Se encuentra usted aquí

Blogs y opiniones de economia en ingles

How to find the next $100 billion stocks

subscribe on YouTube

listen to the whole podcast episode

Big thanks to JC, visit All Star ChartsAll Star Charts to learn more.

...

The post How to find the next $100 billion stocks appeared first on The Reformed Broker.

Categorías: Blogs y opiniones de economia en ingles

Bayer trading at a decade low – Is it an opportunity to buy or should we stay away?

Bayer dropped in price again after their recent Q2 earnings and additional provision for Roundup settlements. What to do with it right now?

The post Bayer trading at a decade low – Is it an opportunity to buy or should we stay away? appeared first on European Dividend Growth Investor.

Categorías: Blogs y opiniones de economia en ingles

Letters to the editor

A selection of correspondence

Categorías: Blogs y opiniones de economia en ingles

Building The Perfect Ponzi Scheme

Today's bullish pundits can take pride in the fact that they have successfully participated in creating human history's biggest Ponzi scheme. All of the fraud and criminality from the past two cycles is rolled into one massive mega bubble. In doing so, they fully exploited the younger generations who have not the slightest clue how this level of fraud ends. They told them they were democratizing markets when all they were doing was democratizing bagholding. Today's ubiquitous sociopathic salesmen succeeded in leveraging a pandemic to create buying panics in everything that can be bought and sold from toilet paper to ammunition to McMansions, crypto Ponzi schemes, Ark ETFs, commodities, SPAC frauds, IPO garbage and of course S&P 500 stonks...

{kind=link}

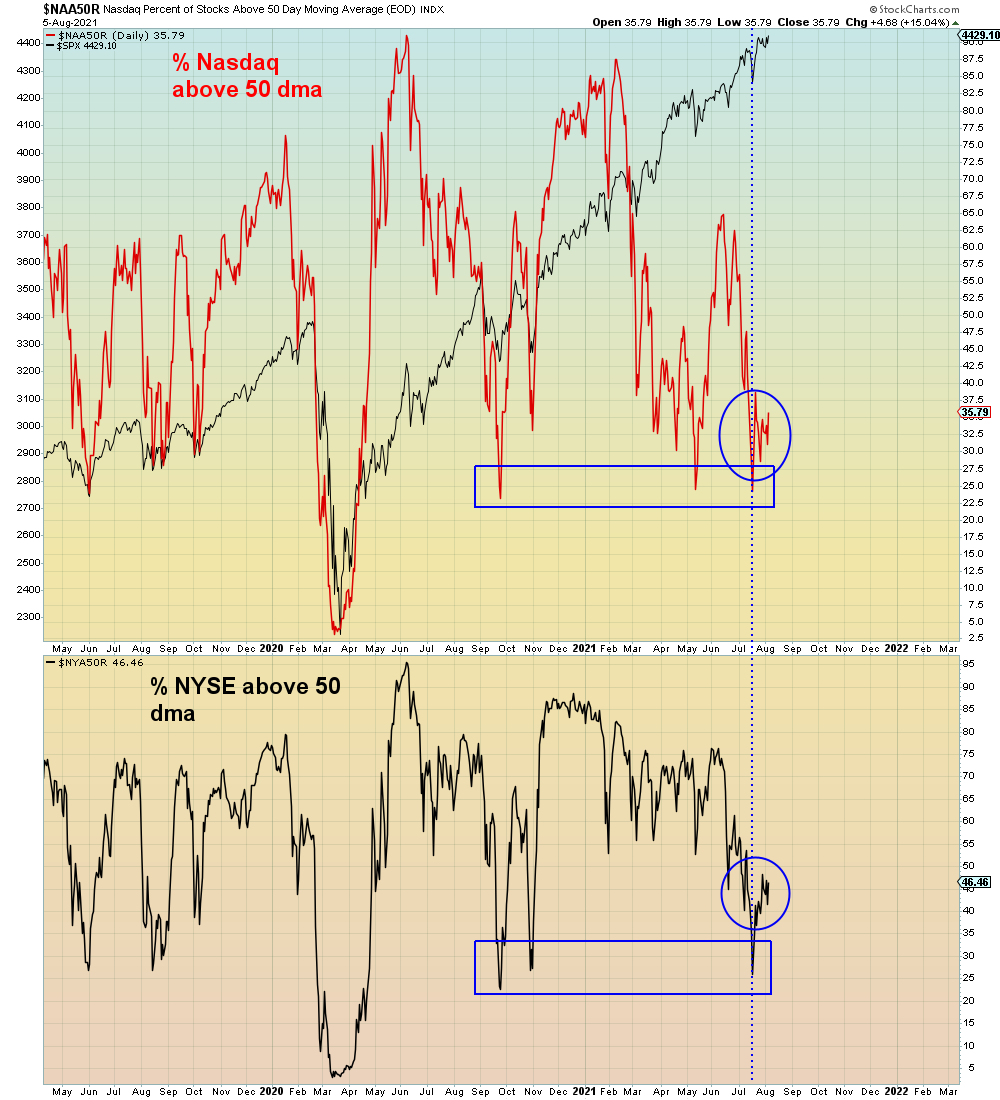

There are few if any pundits questioning this hyper bubble anymore. Skepticism peaked months ago. Why? Because from their point of view this Ponzi scheme is now flawless. It has achieved perfect extreme over-valuation and ALL IN risk positioning. In their minds, this Ponzi bubble has done nothing "wrong". On Twitter, I made the analogy of the Olympics - we celebrate the winners while ignoring the majority losers going home empty handed. It's called survivor bias. One troll asked recently if I ever make money. My response was never in Ponzi schemes. So far I have accurately predicted doom for crypto currencies, gold trades, Ark ETFs, Chinese stonks, and SPAC junk. In addition, I correctly predicted the rollover in bond yields which is something no mainstream pundits saw coming. Of course, the one prediction that remains elusive is that of the collapse of the major averages. Why? Because even as one after another sector dominoes collapse, the averages are seeing constant sector rotation. However, now we are witnessing breadth collapse in BOTH the NYSE and Nasdaq at the same time. And in addition, breadth has failed to rally during this latest "new high" in the S&P. The internals of the market are now the perfect analog for this speculative casino - a handful of winners and a majority of losers:

{kind=link}

One thing we've learned in spades is that a society bereft of dignity and virtue will never appreciate dignity and virtue. Instead they flock to all of the various charlatans who will gladly exploit useful idiots to their own means. The definition of "inflation" is that prices can only go higher. Even at this late stage, the specious inflation narrative remains dominant. We have achieved inflation sans middle class. Even the Fed believes it now.

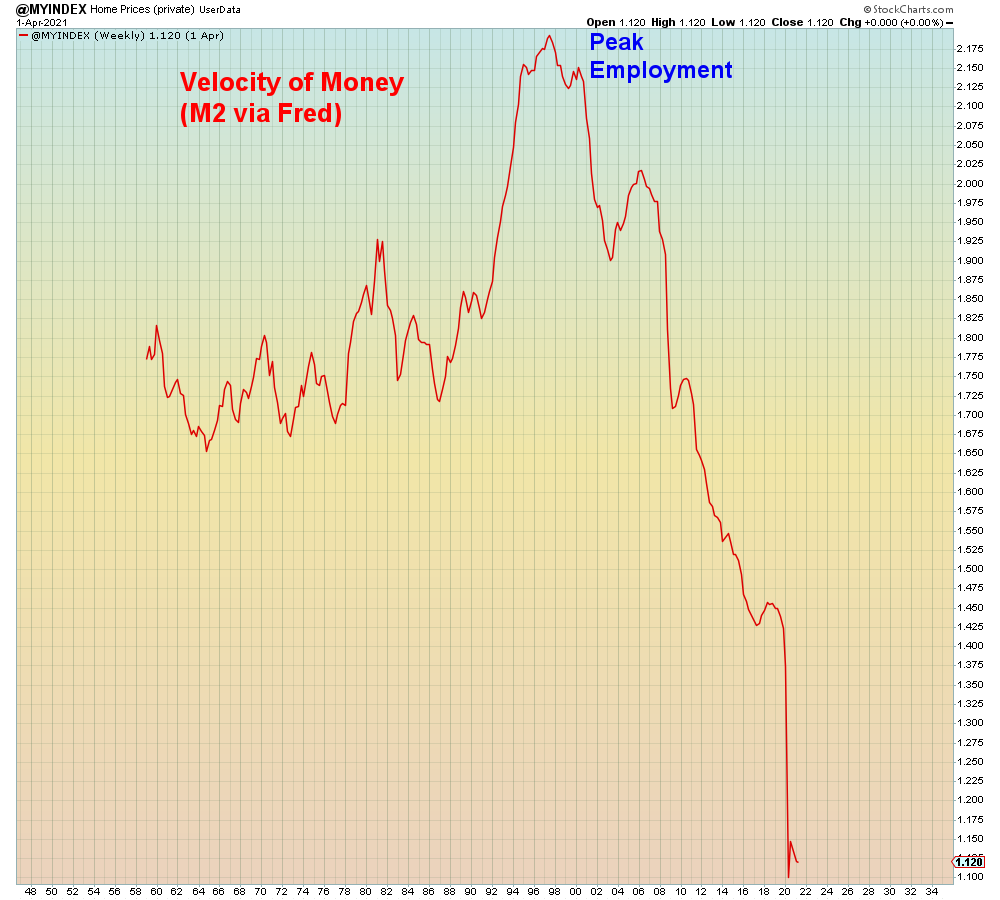

Here we see the velocity of money peaked twenty years ago when GDP growth and employment peaked in the U.S. The velocity of money measures the speed at which each dollar circulates throughout the economy. In an inflationary economy, the velocity of money sky rockets as consumers dump cash to hoard merchandise.

{kind=link}

In summary, the magnitude of this fraud is directly proportional to the moral collapse of a decadent society in late stage self-destruct mode. ALL of the criminality of the past two decades has now been exceeded in this past year. A super Tech bubble with record junk IPO issuance. An even bigger housing bubble. Regulators asleep at the wheel, and of course wanking fucking bankers.

Categorías: Blogs y opiniones de economia en ingles

Investing Insights: Inflation Protection and August Financial Tasks

Categorías: Blogs y opiniones de economia en ingles

Visualizing the Gravitational Pull of the Planets

-

Visualizing the Gravitational Pull of the Planets

Gravity is one of the basic forces in the universe. Every object out there exerts a gravitational influence on every other object, but to what degree?

The gravity of the sun keeps all the planets in orbit in our solar system. However, each planet, moon and asteroid have their own gravitational pull defined by their density, size, mass, and proximity to other celestial bodies.

Dr. James O’Donoghue, a Planetary Astronomer at JAXA (Japan Aerospace Exploration Agency) created an animation that simplifies this concept by animating the time it takes a ball to drop from 1,000 meters to the surface of each planet and the Earth’s moon, assuming no air resistance, to better visualize the gravitational pull of the planets.

Sink like a Stone or Float like a FeatherNow, if you were hypothetically landing your spacecraft on a strange planet, you would want to know your rate of descent. Would you float like a feather or sink like a stone?

It is a planet’s size, mass, and density that determines how strong its gravitational pull is, or, how quick or slow you will approach the surface.

Mass (1024kg)Diameter (km)Density (kg/m3)Gravity (m/s2)Escape Velocity (km/s) Mercury0.334,8795,4273.74.3 Venus4.8712,1045,2438.910.4 Earth5.9712,7565,5149.811.2 Moon0.0733,4753,3401.62.4 Mars0.6426,7923,9333.75.0 Jupiter1,898142,9841,32623.159.5 Saturn568120,5366879.035.5 Uranus86.851,1181,2718.721.3 Neptune10249,5281,63811.023.5 Pluto0.01462,3702,0950.71.3According to Dr. O’Donoghue, large planets have gravity comparable to smaller ones at the surface—for example, Uranus attracts the ball down slower than on Earth. This is because the relatively low average density of Uranus puts the actual surface of the planet far away from the majority of the planet’s mass in the core.

Similarly, Mars is almost double the mass of Mercury, but you can see the surface gravity is actually the same which demonstrates that Mercury is much denser than Mars.

Exploring the Outer Reaches: Gravity AssistanceKnowing the pull of each of the planets can help propel space flight to the furthest extents of the solar system. The “gravity assist” flyby technique can add or subtract momentum to increase or decrease the energy of a spacecraft’s orbit.

Generally it has been used in solar orbit, to increase a spacecraft’s velocity and propel it outward in the solar system, much farther away from the sun than its launch vehicle would have been capable of doing, as in the journey of NASA’s Voyager 2.

Launched in 1977, Voyager 2 flew by Jupiter for reconnaissance, and for a trajectory boost to Saturn. It then relied on a gravity assist from Saturn and then another from Uranus, propelling it to Neptune and beyond.

Despite the assistance, Voyager 2’s journey still took over 20 years to reach the edge of the solar system. The potential for using the power of gravity is so much more…

Tractor Beams, Shields, and Warp Drives…Oh My!Imagine disabling an enemy starship with a gravity beam and deflecting an incoming photon torpedo with gravity shields. It would be incredible and a sci-fi dream come true.

However, technology is still 42 years from the fictional date in Star Trek when mankind built the first warp engine, harnessing the power of gravity and unlocking the universe for discovery. There is still time!

Currently, the ALPHA Experiment at CERN is investigating whether it is possible to create some form of anti-gravitational field. This research could create a gravitational conductor shield to counteract the forces of gravity and allow the creation of a warp drive.

By better understanding the forces that keep us grounded on our planets, the sooner we will be able to escape these forces and feel the gravitational pull of the planets for ourselves.

…to boldly go where no one has gone before!

The post Visualizing the Gravitational Pull of the Planets appeared first on Visual Capitalist.

Categorías: Blogs y opiniones de economia en ingles

30% of social media use is due to lack of self-control

One of the eternal questions to me is how much of our life is spent with useless and unproductive things. This is not to say that we should always be productive. There is a time for fun and my Friday posts are one such exercise in writing about economics and finance without it necessarily being useful. But what bugs me is if companies exploit their customers through unfair means. For example, I have written in the past that there are some experiments that show that Facebook and other social media sites are addictive like tobacco.

This obviously begs the question of how addictive they are and how much time is lost to us users succumbing to our social media addiction. In my previous post, the researchers tried to get to the bottom of it by asking people how much they would be willing to pay to get access to social media for a week or a month. Now, a group of researchers from Stanford University and Microsoft have done another set of experiments. They asked people if they think they are using social media and other apps too often and too much. And indeed, most people are aware that they use these apps too much. Asked about how much time they would spend doing other things if these apps weren’t readily available on their phones and computers, people expected that they would spend about 20% less time on Facebook, about 10% less time gaming, and about 5% less time with YouTube, Snapchat, Twitter, etc.

Then these people were restricted in their social media use for several weeks either by having a limiter installed on their phones that limits the amount of time they can spend or by being offered a bonus if they reduced their social media use below a certain number of hours per week. Note that even in the limiter case, users could decide themselves, what limit they wanted to set themselves and they could change that time limit daily, so it is not an enforced limit.

What happened afterward shed some light on how addictive social media apps are. First, people reduced their social media use substantially more than they expected when they were offered a limiter or a bonus. But once that restriction was removed again, they again underestimated how much they would reduce their social media use if they could. In other words, people are aware that they are using social media too much and they substantially reduce their usage if they are incentivised to do so. But they systematically underestimate the amount of excess use they have on social media. If that sounds like an alcoholic who is aware that he drinks too much but only by a little, or a smoker who is aware that smoking is bad he only smokes a few cigarettes a day, then this is no coincidence. It is classic addictive behaviour that is observed with social media.

And the experiments provide a hint at how much social media is due to addictive overuse. In the case of Facebook, about 20 minutes per day, or roughly 30% of daily use. Imagine what you could achieve in your life if you could reduce your time on social media by 30% each day. You wouldn’t miss out on any of the fun, and become more productive at the same time.

Reduction in social media use under self-imposed restrictions

a.image2.image-link.image2-691-1456 { padding-bottom: 47.458791208791204%; padding-bottom: min(47.458791208791204%, 691px); width: 100%; height: 0; } a.image2.image-link.image2-691-1456 img { max-width: 1456px; max-height: 691px; }Source: Allcott et al. (2021).

Categorías: Blogs y opiniones de economia en ingles

What We're Reading

I refer to “increasing status” in the positive sense: accomplishing something impressive or contributing to others in a way that increases their estimation of you. That’s the only way that works, anyway. Paraphrasing Taleb: anything done with explicit intent to improve one’s status likely *won’t *improve one’s status. After all, the most respected people achieved their status as a byproduct of doing something great, like pursuing ambition, honor, and integrity!

Your truth and *the *truth are not always the same thing. *The *truth is a fact. Your truth is just an opinion. Nobody values somebody who is honest about their opinions if their opinions always suck. Knowing when to offer your truth and keep your mouth shut is a rare quality. The line between thoughtful dialogue and disrespectful disagreement is razor-thin.

Have a good weekend.

Categorías: Blogs y opiniones de economia en ingles

Other People’s Mistakes

George Carlin once joked how easy it is to spot stupid people. “Carry a little pad and pencil around with you. You’ll wind up with 30 or 40 names by the end of the day. It doesn’t take long to spot one of them, does it? Takes about eight seconds.”

Like most comedy it’s funny because it’s true.

But Daniel Kahneman mentions a more important truth in his book, Thinking, Fast and Slow: “It is easier to recognize other people’s mistakes than our own.”

I would add my own theory: It’s easier to blame other people’s mistakes on stupidity and greed than our own.

That’s because when you make a mistake, I judge it solely based on what I see. It’s quick and easy.

But when I make a mistake there’s a long and persuasive monologue in my head that justifies bad decisions and adds important context other people don’t see.

Everyone’s like that. It’s normal.

But it’s a problem, because it makes it easy to underestimate your own flaws and become too cynical about others’.

I try to stop myself whenever my explanation for other people’s behavior – financial or otherwise – is “well, they’re not very smart.” Or greedy. Or immoral. Yeah, sometimes it’s true. But probably less than we assume. More often there’s something else going on that you’re not seeing that makes the behavior more understandable, even if it’s still wrong.

A few things make it that way.

1. When judging others’ poor behavior it’s easy to underestimate your own susceptibility to the power of incentives.

The worst behavior resides in industries with the most extreme incentives. Finance, where scams are everywhere. High-end art, where counterfeits proliferate.

But it’s important to ask: Are immoral people attracted to industries where there are big rewards for bad behavior? Or do big rewards for bad behavior cause good people to slide into immorality, justifying their decisions along the way?

I think so often it’s the latter.

It helps explain things like the 2008 financial crisis. Was it caused by greedy bankers? Maybe here and there. But the huge majority of it was good, honest people who wanted to do the right thing but whose definition of “the right thing” is instantly warped when they’re paid $8 million a year to sell subprime bonds.

Incentives are almost like a drug in their ability to cloud your judgment in a way you would have found unthinkable beforehand. They can get good people to justify all kinds of things.

That doesn’t excuse bad behavior. But it’s hard to know what you’d be willing to do until you’re exposed to an extreme incentive, and that blindness makes it easy to criticize other people’s mistakes when you yourself may have been just as tempted if you were in their shoes.

2. It’s hard to tell the difference between boldness and recklessness, greed and ambition, contrarian and wrong.

The same traits needed to be hugely successful are often the same traits needed to spark a catastrophe. Not always, but a lot of the time.

A low-probability bet that works makes you look like a genius.

A low-probability bet that fails makes you look like a … failure, maybe even an idiot, in the eyes of others.

But the difference between the two may have been minuscule. It could have been the same person doing the exact same thing ending up on the fortune or unfortunate side of luck.

Everything worth pursuing has a less than 100% chance of working. And a lot of terrible ideas have at least some chance of working. So you can make good decisions that don’t work, bad ones that do, and everything in between.

The hard thing is that when the probability isn’t easy to determine, the path of least resistance is to put your own failures in the “good bet that unfortunately didn’t work” category and other people’s failures in the “that was clearly a bad idea” one.

When judging others you want a simple story – did it work or did it not? And when judging yourself you want a comforting story – “my actions were worthwhile and I’m a good person.”

But those are just the easy explanations, not necessarily the right ones. So you may not be as great, and other people may not be as bad, as it looks.

3. Not all relevant information is visible.

My brother in law, a social worker, recently told me, “All behavior makes sense with enough information.”

It’s such a good point.

You see someone doing something crazy and think, “Why in the world would you do that?” Then you sit down with them, hear about their life, and after a while you realize, “Ah, I kind of get it now.”

Everyone is a product of their own life experiences, few of which are visible or known to other people.

What makes sense to me might not make sense to you because you don’t know what kind of experiences have shaped me and vice versa.

The question, “Why don’t you agree with me?” can have infinite answers.

Sometimes one side is selfish, or stupid, or blind, or uninformed.

But usually a better question is, “What have you experienced that I haven’t that would make you believe what you do? And would I think about the world like you do if I experienced what you have?”

It’s the question that contains the most answers of why people don’t agree with each other.

But it’s such a hard question to ask.

It’s uncomfortable to think that what you haven’t experienced might change what you believe because it’s admitting your own ignorance. It’s much easier to assume those who disagree with you aren’t thinking as hard as you are – especially when judging others’ mistakes.

Categorías: Blogs y opiniones de economia en ingles

Histomap: Visualizing the 4,000 Year History of Global Power

Imagine creating a timeline of your country’s whole history stretching back to its inception.

It would be no small task, and simply weighing the relative importance of so many great people, technological achievements, and pivotal events would be a tiny miracle in itself.

While that seems like a challenge, imagine going a few steps further. Instead of a timeline for just one country, what about creating a graphical timeline showing the history of the entire world over a 4,000 year time period, all while having no access to computers or the internet?

An All-Encompassing Timeline?Today’s infographic, created all the way back in 1931 by a man named John B. Sparks, maps the ebb and flow of global power going all the way back to 2,000 B.C. on one coherent timeline.

View a high resolution version of this graphic

Histomap, published by Rand McNally in 1931, is an ambitious attempt at fitting a mountain of historical information onto a five-foot-long poster. The poster cost $1 at the time, which would equal approximately $18 when accounting for inflation.

Although the distribution of power is not quantitatively defined on the x-axis, it does provide a rare example of looking at historic civilizations in relative terms. While the Roman Empire takes up a lot of real estate during its Golden Age, for example, we still get a decent look at what was happening in other parts of the world during that period.

The visualization is also effective at showing the ascent and decline of various competing states, nations, and empires. Did Sparks see world history as a zero-sum exercise; a collection of nations battling one another for control over scarce territory and resources?

Timeline CaveatsCrowning a world leader at certain points in history is relatively easy, but divvying up influence or power to everyone across 4,000 years requires some creativity, and likely some guesswork, as well. Some would argue that the lack of hard data makes it impossible to draw these types of conclusions (though there have been other more quantitative approaches.)

Another obvious criticism is that the measures of influence are skewed in favor of Western powers. China’s “seam”, for example, is suspiciously thin throughout the length of the timeline. Certainly, the creator’s biases and blind spots become more apparent in the information-abundant 21st century.

Lastly, Histomap refers to various cultural and racial groups using terms that may seem rather dated to today’s viewers.

The Legacy of HistomapJohn Spark’s creation is an admirable attempt at making history more approachable and entertaining. Today, we have seemingly limitless access to information, but in the 1930s an all encompassing timeline of history would have been incredibly useful and groundbreaking. Indeed, the map’s publisher characterized the piece as a useful tool for examining the correlation between different empires during points in history.

Critiques aside, work like this paved the way for the production of modern data visualizations and charts that help people better understand the world around them today.

Without a map who would attempt to study geography? –John B. Sparks

This post was first published in 2017. We have since updated it, adding in new content for 2021.

The post Histomap: Visualizing the 4,000 Year History of Global Power appeared first on Visual Capitalist.

Categorías: Blogs y opiniones de economia en ingles

Maker of Meme Stocks

In hindsight, it should have been obvious that Robinhood, maker of meme stocks, would have turned into a meme stock.

On the first day of trading, Robinhood fell 8.4%, the worst debut of 51 companies that raised as much cash as they did. Investor enthusiasm just wasn’t there on its opening day. According to data from Vanda Track

On the first day of listing, HOOD was only the 28th most traded stock on retail platform

...

The post Maker of Meme Stocks appeared first on The Irrelevant Investor.

Categorías: Blogs y opiniones de economia en ingles

How to survive a black swan event: Cash is the only thing

The Covid shock has been extraordinary in so many ways. It clearly has been the most severe shock to the revenues of companies in almost all sectors and can truly be called a black swan event. Especially in the leisure and retail sectors, companies had to cope with revenue declines of 30% or more and struggled to survive. Thank goodness, government and central banks acted swiftly and decisively to help many of these companies survive.

But government support is running out in many countries in the next few months and we may not have seen all the fallout from the pandemic on the corporate front, yet. Nevertheless, both corporate executives and investors should use the coming months to assess how to deal with the next big shock to the system. Because this time, the government was there to help since it was a global shock that affected all of society, but next time, it could be a shock that affects only a specific industry or an individual company. And these shocks become more frequent across all industries. The chart below shows the share of companies in different sectors with revenue drops of 30% to 90% year-on-year (red) and 50% to 90% year-on-year (green).

Share of companies with extreme revenue drops

a.image2.image-link.image2-827-1377 { padding-bottom: 60.05809731299927%; padding-bottom: min(60.05809731299927%, 827px); width: 100%; height: 0; } a.image2.image-link.image2-827-1377 img { max-width: 1377px; max-height: 827px; }Source: Christie et al. (2021).

The chart is taken from a study of all companies in the Compustat database globally that investigated how many companies are subject to such extreme revenue shocks, which ones survive, and what drives the chance of survival. So here is the good news. The vast majority of companies (77%) that experience a revenue decline of more than 30% year-on-year survive. Only 23% of listed companies exit the market by being acquired, filing for bankruptcy, or other means. Of the 77% that survive, 44% show positive revenue growth the following year and 33% continue to experience declining revenues. But amongst those companies where revenues rebound the following year, the rebound tends to be weak. Only 13% experienced a strong rebound of 75% or more of lost revenue.

Extreme revenue shocks are typically not a short-term phenomenon but the fallout stays with a company for a long time, even if it survives the direct hit.

The fate of companies after a revenue shock

a.image2.image-link.image2-877-1379 { padding-bottom: 63.59680928208847%; padding-bottom: min(63.59680928208847%, 877px); width: 100%; height: 0; } a.image2.image-link.image2-877-1379 img { max-width: 1379px; max-height: 877px; }Source: Christie et al. (2021)

From a corporate perspective, there are basically three ways to cope with such extreme shocks and survive both the immediate impact as well as the following years. A company can have enough cash and liquidity reserves, it can have a high equity capital ratio and increase borrowing, or it can change its operations and become more flexible and leaner.

And when it comes to these three levers, the historical evidence seems pretty clear cut. The only thing that helps a company survive these extreme revenue shocks is access to cash. Companies that either had lots of liquidity at hand or could tap into existing credit lines to increase their cash at hand were more likely to survive and recovered more quickly.

Companies that had low financial leverage and a high equity capital ratio may want to borrow money to raise cash but once the revenue hit has come, banks and bond markets prove remarkably reluctant to extend any new credit to these companies. It’s the classic tale of banks willing to give a man an umbrella when the sun shines but asking for it to be returned when it starts to rain.

That an abundance of equity capital does not increase the chance of survival and that cash at hand does should also be a warning to investors in private equity. LBOs and other private equity strategies rely on an increase in leverage to improve profitability and accelerate a return of cash to investors. But that makes these companies extremely vulnerable to adverse market shocks – more so than listed companies. In essence, many private equity firms optimise their holdings for a sunny day and reduce the resilience of their portfolio companies to a thunderstorm.

Personally, I think this is what we will see in the aftermath of the pandemic as well. If I look at the publicly listed leisure companies in the UK, I find that so many of them are flush with cash. Many of them could survive a full year or more without any revenues. Meanwhile, so many restaurant chains and coffee shops owned by private equity firms had to enter into voluntary arrangements (the UK version of chapter 11 bankruptcy) because they simply didn’t have the liquidity to continue to operate and couldn’t get any new lines of credit.

But what about the third lever available to companies: Making the company leaner and increasing its operating flexibility. This is what so many private equity firms pride themselves on and what so many executives of listed companies try to do as flanking measures besides raising cash.

Well, it turns out that these efforts have hardly any impact on the chance of survival at all. In many cases, increasing operational flexibility takes a long time to achieve, often too long to be a meaningful help for a company struggling to survive. And making the company leaner aka cutting costs aka firing people has its own problems. Typically, it helps a company survive in the short run but reduces its ability to bounce back from the shock in the medium term. By firing lots of people, the company loses institutional knowledge and cuts into the very growth initiatives that could ensure a rebound after the crisis (often, “nice to have” growth projects are the first to face the chopping board in a crisis).

It’s not what managers learn in business school, but cutting costs is in the best case, useless and in the worst case puts a company on a path of continuous decline. Just look at companies like IAG, American Airlines, GM, US Steel, GE, Deutsche Bank, etc. Compared to their international peers and local challengers, they have cut their costs right into a bankruptcy or into market losers.

Categorías: Blogs y opiniones de economia en ingles

3 Lessor Known Dividend Kings

Let's talk about three lessor known Dividend Kings. These are relatively unknown companies with more than 50 years of dividend growth.

The post 3 Lessor Known Dividend Kings appeared first on European Dividend Growth Investor.

Categorías: Blogs y opiniones de economia en ingles

Companies Going Public in 2021: Visualizing IPO Valuations

Can I share this graphic?

Yes. Visualizations are free to share and post in their original form across the web—even for publishers. Please link back to this page and attribute Visual Capitalist. When do I need a license?

Licenses are required for some commercial uses, translations, or layout modifications. You can even whitelabel our visualizations. Explore your options. Interested in this piece?

Click here to license this visualization.

Yes. Visualizations are free to share and post in their original form across the web—even for publishers. Please link back to this page and attribute Visual Capitalist. When do I need a license?

Licenses are required for some commercial uses, translations, or layout modifications. You can even whitelabel our visualizations. Explore your options. Interested in this piece?

Click here to license this visualization.

▼ Use This Visualizationa.bg-showmore-plg-link:hover,a.bg-showmore-plg-link:active,a.bg-showmore-plg-link:focus{color:#0071bb;}

Companies Going Public in 2021: Visualizing ValuationsThe beginning of the year has been a productive one for global markets, and companies going public in 2021 have benefited.

From much-hyped tech initial public offerings (IPOs) to food and healthcare services, many companies with already large followings have gone public this year. Some were supposed to go public in 2020 but got delayed due to the pandemic, and others saw the opportunity to take advantage of a strong current market.

This graphic measures 47 companies that have gone public just past the first half of 2021 (from January to July)— including IPOs, SPACs, and Direct Listings—as well as their subsequent valuations after listing.

Who’s Gone Public in 2021 So Far?Historically, companies that wanted to go public employed one main method above others: the initial public offering (IPO).

But companies going public today readily choose from one of three different options, depending on market situations, associated costs, and shareholder preference:

- Initial Public Offering (IPO): A private company creates new shares which are underwritten by a financial organization and sold to the public.

- Special Purpose Acquisition Company (SPAC): A separate company with no operations is created strictly to raise capital to acquire the company going public. SPACs are the fastest method of going public, and have become popular in recent years.

- Direct Listing: A private company enters a market with only existing, outstanding shares being traded and no new shares created. The cost is lower than that of an IPO, since no fees need to be paid for underwriting.

So far, the majority of companies going public in 2021 have chosen the IPO route, but some of the biggest valuations have resulted from direct listings.

Listing DateCompanyValuation ($B)Listing Type 08-Jan-21Clover Health$7.0SPAC 13-Jan-21Affirm$11.9IPO 13-Jan-21Billtrust$1.3SPAC 14-Jan-21Poshmark$3.0IPO 15-Jan-21Playtika$11.0IPO 21-Jan-21Hims and Hers Health$1.6SPAC 28-Jan-21Qualtrics$15.0IPO 09-Feb-21Metromile-SPAC 11-Feb-21Bumble$8.2IPO 26-Feb-21ChargePoint Holdings$0.45SPAC 03-Mar-21Oscar Health$7.9IPO 10-Mar-21Roblox$30.0Direct Listing 11-Mar-21Coupang$60.0IPO 23-Mar-21DigitalOcean$5.0IPO 25-Mar-21VIZIO$3.9IPO 26-Mar-21ThredUp$1.3IPO 31-Mar-21Coursera$4.3IPO 01-Apr-21Compass$8.0IPO 14-Apr-21Coinbase$86.0Direct Listing 15-Apr-21AppLovin$28.6IPO 21-Apr-21UiPath$35.0IPO 21-Apr-21DoubleVerify$4.2IPO 05-May-21The Honest Company$1.4IPO 07-May-21Lightning eMotors$0.82SPAC 07-May-21Blade Air Mobility$0.83SPAC 19-May-21Squarespace$7.4Direct Listing 19-May-21Procore$9.6IPO 19-May-21Oatly$10.0IPO 26-May-21ZipRecruiter$2.4IPO 26-May-21FIGS$4.4IPO 01-Jun-21SoFi$8.7SPAC 02-Jun-21BarkBox$1.6SPAC 08-Jun-21Marqueta$15.0IPO 10-Jun-21Monday.com$7.5IPO 16-Jun-21WalkMe$2.5IPO 22-Jun-21Sprinklr$3.7IPO 24-Jun-21Confluent$9.1IPO 29-Jun-21Clear$4.5IPO 30-Jun-21SentinelOne$10.0IPO 30-Jun-21LegalZoom$7.0IPO 30-Jun-21Didi Chuxing$73.0IPO 16-Jul-21Blend$4IPO 21-Jul-21Kaltura$1.24IPO 21-Jul-21DISCO$2.5IPO 21-Jul-21Couchbase$1.4IPO 23-Jul-21Vtex$3.5IPO 23-Jul-21Outbrain$1.1IPOThough there are many well-known names in the list, one of the biggest through lines continues to be the importance of tech.

A majority of 2021’s newly public companies have been in tech, including multiple mobile apps, websites, and online services. The two biggest IPOs so far were South Korea’s Coupang, an online marketplace valued at $60 billion after going public, and China’s ride-hailing app Didi Chuxing, the year’s largest post-IPO valuation at $73 billion.

And there were many apps and services going public through other means as well. Gaming company Roblox went public through a direct listing, earning a valuation of $30 billion, and cryptocurrency platform Coinbase has earned the year’s largest valuation so far, with an $86 billion valuation following its direct listing.

Big Companies Going Public in Late 2021As with every year, some of the biggest companies going public are lined up for the later half.

Tech will continue to be the talk of the markets. Payment processing firm Stripe is setting up to be the year’s biggest IPO with an estimated valuation of $95 billion, and now-notorious trading platform Robinhood is looking to go public with an estimated valuation of $12 billion.

But other big players are lined up to capture hot market sentiments as well.

Electric truck startup Rivian Automotive (backed by Amazon) is estimated to earn a public valuation around $70 billion, which would make it one of the world’s largest automakers by market cap. Likewise, online grocery delivery platform InstaCart, which saw a big upswing in traction due to the pandemic, is looking at an estimated valuation of at least $39 billion.

Of course, there’s always a chance that potential public listings and offerings fall through. Whether they get delayed due to weak market conditions or cancelled at the last minute, anything can happen when it comes to public markets.

This post will be periodically updated throughout the year.

The post Companies Going Public in 2021: Visualizing IPO Valuations appeared first on Visual Capitalist.

Categorías: Blogs y opiniones de economia en ingles

Episode #337: Professor Richard Thaler, University of Chicago, “When Somebody Would Fire Us, It Was Almost Always At Exactly The Wrong Time”

Episode #337: Professor Richard Thaler, University of Chicago, “When Somebody Would Fire Us, It Was Almost Always At Exactly The Wrong Time” Guest: Richard Thaler is the Charles R. Walgreen Distinguished Service Professor of Behavioral Science and Economics at the University of Chicago Booth School. Thaler is […]

The post Episode #337: Professor Richard Thaler, University of Chicago, “When Somebody Would Fire Us, It Was Almost Always At Exactly The Wrong Time” appeared first on Meb Faber Research - Stock Market and Investing Blog.

Categorías: Blogs y opiniones de economia en ingles

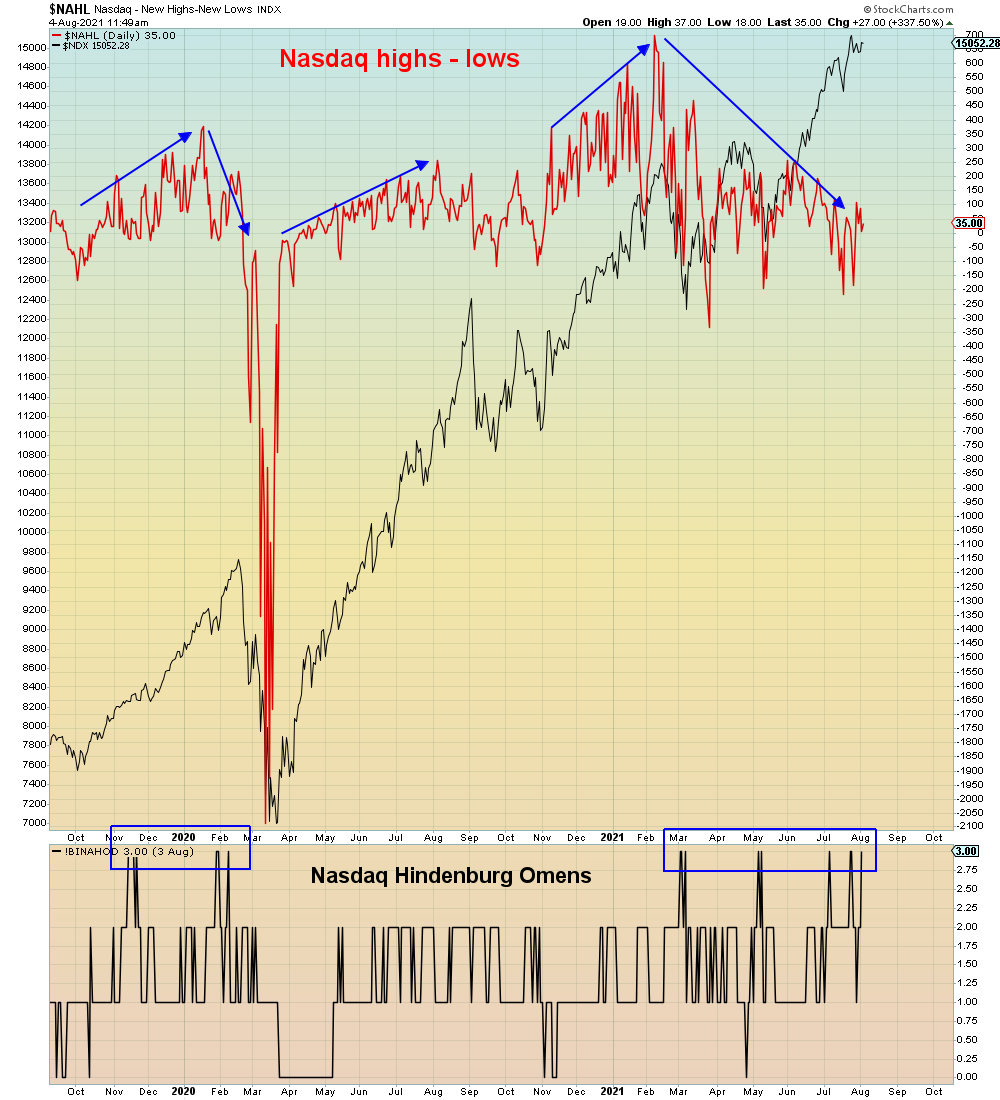

A Manic Reach For Explosion

We are now learning that the sole purpose of Monetary policy is to stimulate greed in an ultra greedy society. Central banks are keeping the spigots wide open to support the economy which is driving greed-addled gamblers to buy record inequality...

Another Nasdaq Hindenburg Omen yesterday - the third in less than two weeks, indicative of a bifurcated market disintegrating in real-time:

{kind=link}

This greed-addled society has long since forgotten how this movie ended the last two times. The COVID ultra bubble makes the Dotcom bubble and Housing bubbles seem minor by comparison. COVID exposed Globalization's economic frailties which are now sending markets and the economy in opposite directions. Central banks are keeping the spigots wide open ostensibly to help the economy, but the only effect is driving economic inequality to ludicrous levels. Yesterday we learned that household debt is exploding at the fastest pace since the 2007 top. Too many people forget that debt follows asset prices higher, BUT not lower. When assets crash they turn into liabilities. Debt is deflationary. Underwater debt is lethal.

Trolls and other low life criminals now abound, exhorting everyone to engage in maximum Ponzi. The greed-fueled inflation thesis jumped the shark from risk asset markets to the economy and back again. No fool should be left behind. The concept of financial and economic responsibility is an abandoned relic of a bygone era. Deemed to be of no value in the golden age of printed money.

Unfortunately, nothing could be further from the truth. As Japan and China have already learned the hard way, all of this central bank driven speculation brutally turns back into a deflated pumpkin overnight.

As the economic data continues to weaken, gamblers are attempting a last ditch rotation back to Tech stocks which are approaching another melt-up high. This time amid chasmic breadth divergences.

Here we see breadth attending this latest all time high:

{kind=link}

Yesterday another Hindenburg Omen on the Nasdaq (lower pane):

{kind=link}

Semis are leading this latest Tech melt-up. The Rydex ratio (lower pane) keeps making new highs indicating a manic reach for risk:

{kind=link}

This is all very reminiscent of August 2015 when Chinese authorities used monetary policy to inflate the stock market in the face of an imploding economy. Shockingly, it didn't work. It was the end of imagined realities.

Guess whose turn it is this time.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

The Long View: Martin Lau - Now Is a Better Time to Buy China

Categorías: Blogs y opiniones de economia en ingles

Animal Spirits: The Best Way to Get a Raise

Today’s Animal Spirits is brought to you by YCharts

Mention Animal Spirits to receive 20% off when you initially sign up for the service.

On today’s show we discuss:

Crony Capitalism

Clayton fights for Bitcoin ETF

The best way to get a raise

Might be time to change how we think about debt

Don’t obsess over money

Boz Angeles

How much money to feel financial secure?

Disney Vax

Wal-Mart too

Corporations setti...

The post Animal Spirits: The Best Way to Get a Raise appeared first on The Irrelevant Investor.

Categorías: Blogs y opiniones de economia en ingles

CBDC Part 2: The tradeoffs

Last week, I introduced the concept of retail Central Bank Digital Currencies (CBDC) and why central banks may want to issue them. In this part, I am going to look at the practical difficulties that CBDC must overcome. I will do this by looking at the three basic functions of cash, namely to act as a medium of exchange, a store of value, and a unit of accounting. Hopefully, by doing this, you will understand why it is so much harder to launch a CBDC than any run-of-the-mill cryptocurrency or electronic payment system and get an appreciation for what a genius invention physical cash really is.

Store of value vs. medium of exchange

When we think of physical cash, we immediately think of it as a store of value and a medium of exchange. Cash is worth the same tomorrow (at least nominally) as it is today, and I can readily buy things with it in a store.

The problem with CBDC is that they are electronic and the folks in Silicon Valley and big cities might not realise this, but there are a lot of people who cannot live without physical cash. In 2019 the Access to Cash Review concluded that 17% of the population in the UK need physical cash to live their lives. Having only electronic cash available to them would cause serious disruptions in their business or make it impossible for them to purchase the goods they need for daily life. And this is in one of the most developed countries in the world. Across the Euro Area (EA) and Japan, the use of physical cash is far more prevalent than in the UK or the United States as the chart below shows.

Share of retail transactions done with cash

a.image2.image-link.image2-1178-946 { padding-bottom: 124.5243128964059%; padding-bottom: min(124.5243128964059%, 1178px); width: 100%; height: 0; } a.image2.image-link.image2-1178-946 img { max-width: 946px; max-height: 1178px; }Source: BIS

One key reason for this need for physical cash is that the IT and telecom infrastructure is not available to access modern electronic payment systems 24/7. And this is one of the key challenges for CBDC to overcome. A CBDC needs to be available 24/7 and cannot experience server outages or downtimes. This means that either there is an enormously robust IT infrastructure available everywhere (which would require billions in infrastructure investments even in the most developed countries), or the CBDC must be transferable and be usable as a method of exchange offline. The current thinking is that CBDC will likely be transferrable offline in limited amounts to enable its use as a method of exchange even in the absence of internet connections.

But here is the rub. If you can transfer it offline, how do you make sure it is a valid transaction? Distributed ledger technologies that are at the heart of all cryptocurrencies are based on the proof of work or the proof of stake concept where a transaction is validated by calculations on computers that proof you are the rightful owner of a coin. If you don’t have a connection to a computer, how do you come up with a proof of work or proof of stake? This is why there will likely be limits to the amount of CBDC that can change hands before a proof of stake will become necessary. If the proof of stake fails, the transactions can be unwound without disrupting the overall payment system too much.

But here is the next difficulty. If you use distributed ledger technology as the foundation of a CBDC, you increase its security because the information about the CBDC and past transactions is stored on many computers and thus less prone to hacks and cyber-attacks. Yet, by distributing the information about the CBDC tokens (or coins) you also reduce the transaction speed. Payment systems that are handled by a central ledger like every credit card system, electronic payment systems, or bank accounts can handle tens of thousands of transactions per second. Bitcoin can handle only a handful. Progress is being made in enabling cryptocurrencies to perform more transactions, but we are nowhere near the number of transactions that need to be made for a currency to act as a universal replacement for physical cash. If you want to create a CBDC that is a universal method of exchange, you need to compromise its safety and thus reduce the trust people have in it as a store of value.

This tension between store of value and medium of exchange is nothing new, by the way. In the days of the gold standard, a central bank could only increase the amount of money in circulation if it had enough gold bullions in its safe. This meant that if cash became scarce (e.g. during a recession or a run on banks), central banks had to increase interest rates to incentivise people to put more gold into its safe so it could issue more cash to the public. This is one of the key reasons why the Great Depression turned out so bad. The moment the economy faced a liquidity crunch, the central bank had to reduce liquidity even more to protect its gold holdings. This is unfortunately something gold fetishists forget all too often. It is only with the introduction of fiat money and the end of the gold standard that we could start to manage recession better and prevent waves of default during every economic downturn. Look at the decline in economic activity and the spike in unemployment during economic downturns in the era of the gold standard and the years since and you will see what we have gained by abandoning it.

The current thinking is that with CBDC it is probably best to err on the side of enabling more transactions rather than making it an incredibly safe store of value. Probably the best way to strike a balance is the use of CBDC that are either based on a centralised ledger or a distributed ledger technology but with a limited number of permissioned participants in the distributed ledger. Most likely such a technology would use commercial banks that are regulated by the central bank as the nodes of a distributed ledger network.

Even so, if you have a generally accepted store of value that can handle many transactions per second, you suddenly run into another problem. If CBDC are proper stores of value like physical cash, they could be used like traditional bank accounts. People could transfer electronic money from their bank accounts into CBDC and store their wealth there. You may say that this surely isn’t a problem, since you can just go to your bank and ask to get all the money in your bank account paid out in cash and your bank teller will readily oblige. That may be true for you and me, but in practice, there are limits to how much physical cash you can hold. First, there are the obvious limits that physical cash takes up space and you need to store it safely (you can also opt to leave it out in the open, but then its characteristic as a store of value may be undermined by its extreme fungibility as other people will help themselves to your stored value). But even if you managed to build a massive safe and hire a couple of security people and armoured vehicles to transport the cash from your bank to your safe, try getting any large amounts paid out to you. Why do you think there are no ETFs backed by physical cash anywhere in the world? In theory, these ETFs would accept people’s electronic money and invest it into physical cash stored in a vault. It’s a remarkably simple concept and in a world of negative interest rates, it can become a profitable investment since the cost of safekeeping for these large amounts is a few basis points compared to the 40 basis points or so people have to pay on bank deposits in the Eurozone, for example.

So, if we accept that in practice, you cannot hold unlimited amounts of physical cash, but with CBDC, it is easily possible to accumulate enormous amounts in a few seconds or minutes, we have to think about how we can limit the amount of CBDC held by any individual. This means limiting the amount of CBDC that can be held in any one electronic wallet. But more than that, it means that central banks or commercial banks have to be able to identify many different electronic wallets that belong to the same owner because otherwise, we would quickly see a virtual run on banks where bank deposits would be raided and moved into CBDC wallets thus creating a universal financial crisis that would make 2008 look like child’s play. But if we want to be able to control how much CBDC any one user can own across many different electronic wallets, we have to be able to identify the owner of each wallet. And this means that CBDC is no longer anonymous, but ownership can be linked to an individual. It’s like having to sign every bill you get in the shop with your name and the shopkeeper notifying the central bank of the new owner of the bill.

Now assume we introduce such an identification mechanism (even if it is anonymised) and combine it with distributed ledger technology. This means that the ownership of every unit of CBDC is not only stored at a computer in the central bank but a copy of it is stored on every computer participating in the network. And if that computer gets hacked, it might not bring down the network, but it will expose ownership of the different CBDC units. To make things even more fun, the GDPR in Europe enshrined a right to be forgotten into law. But a blockchain-based distributed ledger technology doesn’t forget. One of the components that makes it so safe and trustworthy is that it has an eternal memory of all transactions ever made with an electronic coin. But if you ingrain that technology into a CBDC and only one person in the EU buys one of these coins, the GDPR becomes applicable and with it this person’s right to be forgotten. Now you go deal with all the privacy lawyers in the world to sort that one out.

Currently, the only way out of this misery is to rely on centralised ledgers owned by the central bank or use distributed ledgers with only commercial banks permitted as nodes after they have done a proper KYC on their clients. For emerging markets with millions of unbanked people, a distributed ledger technology is probably not feasible anyway due to the required infrastructure. so, in these countries, one would expect a CBDC to be based on one central ledger held by the central bank. But that still means that the central bank can see your identity. The Chinese efforts in developing a CBDC go down this route by allowing every user of the CBDC to control who can see their identity. This way, users of CBDC can remain anonymous with the exception of one counterparty: The People’s Bank of China will always know who each user is. This is necessary to run the ledger but of course, it potentially could prove to be a weak point if a central bank is not independent of the government and may be forced by governments to hand over identifying information about CBDC ownership.

Meanwhile, the ECB has experimented with ‘anonymity vouchers’ that allow users of CBDC to transfer ownership of a limited amount of currency over a limited amount of time without their identity being known to counterparties or the central bank. But the problem here is still that the vouchers themselves have to be monitored and audited, which opens up the possibility to identify the users of these vouchers.

Method of exchange vs. unit of accounting

By now you have probably thrown your hands into the air about the difficulties of CBDC and their prospects of replacing physical cash. But let me throw one more obstacle at you. Physical cash is a natural unit of accounting in a way that most electronic cash is not. If you go to PayPal, for example, and you deposit money on your account, it becomes part of PayPal’s balance sheet. This is fine most of the time, but as I have discussed here, it can become a massive problem if PayPal becomes illiquid or bankrupt. Then, your money becomes part of the insolvency proceedings and you become an unsecured creditor of PayPal. This is not the case with physical cash or central bank-issued electronic money. That stuff has to stay around even if the payment provider goes under. One natural way to roll out a CBDC is for the central bank to issue the currency to commercial banks just like they do at the moment with traditional money (both physical and electronic). These commercial banks then distribute the money through loans, etc. Because of the fractional reserve system, the amount of money distributed across the economy is a multiple of the actual central bank money created in the first place. Because CBDC would be a replacement for physical cash, we have to assume that to roll out the CBDC, the commercial banks would be the distributors. Then, either these commercial banks or third-party firms would develop technologies like payment systems and electronic wallets to enable people to use CBDC as a method of exchange.

But these third-party firms that develop payment systems and electronic wallets can (and will) go bankrupt. And the CBDC has to be still in place after these companies have gone bankrupt. In fact, there has to be an easy mechanism to transfer CBDC from an insolvent payment provider to a solvent one in order to keep the financial system stable and avoid a run on banks.

But to do this, every payment provider needs to have separate accounts for its electronic cash and payments and for the CBDC so that it is straightforward to identify the CBDC if needed. That also means that every payment provider needs to know who owns which CBDC at any given point in time. Et voila, we are back to the privacy issue because now, all of a sudden, every CBDC coin has to be at least linked to a private key and ultimately an owner and that reduces privacy and makes it inferior to physical cash. I can already hear the cryptocurrency fans shouting at me that private keys for a token are anonymous, but these keys are either held in e-wallets or in accounts on crypto exchanges. Next week, I will talk about the security risks associated with these storage systems and why they may not be as anonymous as many people think.

If all of this feels like we are going in circles it’s because we are. The latest thinking is that CBDC will be less private than physical cash and that with the ownership of a CBDC coin will come an anonymised identifier of current ownership. This way, it is possible to track who owns the coins without identifying the person by name. Only once the person demands access to the CBDC can he or she show the identifier and proof of ownership. Nevertheless, the translation mechanism between the anonymous identifier and the name of the owner can be hacked and provides another security risk. But this is where we stop this week in order to pick it up next week to discuss the myriads of IT security issues with CBDC.

Categorías: Blogs y opiniones de economia en ingles

10 Reasons Why Stocks Fall

“It’s hard to hold onto stocks for a long period of time.”

Carl Kawaja said this in an excellent conversation with Patrick O’Shaughnessy.

This made me decide to revisit a post I did a few years back, Looking For the Next Amazon.

Amazon is one of the best-performing stocks ever, but it hasn’t been the easiest stock to hold over the last year. It’s up 6%, while the Nasdaq-100 is up almost...

The post 10 Reasons Why Stocks Fall appeared first on The Irrelevant Investor.

Categorías: Blogs y opiniones de economia en ingles

Páginas

Custom Search