Se encuentra usted aquí

Agregador de canales de noticias

Episode #337: Professor Richard Thaler, University of Chicago, “When Somebody Would Fire Us, It Was Almost Always At Exactly The Wrong Time”

Episode #337: Professor Richard Thaler, University of Chicago, “When Somebody Would Fire Us, It Was Almost Always At Exactly The Wrong Time” Guest: Richard Thaler is the Charles R. Walgreen Distinguished Service Professor of Behavioral Science and Economics at the University of Chicago Booth School. Thaler is […]

The post Episode #337: Professor Richard Thaler, University of Chicago, “When Somebody Would Fire Us, It Was Almost Always At Exactly The Wrong Time” appeared first on Meb Faber Research - Stock Market and Investing Blog.

Categorías: Blogs y opiniones de economia en ingles

Cuchillos para talla de madera. "Carving knife".

Hace tiempo descubrí que una de las cosas que más me relaja es coger un "cacho" palo y mi Mora Carving, echar camino alante y sacar viruta para acabar en el chiringuito junto al rio, echando una cañita mientras continúo con mi faena. Sobre todo cucharas o tenedores....me resulta relativamente fácil y son resultones....

.....consciente de mi "ansia viva" por los filos porque no intentar hacerme unos cuchillines de talla jajajaja. Pues ni uno ni dos .....seis salieron.....y ahi van.

Las hojas salieron de unos discos de corte y tras hacer el primero a modo de prueba templando y reviniendo.... funcionó.

Tras el REVENIDO sesión de codo y lija....(pendiente dejo mostraros lo que salió de esa vieja lima de Bellota)

toca elegir la madera para los cabos

v

Un buen tarillo de lija y a dar forma....

un poco de magia jjjjjj

para los cabos madera de Roble Americano y Fresno y para las virolas de izquierda a derecha Cocobolo, Granadillo , Palo violeta y Granadillo

Muchaaaaaasss fotossss.....

No van mal y cumplen su función . Ahora tendré el dilema de cual llevar jajajjaja.

UN cordial SALUDO y muchas gracias por llegar hasta aquí

Categorías: Metalurgia, forja y fundicion

A Manic Reach For Explosion

We are now learning that the sole purpose of Monetary policy is to stimulate greed in an ultra greedy society. Central banks are keeping the spigots wide open to support the economy which is driving greed-addled gamblers to buy record inequality...

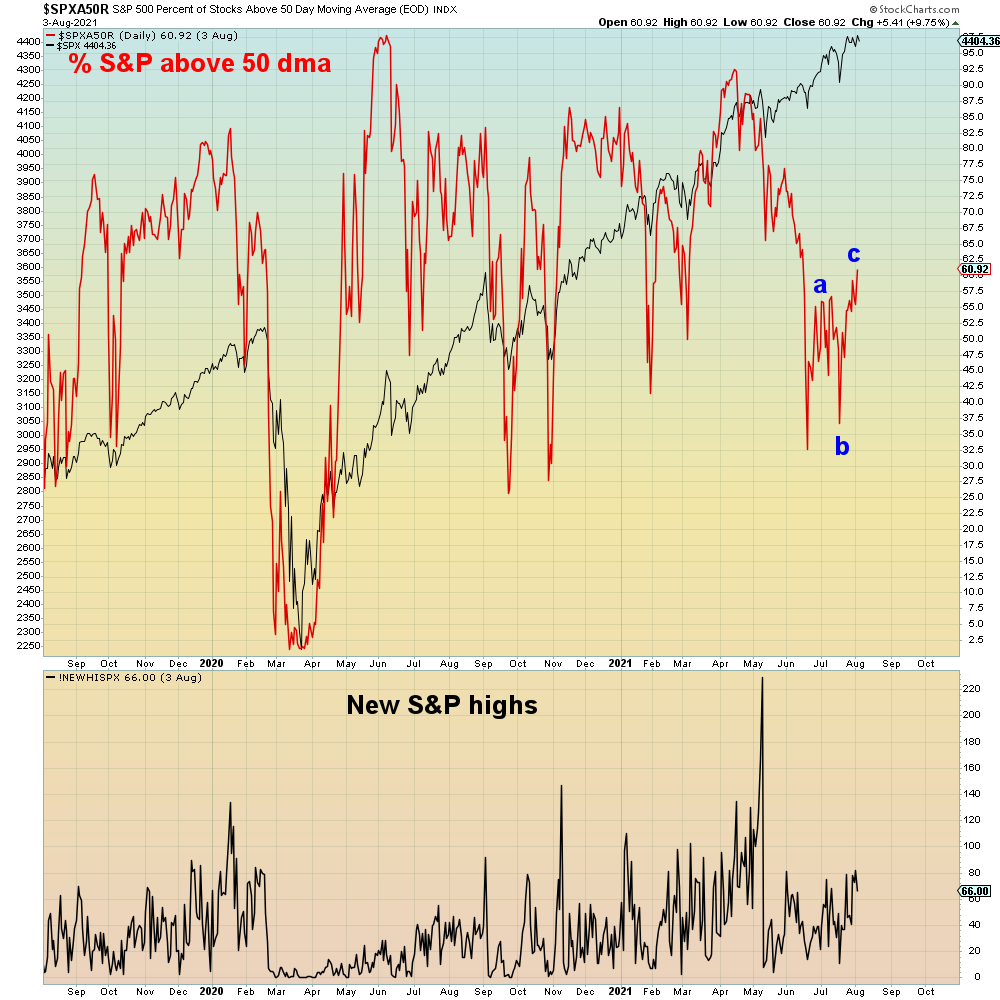

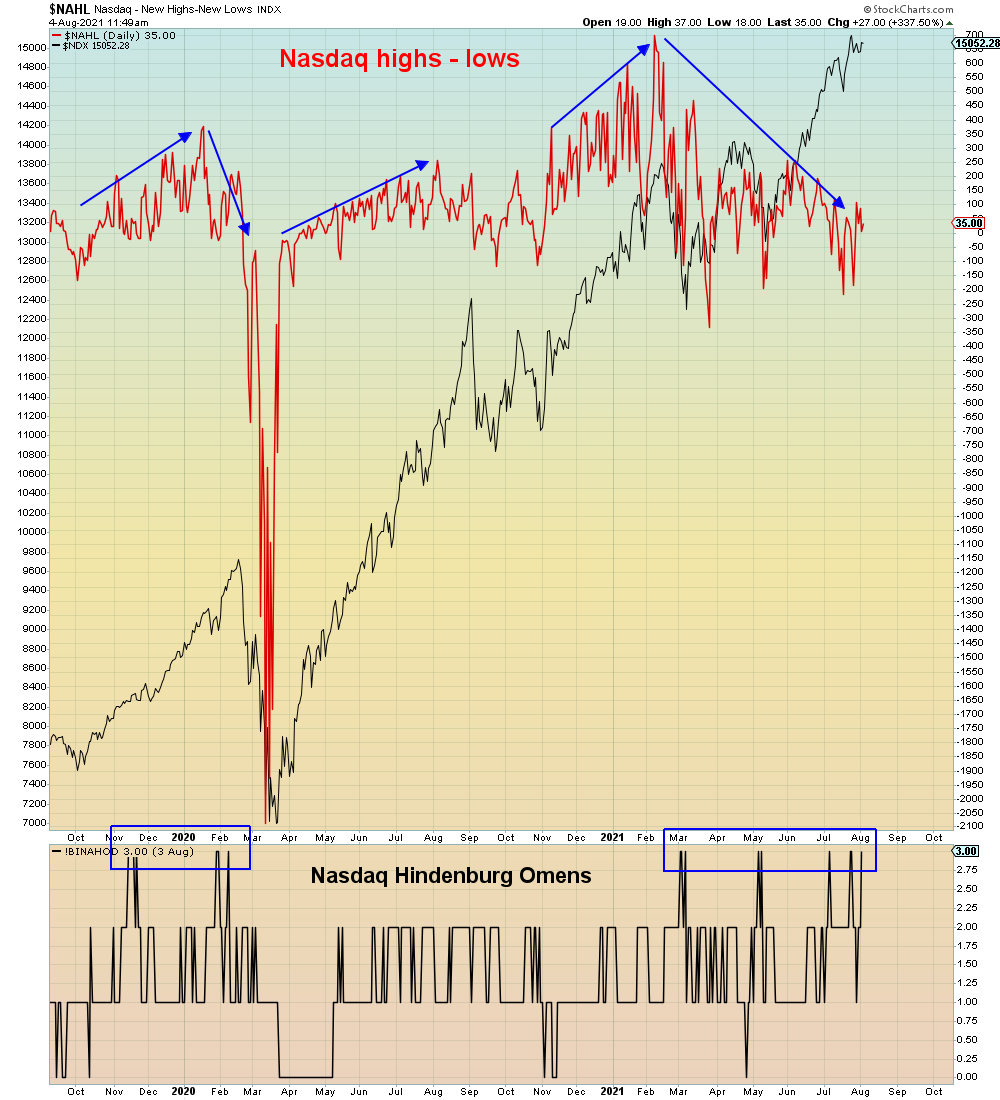

Another Nasdaq Hindenburg Omen yesterday - the third in less than two weeks, indicative of a bifurcated market disintegrating in real-time:

{kind=link}

This greed-addled society has long since forgotten how this movie ended the last two times. The COVID ultra bubble makes the Dotcom bubble and Housing bubbles seem minor by comparison. COVID exposed Globalization's economic frailties which are now sending markets and the economy in opposite directions. Central banks are keeping the spigots wide open ostensibly to help the economy, but the only effect is driving economic inequality to ludicrous levels. Yesterday we learned that household debt is exploding at the fastest pace since the 2007 top. Too many people forget that debt follows asset prices higher, BUT not lower. When assets crash they turn into liabilities. Debt is deflationary. Underwater debt is lethal.

Trolls and other low life criminals now abound, exhorting everyone to engage in maximum Ponzi. The greed-fueled inflation thesis jumped the shark from risk asset markets to the economy and back again. No fool should be left behind. The concept of financial and economic responsibility is an abandoned relic of a bygone era. Deemed to be of no value in the golden age of printed money.

Unfortunately, nothing could be further from the truth. As Japan and China have already learned the hard way, all of this central bank driven speculation brutally turns back into a deflated pumpkin overnight.

As the economic data continues to weaken, gamblers are attempting a last ditch rotation back to Tech stocks which are approaching another melt-up high. This time amid chasmic breadth divergences.

Here we see breadth attending this latest all time high:

{kind=link}

Yesterday another Hindenburg Omen on the Nasdaq (lower pane):

{kind=link}

Semis are leading this latest Tech melt-up. The Rydex ratio (lower pane) keeps making new highs indicating a manic reach for risk:

{kind=link}

This is all very reminiscent of August 2015 when Chinese authorities used monetary policy to inflate the stock market in the face of an imploding economy. Shockingly, it didn't work. It was the end of imagined realities.

Guess whose turn it is this time.

{kind=link}

Categorías: Blogs y opiniones de economia en ingles

EEUU: crea 330.000 empleos en el sector privado en julio

Según datos de la entidad Automatic Data Processing, el sector privado estadounidense creó 330.000 empleos en el mes de julio sobre el mes de junio. Aunque la cifra en términos históricos es un gran número, el resultado final ha sido de menos de la mitad de lo esperado por el mercado.

Las principales creadoras de empleo fueron las empresas medianas, que añadieron 132.000 empleos, seguidas de las grandes, que sumaron 106.000 empleos y las pequeñas empresas que lograron añadir 91.000 empleos.

Todos los sectores crearon empleo a excepción del de las tecnologías de la información, que destruyó empleo (-1.000).

Categorías: Blogs y opiniones de economia en español

The Long View: Martin Lau - Now Is a Better Time to Buy China

Categorías: Blogs y opiniones de economia en ingles

Wells Fargo espera que el Banco Central Europeo mantenga sus políticas actuales

El máximo ente emisor del euro, el Banco Central Europeo, ha mantenido una política monetaria acomodaticia, en la que se imprimen mayores cantidades de dinero para compensar la falta de liquidez producida por el Covid-19 en el último año. La lógica indicaría que este tipo de políticas incrementarían los niveles de inflación e iniciaría un proceso de devaluación del euro frente a otras monedas internacionales.

Sin embargo, lo que se ha visto es prácticamente lo contrario, según Wells Fargo, se ha observado un rendimiento mucho mejor durante el segundo trimestre de 2021, lo cual indica que el BCE puede continuar con las políticas acomodaticias y, de no observarse una tendencia alcista en la inflación, el ente podría ampliar el programa de compra de bonos de deuda que ha venido manteniendo durante 2020 y la primera mitad de 2021. Al parecer, el mercado de Forex se ha visto favorecido por estas políticas, en especial por quienes apuestan por el índice euro por encima de monedas que sí han mostrado debilidad, como el propio dólar americano, cuyo valor decreció con respecto al euro durante gran parte de 2020 y no mejoró con los resultados electorales de diciembre.

¿Han sido exitosas las políticas acomodaticias del BCE?En primera instancia, podría decirse que sí, ya que, al combinar la compra de bonos de deuda con la emisión de dinero orgánico, el Banco ha logrado incrementar la liquidez sin impactar negativamente en los indicadores económicos como la inflación. Además, el incremento del comercio con la reapertura de las economías europeas y la competencia internacional del euro frente a otras monedas han favorecido el valor de las mismas.

El único factor que podría llegar a modificar a mediano plazo las decisiones del BCE en cuanto a sus políticas monetarias, es la propia Covid-19 y el impacto que la enfermedad pueda llegar a tener en los mercados y en las tasas de inflación. Si se logra una tasa más regular del proceso de inmunizaciones, reduciendo así las muertes a un mínimo histórico a finales del año, haciendo que sean innecesarias nuevas políticas de aislamiento, el BCE podría ampliar su programa de compra de bonos y mantener las políticas monetarias que se han venido llevando a cabo, de lo contrario, si la inflación llegará a mostrar signos de alza, las políticas monetarias tendrían que replantearse.

Las predicciones de Wells FargoEn primer lugar, Wells Fargo ha declarado que esperan que el BCE no reduzca sus políticas de compra de bonos a través de PEPP intentando mantener un valor simétrico de inflación del 2%, con esto en mente, se espera que para finales de año, dependiendo, como hemos mencionado, de que la inflación se vuelva o no alcista, se espera que el BCE invierta alrededor de 500.000 millones de euros en bonos de deuda a través del PEPP, lo cual incrementa el valor del programa a unos 2350 billones de euros.

Por otro lado, Wells Fargo también ha predicho que el programa de compra de bonos a través del PEPP continuarían, de todo salir como se tiene planeado, hasta septiembre del año 2022.

Categorías: Blogs y opiniones de economia en español

Animal Spirits: The Best Way to Get a Raise

Today’s Animal Spirits is brought to you by YCharts

Mention Animal Spirits to receive 20% off when you initially sign up for the service.

On today’s show we discuss:

Crony Capitalism

Clayton fights for Bitcoin ETF

The best way to get a raise

Might be time to change how we think about debt

Don’t obsess over money

Boz Angeles

How much money to feel financial secure?

Disney Vax

Wal-Mart too

Corporations setti...

The post Animal Spirits: The Best Way to Get a Raise appeared first on The Irrelevant Investor.

Categorías: Blogs y opiniones de economia en ingles

CBDC Part 2: The tradeoffs

Last week, I introduced the concept of retail Central Bank Digital Currencies (CBDC) and why central banks may want to issue them. In this part, I am going to look at the practical difficulties that CBDC must overcome. I will do this by looking at the three basic functions of cash, namely to act as a medium of exchange, a store of value, and a unit of accounting. Hopefully, by doing this, you will understand why it is so much harder to launch a CBDC than any run-of-the-mill cryptocurrency or electronic payment system and get an appreciation for what a genius invention physical cash really is.

Store of value vs. medium of exchange

When we think of physical cash, we immediately think of it as a store of value and a medium of exchange. Cash is worth the same tomorrow (at least nominally) as it is today, and I can readily buy things with it in a store.

The problem with CBDC is that they are electronic and the folks in Silicon Valley and big cities might not realise this, but there are a lot of people who cannot live without physical cash. In 2019 the Access to Cash Review concluded that 17% of the population in the UK need physical cash to live their lives. Having only electronic cash available to them would cause serious disruptions in their business or make it impossible for them to purchase the goods they need for daily life. And this is in one of the most developed countries in the world. Across the Euro Area (EA) and Japan, the use of physical cash is far more prevalent than in the UK or the United States as the chart below shows.

Share of retail transactions done with cash

a.image2.image-link.image2-1178-946 { padding-bottom: 124.5243128964059%; padding-bottom: min(124.5243128964059%, 1178px); width: 100%; height: 0; } a.image2.image-link.image2-1178-946 img { max-width: 946px; max-height: 1178px; }Source: BIS

One key reason for this need for physical cash is that the IT and telecom infrastructure is not available to access modern electronic payment systems 24/7. And this is one of the key challenges for CBDC to overcome. A CBDC needs to be available 24/7 and cannot experience server outages or downtimes. This means that either there is an enormously robust IT infrastructure available everywhere (which would require billions in infrastructure investments even in the most developed countries), or the CBDC must be transferable and be usable as a method of exchange offline. The current thinking is that CBDC will likely be transferrable offline in limited amounts to enable its use as a method of exchange even in the absence of internet connections.

But here is the rub. If you can transfer it offline, how do you make sure it is a valid transaction? Distributed ledger technologies that are at the heart of all cryptocurrencies are based on the proof of work or the proof of stake concept where a transaction is validated by calculations on computers that proof you are the rightful owner of a coin. If you don’t have a connection to a computer, how do you come up with a proof of work or proof of stake? This is why there will likely be limits to the amount of CBDC that can change hands before a proof of stake will become necessary. If the proof of stake fails, the transactions can be unwound without disrupting the overall payment system too much.

But here is the next difficulty. If you use distributed ledger technology as the foundation of a CBDC, you increase its security because the information about the CBDC and past transactions is stored on many computers and thus less prone to hacks and cyber-attacks. Yet, by distributing the information about the CBDC tokens (or coins) you also reduce the transaction speed. Payment systems that are handled by a central ledger like every credit card system, electronic payment systems, or bank accounts can handle tens of thousands of transactions per second. Bitcoin can handle only a handful. Progress is being made in enabling cryptocurrencies to perform more transactions, but we are nowhere near the number of transactions that need to be made for a currency to act as a universal replacement for physical cash. If you want to create a CBDC that is a universal method of exchange, you need to compromise its safety and thus reduce the trust people have in it as a store of value.

This tension between store of value and medium of exchange is nothing new, by the way. In the days of the gold standard, a central bank could only increase the amount of money in circulation if it had enough gold bullions in its safe. This meant that if cash became scarce (e.g. during a recession or a run on banks), central banks had to increase interest rates to incentivise people to put more gold into its safe so it could issue more cash to the public. This is one of the key reasons why the Great Depression turned out so bad. The moment the economy faced a liquidity crunch, the central bank had to reduce liquidity even more to protect its gold holdings. This is unfortunately something gold fetishists forget all too often. It is only with the introduction of fiat money and the end of the gold standard that we could start to manage recession better and prevent waves of default during every economic downturn. Look at the decline in economic activity and the spike in unemployment during economic downturns in the era of the gold standard and the years since and you will see what we have gained by abandoning it.

The current thinking is that with CBDC it is probably best to err on the side of enabling more transactions rather than making it an incredibly safe store of value. Probably the best way to strike a balance is the use of CBDC that are either based on a centralised ledger or a distributed ledger technology but with a limited number of permissioned participants in the distributed ledger. Most likely such a technology would use commercial banks that are regulated by the central bank as the nodes of a distributed ledger network.

Even so, if you have a generally accepted store of value that can handle many transactions per second, you suddenly run into another problem. If CBDC are proper stores of value like physical cash, they could be used like traditional bank accounts. People could transfer electronic money from their bank accounts into CBDC and store their wealth there. You may say that this surely isn’t a problem, since you can just go to your bank and ask to get all the money in your bank account paid out in cash and your bank teller will readily oblige. That may be true for you and me, but in practice, there are limits to how much physical cash you can hold. First, there are the obvious limits that physical cash takes up space and you need to store it safely (you can also opt to leave it out in the open, but then its characteristic as a store of value may be undermined by its extreme fungibility as other people will help themselves to your stored value). But even if you managed to build a massive safe and hire a couple of security people and armoured vehicles to transport the cash from your bank to your safe, try getting any large amounts paid out to you. Why do you think there are no ETFs backed by physical cash anywhere in the world? In theory, these ETFs would accept people’s electronic money and invest it into physical cash stored in a vault. It’s a remarkably simple concept and in a world of negative interest rates, it can become a profitable investment since the cost of safekeeping for these large amounts is a few basis points compared to the 40 basis points or so people have to pay on bank deposits in the Eurozone, for example.

So, if we accept that in practice, you cannot hold unlimited amounts of physical cash, but with CBDC, it is easily possible to accumulate enormous amounts in a few seconds or minutes, we have to think about how we can limit the amount of CBDC held by any individual. This means limiting the amount of CBDC that can be held in any one electronic wallet. But more than that, it means that central banks or commercial banks have to be able to identify many different electronic wallets that belong to the same owner because otherwise, we would quickly see a virtual run on banks where bank deposits would be raided and moved into CBDC wallets thus creating a universal financial crisis that would make 2008 look like child’s play. But if we want to be able to control how much CBDC any one user can own across many different electronic wallets, we have to be able to identify the owner of each wallet. And this means that CBDC is no longer anonymous, but ownership can be linked to an individual. It’s like having to sign every bill you get in the shop with your name and the shopkeeper notifying the central bank of the new owner of the bill.

Now assume we introduce such an identification mechanism (even if it is anonymised) and combine it with distributed ledger technology. This means that the ownership of every unit of CBDC is not only stored at a computer in the central bank but a copy of it is stored on every computer participating in the network. And if that computer gets hacked, it might not bring down the network, but it will expose ownership of the different CBDC units. To make things even more fun, the GDPR in Europe enshrined a right to be forgotten into law. But a blockchain-based distributed ledger technology doesn’t forget. One of the components that makes it so safe and trustworthy is that it has an eternal memory of all transactions ever made with an electronic coin. But if you ingrain that technology into a CBDC and only one person in the EU buys one of these coins, the GDPR becomes applicable and with it this person’s right to be forgotten. Now you go deal with all the privacy lawyers in the world to sort that one out.

Currently, the only way out of this misery is to rely on centralised ledgers owned by the central bank or use distributed ledgers with only commercial banks permitted as nodes after they have done a proper KYC on their clients. For emerging markets with millions of unbanked people, a distributed ledger technology is probably not feasible anyway due to the required infrastructure. so, in these countries, one would expect a CBDC to be based on one central ledger held by the central bank. But that still means that the central bank can see your identity. The Chinese efforts in developing a CBDC go down this route by allowing every user of the CBDC to control who can see their identity. This way, users of CBDC can remain anonymous with the exception of one counterparty: The People’s Bank of China will always know who each user is. This is necessary to run the ledger but of course, it potentially could prove to be a weak point if a central bank is not independent of the government and may be forced by governments to hand over identifying information about CBDC ownership.

Meanwhile, the ECB has experimented with ‘anonymity vouchers’ that allow users of CBDC to transfer ownership of a limited amount of currency over a limited amount of time without their identity being known to counterparties or the central bank. But the problem here is still that the vouchers themselves have to be monitored and audited, which opens up the possibility to identify the users of these vouchers.

Method of exchange vs. unit of accounting

By now you have probably thrown your hands into the air about the difficulties of CBDC and their prospects of replacing physical cash. But let me throw one more obstacle at you. Physical cash is a natural unit of accounting in a way that most electronic cash is not. If you go to PayPal, for example, and you deposit money on your account, it becomes part of PayPal’s balance sheet. This is fine most of the time, but as I have discussed here, it can become a massive problem if PayPal becomes illiquid or bankrupt. Then, your money becomes part of the insolvency proceedings and you become an unsecured creditor of PayPal. This is not the case with physical cash or central bank-issued electronic money. That stuff has to stay around even if the payment provider goes under. One natural way to roll out a CBDC is for the central bank to issue the currency to commercial banks just like they do at the moment with traditional money (both physical and electronic). These commercial banks then distribute the money through loans, etc. Because of the fractional reserve system, the amount of money distributed across the economy is a multiple of the actual central bank money created in the first place. Because CBDC would be a replacement for physical cash, we have to assume that to roll out the CBDC, the commercial banks would be the distributors. Then, either these commercial banks or third-party firms would develop technologies like payment systems and electronic wallets to enable people to use CBDC as a method of exchange.

But these third-party firms that develop payment systems and electronic wallets can (and will) go bankrupt. And the CBDC has to be still in place after these companies have gone bankrupt. In fact, there has to be an easy mechanism to transfer CBDC from an insolvent payment provider to a solvent one in order to keep the financial system stable and avoid a run on banks.

But to do this, every payment provider needs to have separate accounts for its electronic cash and payments and for the CBDC so that it is straightforward to identify the CBDC if needed. That also means that every payment provider needs to know who owns which CBDC at any given point in time. Et voila, we are back to the privacy issue because now, all of a sudden, every CBDC coin has to be at least linked to a private key and ultimately an owner and that reduces privacy and makes it inferior to physical cash. I can already hear the cryptocurrency fans shouting at me that private keys for a token are anonymous, but these keys are either held in e-wallets or in accounts on crypto exchanges. Next week, I will talk about the security risks associated with these storage systems and why they may not be as anonymous as many people think.

If all of this feels like we are going in circles it’s because we are. The latest thinking is that CBDC will be less private than physical cash and that with the ownership of a CBDC coin will come an anonymised identifier of current ownership. This way, it is possible to track who owns the coins without identifying the person by name. Only once the person demands access to the CBDC can he or she show the identifier and proof of ownership. Nevertheless, the translation mechanism between the anonymous identifier and the name of the owner can be hacked and provides another security risk. But this is where we stop this week in order to pick it up next week to discuss the myriads of IT security issues with CBDC.

Categorías: Blogs y opiniones de economia en ingles

10 Reasons Why Stocks Fall

“It’s hard to hold onto stocks for a long period of time.”

Carl Kawaja said this in an excellent conversation with Patrick O’Shaughnessy.

This made me decide to revisit a post I did a few years back, Looking For the Next Amazon.

Amazon is one of the best-performing stocks ever, but it hasn’t been the easiest stock to hold over the last year. It’s up 6%, while the Nasdaq-100 is up almost...

The post 10 Reasons Why Stocks Fall appeared first on The Irrelevant Investor.

Categorías: Blogs y opiniones de economia en ingles

Why Britain must shelter Afghan journalists

They helped Western media inform the world about the country. Now they need protection from brutal retribution by the Taliban

Categorías: 3 Noticias economicas ingles

Una recuperación laboral incompleta

El Gobierno tiene que alejarse de los mensajes triunfalistas en un momento de incertidumbres. Leer

Categorías: 1 Noticias economicas en español

¿Es legal pedir datos médicos para poder alojarse en un hotel?

Categorías: 1 Noticias economicas en español

Simple Wealth, Inevitable Wealth - Nick Murray

{kind=link}

simple wealth inevitable de nick murray, Antiguo o usado - Iberlibro-ats--used

Aquí les traigo el que para mí es el mejor libro para introducirse en la inversión. De hecho, debo decir que marcó un antes y un después en mi etapa inversora.

Si alguno ha leído algún libro de N.N. Taleb, pensad que Nick Murray es la antítesis de Taleb en lo que a escritura refiere. Es un estilo de escritura muy sencillo, que no simple, bien estructurado, y en un lenguaje entendible.

El libro es un libro que es básico. Cualquier persona que tenga un conocimiento mínimo sobre inversiones utilizará adjetivos del tipo “demasiado simple”, “esto no es completamente cierto”, “puede mejorar”.

El objetivo del libro es introducir a la inversión a cualquier persona, de cualquier edad, en el ámbito de la inversión. Creo que es un libro que expone, perfectamente bien, por qué preferir las acciones a los bonos y cómo formar una buena cartera de fondos.

Es un libro que considero que hay que leer una vez al año, por cuanto forma no solo a nivel financiero sino también a nivel psicológico, a fin de preparar al inversor sobre ciertos vaivenes que se producen en el futuro.

En lo que a longitud respecta, son menos de 200 páginas, y se lee muy rápido; calculen menos de 2 horas de lectura.

Es el libro sobre el que he edificado mis fundamentos serios de inversión; y lo recomiendo a todos: a los que se inician como lectura primera y necesaria; a los que llevan tiempo en el camino como “divertimento”.

Es un libro que en Europa “vuela por debajo del radar”, en EEUU es más conocido. En una palabra: una perla.

1 publicación - 1 participante

Alibaba no cumple con las previsiones tras ganar un 5% menos en su primer trimestre fiscal

Categorías: 1 Noticias economicas en español

Conectarse desde la playa... ¿le convierte en un teletrabajador más productivo?

Categorías: 1 Noticias economicas en español

My Investing Nightmare

Recently a friend asked me:

What keeps you up at night financially? What is your version of an investing nightmare?

Fortunately, I don’t have anything that keeps me up at night (I tend to be an optimist), but if I had to describe my investing nightmare, it wouldn’t be something we haven’t seen in recent decades. In fact, I’d argue we haven’t seen it within the last 100 years of U.S. market hi...

The post My Investing Nightmare appeared first on Of Dollars And Data.

Semana de emociones

Los bancos españoles se han enfrentado en estos días a tres circunstancias de la mayor importancia y que tienen un cierto grado de interconexión entre ellas, como son la publicación de sus resultados del primer semestre y la de los hipotéticos impactos del test de estrés que ha realizado la Autoridad Bancaria Europea (EBA). Además, está la decisión del BCE respecto al pago de dividendos. Leer

Categorías: 1 Noticias economicas en español

Need Help! Issue on Willemin 408b

Hello,

I work on Willemin 408b. And yesterday I had an issue on it.

There is no problem when I start the spindle with M3 S1000. However when I want to stop her with M5. The spindle doesn't stop and this alarm appears : 1301 Time-out start/stop spindle.

But when I start the spindle with M4 there is no problem to stop her with M5.

Do you have an answer for this problem ?

Thank you.

I work on Willemin 408b. And yesterday I had an issue on it.

There is no problem when I start the spindle with M3 S1000. However when I want to stop her with M5. The spindle doesn't stop and this alarm appears : 1301 Time-out start/stop spindle.

But when I start the spindle with M4 there is no problem to stop her with M5.

Do you have an answer for this problem ?

Thank you.

Categorías: Modelismo y CNC en ingles

No deberíamos ser demasiado optimistas sobre una población que se reduce

La caída de las tasas de natalidad es una buena noticia para el planeta, pero también es un síntoma de la desigualdad generacional. Leer

Categorías: 1 Noticias economicas en español

La Justicia condena a las aseguradoras a cubrir las pérdidas del confinamiento

Eso sí, no todos los seguros multirriesgo cubren este tipo de contingencias. Es necesario que contemplen una cláusula de cobertura de riesgos. “Aún así, las aseguradoras alegan que la pandemia fue un riesgo imprevisto, una especie de catástrofe natural que no deben de cubrir; la Justicia no lo entiende así y les ha condenado a pagar”, explica Navas.

El experto recomienda a todos los comercios y restaurantes afectados que exploren en sus contratos de seguro esta posibilidad. “Para muchos puede ser la única oportunidad para mantener en pie sus negocios, el servicio al público y el empleo”, concluye el socio-director de navascusi.com

Categorías: 1 Noticias economicas en español

Páginas

Custom Search