Se encuentra usted aquí

Blogs y opiniones de economia en ingles

The Fool Or The One That Follows?

Sadly, in an Idiocracy, there is no strength in numbers. Far too many people nowadays are seeking consensus from like-minded fools. On the 13th anniversary since Lehman, these corruption zealots STILL haven't learned that con men can't be trusted. The revelation will be biblical in scale and impact...

As the world implodes in real-time, led by the second largest economy and the most important economy from a marginal demand standpoint, still there remains a steadfast belief in "inflation", bought with both hands by true believers in serial fraud and criminality.

In my last post I laid out the case for why we will soon see record deflation as China implodes for the last time in this "cycle". Ironically, it was the U.S. property market that imploded in 2008, while China led the world to recovery. This time around, China is the weak link as their property market has continued to become ever more over-leveraged since Lehman.

Too many people nowadays have been convinced that a collapsed standard of living is driving "inflation". They believe that losing a full time job with benefits and turning to gig work is driving up their cost of living. Hence they believe the inflation hysteria. However, on a macro level, millions of people losing full time benefits and turning to marginalized "gig jobs" which generally pay a fraction of the wages and ZERO benefits, is highly deflationary. It takes a huge chunk out of long-term demand.

Nevertheless, the inflation hypothesis is rampant and of course it's politically motivated to cast aspersions on Joe Biden's economic program. And therefore it's self-fulfilling, people are told there are shortages so what do they do they hoard merchandise - homes, and cars, and AR15s etc. In the process THEY are creating the self-fulfilling "inflation". Nevertheless, it's not sustainable by any means. It's solely a function of cheap money and record leverage and collapsed morality.

"Never seen anything like it," Musk tweeted on Wednesday. "Fear of running out [of computer chips] is causing every company to overorder — like the toilet paper shortage, but at epic scale."

"That said, it's obviously not a long-term issue".

There is nothing obvious in an Idiocracy. They specialize in ignoring obvious risks and they've been incentivized by central banks to do so.

Semiconductors are at the intersection of the spike in car prices and the spike in Tech stonks. Last week, China fined three auto parts distributors for hoarding semiconductors in order to drive up prices. I know.

When semis reverse this rising wedge, the auto bubble AND the Tech bubble will explode at the same time. There is no way a hundred dollar part is worth an additional $8k for a $35k car I was checking out recently.

In the deflationary collapse, cars will be selling for cents on the dollar.

There are only two real sources of sustainable inflation in this pseudo-economy - college tuition and healthcare. These two eminently corrupt cartels have far outstripped the rest of the economy in price increases year after year. And in doing so they have forced the middle class to cut costs in every other part of their lifestyle. Again, that is not overall inflation.

This hoarding obsession at the brink of the most deflationary crisis in world history can only end catastrophically for those people who believe in it. The deflationary instinct is to cut debt and leverage and reduce lifestyle, which is what the masses should be doing right now if not the past decade since the Lehman warning. The inflationary instinct however is to expand debt and hoard merchandise, which is what the sheeple have been doing. Once again, Wall Street's penchant for being wrong at the end of the cycle is coming around one more time for bailout. And this time who can the sheeple blame but themselves for believing today's ubiquitous con men. The inflation hypothesis which is spewed forth by Faux News, is now rampant. Aside from politics which infects every viewpoint nowadays, the reason so few investors see this coming is a function of lack of empathy for the working class who are now drowning in this post-COVID virtual economy. Removing unemployment support while there are near record numbers of long-term unemployed is greatly exacerbating the deflationary impulse. Add in impending Fed taper, the debt ceiling stalemate, record asset valuations, record IPO issuance, and record leverage, it's a disaster wanting to happen. Decade low consumer sentiment can only go lower from here, which portends badly for bailout addicts.

The fact that markets are already overweight Tech stocks while this fake inflation thesis abides, is a glaring warning as to what happens next. When the deflation freight train arrives from the other direction, there will be NOWHERE to hide.

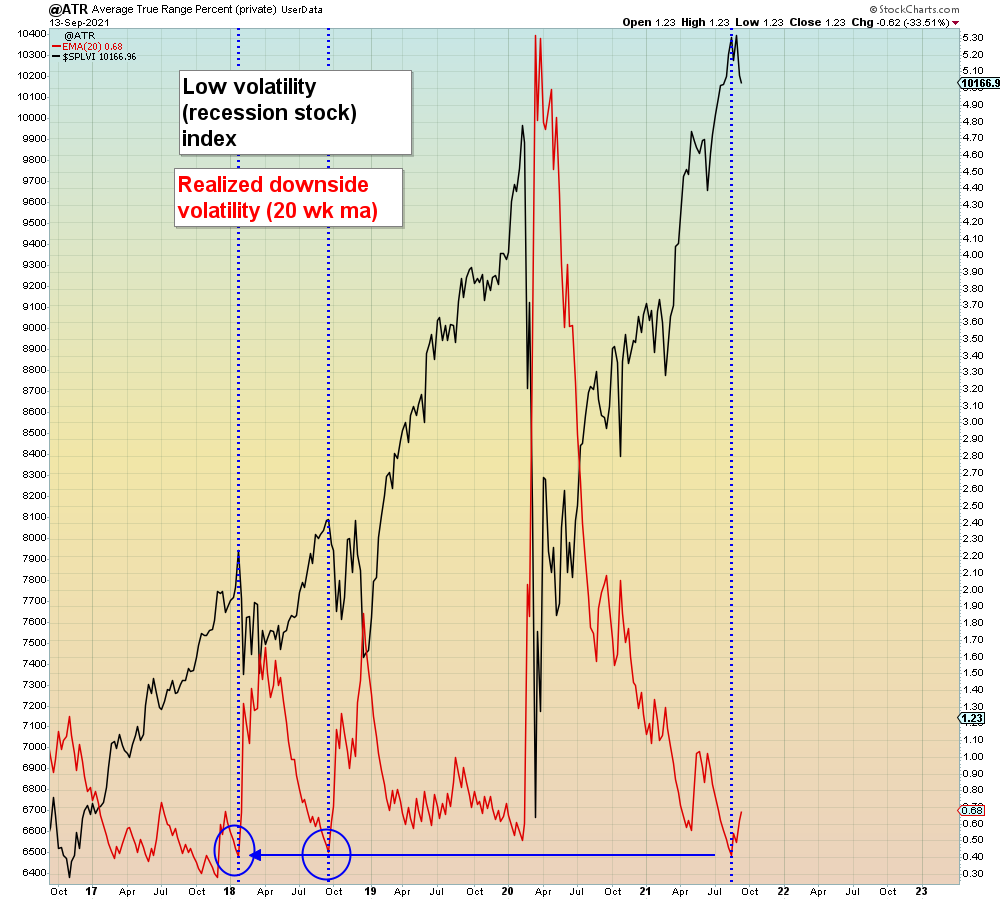

As I pointed out recently on Twitter, the low vol recession "safe havens" have seen the lowest realized volatility in three years:

While U.S. gamblers have been buying the overnight dip every day since the Jackson Hole high, Asian markets have been rolling over again, led by Hong Kong.

The IBD 50 growth index is carving out the same pattern as 2018 the last time global deflation was ignored in the U.S.:

Overlaying the IBD 50 behind the MSCI China stock index shows the magnitude of denial.

In summary, it's FOMC time again: Fear Of Missing Crash.

{kind=link}

As the world implodes in real-time, led by the second largest economy and the most important economy from a marginal demand standpoint, still there remains a steadfast belief in "inflation", bought with both hands by true believers in serial fraud and criminality.

In my last post I laid out the case for why we will soon see record deflation as China implodes for the last time in this "cycle". Ironically, it was the U.S. property market that imploded in 2008, while China led the world to recovery. This time around, China is the weak link as their property market has continued to become ever more over-leveraged since Lehman.

Too many people nowadays have been convinced that a collapsed standard of living is driving "inflation". They believe that losing a full time job with benefits and turning to gig work is driving up their cost of living. Hence they believe the inflation hysteria. However, on a macro level, millions of people losing full time benefits and turning to marginalized "gig jobs" which generally pay a fraction of the wages and ZERO benefits, is highly deflationary. It takes a huge chunk out of long-term demand.

Nevertheless, the inflation hypothesis is rampant and of course it's politically motivated to cast aspersions on Joe Biden's economic program. And therefore it's self-fulfilling, people are told there are shortages so what do they do they hoard merchandise - homes, and cars, and AR15s etc. In the process THEY are creating the self-fulfilling "inflation". Nevertheless, it's not sustainable by any means. It's solely a function of cheap money and record leverage and collapsed morality.

"Never seen anything like it," Musk tweeted on Wednesday. "Fear of running out [of computer chips] is causing every company to overorder — like the toilet paper shortage, but at epic scale."

"That said, it's obviously not a long-term issue".

There is nothing obvious in an Idiocracy. They specialize in ignoring obvious risks and they've been incentivized by central banks to do so.

Semiconductors are at the intersection of the spike in car prices and the spike in Tech stonks. Last week, China fined three auto parts distributors for hoarding semiconductors in order to drive up prices. I know.

When semis reverse this rising wedge, the auto bubble AND the Tech bubble will explode at the same time. There is no way a hundred dollar part is worth an additional $8k for a $35k car I was checking out recently.

In the deflationary collapse, cars will be selling for cents on the dollar.

{kind=link}

There are only two real sources of sustainable inflation in this pseudo-economy - college tuition and healthcare. These two eminently corrupt cartels have far outstripped the rest of the economy in price increases year after year. And in doing so they have forced the middle class to cut costs in every other part of their lifestyle. Again, that is not overall inflation.

This hoarding obsession at the brink of the most deflationary crisis in world history can only end catastrophically for those people who believe in it. The deflationary instinct is to cut debt and leverage and reduce lifestyle, which is what the masses should be doing right now if not the past decade since the Lehman warning. The inflationary instinct however is to expand debt and hoard merchandise, which is what the sheeple have been doing. Once again, Wall Street's penchant for being wrong at the end of the cycle is coming around one more time for bailout. And this time who can the sheeple blame but themselves for believing today's ubiquitous con men. The inflation hypothesis which is spewed forth by Faux News, is now rampant. Aside from politics which infects every viewpoint nowadays, the reason so few investors see this coming is a function of lack of empathy for the working class who are now drowning in this post-COVID virtual economy. Removing unemployment support while there are near record numbers of long-term unemployed is greatly exacerbating the deflationary impulse. Add in impending Fed taper, the debt ceiling stalemate, record asset valuations, record IPO issuance, and record leverage, it's a disaster wanting to happen. Decade low consumer sentiment can only go lower from here, which portends badly for bailout addicts.

The fact that markets are already overweight Tech stocks while this fake inflation thesis abides, is a glaring warning as to what happens next. When the deflation freight train arrives from the other direction, there will be NOWHERE to hide.

As I pointed out recently on Twitter, the low vol recession "safe havens" have seen the lowest realized volatility in three years:

{kind=link}

While U.S. gamblers have been buying the overnight dip every day since the Jackson Hole high, Asian markets have been rolling over again, led by Hong Kong.

{kind=link}

The IBD 50 growth index is carving out the same pattern as 2018 the last time global deflation was ignored in the U.S.:

{kind=link}

Overlaying the IBD 50 behind the MSCI China stock index shows the magnitude of denial.

{kind=link}

In summary, it's FOMC time again: Fear Of Missing Crash.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Hurricane Ida Finale

After a few conversations with readers this week, I realized that I never wrote a finale to our Hurricane Ida experience. My apologies, this is my brain on a hurricane. The personal news is that we were fine. Our house suffered no damage or water intrusion. We were able to confirm this late in the day after the storm. A friend was able to empty our fridge before it got bad, and he saved a lot of our freezer items with a g...

The post Hurricane Ida Finale appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

Boring is Beautiful

The stock market isn’t making news right now. The news this morning was dominated by a nuclear deal between the US, UK, and Australia, the chaos in Afghanistan, and the first civilian spaceflight by SpaceX. There’s a lot going on in the world, and the stock market is boring. I love it this way.

In the early ’90s, the Chicago Board Options Exchange (CBOE) began calculating the implied volatility of the s...

The post Boring is Beautiful appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

The Long View: Laura Carstensen - 'I'm Suggesting We Change the Way We Work'

Categorías: Blogs y opiniones de economia en ingles

First Eagle Investment Management

Bought: ATEN AIR ACHC ACR ADTN AEIS ASIX AL AA ALEX ATI ALGT AOSL APEI AVD AMWD CRMT AMKR ASYS APOG AROC ACA ASC AHH AINC ATRO AAWW AVYA AVT AX RILY BW BHR CAMP PRTS CRS CARS CSLT CVCO CNTY CCS CLDT CHEF CHK CIR COHU FIX CMC CVGI CMTL CONN CVA CCRN CUTR DAN DSKE DSX DGII DHC DXYN LPG DS DCO DZSI ESTE NPO ETD FN GSM FFWM FLXN FORM ROCK GLT GPX GRBK GFF HAYN HCI HP HRI HCCI HRTG HXL HTH HZN HMHC HLI HUBG HUN ICHR IIVI INFN IDCC TILE IPI IIN ITI JAX JELD KLR KAR KIRK KRA KLIC LAKE LGIH LMB LIQT LTHM LXU LYTS LL LXFR MAC MNTX MCHX MCS MTDR MTOR MESA MTG MGPI MG MOD MC MGI NGVC NVGS STIM NWHM NR NMIH NNBR NDLS ORI OLN ZEUS ONTO OOMA OPCH ORN OCDX OFIX OSTK PKOH PCTI PGTI PBI PBPB PRIM QRHC QNST RDN RLGT RLGY REPH REED RGS RUTH SBCF SCWX SIC SEM SIEN SIX SKY SAH SCS STC SRI SUP SRGA SKT TPR TMHC TCBI TMST TOL TREC TPH TRN TSC TGI TROX TBI SLCA USX UCTT UFAB UFCS UNVR VECO VIAO VSH VSEC WNC WCC ZVO

Added to: BABA WLTW BDX NOV KOF TSM HCA HD MMP ORLA DEI CRH BTG NG AU RDS.A CRM SNY ABEV UL GOLD MAG LYG DEO CCU FMX GSK BTI BXP KGC KL AGI

Categorías: Blogs y opiniones de economia en ingles

The Most Deflationary Event In History

The COVID pandemic accelerated all of the deflationary factors that resulted from decades of "free trade" which culminated in the desperate gambit of using homes as ATM machines. This time, the internet virtualization of the economy went into overdrive during the COVID lockdown phase amid global mass layoffs 4x the rate of 2008. And yet today's economic illiterates see nothing but "inflation", which they are praying will keep a bid under their hyper-inflated risk assets...

The only disagreement is from the bond market.

For the record, the COVID pandemic was the most deflationary event in modern world history. How do we know? Because oil went negative for the first time ever. Now it has recovered back to the pre-pandemic level and copious morons are convinced THIS is inflation.

Here we see that reflation expectations and the oil market track each other 1:1.

Last year's deflation "event" is quite clear on this chart.

There is no doubt that on the supply side, bottlenecks in the global supply chain have been exacerbated by this halting clusterfuck of an economic restart as Keystone Kops policy-makers use "science" as an excuse to implode the economy.

Unfortunately, as indicated by decade low consumer sentiment, there will be NO demand-side follow-through to keep this level of "inflation" sustained. Even less likely now that the pandemic emergency unemployment program has officially ended.

Nevertheless, it's clear that today's economic illiterates still haven't learned that "inflation" is always highest at the end of the cycle and lowest at the beginning.

With the CPI report due out this week, I have no doubt that we will be hearing plenty of inflation hysteria. All of which is highly reminiscent of September 2008 when the collapsing banking dominoes were ignored due to end of cycle inflation concerns.

Needless to say I am dubious of this strategy of bidding up every asset class ahead of what will soon become the NEW most deflationary event in global history making last year's gamble-from-home vacation seem like a picnic.

I can't see how artificially bidding up prices to unsustainable levels AND thereby maximizing liabilities ahead of a burgeoning global debt crisis makes any sense. One thing we know for certain is that it has certainly raised the political stakes resulting from the fallout of this failed gambit.

Here we see that auto loans have been going parabolic since the pandemic began. At a level not seen since the Y2K Tech bubble:

I believe this is a bad idea.

Auto loans, $ change billions

Gamblers are also ignoring the fact that the prime beneficiaries of this "inflation" bubble have been the mega cap Tech deflation trades. Stocks that have been on a parabolic rise higher since the pandemic began.

This chart shows that the average U.S. stock gave up ALL of its past decade gains during the pandemic. It shows that Tech stocks accounts for virtually of the "market" gains. Which means that the S&P 500 has turned into a closet Tech bubble.

Another warning sign. IGNORED.

I've heard many people claim that this is a "stagflationary" event. However, the stagflation of the 1970s took place when capacity utilization was near record highs AND labor share of the economy was AT record highs. Today, both are at RECORD lows.

Imagine how happy Jeff Bezos is now that he has millions more drivers to deliver bon bons in real-time. Now yuppies can click a button and hear the doorbell ring :15 minutes later.

True paradise.

In summary, this is all very reminiscent of September 2008, only this time the stakes are 10x higher.

"Evergrande has the distinction of being the world’s most debt-saddled property developer and has been on life support for months. A steady drumbeat of bad news in recent weeks has accelerated what many experts warn is inevitable: failure."

Observers are watching to see if Chinese regulators make good on their pledge to clean up the country’s corporate sector by letting “debt bombs” like Evergrande collapse"

Back in September 2008, the Fed let Lehman collapse. And then the Disney markets shit a brick when they realized there IS such a thing as real losses.

Position accordingly.

The only disagreement is from the bond market.

{kind=link}

For the record, the COVID pandemic was the most deflationary event in modern world history. How do we know? Because oil went negative for the first time ever. Now it has recovered back to the pre-pandemic level and copious morons are convinced THIS is inflation.

{kind=link}

Here we see that reflation expectations and the oil market track each other 1:1.

Last year's deflation "event" is quite clear on this chart.

{kind=link}

There is no doubt that on the supply side, bottlenecks in the global supply chain have been exacerbated by this halting clusterfuck of an economic restart as Keystone Kops policy-makers use "science" as an excuse to implode the economy.

Unfortunately, as indicated by decade low consumer sentiment, there will be NO demand-side follow-through to keep this level of "inflation" sustained. Even less likely now that the pandemic emergency unemployment program has officially ended.

Nevertheless, it's clear that today's economic illiterates still haven't learned that "inflation" is always highest at the end of the cycle and lowest at the beginning.

With the CPI report due out this week, I have no doubt that we will be hearing plenty of inflation hysteria. All of which is highly reminiscent of September 2008 when the collapsing banking dominoes were ignored due to end of cycle inflation concerns.

{kind=link}

Needless to say I am dubious of this strategy of bidding up every asset class ahead of what will soon become the NEW most deflationary event in global history making last year's gamble-from-home vacation seem like a picnic.

I can't see how artificially bidding up prices to unsustainable levels AND thereby maximizing liabilities ahead of a burgeoning global debt crisis makes any sense. One thing we know for certain is that it has certainly raised the political stakes resulting from the fallout of this failed gambit.

Here we see that auto loans have been going parabolic since the pandemic began. At a level not seen since the Y2K Tech bubble:

I believe this is a bad idea.

Auto loans, $ change billions

{kind=link}

Gamblers are also ignoring the fact that the prime beneficiaries of this "inflation" bubble have been the mega cap Tech deflation trades. Stocks that have been on a parabolic rise higher since the pandemic began.

This chart shows that the average U.S. stock gave up ALL of its past decade gains during the pandemic. It shows that Tech stocks accounts for virtually of the "market" gains. Which means that the S&P 500 has turned into a closet Tech bubble.

Another warning sign. IGNORED.

{kind=link}

I've heard many people claim that this is a "stagflationary" event. However, the stagflation of the 1970s took place when capacity utilization was near record highs AND labor share of the economy was AT record highs. Today, both are at RECORD lows.

Imagine how happy Jeff Bezos is now that he has millions more drivers to deliver bon bons in real-time. Now yuppies can click a button and hear the doorbell ring :15 minutes later.

True paradise.

{kind=link}

In summary, this is all very reminiscent of September 2008, only this time the stakes are 10x higher.

"Evergrande has the distinction of being the world’s most debt-saddled property developer and has been on life support for months. A steady drumbeat of bad news in recent weeks has accelerated what many experts warn is inevitable: failure."

Observers are watching to see if Chinese regulators make good on their pledge to clean up the country’s corporate sector by letting “debt bombs” like Evergrande collapse"

Back in September 2008, the Fed let Lehman collapse. And then the Disney markets shit a brick when they realized there IS such a thing as real losses.

Position accordingly.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Snap’s Shares Soar As Institutions Build Big Positions

Snap Inc. (SNAP) experienced soaring growth over the last ten months, significantly outperforming the S&P 500. The camera and social media company’s stock rose by approximately 357.0% since the start of 2020 compared to the S&P’s gain of about 39.1%. Given this astounding level of growth, it is understandable to see hedge funds and institutions actively buying.

Snap is widely known for its technological products and services, such as the Snapchat application for smartphones and Bitmoji, personalized cartoon avatars. Snap also recently announced augmented reality smart glasses geared towards developers, called Spectacles. Snap originated as a camera company, utilizing its Snapchat camera app to connect people through a playful medium and sell advertising space. It ultimately grew into a strong player in the social media industry, focusing on empowering self-expression, increasing communication among family and friends, and general entertainment. While Snap experienced a decline in value during the earlier stages of the coronavirus pandemic, the stock has seen rapid growth in 2021 with boosts in digital advertising spending and greater demand for advertising partnerships.

{kind=link}

Hedge Funds Are Enthusiastic

Hedge funds and institutions heavily bought Snap’s stock in the second quarter of 2021. For hedge funds, the aggregate 13F shares held increased to about 219.7 million from 207.7 million, an increase of approximately 5.8%. Of the hedge funds, 41 created new positions, 71 added to existing ones, 40 closed out their holdings, and 45 reduced their stakes. Institutions were also purchasing the stock, and aggregate holdings increased by about 3.4% to approximately 830.4 million from 803.2 million. As a result, the stock was added to the WhaleIndex 100 on August 17, 2021.

{kind=link}

Positive Multi-year Figures

Analysts expect to see earnings rise in 2021 and 2022 to an estimated $0.35 per share and $0.79 per share, respectively. Revenue estimates are also encouraging, predicting approximately $4.2 billion for December 2021 and rising to about $6.2 billion by December 2022. The 13F metrics between 2016 and 2021 are a good reflection of Snap’s ascending stock price and demonstrate the potential for the stock to continue on an upward trend, and institutional investors build longer-term positions.

{kind=link}

Analysts Raise Price Targets

Snap’s shares are setting new records for the company, and analysts have taken notice. Brent Thill of Jefferies Group LLC was impressed by the recent performance and raised their price target on Snap to $90 from $81. Barclays Investment Bank raised its price target on the stock to $81 from $75. Also, Piper Sandler Companies noted that revenue was better than anticipated. Analyst Thomas Champion reiterated an Overweight rating and $85 price target on the stock.

Positive Outlook

Snap’s amazing growth is no camera trick or tweaked reality. Hedge fund activity is an encouraging sign for investors. While Snap has its fair share of competition from tech companies and social media platforms, it has been able to innovate, stay relevant, and leverage advertising demand. Second-quarter results impressed, and earnings estimates through to 2022 provide a positive outlook.

Categorías: Blogs y opiniones de economia en ingles

L’Oréal stock analysis | When to buy the stock?

Check my L'Oréal stock analysis. We all know their brand, but is it really an excellent business? And what about their stock? When should we buy it?

The post L’Oréal stock analysis | When to buy the stock? appeared first on European Dividend Growth Investor.

Categorías: Blogs y opiniones de economia en ingles

This Week in Women

How one ETF up nearly 20% this year promotes female empowerment

“I hate to use the word ‘guarantee,’ but we certainly provide some assurance that … the over 200 companies that are involved in the ETF are doing the right thing to empower women,” Herrera said. “As we know, companies that have a focus this intently on their workforce tend to be very well run.”

The Privilege To Turn Off (Joelle Boneparth)

I ...

The post This Week in Women appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

Machiavelli For Women

On this special episode of This Week in Women LIVE, I spoke to Stacey Vanek Smith (yes, the one from NPR’s The Indicator!) about her new book, Machiavelli For Women, which is out this week. Stacey has written the most practical book of advice for women seeking success in the workplace, and she does it using wisdom from Machiavelli’s The Prince.

Remember The Prince? “It is better to be feared than loved&#...

The post Machiavelli For Women appeared first on The Belle Curve.

Categorías: Blogs y opiniones de economia en ingles

Investing Insights: Ed Slott Talks Taxes, IRAs, and More

Categorías: Blogs y opiniones de economia en ingles

Letters to the editor

A selection of correspondence

Categorías: Blogs y opiniones de economia en ingles

The Long View: Meb Faber - '‘To Be a Good Investor, You Have to Be a Good Loser’

Categorías: Blogs y opiniones de economia en ingles

Exorbitant Ignorance

Many Americans have been brainwashed to believe they have inherited the mantle of greatness passed down from prior generations. What they have actually inherited is the bill...

Those pundits who analyze the U.S. dollar reserve currency usually do so in the financial sense vis-a-vis the capital account. They happily ignore the long-term impact of an economy increasingly reliant upon foreign imports. They extol the fact that the dollar reserve currency allows the U.S. to import both capital AND goods from around the world on a seemingly unlimited basis. Vendor financing on a global scale. This has allowed the U.S. the "exorbitant privilege" of ignoring its ever-widening twin deficits - fiscal and trade.

Which is why it's no surprise the U.S. invented the concept of "Free Trade". No other major trading country - Japan, China, Germany believes in such a thing. Unlike the U.S. they are all trade mercantilists which believe as the British did hundreds of years ago:

"The Balance of Foreign Trade is the Rule of Our Treasure"

Historically those countries that rested on their laurels and relied upon their currency reserves to fund their standard of living soon found their currency reserves depleted. Mercantilist nations running trade surpluses happily relieved them of their burden. The most common example being Spain during its reign of empire. Of course in the age of fiat currencies and unlimited debt monetization, the price to be paid is not in gold reserves. The price is one that has been ignored for the past four decades - industrial capacity, intellectual property, scientific and engineering capability. A transition from a high productivity manufacturing economy to a low productivity services economy.

Voila.

The silver lining in this rapid descent into Third World penury is the fact that China now needs the U.S. trade deficit as much as the U.S. does. China can ill afford to have its factories idled and its population mass unemployed, so instead they continue to accept the seemingly worthless dollar in exchange for their exports.

So does living off the largesse of all prior generations still confer greatness? Today's morons clearly believe it does. History won't be as kind.

My wife and I both in our early 50s discuss what will happen to Social Security long-term. What most people don't know is that the program is already in the red. The so-called Social Security "trust fund" is a fictional entity that contains worthless IOUs from the Federal government to the Social Security fund. Each IOU from the government that must now be cashed in to pay retirees represents Treasury issuance on the open market. The Social Security "surplus" that existed for the past several decades during peak Boomer employment was squandered on successive rounds of tax cuts for the ultra wealthy. The Social Security surplus was "borrowed" by the Federal government in order to pretend the tax cut driven deficit was much smaller than it really was. Complicit economists merely claimed it was money we borrowed from ourselves which is why they excluded it from the "public deficit". However, now that Social Security proceeds are LESS than the payouts, it turns out that this private deficit is money we need to now borrow from others because we don't bring in enough taxes to borrow from ourselves anymore. Which means that if you are someone over a certain age who is soon to be reliant on Social Security, then you have to pray that we are now Japan and locked in a state of permanent deflation.

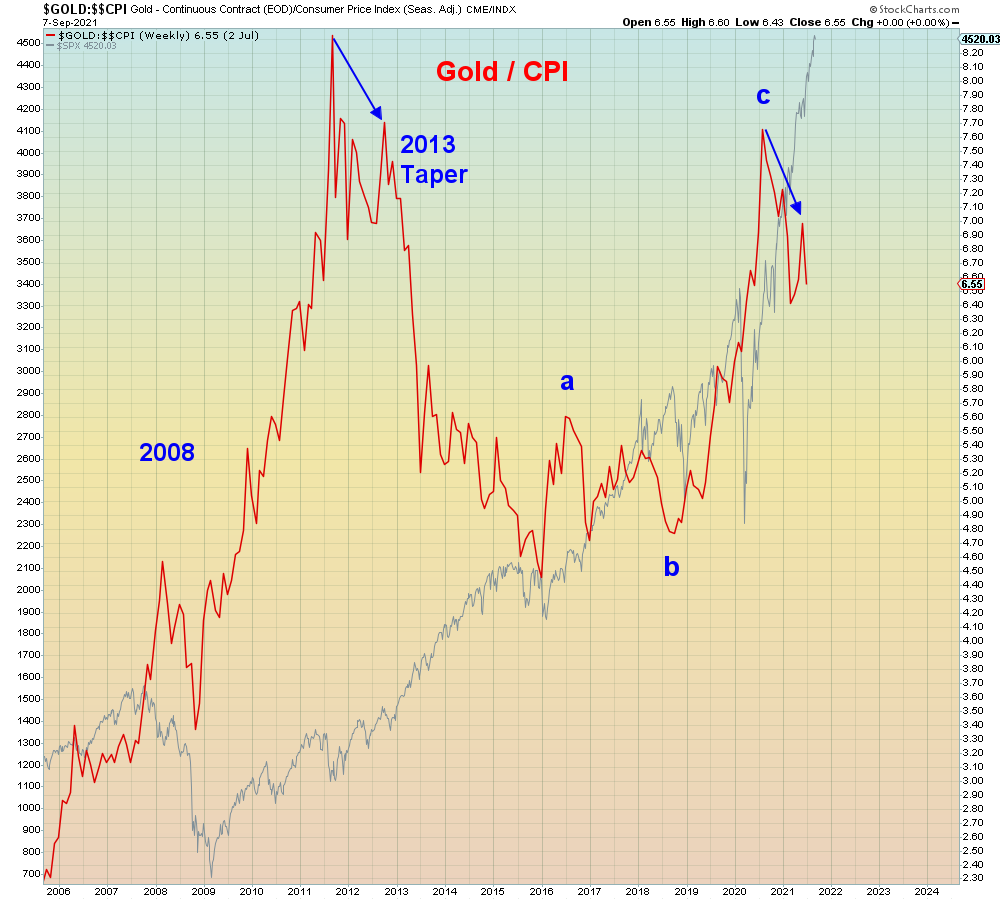

If not, you must allocate a certain portion of your wealth to gold to protect against inevitable inflation. Don't fall for this bullshit that Bitcoins are the new gold. Having a certain allocation to gold in a portfolio will likely prove more valuable than stocks in the long-term.

Gold has outperformed stocks for the past twenty years:

Nevertheless, when you put it all together, one realizes that the outsourcing of the economy has essentially ensured a deflationary outcome. As the U.S. fiscal deficit grows, the trade deficit grows in direct correlation. The U.S. is importing deflation from Asia. Which is why Biden's stimulus will have no long-term inflationary effect. The money is heading straight back to China where it originated.

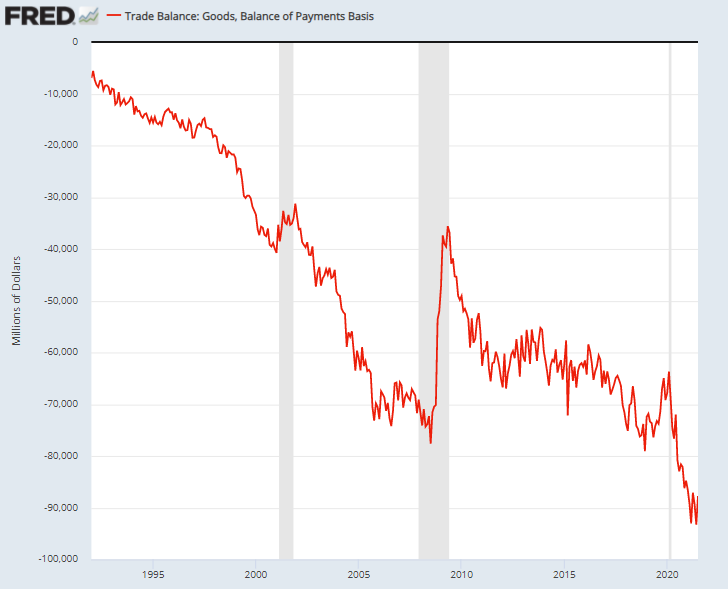

The balance of trade is record wide in 2021:

In addition, at the peak of the largest asset and credit bubble in human history, owning any risk asset at this juncture is a dangerous proposition. There will be plenty of gold and stocks puked back onto the market during the global margin call.

Gold is warning us that inflation is a hoax. Those who don't heed that warning will soon realize that they were only renting exorbitant ignorance all along.

{kind=link}

Those pundits who analyze the U.S. dollar reserve currency usually do so in the financial sense vis-a-vis the capital account. They happily ignore the long-term impact of an economy increasingly reliant upon foreign imports. They extol the fact that the dollar reserve currency allows the U.S. to import both capital AND goods from around the world on a seemingly unlimited basis. Vendor financing on a global scale. This has allowed the U.S. the "exorbitant privilege" of ignoring its ever-widening twin deficits - fiscal and trade.

Which is why it's no surprise the U.S. invented the concept of "Free Trade". No other major trading country - Japan, China, Germany believes in such a thing. Unlike the U.S. they are all trade mercantilists which believe as the British did hundreds of years ago:

"The Balance of Foreign Trade is the Rule of Our Treasure"

Historically those countries that rested on their laurels and relied upon their currency reserves to fund their standard of living soon found their currency reserves depleted. Mercantilist nations running trade surpluses happily relieved them of their burden. The most common example being Spain during its reign of empire. Of course in the age of fiat currencies and unlimited debt monetization, the price to be paid is not in gold reserves. The price is one that has been ignored for the past four decades - industrial capacity, intellectual property, scientific and engineering capability. A transition from a high productivity manufacturing economy to a low productivity services economy.

Voila.

The silver lining in this rapid descent into Third World penury is the fact that China now needs the U.S. trade deficit as much as the U.S. does. China can ill afford to have its factories idled and its population mass unemployed, so instead they continue to accept the seemingly worthless dollar in exchange for their exports.

So does living off the largesse of all prior generations still confer greatness? Today's morons clearly believe it does. History won't be as kind.

My wife and I both in our early 50s discuss what will happen to Social Security long-term. What most people don't know is that the program is already in the red. The so-called Social Security "trust fund" is a fictional entity that contains worthless IOUs from the Federal government to the Social Security fund. Each IOU from the government that must now be cashed in to pay retirees represents Treasury issuance on the open market. The Social Security "surplus" that existed for the past several decades during peak Boomer employment was squandered on successive rounds of tax cuts for the ultra wealthy. The Social Security surplus was "borrowed" by the Federal government in order to pretend the tax cut driven deficit was much smaller than it really was. Complicit economists merely claimed it was money we borrowed from ourselves which is why they excluded it from the "public deficit". However, now that Social Security proceeds are LESS than the payouts, it turns out that this private deficit is money we need to now borrow from others because we don't bring in enough taxes to borrow from ourselves anymore. Which means that if you are someone over a certain age who is soon to be reliant on Social Security, then you have to pray that we are now Japan and locked in a state of permanent deflation.

If not, you must allocate a certain portion of your wealth to gold to protect against inevitable inflation. Don't fall for this bullshit that Bitcoins are the new gold. Having a certain allocation to gold in a portfolio will likely prove more valuable than stocks in the long-term.

Gold has outperformed stocks for the past twenty years:

{kind=link}

Nevertheless, when you put it all together, one realizes that the outsourcing of the economy has essentially ensured a deflationary outcome. As the U.S. fiscal deficit grows, the trade deficit grows in direct correlation. The U.S. is importing deflation from Asia. Which is why Biden's stimulus will have no long-term inflationary effect. The money is heading straight back to China where it originated.

The balance of trade is record wide in 2021:

{kind=link}

In addition, at the peak of the largest asset and credit bubble in human history, owning any risk asset at this juncture is a dangerous proposition. There will be plenty of gold and stocks puked back onto the market during the global margin call.

Gold is warning us that inflation is a hoax. Those who don't heed that warning will soon realize that they were only renting exorbitant ignorance all along.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

Uber’s Stock Stalls Despite Falling In Favor Among Hedge Funds

Uber Technologies, Inc. (UBER) has been on a rocky path over the past year and a half, and the gains realized over the past six months appear to have stalled. The ride-sharing company’s stock has recently fallen, bringing it into alignment with the S&P 500. Uber rose by approximately 40.4% as of late August 2021 compared to the S&P 500’s gain of roughly 39.2% since the start of 2020.

Uber faced its share of challenges throughout the coronavirus pandemic due to government-imposed travel restrictions. However, despite the negative impacts of the pandemic, Uber recently ascended in the second quarter to a rank of 10 on the WhaleWisdom Heatmap.

{kind=link}

Hedge Funds Are Active

Uber received positive attention from hedge funds, which increased their aggregate 13F shares held to approximately 522.0 million from about 514.5 million in the second quarter, representing an increase of roughly 1.5%. Of hedge funds, 51 created new positions, 123 added to an existing one, 51 exited, and 80 reduced their stakes. In contrast to hedge funds, institutions decreased their aggregate holdings slightly by about 1.0% to approximately 1.37 billion. The 13F metrics from 2019 through 2021 suggest that Uber’s investment potential remains steady, despite ups and downs.

{kind=link}

{kind=link}

Encouraging Revenue Estimates

Analysts appear optimistic with their revenue estimates, though earnings estimates are less rosy. It is anticipated that year-over-year revenue growth may range from approximately 44.5% to 25.9% between 2021 and 2023, which could bring revenue to about $28.4 billion by December 2023, up from an estimated $16.1 billion in December 2021. Earnings per share will initially decline in 2021 and 2022 before extraordinary year-over-year growth of 723.3% is predicted for 2023, bringing earnings to $0.43.

Mixed Reactions After Disappointing Second Quarter

Many analysts lowered price targets amid disappointing second-quarter results. Doug Anmuth from JP Morgan & Co. kept an Overweight rating on the stock and lowered the firm’s price target to $72 from $74. Anmuth believes that the recent selloff of shares creates an attractive long-term opportunity. Wedbush Securities analyst Ygal Arounian lowered the firm’s price target to $51 from $66, maintaining an Outperform rating on Uber shares. Oppenheimer & Co. analyst Jason Helfstein lowered their price target on Uber to $70 from $80 and kept an Outperform rating on shares, acknowledging Uber’s efforts to address driver supply challenges through driver incentives. However, Jefferies analyst Brent Thill is optimistic for better third and fourth quarter performance and kept a Buy rating and $75 price target on the stock following second-quarter results.

Optimism Beyond 2021

Customer demand for travel and meal delivery services remains in flux as the pandemic continues; however, it seems likely that the foundation of Uber’s business, ride-hailing, and ride-sharing, will ultimately see a rebound in demand. Increased coronavirus vaccination rates and the promise of boosters against variants will certainly help consumer mobility recover over time. Uber has taken strategic steps to strengthen its driver supply and incentivize its workforce in the interim. Uber may not be a buy for all investors, but it holds possibilities for investors seeking a long-term opportunity.

Categorías: Blogs y opiniones de economia en ingles

[Video] 3 High Yield Dividend Stocks with more than 7% dividend yield

3 high yield dividend stocks all yielding more than 7%. Check it out in my latest video. It includes my fair value estimates.

The post [Video] 3 High Yield Dividend Stocks with more than 7% dividend yield appeared first on European Dividend Growth Investor.

Categorías: Blogs y opiniones de economia en ingles

Letters to the editor

A selection of correspondence

Categorías: Blogs y opiniones de economia en ingles

Investing Insights: Struggling Funds and Stretch IRA Updates

Categorías: Blogs y opiniones de economia en ingles

A 100 Year Storm

As we're witnessing in real-time, reality doesn't give a damn what today's denialists "believe". They're being hunted into extinction and they want no warning as to what's coming...

What went wrong? That's the question archaeologists will ask. It's a question that is assiduously avoided by today's de facto Idiocracy. This inherited belief in God given exceptionalism has made this society fat, dumb, and lazy. Denialist ignorance is the path of least resistance, bounding down the continual descent into squalor.

The 100 year storm flooded our basement this week so I spent the past several days fixing the damage and improving the drainage before Noah starts loading the animals onto the Ark for the next round. I am under no illusion that this was a "one time event". Half this country is currently under extreme drought and the other half is under water. Large tracts of housing are now blighted and permanently uninsurable. The square footage per person of U.S. homes doubled in the past fifty years while the population doubled as well. Third grade math indicates the unsustainability of this mass consumption orgy. You don't have to be a genius to figure out "what changed".

Afghanistan is another major example of never ending denialism. Biden should have never attempted to pull out of that country which collapsed like a cheap tent. Held up all these years only by a continuous flow of foreign aid and the permanent U.S. presence. What was he thinking? There was no upside to decisive action. Talk constantly and do nothing, that is the new American way. Now he is receiving the full wrath of two decades of collapsed hubris. He made all of today's "experts" look like the idiots they've been all along. His presidency blighted by honesty.

Which gets me to this ongoing COVID debacle which is being managed in the worst way possible. Half the country that is vaccinated is in a constant state of hysteria over the virus. The other half of the country is unvaccinated and pretending the virus doesn't exist. One side is racing into the virtual reality of the future and the other side is clinging to the blighted past.

One wonders, would so many of these yuppies be enthralled by night after night of COVID hysteria on CNN if it wasn't conducive to a permanent work from home situation? As we got closer to the end of the summer and the dreaded return to the office, back came the masks and the calls for "responsibility". Make no mistake, this is a yuppy paradise - untold numbers of marginally attached gig workers are now attending their every whim while they get rich in the markets sitting at home. We don't need arrays of tall downtown skyscrapers anymore, the iPhone is the new office.

To date, the 100 year storm has yet to reach the placid shores of these central bank managed Disney markets, but it's only a matter of time before the cars are floating down Wall Street as well.

Going into the Labor Day long weekend, the Nasdaq is six months overbought (lower pane), and the beloved virtual economy is tracing out an identical pattern to the February top:

Cyclicals are getting monkey hammered this week, while positioning (lower pane) remains at extremes. JP Morgan put out a note this week saying that retail investor inflows remain at a record high in August.

Chinese stocks have enjoyed a nice bounce, but now we learn that the most leveraged company on the planet is on the verge of default. Investors are assuming the Chinese government will organize a bailout, but given the theme of "Common Prosperity", it's far from a sure bet.

It appears that unlike the U.S. where inequality is the new beloved business model, the Chinese are getting serious about the problem.

"Common prosperity" as an idea is not new in China, but a sharp escalation in official rhetoric and a crackdown on excesses in industries including technology and private tuition has rattled investors in the world's second-largest economy"

Does common prosperity include bailouts for the rich? If it doesn't, then inequality is going to get fixed sooner rather than later.

Ironically, due to the implosion of the real estate sector, Chinese speculators are now speculating in stocks at volumes not seen since the crash of 2015.

"On Wednesday, trading volume in the Shanghai composite was the highest since July 2015, the summer China’s stock market crashed amid high speculation."

Markets should be prepared for what could be a much worse-than-expected growth slowdown, more loan and bond defaults, and potential stock market turmoil"

Or not.

Conversely, the U.S. approach to fixing inequality is to continue to dump insane amount of junk stocks into an extreme overbought market, thus allowing insiders to cash out at public expense.

"The IPO market has already had its busiest year since the internet bubble in 2000"

"After-market performance (the performance after the first day of trading) for IPOs was negative for most of this year. An investor who put money into an IPO after the first day of trading, on average, lost money"

In summary, the question on the table is will human history's biggest pump and dump continue into this Fall and therefore keep the yuppy dream alive?

Or will inconvenient reality burst their bubble?

My prediction is that the inequality reduction will begin overnight in a widely ignored time zone.

{kind=link}

What went wrong? That's the question archaeologists will ask. It's a question that is assiduously avoided by today's de facto Idiocracy. This inherited belief in God given exceptionalism has made this society fat, dumb, and lazy. Denialist ignorance is the path of least resistance, bounding down the continual descent into squalor.

The 100 year storm flooded our basement this week so I spent the past several days fixing the damage and improving the drainage before Noah starts loading the animals onto the Ark for the next round. I am under no illusion that this was a "one time event". Half this country is currently under extreme drought and the other half is under water. Large tracts of housing are now blighted and permanently uninsurable. The square footage per person of U.S. homes doubled in the past fifty years while the population doubled as well. Third grade math indicates the unsustainability of this mass consumption orgy. You don't have to be a genius to figure out "what changed".

Afghanistan is another major example of never ending denialism. Biden should have never attempted to pull out of that country which collapsed like a cheap tent. Held up all these years only by a continuous flow of foreign aid and the permanent U.S. presence. What was he thinking? There was no upside to decisive action. Talk constantly and do nothing, that is the new American way. Now he is receiving the full wrath of two decades of collapsed hubris. He made all of today's "experts" look like the idiots they've been all along. His presidency blighted by honesty.

Which gets me to this ongoing COVID debacle which is being managed in the worst way possible. Half the country that is vaccinated is in a constant state of hysteria over the virus. The other half of the country is unvaccinated and pretending the virus doesn't exist. One side is racing into the virtual reality of the future and the other side is clinging to the blighted past.

One wonders, would so many of these yuppies be enthralled by night after night of COVID hysteria on CNN if it wasn't conducive to a permanent work from home situation? As we got closer to the end of the summer and the dreaded return to the office, back came the masks and the calls for "responsibility". Make no mistake, this is a yuppy paradise - untold numbers of marginally attached gig workers are now attending their every whim while they get rich in the markets sitting at home. We don't need arrays of tall downtown skyscrapers anymore, the iPhone is the new office.

To date, the 100 year storm has yet to reach the placid shores of these central bank managed Disney markets, but it's only a matter of time before the cars are floating down Wall Street as well.

Going into the Labor Day long weekend, the Nasdaq is six months overbought (lower pane), and the beloved virtual economy is tracing out an identical pattern to the February top:

{kind=link}

Cyclicals are getting monkey hammered this week, while positioning (lower pane) remains at extremes. JP Morgan put out a note this week saying that retail investor inflows remain at a record high in August.

{kind=link}

Chinese stocks have enjoyed a nice bounce, but now we learn that the most leveraged company on the planet is on the verge of default. Investors are assuming the Chinese government will organize a bailout, but given the theme of "Common Prosperity", it's far from a sure bet.

It appears that unlike the U.S. where inequality is the new beloved business model, the Chinese are getting serious about the problem.

"Common prosperity" as an idea is not new in China, but a sharp escalation in official rhetoric and a crackdown on excesses in industries including technology and private tuition has rattled investors in the world's second-largest economy"

Does common prosperity include bailouts for the rich? If it doesn't, then inequality is going to get fixed sooner rather than later.

Ironically, due to the implosion of the real estate sector, Chinese speculators are now speculating in stocks at volumes not seen since the crash of 2015.

"On Wednesday, trading volume in the Shanghai composite was the highest since July 2015, the summer China’s stock market crashed amid high speculation."

Markets should be prepared for what could be a much worse-than-expected growth slowdown, more loan and bond defaults, and potential stock market turmoil"

Or not.

{kind=link}

Conversely, the U.S. approach to fixing inequality is to continue to dump insane amount of junk stocks into an extreme overbought market, thus allowing insiders to cash out at public expense.

"The IPO market has already had its busiest year since the internet bubble in 2000"

"After-market performance (the performance after the first day of trading) for IPOs was negative for most of this year. An investor who put money into an IPO after the first day of trading, on average, lost money"

{kind=link}

In summary, the question on the table is will human history's biggest pump and dump continue into this Fall and therefore keep the yuppy dream alive?

Or will inconvenient reality burst their bubble?

My prediction is that the inequality reduction will begin overnight in a widely ignored time zone.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

How I’m Thinking About the Shiller P/E

The Shiller P/E (or CAPE ratio) since 1881

A Maddening Ratio

The Shiller P/E (or CAPE) is a measure of market valuations developed by Nobel-prize winner Robert Shiller. It smooths out earnings over 10 years (because earnings are extraordinarily volatile in the short run) and then compares them to market prices. You can check out the data for free, right here.

The Shiller P/E is a metric that has long maddened me. This is because I used it wrong. I thought that the Shiller P/E could be used as a tool to predict the market and that’s not really what it does.

I’ve long looked at it in the context of ‘the bigger they are, the harder they fall.’ I thought that the Shiller P/E could be used as a prediction tool. That’s not really how it works.

My History With the Ratio

As a teen in the ’90s, I was a bulled-up internet bubble believer who was lucky enough to come across ‘The Intelligent Investor’ in the summer of 2000. I looked at the prices, thought they were crazy in the context of Ben Graham, and then I got out.

Of course, Ben Graham was new to me at the time. I never fully appreciated the frustration of people who used a price-to-multiple approach through the 1990’s.

CAPE became expensive in historical terms in the early 1990’s. Someone using that approach would have been maddened by the insanity that happened for the rest of the decade. Someone using that classic approach missed out on most of the ’90s bull market.

I simply was lucky enough to discover value investing at exactly the right time. My timing gave me a flawed sense of confidence in predicting markets.

Throughout the 2010’s, I looked at a rising CAPE ratio and assumed this was all going to crash, eventually. I’d tell people I didn’t know for sure – but I didn’t really believe that in my bones.

Of course, I didn’t think this would happen on its own. My theory was that a catalyst was necessary to make CAPE crash. Historically, the catalyst is typically a recession.

I thought you could predict recessions with the yield curve, which is a reliable indicator. Once a frothy market like the US runs into a recession, the CAPE ratio will mean revert.

When COVID came along, I thought this was the ticket. This was the catalyst that was going to make the Shiller PE mean revert.

As anyone who follows this blog knows, that didn’t happen. CAPE only got down to 24x. This is hardly ‘cheap’ in any historical context. I figured – at the very least – it would get down to 15x. That was around the low reached in 2009.

(Interestingly, the 2009 low wasn’t even particularly ‘cheap,’ either. The average CAPE ratio since 1881 has been 17.)

The Trouble With Historical Multiples

Since 1881, CAPE has gyrated between a low of 4.78 (1920) and the high of 44.2 (1999).

More recently, in 1980, it reached a low of 8.1. This was mainly because interest rates were at all-time-highs in the context of thousands of years of human history.

Looking at a historical chart, timing the market with CAPE looks easy. Sell when you’re at all-time highs in 2000. Buy when in the single-digits in the early 1980’s. Smoke a fat cigar and laugh at the idiots who bought at the highs and didn’t recognize the opportunity at the lows.

Unfortunately, as I have discovered the hard way, that’s not how the real world actually works.

When is it at the high? When is the low? There is no one who can tell you when that is. Alan Greenspan talked about ‘irrational exuberance’ in 1996. That looked like the top to a lot of people and it was not. The market looked cheap compared to the ’90s and 2000’s in the summer of 2008, but it had much further to fall.

The average throughout history is 17. Since 1995, the US market has only spent 3.2% of the time below 17. Imagine if you only invested in stocks when they were below the average.

Literally, the only time you would have invested since ’95 is 3% of the time. Meanwhile, since ’95, the US stock market has turned $10,000 into $162,188.

At this point, if you’ve been bearish since ’95, the market needs to fall 95% for you to be vindicated. That’s probably not going to happen. (Insert long perma bear rant about the Fed and how everything is doomed and it’s all a big Ponzi scheme house of cards.)

If it does fall 95%, I guarantee you that something so horrific is happening in the world that the size of your portfolio probably doesn’t matter much and we are likely entering a Mad Max style hellscape. Stock up on your ammo.

The Long Term is Longer Than You Think

The S&P 500 has historically grown earnings at about a 6% clip. Let’s say it does that for the next decade. We’ll get a 6% return plus dividends, right?

The actual growth isn’t the full story, though. What multiple will investors be willing to pay for those earnings?

That, my friend, is key and it is totally and completely unpredictable.

Let’s say that it gets down to 22 by 2031. The 6% growth should have resulted in 79% growth.

Unfortunately, the mean reversion of the multiple created a lost decade for US stocks even while the fundamentals grew.

What will the 2031 multiple be? It’s impossible to say. It could stay 40 and we’ll actually earn the growth rate of the companies within the index. If we have a Japan moment, it could go up to 100. It could crash down to 10, again. It’s all totally unpredictable.

The multiple 10 years from now depends on what inflation, growth, and interest rates will be. It will depend on the quality of the companies within the index. If they’re growing fast and have fat margins, a higher multiple can be justified. It’s also possible that the quality of companies deteriorates over the next 10 years. No one knows what is going to happen.

When viewed through the context of the total unpredictability of all of these factors, it’s clear that it’s virtually impossible to predict returns 10 years out, let alone 1 year out or 6 months from now.

I mentioned earlier that the S&P 500 has historically grown earnings at a 6% clip. I think an investor with a truly long time horizon (40 years, for instance) is likely to capture that growth plus dividends.

Everyone likes to say that they have these time horizons, but I don’t believe them. I think most people think of ‘long term’ as 5 or 10 years, but the investment outcomes over those time horizons are totally unpredictable.

The crazy fact is that 10 years is short term in the context of market history.

How I Learned To Stop Worrying and Trust the Weird Portfolio

This realization – that the future is totally unpredictable – has made me gravitate towards an asset allocation that ought to be able to deliver a return across a 10-year time horizon regardless of what happens to the macro-economy. For me, the solution was the weird portfolio.

I’m naturally a pessimist. I try to be optimistic, but I can’t help myself. I listen to someone like Peter Schiff and my natural inclination is to hoard gold bars and ammo. I listen to an optimist like Cathie Wood and my natural inclination is to scoff and assume she has her head in the clouds. Of course, Cathie Wood’s philosophy has worked out a lot better than Peter Schiff’s in the last decade. Which philosophy will win out over the next? I have no idea.

That’s why a conservative asset allocation was so useful for me. Are we going to have a deflationary bust? Alright, I own some long term treasuries. Are we going to have hyperinflation and USD collapse? Well, I have some gold and real estate. Is the multiple going to mean revert slowly over the next decade without ending the world? Well, my stock exposure is tilted to small cap value, which should be somewhat insulated from that mean reversion.

Investing in a diversified approach has helped me to stop worrying about the Shiller PE and our impending doom. Instead, I can methodically save & invest for my future.

I’m glad that I developed this approach before COVID. I kept most of my money in that approach. When COVID hit, I acted correctly with the money that I had invested in the weird portfolio.

For the account that I track on this blog, I expressed my opinions about what the market would do.

My opinion wasn’t worth much. The Shiller PE wasn’t worth much as an analysis tool during that time.

I feel fortunate to have discovered an asset allocation that I’m comfortable with that helped me stop worrying about the Shiller PE.

What works for you? That’s really a question you have to answer for yourself. Are you an optimist? Are you a pessimist? What are your goals? How far out are they?

While I don’t know the right asset allocation for everyone, I have concluded that using CAPE as a market timing tool is a flawed concept. Hopefully people can learn this lesson on my dime.

You will not time the market correctly and smoke a fat cigar while laughing at the idiots, I assure you.

Or – maybe you can, in which case, enjoy the smoky Cuban goodness – but that’s probably not gonna happen.

Random

PLEASE NOTE: The information provided on this site is not financial advice and it is for informational and discussion purposes only. Do your own homework. Read the full disclaimer.

Categorías: Blogs y opiniones de economia en ingles

Páginas

Custom Search