefit of the large multinational oligopolies which have been gaining market share throughout this pandemic.

The ones that now own the government.

This is Shock Doctrine 3.0. The first rendition was 9/11 which hid the mass outsourcing of U.S. factories to China. The second edition of course was the Global Financial Crisis which further accelerated the Financialization of the economy. Libertarians should be up in arms at this latest subversion of liberty, but since it's coming from the private sector, it's A-OK. Yet again, they've been easily fooled by sleight of hand.

What does this have to do with the Casino? Good question. This ups the ante on the downside effects of this latest mega bubble. It's clear now that from an economic standpoint, the COVID crisis hid the impending end of cycle, which was beginning to exert downward pressure in late 2019. Now as the various stimuli recede, deflationary forces are once again exerting themselves on the global economy. Bear in mind, that in addition to the threat of monetary tapering, there is the fact that 7.5 million workers will lose unemployment within a few weeks.

"That’s more than five times the 1.3 million people who lost aid in December 2013 as the country walked away from the Great Recession"

The data indicate that the red states which already terminated Federal pandemic unemployment assistance are not seeing the re-employment they expected. Which portends disaster next month. On my recent road trip to Yellowstone, I saw help wanted signs everywhere. No Mexicans to be found.

So once again, economists, the Fed, salesmen, media pundits, and gamblers stand to be wrong when it hurts the most, as they use one time year over year price changes from a locked down economy to rationalize inflation hysteria.

This is the worst headfake "inflation" since they got it wrong last time:

{kind=link}

"Buy a car now, before we run out"

{kind=link}

"Buy a house now, before we run out"

{kind=link}

In summary, in this bailout addicted society, criminality is expected.

Buyer be unaware.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Monthly Dividend Stock In Focus: Inter Pipeline

Updated on August 11th, 2021 by Bob Ciura The energy industry is well-known for housing exceptional dividend stocks. However, when we think of dividend energy stocks, the heavyweights like Exxon Mobil (XOM) and Chevron (CVX) typically come to mind. Smaller energy companies can be a good source of dividend income as well. Inter Pipeline (IPPLF) […]

The post Monthly Dividend Stock In Focus: Inter Pipeline appeared first on Sure Dividend.

Categorías: Blogs y opiniones de economia en ingles

Episode #339: George Davis, Hotchkis & Wiley, “We’re In Unchartered Territory Right Now”

Episode #339: George Davis, Hotchkis & Wiley, “We’re In Unchartered Territory Right Now” Guest: George Davis serves as CEO and is responsible for setting the firm’s strategic direction. Mr. Davis also serves as a portfolio manager on the Large Cap Fundamental Value and Large Cap Diversified Value portfolios. […]

The post Episode #339: George Davis, Hotchkis & Wiley, “We’re In Unchartered Territory Right Now” appeared first on Meb Faber Research - Stock Market and Investing Blog.

Categorías: Blogs y opiniones de economia en ingles

Páginas

Custom Search