Se encuentra usted aquí

Agregador de canales de noticias

5 highest yielding German dividend stocks

Learn more about the 5 highest yielding German dividend stocks. They all yield more than 4% and provide you with an attractive passive income.

The post 5 highest yielding German dividend stocks appeared first on European Dividend Growth Investor.

Categorías: Blogs y opiniones de economia en ingles

Boom Signal

Ultra-low interest rates and non-stop money supply growth are fueling the race to the bottom for global currency devaluation.

Frightening StatsFor instance, did you know that the global money supply has grown by over 5x in the past 20 years?

Here’s a chart that shows global money supply growth over the last two decades:

Massive amounts of government stimulus, negative interest rates, and ultra-low bond yields around the world have paved the way for soaring gold prices these past two years… setting investors up for a run at another long bull market.

The exciting part is that there’s still a lot of room left to run…

A major bull market can make any investor feel like an expert because a rising tide usually lifts all boats.

That said, there are always a few boats that rise much higher and faster than the others.

These are the investments that professional investors, fund managers, and billionaire resource speculators target for big wins.

A License to Print MoneyIn this crazy world we live in, there are few certainties.

Frankly, anyone peddling you a “sure thing” investment should be treated with extreme caution and skepticism.

But there’s one small corner of the market that’s created an incredible margin of safety for their operations, based around their profit margins.

It’s a unique business model that’s been copied by some of the world’s leading companies.

- Recently, Bill Ackman – one of the world’s leading hedge fund managers – raised billions of dollars trying to break into the sector.

What’s this mysterious line of business, you ask?

It’s the royalty business, and it’s applicable across many different industries.

Music, mining, oil and gas, TV shows and movies, and even oil change businesses are just a few of the many industries where you can find royalties at work.

Happy Birthday, Now Pay UpHave you ever heard the song “Happy Birthday?”

Of course, you have.

But what you probably didn’t know is that the royalties on the song brought in over $50 million to its owners, most recently Warner Music, just from it being used in movies and T.V.

Yes, the Happy Birthday song, the same one you’ve been singing since you were a kid, used to actually be under copyright owned by Warner Music and cost $25,000 each time it was used.

Songwriting brothers George and Ira Gershwin wrote an entire catalog of hits between 1920 and 1937.

- Today, their heirs make around $8 million per year in royalties from songs written nearly a hundred years ago.

More recently, Michael Jackson’s estate was paid $750 million to buy out 50% of his collection of music royalties.

Here’s the strange part of that story: the bulk of the song royalties weren’t even his. Michael Jackson bought the rights to over 4,000 songs, including 250 Beatles songs.

The Royalty Blueprint & Case StudyPioneered in the 1980s by two Canadians, Pierre Lassonde and Seymour Schulich started the first gold royalty company in the world, the original Franco Nevada.

They built the company on the simple framework of “exchange cash today, for a share of tomorrow’s production”.

Below is a chart which shows the “old” Franco Nevada’s incredible rise from CAD$0.21 per share and a market capitalization of CAD$2 million…

To the eventual buy-out by Newmont for CAD$2.5 billion at over CAD$33 per share.

That’s an incredible 15,614% return…

Following the exact same blueprint as the original Franco Nevada, a “new” Franco Nevada went public in 2007.

- Over the last 14 years, the stock has appreciated over 1,100% while gold has gone up 130%.

This should help further highlight the tremendous potential offered by investing in world-class royalty and streaming businesses.

By now, it should be very clear that gold royalty companies make for excellent investment opportunities.

The only question left is: which one to invest in?

Royalties and Streams Are Best Made in Hated MarketsTwo years ago, I was pounding the table on a company I was buying a lot of.

It was in a sector (uranium) that was cheap… it was hated… and no investor or media company wanted to go near it.

That’s when alligator investors like me spend MONTHS doing our due diligence. Except there were hardly any other investors.

This worked to my advantage.

Subscribers and I were able to position ourselves in a royalty company that was a first mover in the uranium industry.

- Fast forward 20 months later and my subscribers and I are up over 701% on that investment as of this writing.

Most importantly, this isn’t some illiquid nano-cap—it’s listed on the BIG U.S. exchanges. Primetime.

And the party’s just getting started. That was one corner of the resource sector where there was NO competition.

I get a real kick out of the poser gurus on social media who would send out messages in 2019 saying “Katusa failed” with his uranium play.

To all the haters, just look at the score—and nobody is doing better than the Katusa subscribers. Nobody.

Was it high risk and was patience required, yes. Nothing is ever guaranteed.

But if you’re not a subscriber to my premium research letter, you’re probably wondering what the next big score will be…

Well, you’re in luck.

Imagine if Bill Gates, Jeff Bezos and Elon Musk all backed a company in the tech sector.

How badly would you want to be an early investor? – I know I would.

Setups like this don’t happen often. And they’re definitely not like clockwork, but when you spot them, be prepared to act.

Because – if I’m right again – I’m convinced it will be another big score.

Regards,

Marin

The post Boom Signal appeared first on Katusa Research.

Categorías: Blogs y foros de trabajar madera en ingles

Google reduce beneficio en España tras elevar un 31% la plantilla de la filial

Categorías: 1 Noticias economicas en español

Hold my beer

CEOs aren’t the kind of people that are commonly known for their humility. Instead, many CEOs are type-A personalities who are extremely competitive. But in some instances, competitiveness can go too far and CEOs in an effort to outdo their peers start to make poor decisions. It’s the classic ‘hold my beer’ moment, where one CEO sees some other guy do something stupid and then decides he can top that.

Nowhere is this reaction more dangerous than at the high stakes game of M&A. The sums involved are large and the impact on a company’s fortunes equally so. Yet, because these are events that often attract a lot of media attention, the temptation to outdo your peers is extremely high for some CEOs. So, instead of acquiring smaller companies that may be a better fit to an existing business and can more easily be integrated into the existing corporate structure (and adopt the existing corporate culture), they are going for fewer but larger mergers and acquisitions. That might end well, just as sometimes a drunk at a bar says ‘hold my beer’ and then performs some amazing feat.

But usually, giving a CEO a lot of liquidity to spend on M&A is like giving a drunk a barrel of beer. You know exactly what is going to happen, you just don’t know which wall he is going to hit.

Examining 751 takeovers in the UK by 202 CEOs between 2007 and 2016, Tom Aabo and his colleagues showed that some CEOs are prone to making fewer but much larger acquisitions for their firms than others. The humbler CEOs made on average three acquisitions during these ten years, each worth about £57m. The high stakes CEOs, on the other hand, made on average one acquisition worth about £351m.

By pursuing these larger takeovers, these CEOs may strike their egos but create costs for shareholders because the share price reacts much less favourably to these large takeover bids than to smaller ones. On the day of the announcement, the large takeovers on average lead to an abnormal share price increase of 0.6% while the smaller takeovers lead to an abnormal share price increase of 2.7%. and because the CEOs who acquire larger targets do so less often than the CEOs who acquire smaller firms, this effect accumulates over time and leads to a better share price performance for companies that make smaller, less costly acquisitions.

So, who are these CEOs that go for fewer but larger acquisitions? How can we identify them as investors? And how can directors of a company identify them in order to limit their acquisition budgets to avoid destroying shareholder value?

In the above-mentioned study, the CEOs that went big were the ones that showed more signs of narcissistic behaviour. And while the study measured narcissism in different ways all of which had similar outcomes, one easy way to measure it is to listen to the CEOs during earnings calls (or rather, analyse the transcripts of these calls). Narcissistic CEOs use more personal pronouns that point to them like ‘I’, ‘my’, ‘mine’ than personal pronouns that point to a group or other people. The higher this ratio of first person personal pronouns to all personal pronouns is, the more likely it is that a CEO will try to engage in dumb outsized acquisitions that will lead to lower shareholder value.

CEO personality and takeover activity

a.image2.image-link.image2-470-972 { padding-bottom: 48.35390946502058%; padding-bottom: min(48.35390946502058%, 470px); width: 100%; height: 0; } a.image2.image-link.image2-470-972 img { max-width: 972px; max-height: 470px; }Source: Aabo et al. (2021)

Categorías: Blogs y opiniones de economia en ingles

The Fool Or The One That Follows?

Sadly, in an Idiocracy, there is no strength in numbers. Far too many people nowadays are seeking consensus from like-minded fools. On the 13th anniversary since Lehman, these corruption zealots STILL haven't learned that con men can't be trusted. The revelation will be biblical in scale and impact...

As the world implodes in real-time, led by the second largest economy and the most important economy from a marginal demand standpoint, still there remains a steadfast belief in "inflation", bought with both hands by true believers in serial fraud and criminality.

In my last post I laid out the case for why we will soon see record deflation as China implodes for the last time in this "cycle". Ironically, it was the U.S. property market that imploded in 2008, while China led the world to recovery. This time around, China is the weak link as their property market has continued to become ever more over-leveraged since Lehman.

Too many people nowadays have been convinced that a collapsed standard of living is driving "inflation". They believe that losing a full time job with benefits and turning to gig work is driving up their cost of living. Hence they believe the inflation hysteria. However, on a macro level, millions of people losing full time benefits and turning to marginalized "gig jobs" which generally pay a fraction of the wages and ZERO benefits, is highly deflationary. It takes a huge chunk out of long-term demand.

Nevertheless, the inflation hypothesis is rampant and of course it's politically motivated to cast aspersions on Joe Biden's economic program. And therefore it's self-fulfilling, people are told there are shortages so what do they do they hoard merchandise - homes, and cars, and AR15s etc. In the process THEY are creating the self-fulfilling "inflation". Nevertheless, it's not sustainable by any means. It's solely a function of cheap money and record leverage and collapsed morality.

"Never seen anything like it," Musk tweeted on Wednesday. "Fear of running out [of computer chips] is causing every company to overorder — like the toilet paper shortage, but at epic scale."

"That said, it's obviously not a long-term issue".

There is nothing obvious in an Idiocracy. They specialize in ignoring obvious risks and they've been incentivized by central banks to do so.

Semiconductors are at the intersection of the spike in car prices and the spike in Tech stonks. Last week, China fined three auto parts distributors for hoarding semiconductors in order to drive up prices. I know.

When semis reverse this rising wedge, the auto bubble AND the Tech bubble will explode at the same time. There is no way a hundred dollar part is worth an additional $8k for a $35k car I was checking out recently.

In the deflationary collapse, cars will be selling for cents on the dollar.

There are only two real sources of sustainable inflation in this pseudo-economy - college tuition and healthcare. These two eminently corrupt cartels have far outstripped the rest of the economy in price increases year after year. And in doing so they have forced the middle class to cut costs in every other part of their lifestyle. Again, that is not overall inflation.

This hoarding obsession at the brink of the most deflationary crisis in world history can only end catastrophically for those people who believe in it. The deflationary instinct is to cut debt and leverage and reduce lifestyle, which is what the masses should be doing right now if not the past decade since the Lehman warning. The inflationary instinct however is to expand debt and hoard merchandise, which is what the sheeple have been doing. Once again, Wall Street's penchant for being wrong at the end of the cycle is coming around one more time for bailout. And this time who can the sheeple blame but themselves for believing today's ubiquitous con men. The inflation hypothesis which is spewed forth by Faux News, is now rampant. Aside from politics which infects every viewpoint nowadays, the reason so few investors see this coming is a function of lack of empathy for the working class who are now drowning in this post-COVID virtual economy. Removing unemployment support while there are near record numbers of long-term unemployed is greatly exacerbating the deflationary impulse. Add in impending Fed taper, the debt ceiling stalemate, record asset valuations, record IPO issuance, and record leverage, it's a disaster wanting to happen. Decade low consumer sentiment can only go lower from here, which portends badly for bailout addicts.

The fact that markets are already overweight Tech stocks while this fake inflation thesis abides, is a glaring warning as to what happens next. When the deflation freight train arrives from the other direction, there will be NOWHERE to hide.

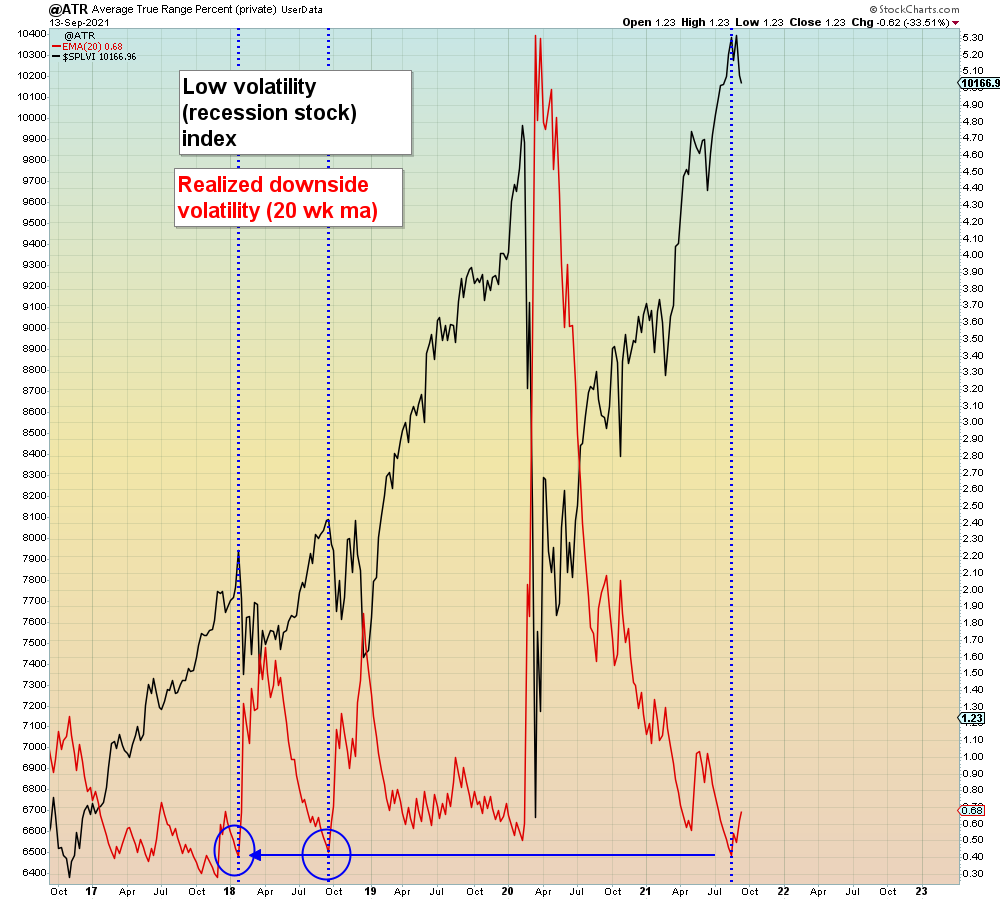

As I pointed out recently on Twitter, the low vol recession "safe havens" have seen the lowest realized volatility in three years:

While U.S. gamblers have been buying the overnight dip every day since the Jackson Hole high, Asian markets have been rolling over again, led by Hong Kong.

The IBD 50 growth index is carving out the same pattern as 2018 the last time global deflation was ignored in the U.S.:

Overlaying the IBD 50 behind the MSCI China stock index shows the magnitude of denial.

In summary, it's FOMC time again: Fear Of Missing Crash.

{kind=link}

As the world implodes in real-time, led by the second largest economy and the most important economy from a marginal demand standpoint, still there remains a steadfast belief in "inflation", bought with both hands by true believers in serial fraud and criminality.

In my last post I laid out the case for why we will soon see record deflation as China implodes for the last time in this "cycle". Ironically, it was the U.S. property market that imploded in 2008, while China led the world to recovery. This time around, China is the weak link as their property market has continued to become ever more over-leveraged since Lehman.

Too many people nowadays have been convinced that a collapsed standard of living is driving "inflation". They believe that losing a full time job with benefits and turning to gig work is driving up their cost of living. Hence they believe the inflation hysteria. However, on a macro level, millions of people losing full time benefits and turning to marginalized "gig jobs" which generally pay a fraction of the wages and ZERO benefits, is highly deflationary. It takes a huge chunk out of long-term demand.

Nevertheless, the inflation hypothesis is rampant and of course it's politically motivated to cast aspersions on Joe Biden's economic program. And therefore it's self-fulfilling, people are told there are shortages so what do they do they hoard merchandise - homes, and cars, and AR15s etc. In the process THEY are creating the self-fulfilling "inflation". Nevertheless, it's not sustainable by any means. It's solely a function of cheap money and record leverage and collapsed morality.

"Never seen anything like it," Musk tweeted on Wednesday. "Fear of running out [of computer chips] is causing every company to overorder — like the toilet paper shortage, but at epic scale."

"That said, it's obviously not a long-term issue".

There is nothing obvious in an Idiocracy. They specialize in ignoring obvious risks and they've been incentivized by central banks to do so.

Semiconductors are at the intersection of the spike in car prices and the spike in Tech stonks. Last week, China fined three auto parts distributors for hoarding semiconductors in order to drive up prices. I know.

When semis reverse this rising wedge, the auto bubble AND the Tech bubble will explode at the same time. There is no way a hundred dollar part is worth an additional $8k for a $35k car I was checking out recently.

In the deflationary collapse, cars will be selling for cents on the dollar.

{kind=link}

There are only two real sources of sustainable inflation in this pseudo-economy - college tuition and healthcare. These two eminently corrupt cartels have far outstripped the rest of the economy in price increases year after year. And in doing so they have forced the middle class to cut costs in every other part of their lifestyle. Again, that is not overall inflation.

This hoarding obsession at the brink of the most deflationary crisis in world history can only end catastrophically for those people who believe in it. The deflationary instinct is to cut debt and leverage and reduce lifestyle, which is what the masses should be doing right now if not the past decade since the Lehman warning. The inflationary instinct however is to expand debt and hoard merchandise, which is what the sheeple have been doing. Once again, Wall Street's penchant for being wrong at the end of the cycle is coming around one more time for bailout. And this time who can the sheeple blame but themselves for believing today's ubiquitous con men. The inflation hypothesis which is spewed forth by Faux News, is now rampant. Aside from politics which infects every viewpoint nowadays, the reason so few investors see this coming is a function of lack of empathy for the working class who are now drowning in this post-COVID virtual economy. Removing unemployment support while there are near record numbers of long-term unemployed is greatly exacerbating the deflationary impulse. Add in impending Fed taper, the debt ceiling stalemate, record asset valuations, record IPO issuance, and record leverage, it's a disaster wanting to happen. Decade low consumer sentiment can only go lower from here, which portends badly for bailout addicts.

The fact that markets are already overweight Tech stocks while this fake inflation thesis abides, is a glaring warning as to what happens next. When the deflation freight train arrives from the other direction, there will be NOWHERE to hide.

As I pointed out recently on Twitter, the low vol recession "safe havens" have seen the lowest realized volatility in three years:

{kind=link}

While U.S. gamblers have been buying the overnight dip every day since the Jackson Hole high, Asian markets have been rolling over again, led by Hong Kong.

{kind=link}

The IBD 50 growth index is carving out the same pattern as 2018 the last time global deflation was ignored in the U.S.:

{kind=link}

Overlaying the IBD 50 behind the MSCI China stock index shows the magnitude of denial.

{kind=link}

In summary, it's FOMC time again: Fear Of Missing Crash.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

How World Bank leaders put pressure on staff to alter a global index

An investigation puts paid to the Doing Business rankings, and puts Kristalina Georgieva in the spotlight

Categorías: 3 Noticias economicas ingles

Hurricane Ida Finale

After a few conversations with readers this week, I realized that I never wrote a finale to our Hurricane Ida experience. My apologies, this is my brain on a hurricane. The personal news is that we were fine. Our house suffered no damage or water intrusion. We were able to confirm this late in the day after the storm. A friend was able to empty our fridge before it got bad, and he saved a lot of our freezer items with a g...

The post Hurricane Ida Finale appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

Boring is Beautiful

The stock market isn’t making news right now. The news this morning was dominated by a nuclear deal between the US, UK, and Australia, the chaos in Afghanistan, and the first civilian spaceflight by SpaceX. There’s a lot going on in the world, and the stock market is boring. I love it this way.

In the early ’90s, the Chicago Board Options Exchange (CBOE) began calculating the implied volatility of the s...

The post Boring is Beautiful appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

Alfonso Gallego de Chaves, nuevo Head of Affinity, SMEs & Digital Solutions de Aon en EMEA

Alfonso Gallego de Chaves ocupaba hasta ahora el puesto de Managing Director de Aon Affinity y Retirement Iberia, cargo que compatibilizaba desde 2018 con el de Head of Growth Countries Affinity EMEA. Con anterioridad había desempeñado distintos puestos de responsabilidad en la firma en áreas como Grandes Cuentas o Health & Benefits. Alfonso, residente en Madrid, está casado y tiene dos hijos.

Acerca de Aon

Aon plc (NYSE: AON) es una empresa líder en servicios profesionales globales que ofrece un amplio abanico de soluciones de riesgos, jubilación y salud. Nuestros 50.000 empleados en 120 países desarrollan al máximo las posibilidades de nuestros clientes utilizando data & analytics propios que nos permiten ayudar a reducir la volatilidad y mejorar los resultados

Categorías: 1 Noticias economicas en español

Keir Starmer, the post-populist

The Labour leader has a vision of Britain after upheaval

Categorías: 3 Noticias economicas ingles

Argentine voters deal a blow to the ruling Peronist coalition

The primary elections are both a referendum on the government and an augury for elections in November

Categorías: 3 Noticias economicas ingles

Agriculture is an economic bright spot in Mexico

That is, if President Andrés Manuel López Obrador does not mess it up

Categorías: 3 Noticias economicas ingles

Abimael Guzmán’s death leaves several questions for Peru

Not least as Pedro Castillo, the new president, has several allies with links to Shining Path

Categorías: 3 Noticias economicas ingles

Middle Eastern foes are giving diplomacy a shot

Exhausted from years of conflict and eager for growth, rivals are talking

Categorías: 3 Noticias economicas ingles

What next for Islamists in the Arab world?

Setbacks in Morocco and Tunisia mark the end of a tough decade for Islamists

Categorías: 3 Noticias economicas ingles

The Gates Foundation’s approach has both advantages and limits

Data isn’t everything, even for the world’s most powerful charity

Categorías: 3 Noticias economicas ingles

How Britain plans to co-exist with covid-19

Vaccine passports, masks and working from home will only be back-up options

Categorías: 3 Noticias economicas ingles

Battersea offers lessons in regeneration

A big development scheme in London suggests how those elsewhere could succeed

Categorías: 3 Noticias economicas ingles

Britain’s successful startups are surprisingly scattered

And it is better at rearing them than its European neighbours

Categorías: 3 Noticias economicas ingles

Páginas

Custom Search